Is a “lost decade” ahead for markets? Stanly Druckenmiller believes that could be the case.

“There’s a high probability in my mind that the market, at best, is going to be kind of flat for 10 years, sort of like this ’66 to ’82 time period.”

Druckenmiller added that with inflation raging, central banks raising rates, deglobalization taking hold, and the war in Ukraine dragging on, he believes the odds of a global recession are now the highest in decades. He pointed out that globalization has a “deflationary” effect because it increases worker productivity and speeds up technological advancement. However, that tailwind is now fading. To wit:

“When I look back at the bull market that we’ve had in financial assets really starting in 1982. All the factors that created that boom not only have stopped, they’ve reversed.”

But Druckenmiller isn’t alone in his views. Gerard Minack also suggests the idea of a “beta drought.” Like Druckenmiller, Minack believes the U.S. is entering a long period of low to negative asset returns for an extended period.

“Prior droughts have been due to rising inflation and/or high market valuation. The US is now at risk from both.

US investors have enjoyed munificent beta for a dozen years: a 60:40 equity/bond portfolio generated a 10½% annual average return between March 2009 and January 2022. But there have been four beta droughts since 1900: extended periods of little or no beta return. Three of the four historical beta droughts – in the 1910s, 1940s and 1970s – were caused by rising inflation, typically decade-average CPI inflation of over 5%. Those three inflation episodes were associated with WW1, WW2, and the 1970s oil shocks. The 2010s beta drought was due to excess equity valuation (like we have seen recently.) The US may now be entering another beta drought. US returns are at now risk from both the prospect of higher inflation, AND the headwind to returns from high starting-point valuations.”

Are Druckenmiller and Minack correct? Should investors be expecting another lost decade?

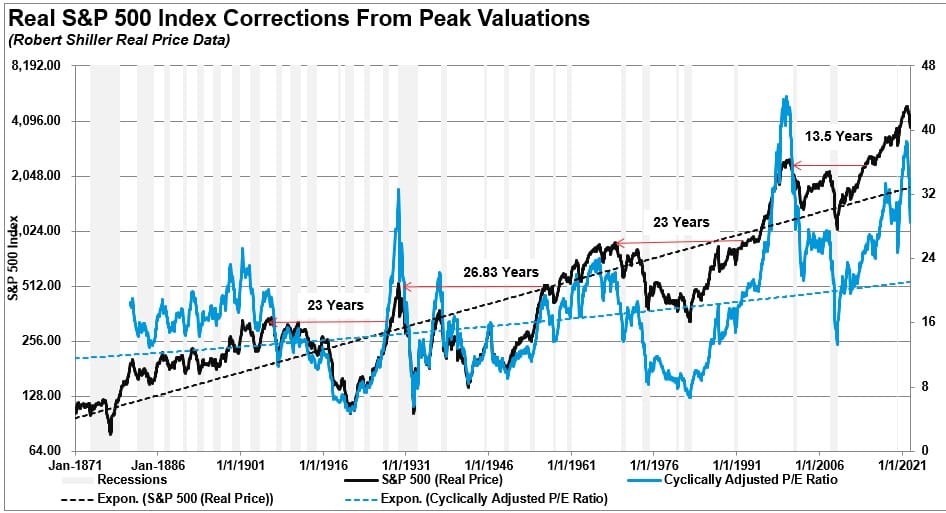

The Value Of Valuations

There is much to both Druckenmiller’s and Minack’s views. Over the last 120 years, valuations have consistently proved to be a strong predictor of future returns, with lost decades common. However, as we discussed previously in “Rationalizing High Valuations:”

“The mistake investors repeatedly make is dismissing the data in the short-term because there is no immediate impact on price returns. Valuations by their very nature are HORRIBLE predictors of 12-month returns. Investors avoid any investment strategy which has such a focus. In the longer term, however, valuations are strong predictors of expected returns.”

