Over the last month, the Federal Reserve, and the Government, have unleashed a torrent of liquidity into the U.S. markets to offset a credit crisis of historic proportions. Here is a list of programs already implemented which have already surpassed all programs during the “Financial Crisis.”

- March 6th – $8.3 billion “emergency spending” package.

- March 12th – Federal Reserve supplies $1.5 trillion in liquidity.

- March 13th – President Trump pledges to reprieve student loan interest payments

- March 13th – President Trump declares a “National Emergency” freeing up $50 billion in funds.

- March 15th – Federal Reserve cuts rates to zero and launches $700 billion in “Q.E.”

- March 17th – Fed launches the Primary Dealer Credit Facility to buy corporate bonds.

- March 18th – Fed creates the Money Market Mutual Fund Liquidity Facility

- March 18th – President Trump signs “coronavirus” relief plan to expand paid leave ($100 billion)

- March 20th – President Trump invokes the Defense Production Act.

- March 23rd – Fed pledges “Unlimited QE” of Treasury, Mortgage, and Corporate Bonds.

- March 23rd – Fed launches two Corporate Credit Facilities:

- A Primary Market Facility (Issuance of new 4-year bonds for businesses.)

- A Secondary Market Facility (Purchase of corporate bonds and corporate bond ETF’s)

- March 23rd – Fed launches the Term Asset-Backed Security Loan Facility (Small Business Loans)

- April 9th – Fed launches several new programs:

- The Paycheck Protection Program Loan Facility (Purchase of $350 billion in SBA Loans)

- A Main Street Business Lending Program ($600 billion in additional Small Business Loans)

- The Municipal Liquidity Facility (Purchase of $500 billion in Municipal Bonds.)

- Expands funding for PMCCF, SMCCF and TALF up to $850 billion.

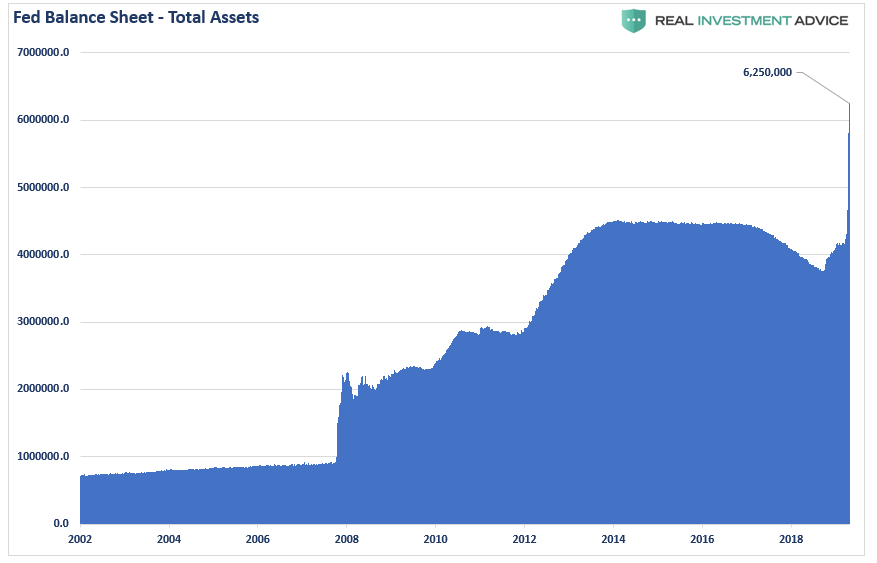

Here is the Fed’s balance sheet through this past Wednesday (estimated at time of writing)

It is currently expected that over the course of the next several quarters, the Fed’s balance sheet will grow to $10 Trillion in total. Such would be a $6 Trillion expansion from the previous levels.

Why is this important?

“John Maynard Keynes’ was correct in his theory that in order for government ‘deficit’ spending to be effective, the ‘payback’ from investments being made through debt must yield a higher rate of return than the debt used to fund it.”

