Is it possible the Fed over-reacted to a natural disaster?

There are two different types of “recessionary” events that occur throughout history. The first is a “business cycle” recession, which happens with some regularity as excesses build up in the economy. These cycles generally take 12-18 months to complete as those excesses are reversed.

Then there are “event-driven” recessions that can occur from “natural disasters.” These are generally much shorter in duration and can be sector specific. One such event was the Japanese earthquake/tsunami in 2011, which led to a temporary manufacturing recession.

Understanding the type of recessionary cycle you are fighting is essential in ensuring the Government applies the correct monetary and fiscal response. As with any illness, the application of the wrong medication can lead to unintended consequences.

There are growing expectations of the COVID-19 economic shutdown, and the subsequent recessionary backlash will be very short-lived. The assumption is that if the economy reopens, the activity will resume, and the economy will quickly regain its footing.

If such an outcome is indeed the case, has the Fed applied the wrong “medication” to cure the economic patient?

Monetary Medicine

As I addressed in “Is The Debt Chasm, Too Big For The Fed To Fill.”

“Over the last month, the Federal Reserve, and the Government, have unleashed a torrent of liquidity into the U.S. markets to offset a credit crisis of historic proportions. A list of programs already implemented has already surpassed all programs during the ‘Financial Crisis.'”

- 03/06 – $8.3 billion “emergency spending” package.

- 03/12 – Federal Reserve supplies $1.5 trillion in liquidity.

- 03/13 – President Trump pledges to reprieve student loan interest payments

- 03/13 – President Trump declares a “National Emergency” freeing up $50 billion in funds.

- 03/15 – Federal Reserve cuts rates to zero and launches $700 billion in “Q.E.”

- 03/17 – Fed launches the Primary Dealer Credit Facility to buy corporate bonds.

- 03/18 – Fed creates the Money Market Mutual Fund Liquidity Facility

- 03/18 – President Trump signs “coronavirus” relief plan to expand paid leave ($100 billion)

- 03/20 – President Trump invokes the Defense Production Act.

- 03/23 – Fed pledges “Unlimited QE” of Treasury, Mortgage, and Corporate Bonds.

- 03/23 – Fed launches two Corporate Credit Facilities:

- A Primary Market Facility (Issuance of new 4-year bonds for businesses.)

- A Secondary Market Facility (Purchase of corporate bonds and corporate bond ETFs)

- 03/23 – Fed starts the Term Asset-Backed Security Loan Facility (Small Business Loans)

- 04/09 – Fed begins several new programs:

- The Paycheck Protection Program Loan Facility (Purchase of $350 billion in SBA Loans)

- A Main Street Business Lending Program ($600 billion in additional Small Business Loans)

- The Municipal Liquidity Facility (Purchase of $500 billion in Municipal Bonds.)

- Expands funding for PMCCF, SMCCF and TALF up to $850 billion.

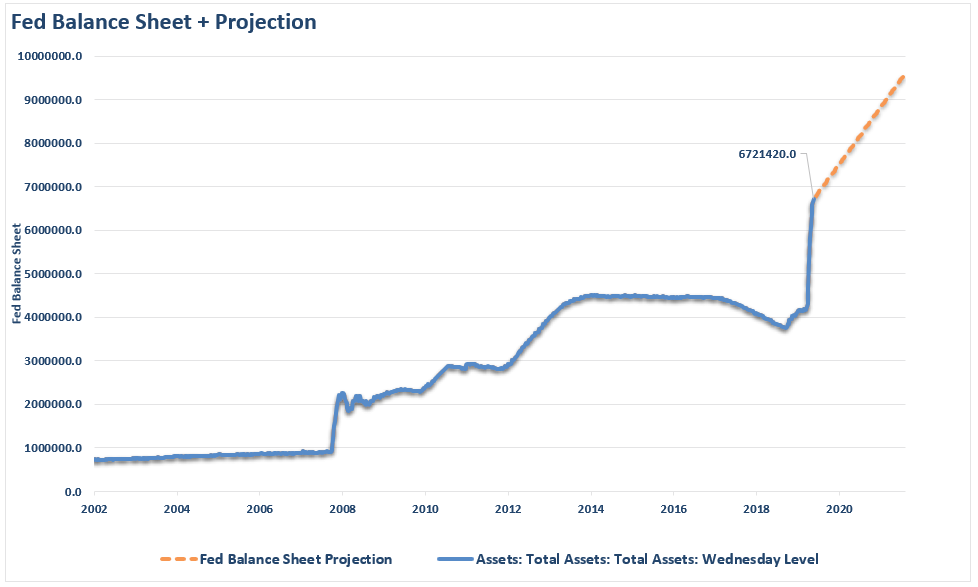

Racking Up The Debt

Here is the Fed’s balance sheet through this past Wednesday (estimated at time of writing)

As investor Paul Tudor Jones stated:

“Investors can take heart that we’ve counteracted this existential shock with the greatest fiscal, monetary bazooka. It’s not even a bazooka. It’s more like a nuclear bomb.”