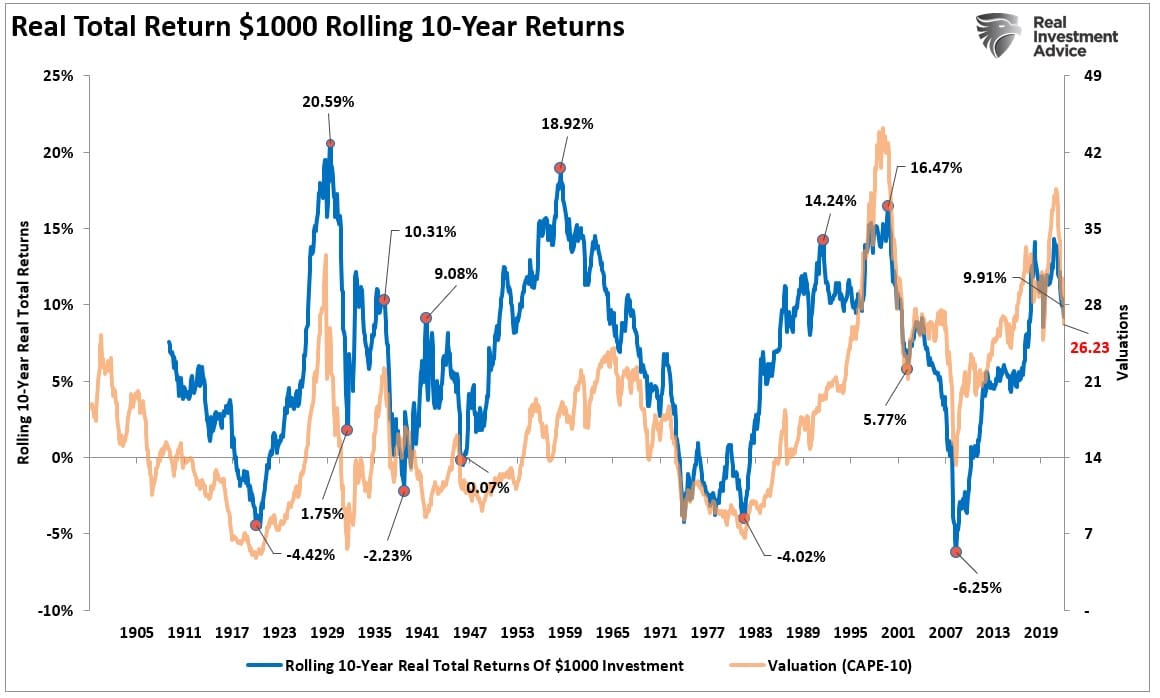

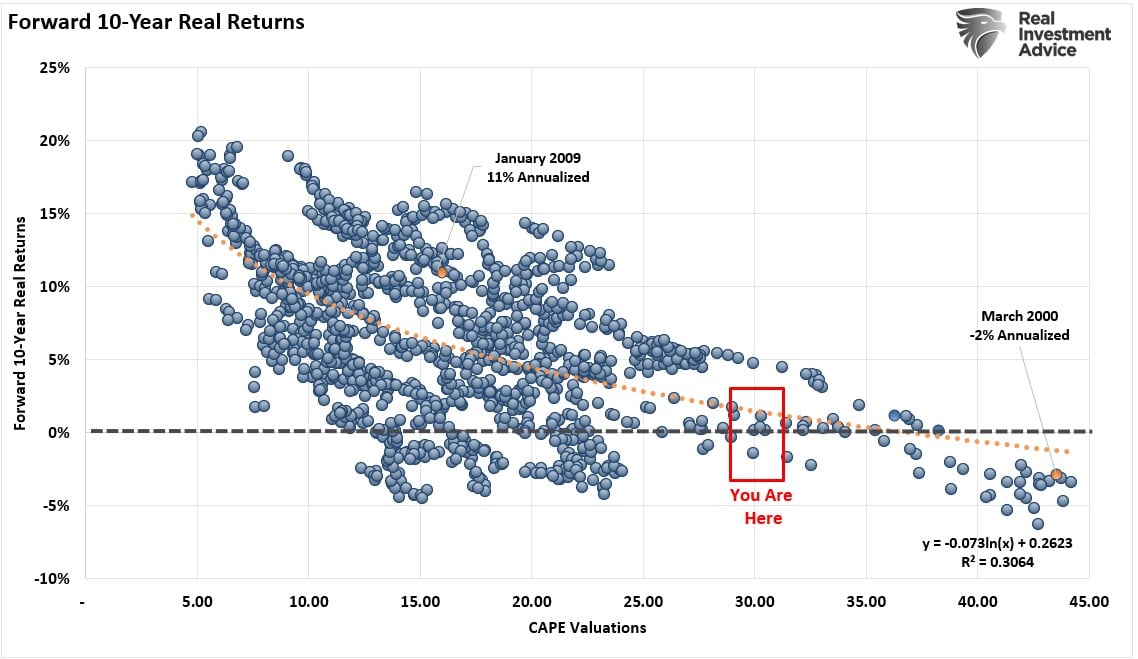

The chart below shows valuations and rolling 10-year total real returns. The obvious conclusion is that overpaying for value leads to lost decades.