The programs currently being pursued with deficit spending, only exacerbate the current problem.

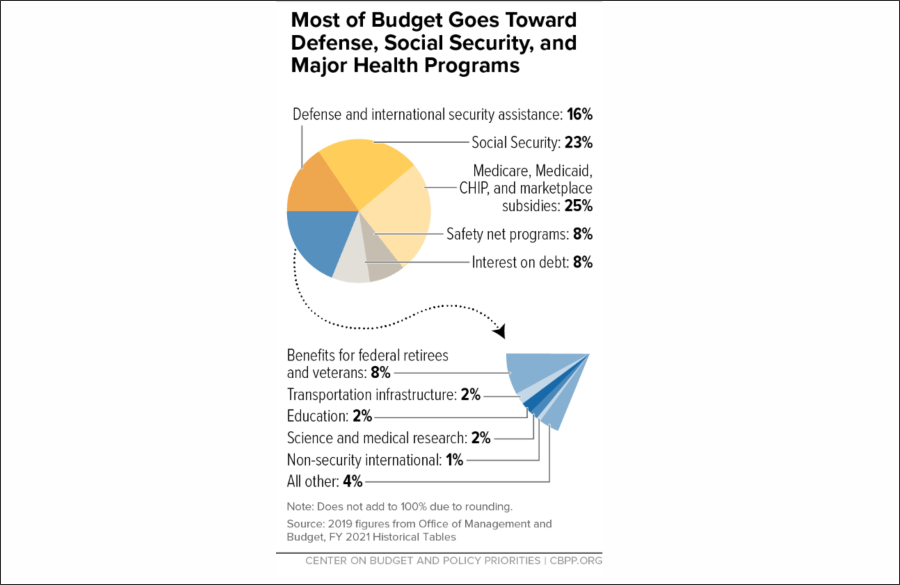

According to the Center On Budget & Policy Priorities, in 2019, roughly 75% of every tax dollar went to non-productive spending.

“In fiscal year 2019, the federal Government spent $4.4 trillion, amounting to 21 percent of the nation’s gross domestic product (GDP). Of that $4.4 trillion, only $3.5 trillion was financed by federal revenues. The remaining amount ($984 billion) was financed by borrowing. As the chart below shows, three major areas of spending make up the majority of the budget.”

Think about that for a minute. If 2019, if 75% of all expenditures went to social welfare and interest on the debt, those payments required $3.3 Trillion of the $3.5 Trillion (or 95%) of the total revenue coming in.

That was BEFORE the shutdown of the economy due to COVID-19, and the subsequent decline in economic activity coming over the course of this year. Just recently, we made some estimates on the severity of the economic impact of the virus. To wit:

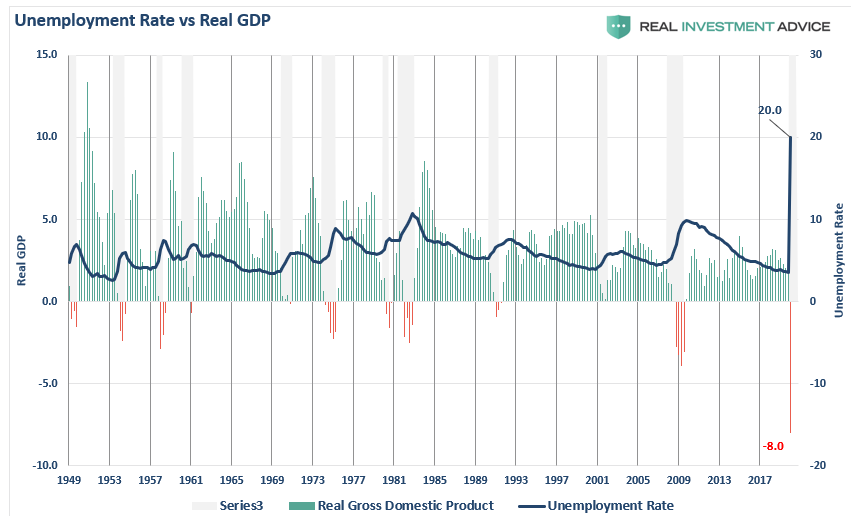

“The importance is that unemployment rates in the U.S. are about to spike to levels not seen since the “Great Depression.” Based on the number of claims being filed, we can estimate that unemployment will jump to 20%, or more, over the next quarter as economic growth slides 8%, or more. (I am probably overly optimistic.)”