Was It Too Much?

Jones’s comment was correct. However, was applying a “nuclear bomb” of monetary policy the proper response to a virus? Such is the question for consideration.

Historically, the world has been through several viruses, world wars, financial panics, major natural disasters, inflationary spikes, terrorist events, corporate defaults, attacks, and more. In every case, the economy, markets, and population survived and eventually flourished.

Was COVID-19 going to change history? I doubt it.

In hindsight, it is becoming easier to comprehend that shutting down the entire economy was probably not the right choice. Infection rates and death tolls are far lower than initially estimated, and the economic fallout was a steep price to pay. However, going in to the crisis such a modest outcome was not known and politicians had touch decisions to make.

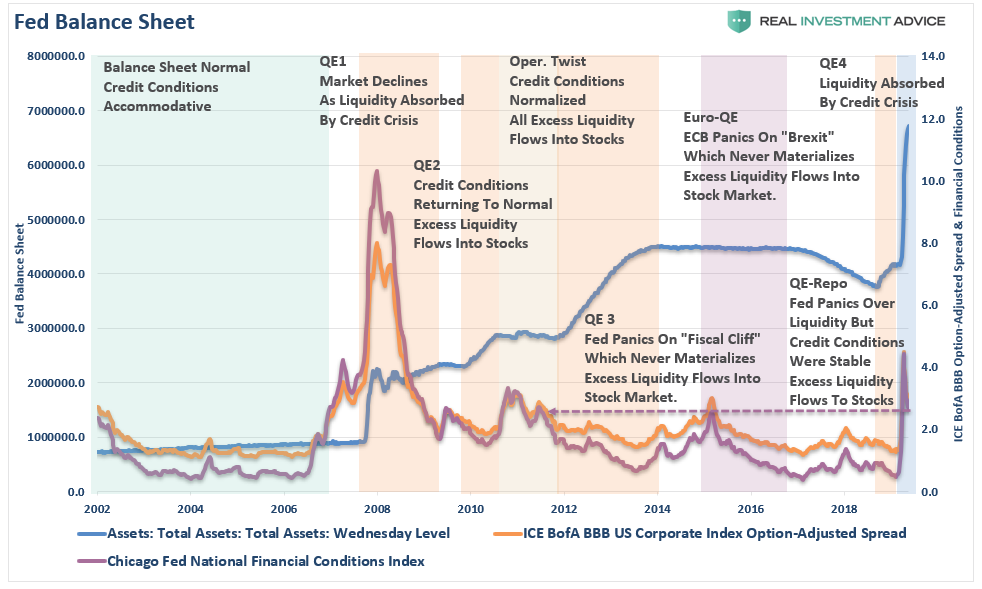

The magnitude of the Fed’s response was also a function of “panic” based more on “recency bias” than facts. The Fed quickly returned to the “Financial Crisis” playbook to anticipate events that may occur in the credit markets rather than responding to outcomes.

There is a difference.

The Financial Crisis was a problem with the banking system. The COVID-19 pandemic is a health crisis.

Notice the difference between the 2008 crisis and today concerning yield spreads, financial conditions, and the Fed’s balance sheet.

