Market pullback or bear market? Such seems to be the question on everyone’s mind as of late, given the rough start to 2022 so far.

There are undoubtedly many issues confronting even the most optimistic of investors currently.

- Geopolitical risk from Russia and the threat to the Ukraine

- Rising interest rates

- Surging inflationary pressures

- Economic growth slowing

- Profit margins under pressure

- Reversal of monetary liqudity

- Tighter monetary policy from the Federal Reserve

- Surging oil prices

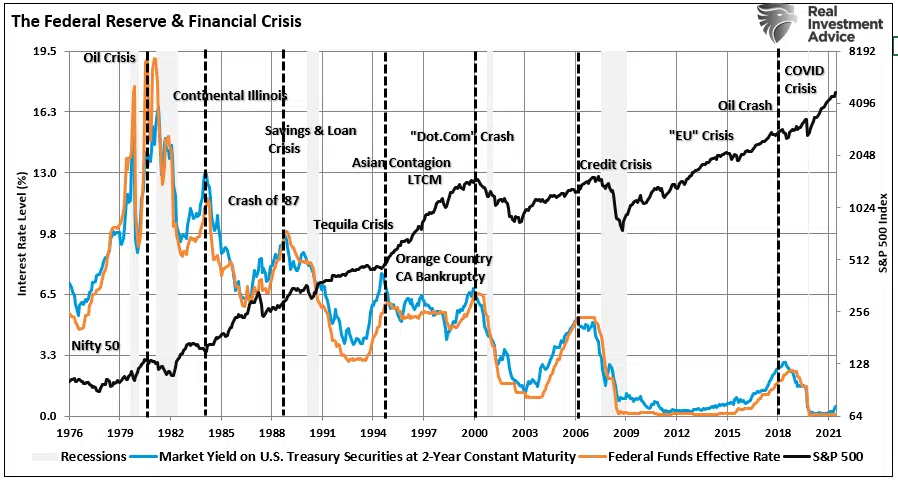

There are certainly others, but you get the idea. The many tailwinds that supported the rapid rise in the markets from 2020 to the present have started to reverse. As shown, the roughly 120% advance from the March lows should not be surprising given the massive liquidity surge from the Government.

Also, not surprisingly, is the subsequent surge in inflation. As Milton Friedman stated:

“Inflation is always and everywhere a monetary phenomenon. It is always and everywhere a result of too much money, of a more rapid increase of money, than of output.”

Friedman’s point is essential. Inflation is always a function of the Government printing too much money. In this case, the result of $5 trillion directly injected into the economy, inflation should be no surprise.

Now, the financial markets are starting to reflect the risk of a more aggressive Fed working to reverse that artificial surge in liquidity.

But, as discussed in “This Time Is Different,” therein lies the risk of a policy mistake.

Predictions Are Difficult

“Prediction is very difficult, especially about the future.” – Neils Bohr

As discussed much recently, the hope is that the Fed can navigate tightening monetary policy and increasing interest rates without creating “financial instability.” Unfortunately, their track record remains unimpressive.

While the weight of evidence suggests that the bears are gaining control of the financial landscape, outcomes are not guaranteed. As investors, betting on “predictions” can often have unintended consequences as market dynamics change.

Therefore, we must be aware of the risks and navigate markets accordingly. As noted in this past weekend’s newsletter:

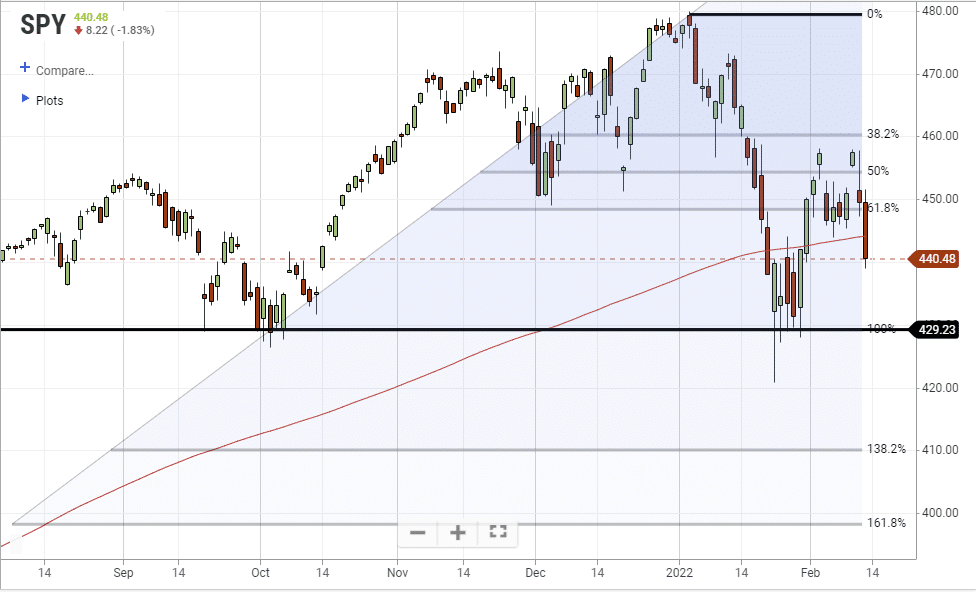

“Another nauseating week in the market as a hotter than expected inflation print and rumors of a Russian invasion of Ukraine sent stocks tumbling backward. The bad news is that support at the 200-dma failed.”

While the break of the 200-dma is notable, we also broke that level in January. Had you sold that break of support, you missed the reflexive rally back to the 50-dma. Such was the point we made in the “heat of the moment:”

“The ‘good news,’ if you want to call it that, and as noted by Zerohedge, is there is now a good bit of ‘combustible fuel’ to create a counter-trend rally heading into the Fed meeting next week.

All this means is that investors are now all on ‘one side of the boat,’ which is a prime setup for a counter-trend bounce. However, it is likely a bounce you will want to use to ‘derisk’ your portfolio.“

The message of “derisking on the rally” has been consistent for the last couple of weeks.

Notably, other than the decline from extreme overbought conditions, so far, the market has not violated important support or bullish trends.

In other words, so far, we are simply working through a market pullback.

Market Pullbacks Can Become Bear Markets

Such is a crucial point. We noted several times in 2021 that extremely “low volatility” would lead to “higher volatility.” To wit:

“A retest of the 200-dma should not be dismissed which is roughly 11% lower. While such a decline is well within the norms of a correction in any given market year, the low levels of volatility will make it ‘feel’ worse than it is.“

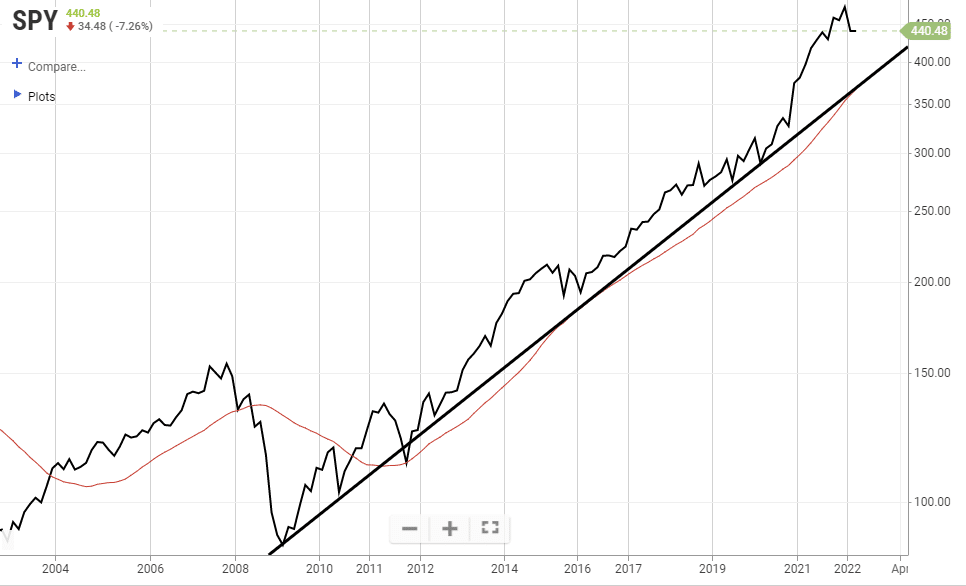

So far, that is what has happened. After a long period of only 5% drawdowns, the 10% market pullback in January “felt” like a crash. However, if we go back to 2009 and draw a trendline along the 24-week moving average, we see the recent correction has done little to violate that bullish trend.

It is worth noting the massive advance of the market from the 2009 lows was a function of more than $43 trillion injected into the economy by the Government and Federal Reserve. With inflation now surging and the Fed trapped into a rate hiking cycle, there is a risk a market pullback could morph into a bear market.