As I stated, I was overly optimistic in my assessment based on the initial data. With more data now pouring in, estimates for negative GDP growth in the 2nd quarter of 2020 have risen to -20%.

There are many important “knock-off” effects from such a dramatic slide in economic growth.

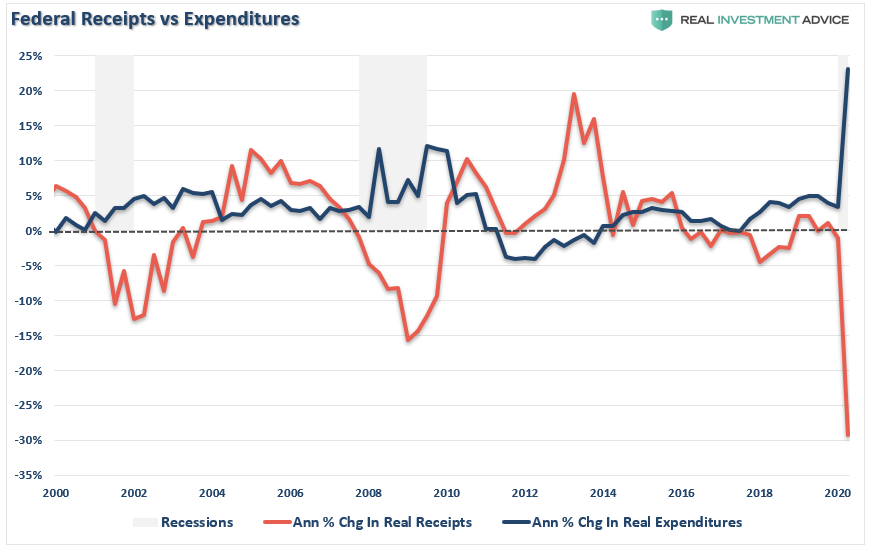

Given that GDP is roughly 70% driven by consumption, the spike in unemployment is going to curtail the consumptive capacity of the individuals. As job losses mount, income tax revenue declines, and demands for government assistance increase.