The chart below shows this more clearly. I highlighted the three most recent points for reference.

- The “Dot.com” bubble peak.

- January 2009 (Start of the current bull market cycle)

- Ending valuation for 2021.

There are two crucial points to take away from the data.

- There are several periods throughout history where market returns were not only low but negative. (Given that most people only have 20-30 functional years to save for retirement, a 20-year low return period can devastate those plans.)

- Periods of low returns follow periods of excessive market valuations and encompass the most negative return years.

The problem going forward, as Druckenmiller notes, is the reversal of globalization and financial inputs that increased annualized return rates over the last decade.

An Artificial Support

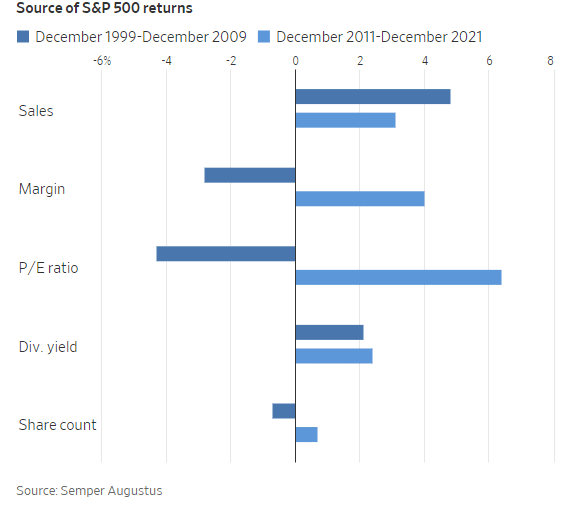

The Wall Street Journal previously discussed the last decade’s stellar returns.

“Investors’ optimism is easier to understand if one looks at the 10 years through the end of 2021, during which the compound annual return of the benchmark S&P 500 was a very good 16.6%. Not so far from what those surveyed extrapolated. Its components need closer scrutiny, though.”

While the Wall Street Journal then tries to make the case that profit margins were responsible for the gains, the reality is that most excess returns came from just two unique sources.

- A decade of monetary interventions and zero interest rate policies; and,

- A massive spending spree by corporations on share repurchases.

