Apple missed earnings estimates for the first time in seven years or the last 28 quarterly earnings reports. Weighing on Apple earnings was a 5.5% year-over-year decline in sales led by a 29% decline in Mac sales and an 8% fall in iPhone sales. Earnings per share at Apple were $1.88 vs. $1.94, as expected. Despite the surprisingly poor earnings, Apple shares were up on the day. Investors are taking solace in Chief Executive Tim Cook’s statement that weak sales are transitory. According to Cook, they were hampered by supply constraints due to China’s various pandemic lockdowns late last year. Apple anticipates recapturing a portion of those lost sales and provided investors with positive forward guidance.

Apple wasn’t the only mega-cap company with shaky earnings. Amazon posted its biggest loss ever on its least profitable holiday quarter since 2014. Unlike Apple, Amazon’s revenue increased versus a year ago and did exceed expectations. Concerning investors, however, is a significant slowdown in AWS revenue. AWS represented about two-thirds of its operating profit in recent years. Google reported EPS of $1.05 per share, compared to $1.53 last year despite slightly higher revenue. Per Google’s Chief Business Officer:

“A pullback in spending by advertisers amid a more challenging economy and foreign exchange headwinds impacted sales.”

What To Watch Today

Economy

- No notable reports are scheduled for release.

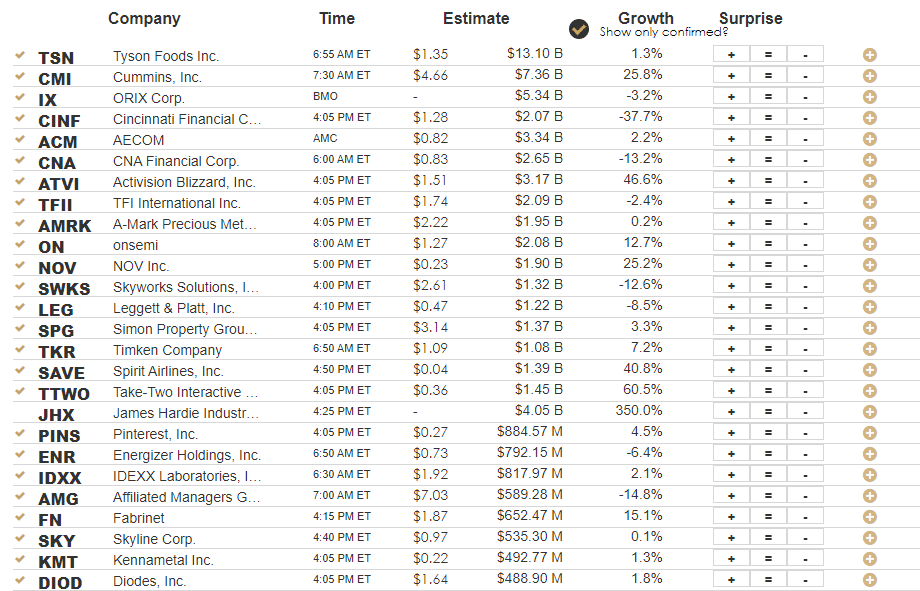

Earnings

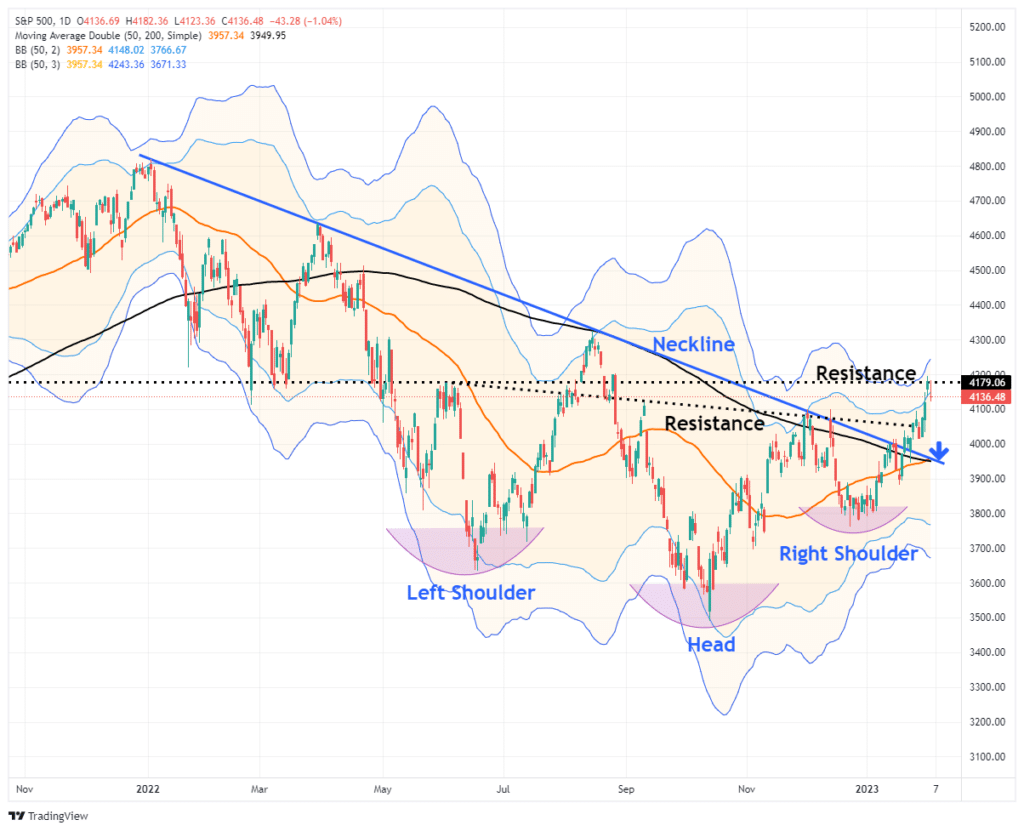

Market Trading Update

Last week’s message asked the question of whether the market’s break above the long-running downtrend line was a “head fake?” To wit:

As we noted, the inverse ‘head-and-shoulder’ pattern already suggests a market bottom has formed. A solid break above the downtrend line (with a successful retest) would confirm the completion of that pattern. Notably, the 50-DMA is rapidly closing in on a cross above the declining 200-DMA. Such is known as the ‘golden cross’ and historically signifies a more bullish setup for markets moving forward.

The market surge continued last week but ran into resistance on Friday as markets are pushing well into 3-standard deviations above the 50-DMA. However, while the weakness on Friday was not unexpected, it is also necessary to determine whether the current breakout is legitimate.