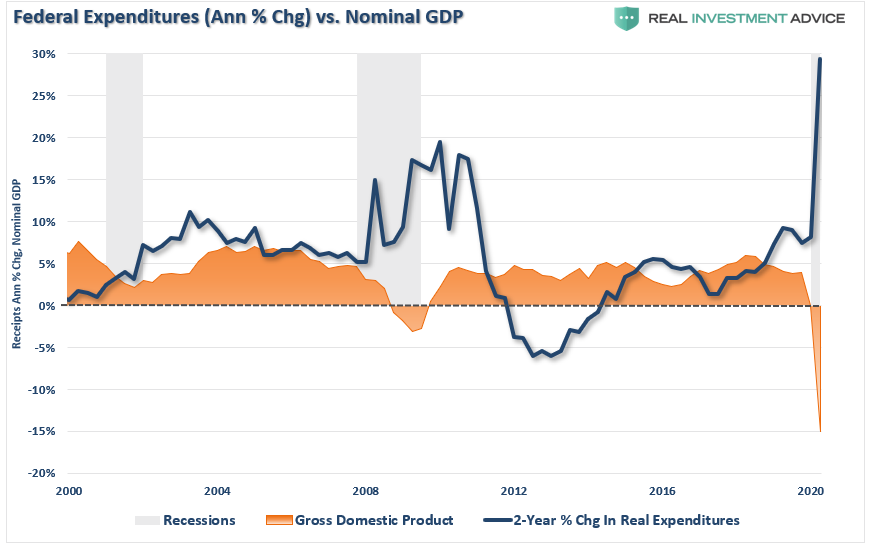

At the same time, as demand falls, so does corporate revenue and incomes, which result in lower corporate tax revenue. Additionally, as we have seen with the myriad of Federal Reserve and Government programs as of late, the collapse in revenue and activity has led to a sharp increase in spending to try and keep businesses operational.

Once we start putting the data together, we can make an assumption that the deficit will likely increase towards $3 trillion as tax revenues fall sharply due to a deep recession. This drop in revenues alone, given that 75% of all government spending is “mandatory,” was already set to cause a surge in the deficit. However, when that drop is combined with the recent “all-out” fiscal campaign to counter the impact of the virus, we are talking about a deficit that will approach 23-25% of GDP.

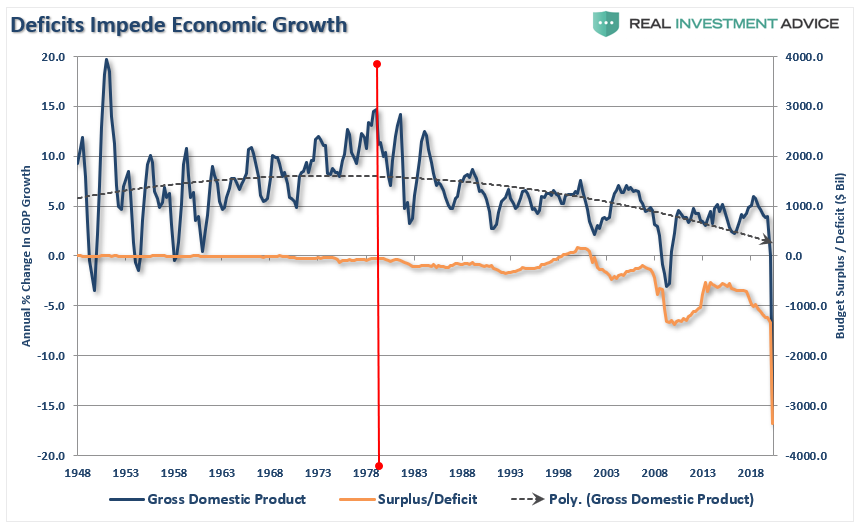

Most importantly, there is a strong correlation between debt, deficits, and economic growth. As I noted previously:

“The larger the balance of debt has become, the more economically destructive it is by diverting an ever-growing amount of dollars away from productive investments to service payments.

Since 2008, the economy has been growing well below its long-term exponential trend. Such has been a consistent source of frustration for both Obama, Trump, and the Fed, who keep expecting higher rates of economic only to be disappointed.”