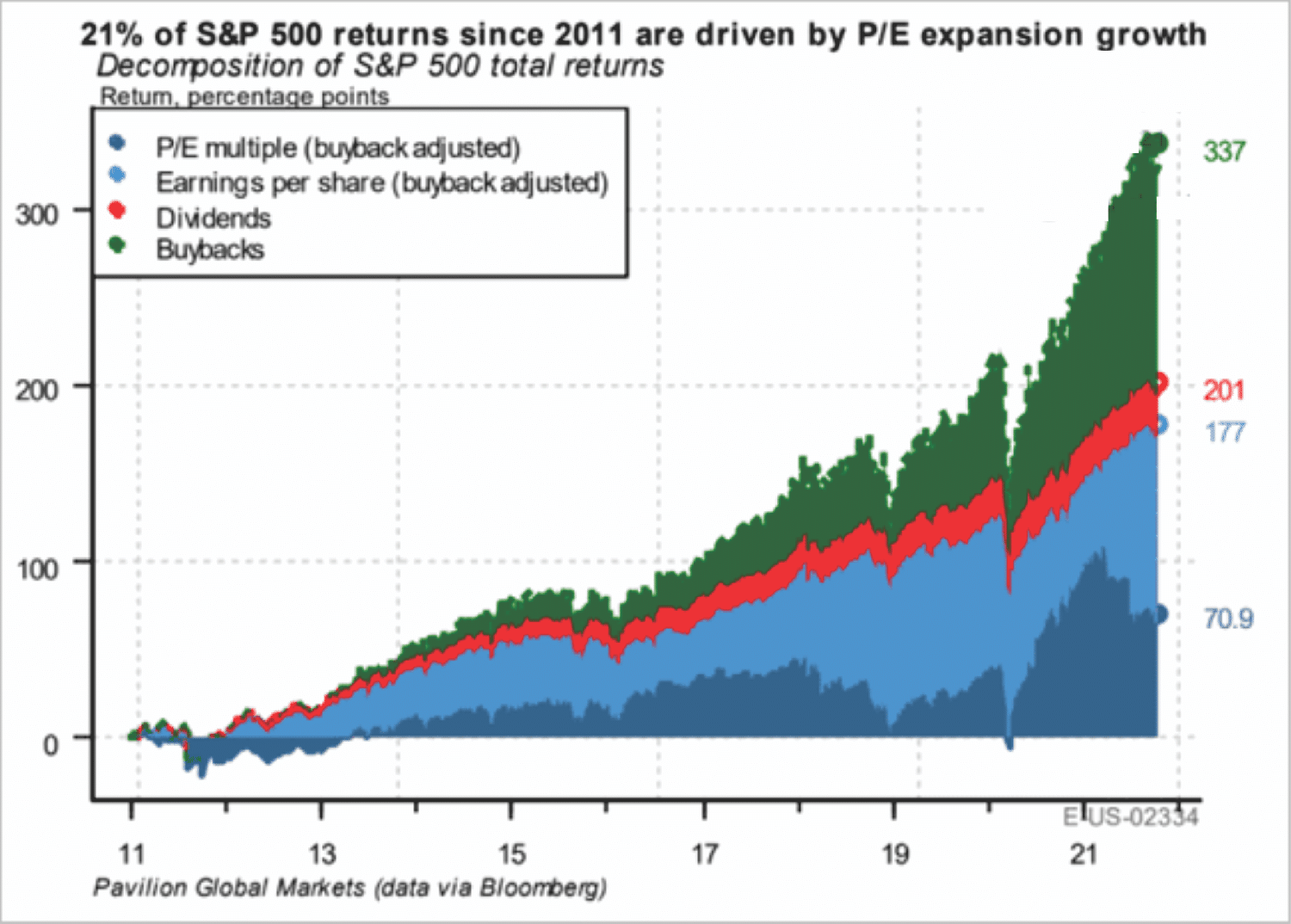

The chart below via Pavilion Global Markets shows the impact of stock buybacks on the market over the last decade. The decomposition of returns for the S&P 500 breaks down as follows:

- 21% from multiple expansions,

- 31.4% from earnings,

- 7.1% from dividends, and

- 40.5% from share buybacks.

In other words, in the absence of share repurchases, the stock market would not be pushing record highs of 4800 but instead levels closer to 2800.

Such would mean that stocks returned a total of about 3% annually or 42% in total over those 14 years.

The combined impact of trillions in share repurchases, over $43 Trillion in liquidity injections by the Federal Reserve, and zero interest rates led to those outsized returns.

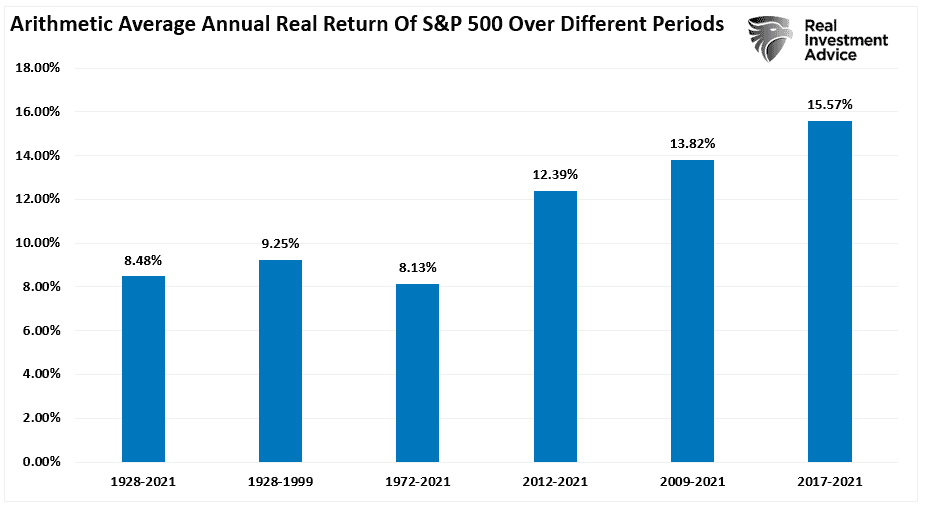

The chart below shows the average annual inflation-adjusted total returns (dividends included) since 1928. I used the total return data from Aswath Damodaran, a Stern School of Business professor at New York University. The chart shows that from 1928 to 2021, the market returned 8.48% after inflation. However, notice that after the financial crisis in 2008, returns jumped by an average of four percentage points for various periods.