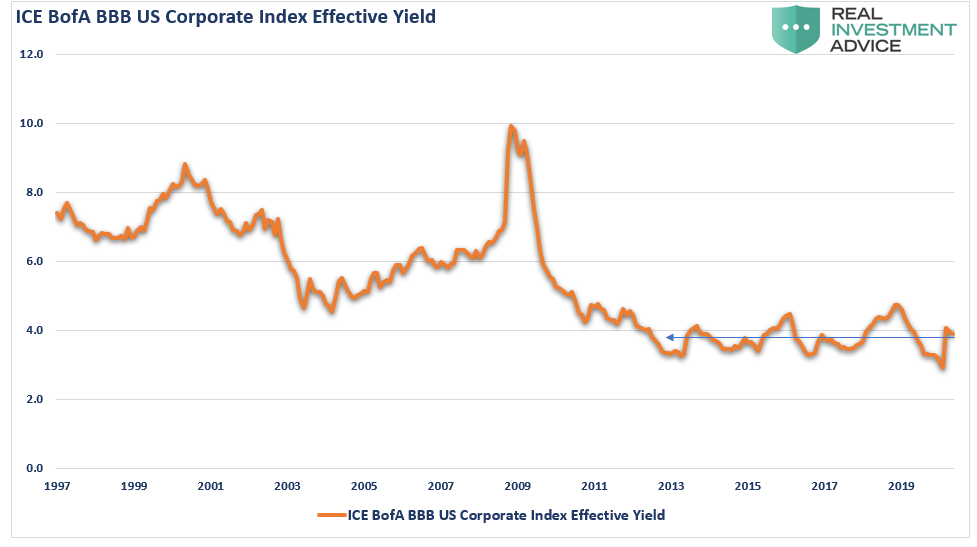

The Yield Tale

The singular purpose of the Fed’s actions was to ensure the proper functioning of the credit markets. While yields did initially spike, that ignition was quickly quenched by the “fire hose” of liquidity from the Fed.

However, the Fed has not ceased their actions. Last week, the Fed began its process of buying corporate and high-yield bond ETF’s. These purchases are being done under the SMCCF program (Secondary Market Corporate Credit Facility) with the sole purpose of ensuring corporate credit markets function smoothly.

“Purchases are focused on reducing the broad-based deterioration of liquidity seen in March 2020 to levels that correspond more closely to prevailing economic conditions,” the document said. It listed an array of metrics that would guide investments, including transaction costs, bid-ask spreads, credit spreads, volatility, and “qualitative market color.”

“Once market functioning measures return to levels that are more closely, but not fully, aligned with levels that correspond to prevailing economic conditions, broad-based purchases will continue at a reduced, steady pace to maintain these conditions.”

Such is interesting as credit condition never blew out and have already returned to levels more closely aligned with previous economic conditions. In fact, in the one area where there is the densest concentration of bonds “at risk,” effective yields haven’t risen much at all.

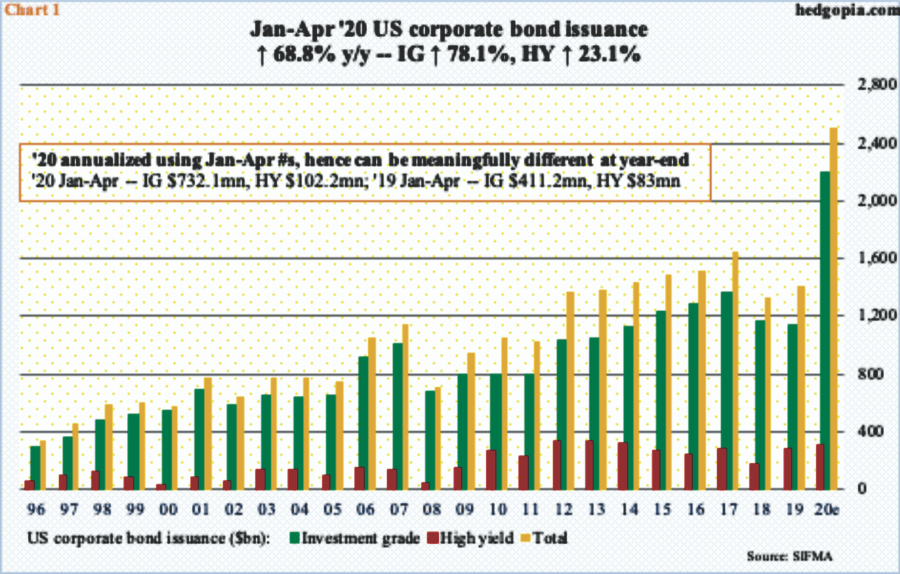

More Debt

Corporate issuers also have had NO trouble issuing debt as of late. In fact, over the past couple of months, there has been a record amount of debt issuance in investment-grade bonds, with high yield issuance close to previous levels.

If yields are within more normal ranges, and bond issuance isn’t a problem, then why is the Federal Reserve continuing to act as if a credit crisis is in process?

Do they see issues in the credit markets the data doesn’t show? Or, are they trying to “front-run” any potential credit disruptions which may occur as the economy reopens?

There Will Be Consequences

If the Fed is correct, and a credit crisis is in process, then the current levels of stimulus may fall short. As noted on April 10th:

“We are now looking at a potential decline of 20% in GDP, which will equate to roughly a $10 Trillion reduction in debt as defaults, bankruptcies, and restructurings rise.

There is a real possibility the Fed is ‘filling in a hole’ that is growing faster than they can fill it. (The Fed is injecting $6 Trillion via the balance sheet expansion versus a potential $10 Trillion shortfall.)”