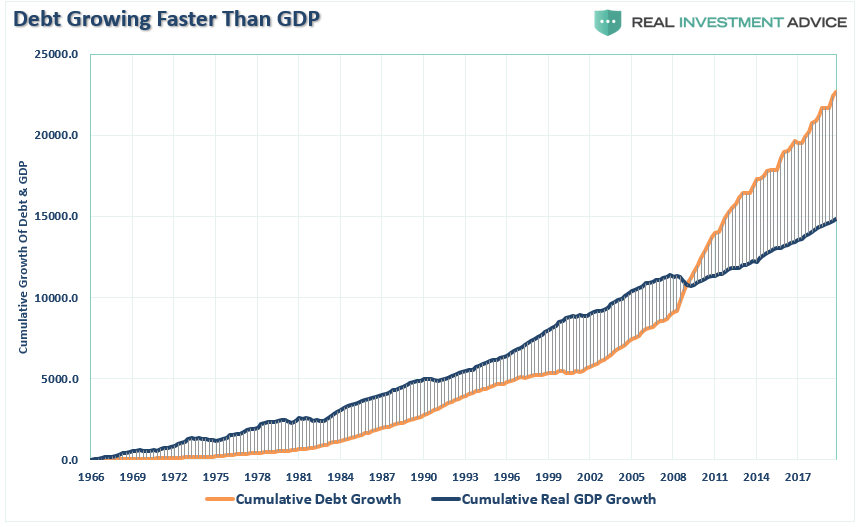

The relevance of debt growth versus economic growth is all too evident. When debt issuance exploded under the Obama administration, and accelerated under President Trump, it has taken an ever-increasing amount of debt to generate $1 of economic growth.

In other words, without debt, there has been no organic economic growth.

What is indisputable is that running ongoing budget deficits that fund unproductive growth is not economically sustainable long-term.

The “Debt Chasm” Is Way Too Big

When credit creation can no longer be sustained, the markets must clear the excesses before the next cycle can begin. It is only then, and must be allowed to happen, can resources be reallocated back towards more efficient uses. This is why all the efforts of Keynesian policies to stimulate growth in the economy have ultimately failed.

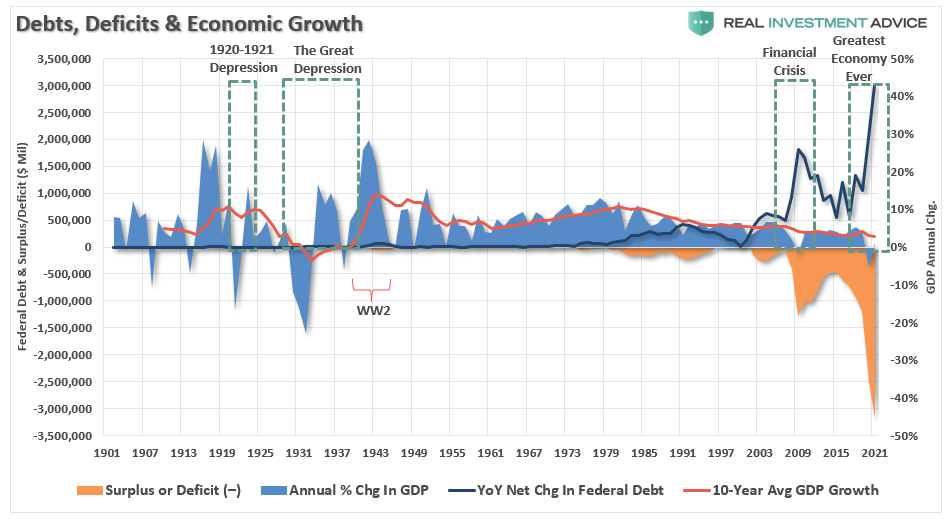

Over the last decade, the Fed’s monetary policies, and the Government’s largesse, has inflated debt to even greater levels than seen during the “Financial Crisis.” However, instead of allowing the “clearing process” to proceed, the Federal Reserve, and the Government, have opted to throw the “kitchen sink” at the credit markets to try and forestall that process. Ultimately, continuing to “kick the can” not only increases the risk of the next crisis, but slows the economic recovery, and further impeded future economic growth.