After more than a decade, many investors have become complacent in expecting elevated rates of return from the financial markets. The question is whether those artificial influences can be, or will be, sustained for another decade.

From Inflation To Deflation – The Reversal Of Growth

Capital gains from markets are primarily a function of market capitalization, nominal economic growth, plus dividend yield. Using John Hussman’s formula, we can mathematically calculate returns over the next 10-year period as follows:

(1+nominal GDP growth)*(normal market cap to GDP ratio / actual market cap to GDP ratio)^(1/10)-1

Therefore, IF we assume that GDP could maintain 2% annualized growth in the future, with no recessions, AND IF current market cap/GDP stays flat at 1.25, AND IF the dividend yield remains at roughly 2%, we get forward returns of:

(1.02)*(1.2/1.5)^(1/10)-1+.02 = 1.75%

But there are a “whole lotta ifs” in that assumption. Most importantly, we must also assume the Fed can keep inflation at its 2% target, which would mean a real rate of return of -0.25%.

In either case, these numbers are well below most financial plan projections, leaving retirees well short of their expected retirement goals.

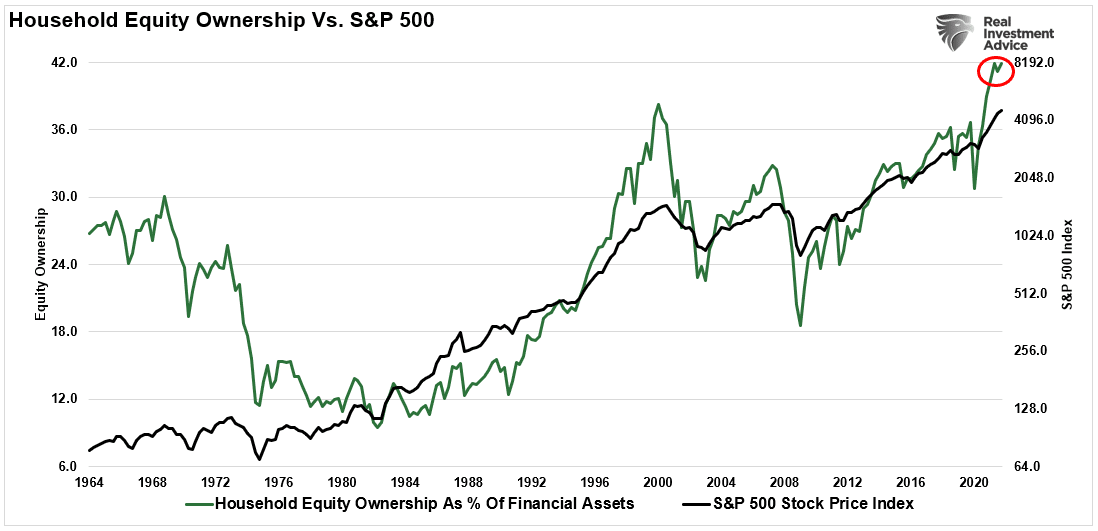

Such is particularly problematic given the current levels of household equity ownership. If Druckenmiller is correct, and a reversal of globalization takes hold, the reduction in valuations as the “everything bubble” is reversed will be quite detrimental.

Earlier this year, Jeremy Grantham made headlines with his market outlook titled “Let The Wild Rumpus Begin.” The crux of the article gets summed up in the following paragraph.

“All 2-sigma equity bubbles in developed countries have broken back to trend. But before they did, a handful went on to become superbubbles of 3-sigma or greater: in the U.S. in 1929 and 2000 and in Japan in 1989. There were also superbubbles in housing in the U.S. in 2006 and Japan in 1989. All five of these superbubbles corrected all the way back to trend with much greater and longer pain than average.

Today in the U.S. we are in the fourth superbubble of the last hundred years.”

As noted above, the deviation from long-term growth trends is unsustainable. Therefore, unless the Federal Reverse is committed to a never-ending program of zero interest rates and quantitative easing, the eventual reversion of returns to their long-term means is inevitable.

Such will solely result in profit margins and earnings returning to levels that align with actual economic activity. As Jeremy Grantham once noted:

“Profit margins are probably the most mean-reverting series in finance. And if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system, and it is not functioning properly.” – Jeremy Grantham

Many things can go wrong in the months ahead.

While investors cling to the “hope” the Fed has everything under control, there is a reasonable chance they don’t.

The next decade could be a disappointment to overly optimistic expectations.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read