If the “bear market” is “canceled,” we will know relatively soon. To confirm whether the breakout is sustainable, thereby canceling the bear market, a pullback to the previous downtrend line that holds is crucial. Such a pullback would accomplish several things, from working off the overbought conditions, turning previous resistance into support, and reloading market shorts to support a move higher. The final piece of the puzzle, if the pullback to support holds, will be a break above the highs of this past week, confirming the next leg higher. Such would put 4300-4400 as a target in place.

A break BELOW the downtrend line, and the current intersection of the 50- and 200-DMA, will suggest the breakout was indeed a “head fake.” Such will confirm the bear market remains, and a retest of last year’s lows is likely.

Given that we don’t know with certainty where the market is headed next, we are remaining underweight equities at the moment and increased cash levels a bit last week due to the overbought conditions of the market. If the market confirms the “cancelation” of the bear cycle, we will aggressively add risk for the next leg higher. If not, we will add to bonds and reduce equity risk further for the next leg lower.

We will have to wait and see what happens now that “J-Pow threw in the towel.”

The Week Ahead

With the big slate of earnings last week behind us, the earnings calendar slows markedly this week. Economic data will also be limited following last week’s employment barrage. This week, we will continue to follow unemployment claims and continuing claims for any signs that labor markets are weakening. The University of Michigan Consumer Survey will shed light on consumer sentiment and their inflation expectations. The Fed is pleased that inflation expectations have moderated over the last few months.

With little earnings and economic data, the likely source for fireworks this week will be the Fed. Jerome Powell will speak on Tuesday, and we expect a slew of other Fed speakers to opine on the Fed’s last meeting and what they think the Fed will do in the coming year. We wonder if Friday’s job data may push some Fed members to take on a more hawkish tone.