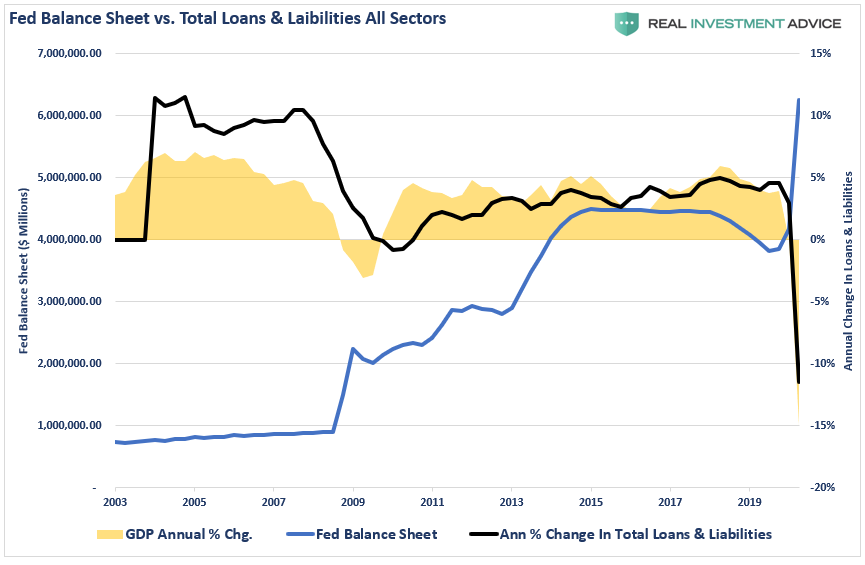

This is the larger problem facing the Fed. This is no longer a game of just “subprime” mortgage debt. This time they are having to bailout debt from credit cards, to auto loans, corporate debt, mortgage debt, mortgage servicing, municipal debt, and fund the entirety of the federal deficit.

The chart below shows the Federal Reserve’s balance sheet versus GDP and total outstanding debt. In 2008, there was, not surprisingly, a sharp decline in debt and economic growth as defaults, bankruptcies, and restructuring occurred. This debt decline coincided with less than a 5% annual drop in GDP.

We are now looking at a potential decline of 20% in GDP, which will equate to roughly a $10 Trillion reduction in debt as defaults, bankruptcies and restructurings rise.

In other words, while investors are currently banking on the Fed’s numerous monetary injections to fuel asset prices higher, there is a real possibility the Fed is simply “filling in a hole” that is growing faster than they can fill it. (The Fed is injecting $6 Trillion via the balance sheet expansion versus a potential $10 Trillion shortfall.)

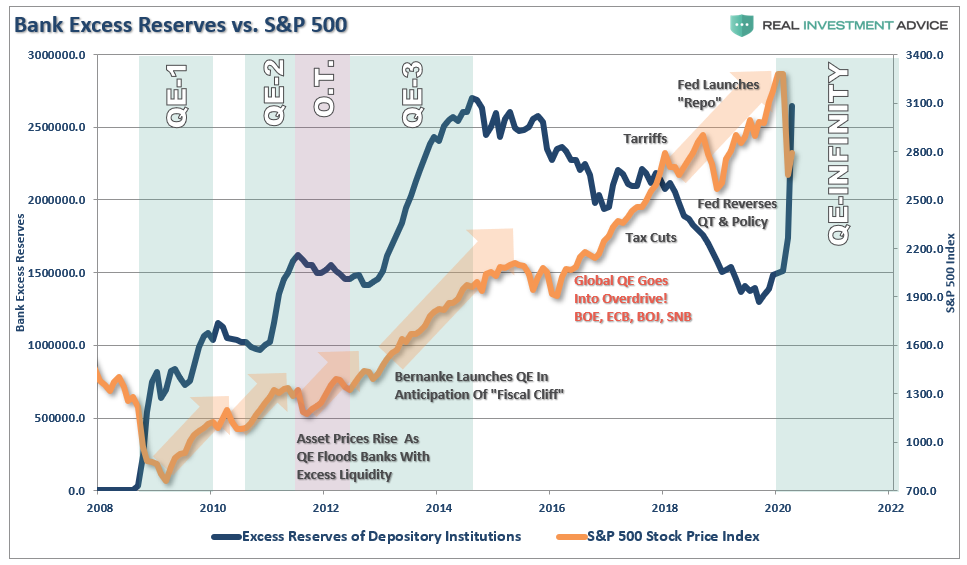

In the short-term, the Fed is massively increasing the liquidity of banks (excess reserves) through the various “Q.E” facilities to stave off a second “financial crisis.” Given the banks do NOT want to loan out any funds not guaranteed by the Federal Reserve, the excess liquidity flows into asset markets.

