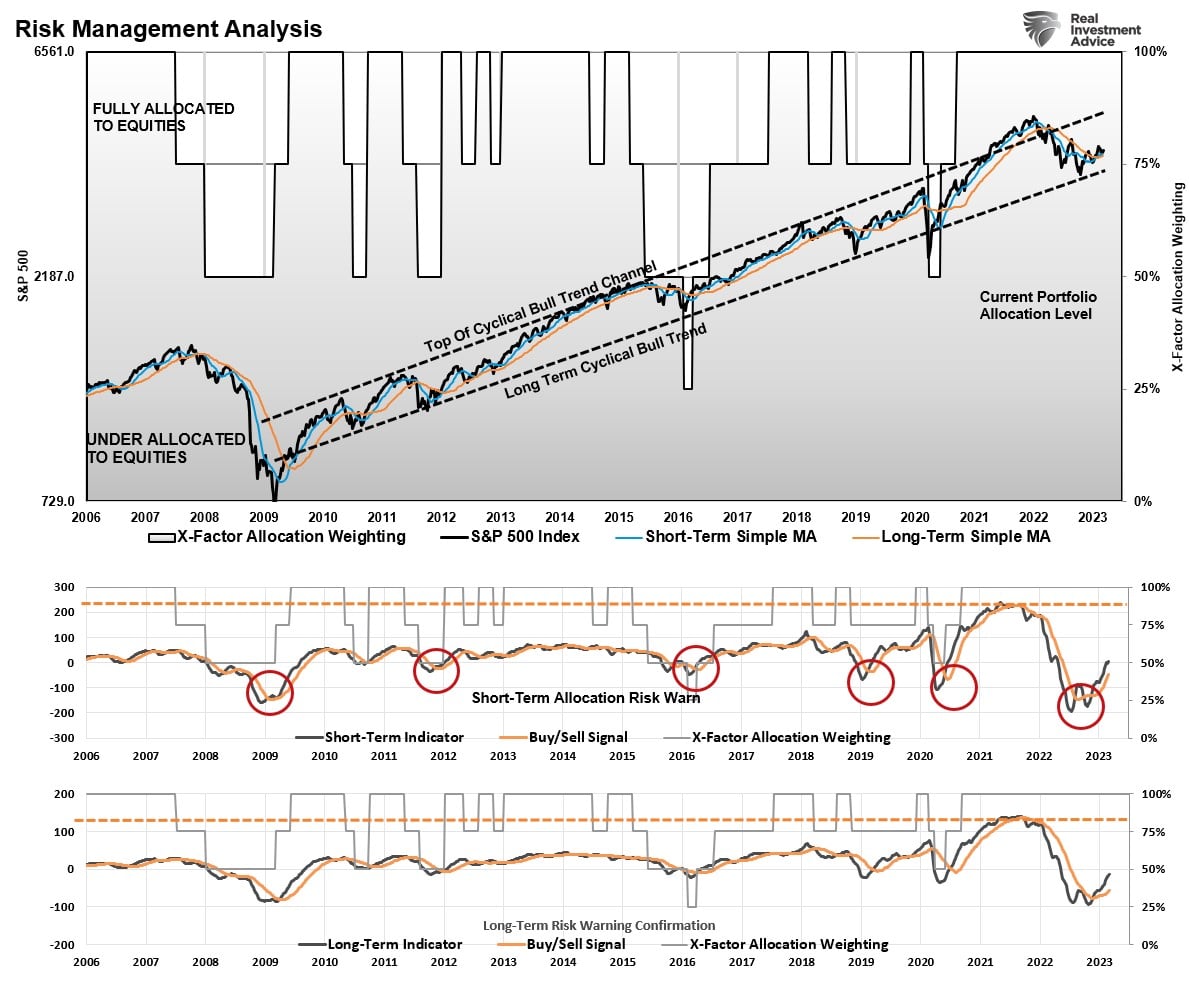

Could the consensus view of a “no recession” scenario be wrong? As portfolio managers, this is the question we ask ourselves daily. Since the lows of last October, the technical backdrop has improved markedly, as discussed last week in “Bear Trap.” To wit:

“Our most critical bullish signals are the short- and intermediate-term Moving Average Convergence Divergence (MACD) indicators. We post this weekly chart in our website’s 401k plan management section. Both sets of weekly MACD indicators have registered buy signals from levels lower than during the financial crisis. The market has also broken above both weekly moving averages and, as noted above, held the long-term bullish trend line.”