All that is needed is a catalyst to change the bullish psychology.

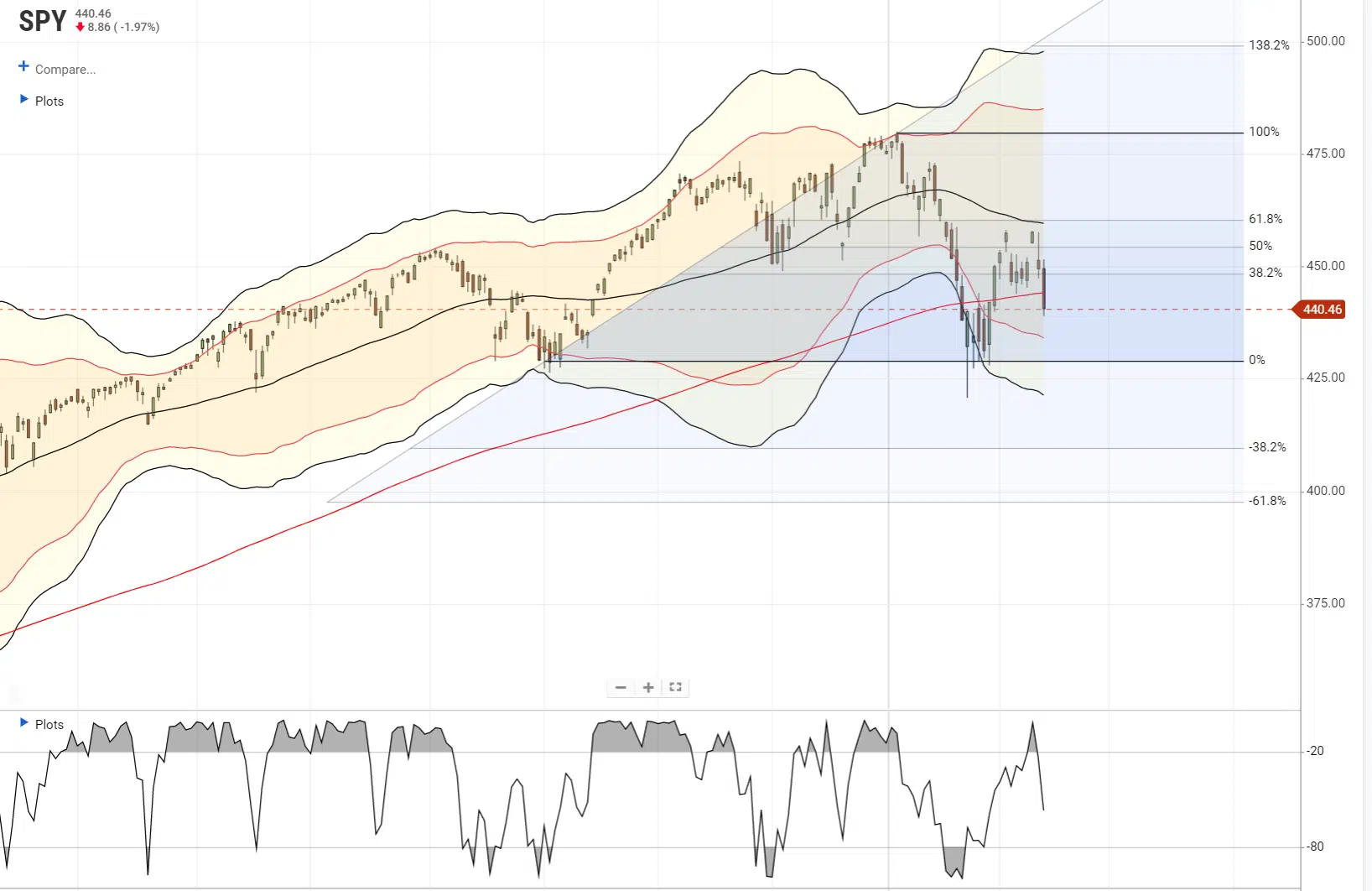

Currently, the risk to investors is a market pullback to October lows. A failure of that support would suggest a deeper correction to the 138.2% and 161.8% Fibonacci retracement levels. Such levels would approach a 20% decline.