However, liquidity flowing into small business loans, one-time payments, etc. does not increase long-term economic demand. There is a very real possibility that many businesses will fail before they get support, many will fail even after, and many others won’t ever recover fully. Such suggests there is likely much more debt at risk of default than the Fed is currently taking in, and disruption of credit markets is still possible.

The problem with monetary policy, in all of its forms, is that it disincentivizes capitalism.

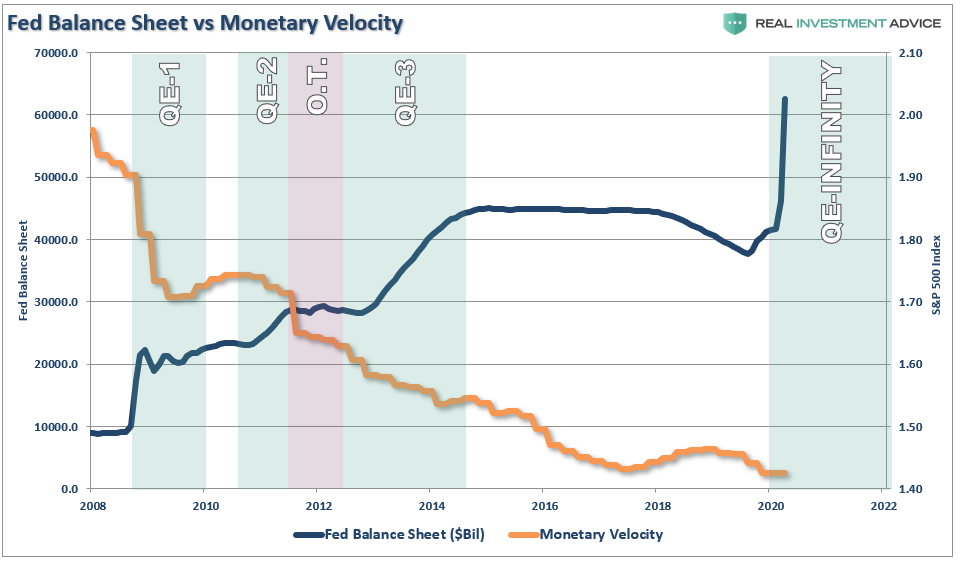

Zero interest rates, excess liquidity, and a closed-loop between the banks and the Fed, removed all incentives to “take risk” of lending money to businesses and individuals to create economic growth. Instead, that liquidity fueled assets prices, stock buybacks, and corporate debt which engendered a wealth gap never before seen in history. In fact, there is no evidence that QE leads to monetary velocity, or rather the transfer of liquidity into the economic system, at any level.

(Monetary policy has acted as the single largest wealth transfer system from the poor to the rich in history.)

While the Federal Reserve’s programs may temporarily support asset prices, eventually asset prices must reflect actual economic growth, revenues, and expectations of future cash flows. Unfortunately, there are a host of problems which suggests future returns from asset markets will be much lower than we have seen over the last two-decades.

- A decline in savings rates

- An aging demographic

- A heavily indebted economy

- A decline in exports

- Slowing domestic economic growth rates.

- An underemployed younger demographic.

- An inelastic supply-demand curve

- Weak industrial production

- Dependence on productivity increases

With the “boomer generation” now at risk of “permanent job losses,” they will become a net drag on “savings,” in turn leading to an increased dependency on the “social welfare net,” and the “pension problem” is lurking in the shadows.

The simple reality is that the ability to continue pulling forward future consumption to stimulate economic activity is gone. There are only so many autos, houses, etc., which can be purchased within a given cycle, and after a decade, that cycle has been reached.

While investors have been trained over the last decade to “not fight the Fed,” what if the “Fed” is throwing money into a “debt chasm” they can’t fill?