BLS Employment Report and Its Flaws

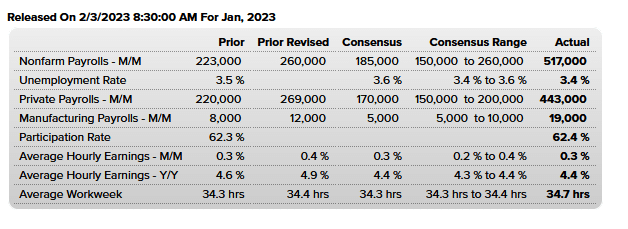

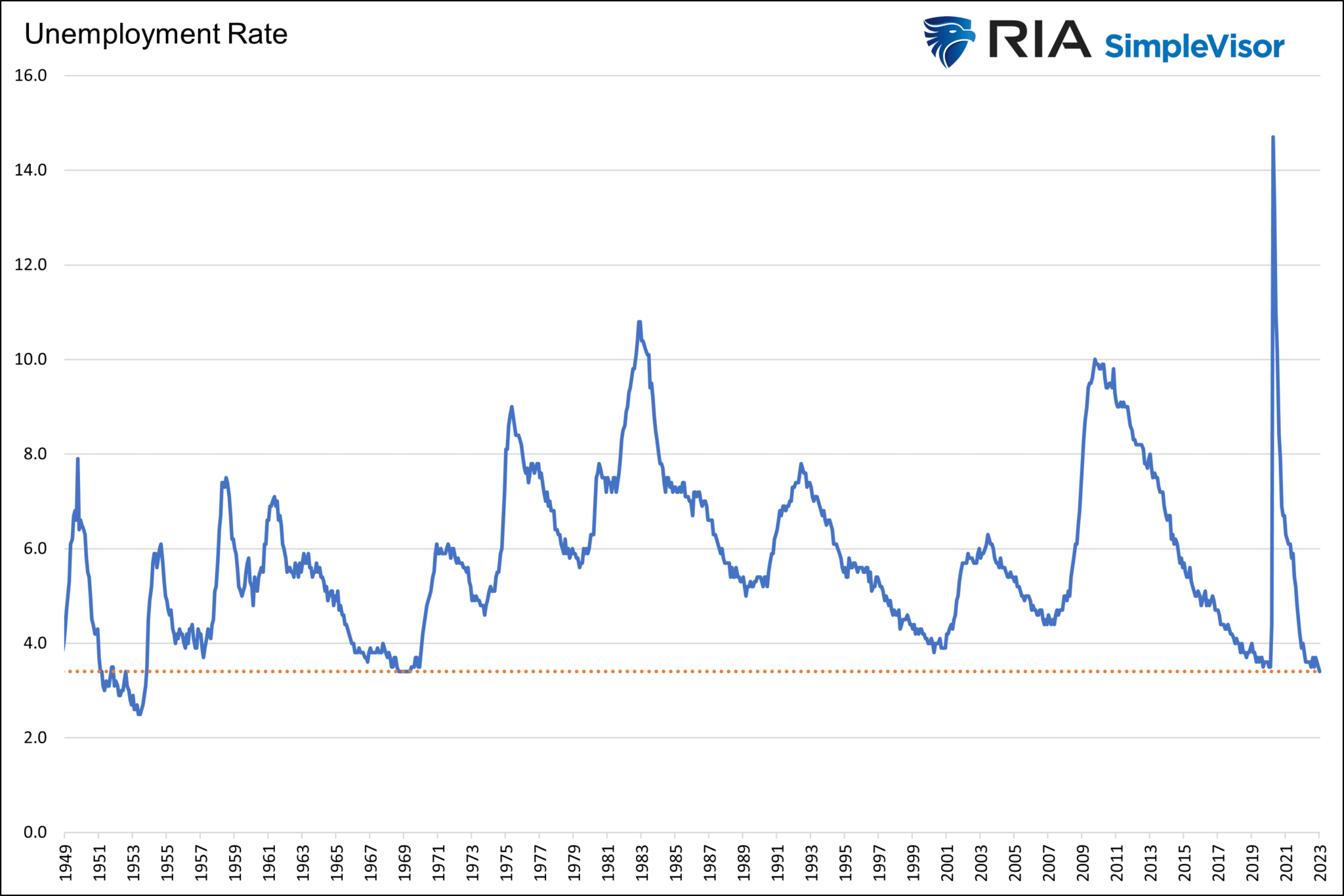

The unemployment rate fell to 3.4%, the lowest since 1969. You have to go back to 1954 to find a lower unemployment rate! It fell in large part due a shocking 517k increase in payrolls. Further, the BLS revised November and December upward by a combined 71k jobs. Expectations for January job growth was only 185k. Also, of note, average hourly earnings rose by 0.3%, in line with expectations. However, the average workweek increased from 34.3 to 34.7 hours. This figure may concern the Fed, as they worry a tight labor market could trigger a price-wage spiral. Typically, companies reduce hours and wages before laying off employees. The pick-up in hours, the robust employment data in Friday’s report, and other employment data we covered in Friday’s Commentary should bolster the Fed’s belief that the labor market remains hot.