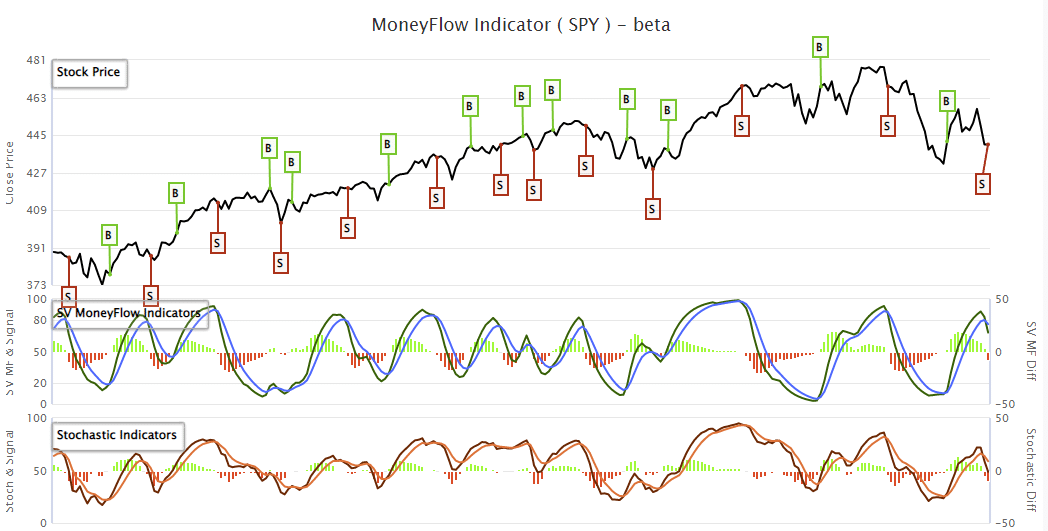

There is sufficient “fuel” for that deeper correction given the current overbought condition of the SimpleVisor money flow indicator, which has registered a sell signal.

Does this mean a “bear market” is inevitable? No.

Does it mean you should sell everything and go to cash? No.

It does mean you should at least be aware, and prepare for, the potential risk.

Navigating Whatever This Is

With that in mind, my job as a portfolio manager is to navigate market risks as we see them. Making a “one-sided” bet on a potential outcome harbors an outsized risk of being wrong. Such would potentially impact client capital and damage financial outcomes.

Therefore, we approach risk management in the market by choosing to hedge risk and reduce potential liabilities. As such, given the market’s current structure, we have three options currently:

- Do Nothing – if the markets correct, we lose destroy capital and time waiting for the portfolio to recover.

- Take Profits – This has been our choice on the recent reflexive rally. Taking profits, raising cash, and reducing equity exposure in advance of a correction mitigates the damage of a decline. However, if wrong, we can repurchase positions, add new ones, or resize portfolio holdings as needed.

- Hedge – We have also opted to hedge by adding a position to the portfolio that is the “inverse” of the market. Such allows us to keep existing positions intact. By “shorting against the portfolio,” we effectively reduce our equity risk (and related capital destruction) during a market correction.

As noted, we have opted to use a combination of both #2 and #3. Doing nothing leaves us too exposed to an unexpected “volatility shock” in the market or the reversal of bullish psychology.

While we are reducing capital risk opportunistically, we are very aware we could give up performance in the short term if the market rallies. For us, that is a choice we can live with if we potentially bypass the risk of a more significant correction.

In our view, we have a choice to either manage risk or ignore it.

The only problem with “ignoring risk” is that such has a long history of not working out well.

Investment Guidelines

When it comes to investing, we tend to repeat our mistakes by forgetting the past. Therefore, it is worth repeating investing guidelines to bring your focus back to what truly matters.

- Investing is not a competition. There are no prizes for winning but severe penalties for losing.

- Emotions have no place in investing.You are generally better off doing the opposite of what you “feel.”

- The ONLY investments that you can “buy and hold” are those providing an income stream and return of principal.

- Market valuations are very poor market timing devices.

- Fundamentals and Economics drive long-term investment decisions – “Greed and Fear” drive short-term trading.

- “Market timing” is impossible– managing exposure to risk is both logical and possible.

- Investment is about discipline and patience. Lacking either one can be destructive to your investment goals.

- There is no value in daily media commentary– turn off the television and save yourself the mental capital.

- Investing is no different than gambling– both are “guesses” about future outcomes based on probabilities. The winner is the one who knows when to “fold” and when to go “all in”.

- No investment strategy works all the time. The trick is knowing the difference between a bad investment strategy and one that is temporarily out of favor.

“The investor’s chief problem – and even his worst enemy – is likely to be himself.” – Benjamin Graham.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read