Unfortunately, that estimate of the decline in GDP was a bit optimistic. Last week, the Atlanta Fed’s real-time economic indicator was predicting a -42.8% decline, or nearly twice the current levels of most estimates.

However, if this turns out to be a short-lived crisis and economic activity comes surging back, then the Fed’s stimulus may be too much, leading to a surge in inflation and downward pressure on the middle class.

Regardless of the eventual outcome, there is one consequence of massive debt and deficit expansions that will not change – slower economic growth.

No Other Choice

With the economy facing an “economic depression,” and in the middle of an election year, the Federal Reserve had a choice to make.

- Allow capitalism to take root by allowing corporations to fail and restructure after spending a decade leveraging themselves to the hilt, buying back shares, and massively increasing their executives’ wealth while compressing the wages of workers. Or,

- Bailout the “bad actors” once again to forestall the “clearing process” that would rebalance the economy, and allow for higher levels of future organic economic growth.

As the Fed’s balance sheet heads toward $10 Trillion, the Fed opted to impede the “clearing process.” By not allowing for debt to fail, corporations to be restructured, and “socializing the losses.” They have removed the risk of speculative practices and ensured a continuation of “bad behaviors.”

Unfortunately, given we now have a decade of experience of watching the “wealth gap” grow under the Federal Reserve’s policies, the next decade will only see the “gap” worsen.

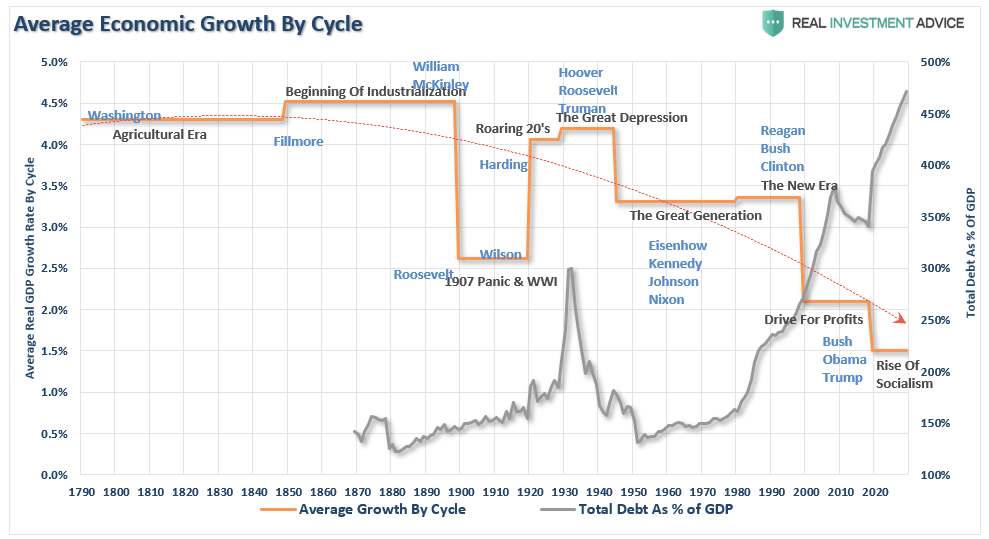

Furthermore, given that we now know surging debt and deficits inhibit organic growth, the massive debt levels added to the backs of taxpayers will only ensure lower long-term rates of economic growth. The chart below shows the 10-year annualized run rates of economic growth throughout history with projected debt and growth levels over the next decade.

The End Game

History is pretty clear about future outcomes from the Fed’s current actions. More importantly, these actions are coming at a time where there were already tremendous headwinds plaguing future economic growth.

- A decline in savings rates

- An aging demographic

- A heavily indebted economy

- A decline in exports

- Slowing domestic economic growth rates.

- An underemployed younger demographic.

- An inelastic supply-demand curve

- Weak industrial production

- Dependence on productivity increases

Yes, another $4-6 Trillion in QE will likely be successful in inflating a third “bubble” to counteract the last deflation.

The problem is that after a decade of pulling forward future consumption to stimulate economic activity, a further expansion of the wealth gap, increased indebtedness; low rates of economic growth will weigh on future economic opportunity for the masses.

Supporting economic growth through increasing levels of debt only makes sense if “growth at all cost” uniformly benefits all citizens. Unfortunately, we are finding out there is a big difference between growth and prosperity.

The United States is not immune to social disruptions. The source of these problems is compounding due to the public’s failure to appreciate it. Until the Fed’s policies are discussed publicly and reconsidered, the policies will remain, and the problems will grow.

Was the “medicine” applied by the Fed to counteract a “virus” the correct prescription? If the patient ultimately dies, we will have our answer.