January is also the month the BLS makes revisions to the prior year. Per the BLS, the population increased by 954k, and the size of the labor force increased by 871k. The BLS also increased March 2022 employment by 568k. The BLS will not publish revisions for the remainder of 2022 until 2024.

Corporate Earnings Overview

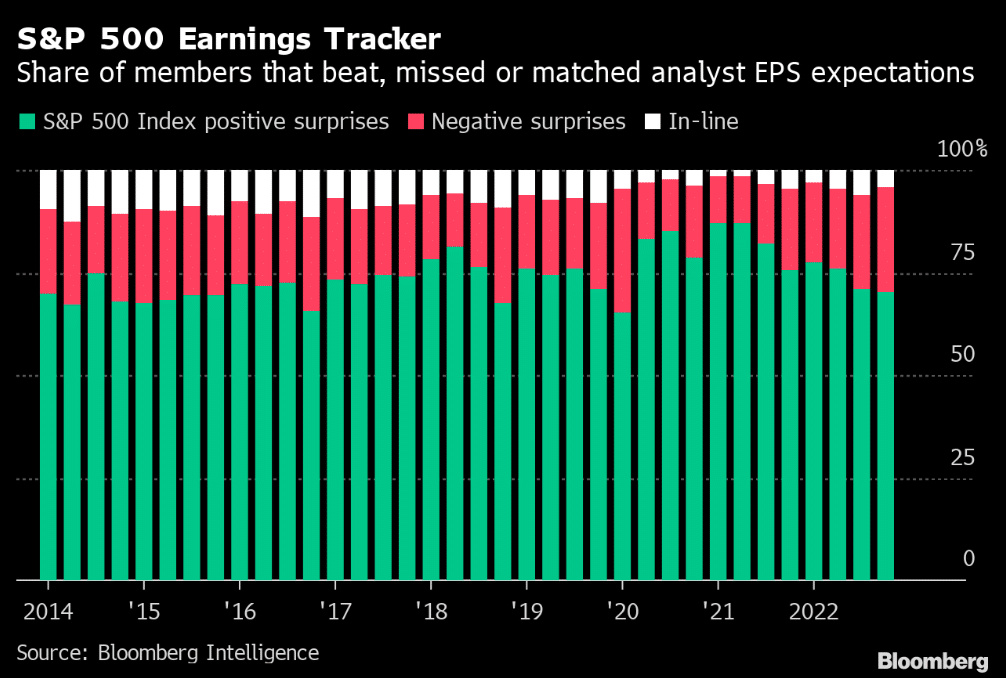

Looking beyond Apple, Amazon, and Google, Bloomberg finds that the prior quarter’s earnings were among the weakest in the last ten years. Excluding 2020, a greater share of S&P 500 companies missed analyst EPS expectations. Similarly, positive earnings surprises, as a share of companies, is among the lowest in the last ten years. The second graph shows that the margin in which companies beat revenue and earnings expectations is the smallest in at least two years.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.