While the technical backdrop continues to confirm and reaffirm a bullish trend supporting the “no recession” scenario, there remain substantial risks to that view. Such risks, as was seen with Silicon Valley Financial (SVB) last week, can arise quickly, turning previously bullish sentiment quickly bearish.

What happened with SVB is a result of tighter monetary policy extracting liquidity from the banking system. In an upcoming article, I quoted Thorsten Polleit from The Mises Institute, stating:

“What is happening is that the Fed is pulling central bank money out of the system. It does this in two ways. The first is not reinvesting the payments it receives into its bond portfolio. The second is by resorting to reverse repo operations, in which it offers “eligible counterparties” (those few privileged to do business with the Fed) the ability to park their cash with the Fed overnight and pay them an interest rate close to the federal funds rate.”

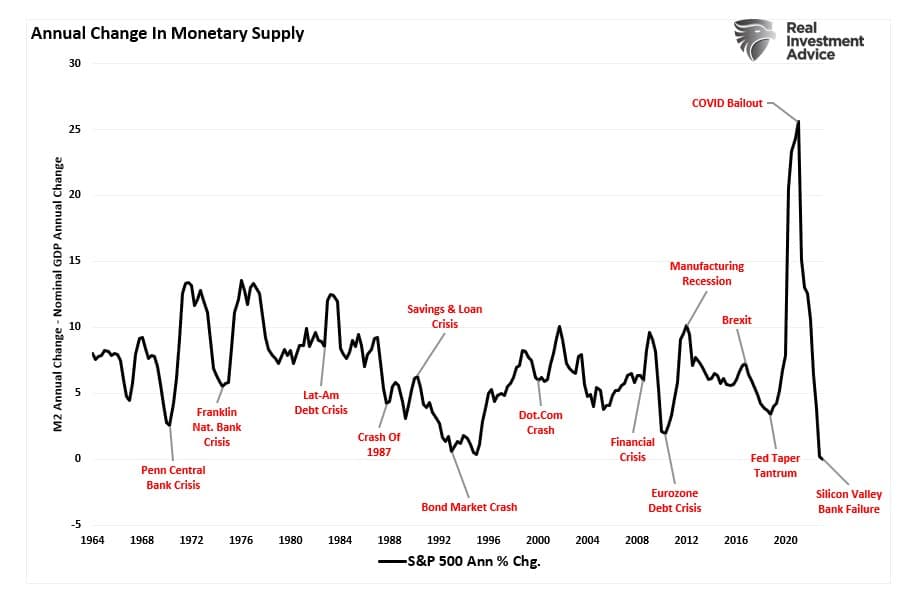

As shown, contractions in nominal M2 have coincided with financial and market-related events in the past. Such is because the Fed is draining liquidity out of the financial system, which is a problem for overleveraged banks.

However, while SVB might be an isolated event, of which we are not sure, the driver of higher asset prices remains a consensus view that earnings will bottom in the second quarter of this year and begin to improve into year-end. If such is the case, given that markets lead fundamental changes, the market’s rally since last October is logical.

But that is the key to the markets this year. Is the consensus view right or wrong?

Will Earnings Bottom?

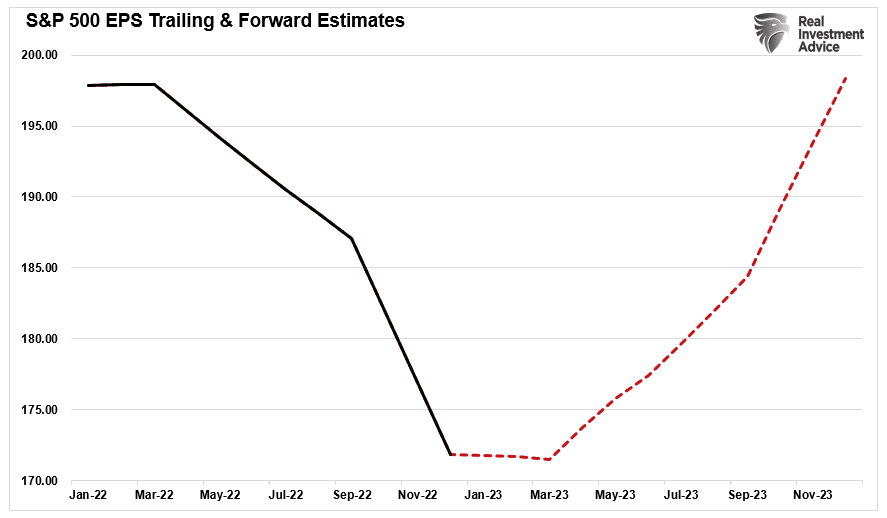

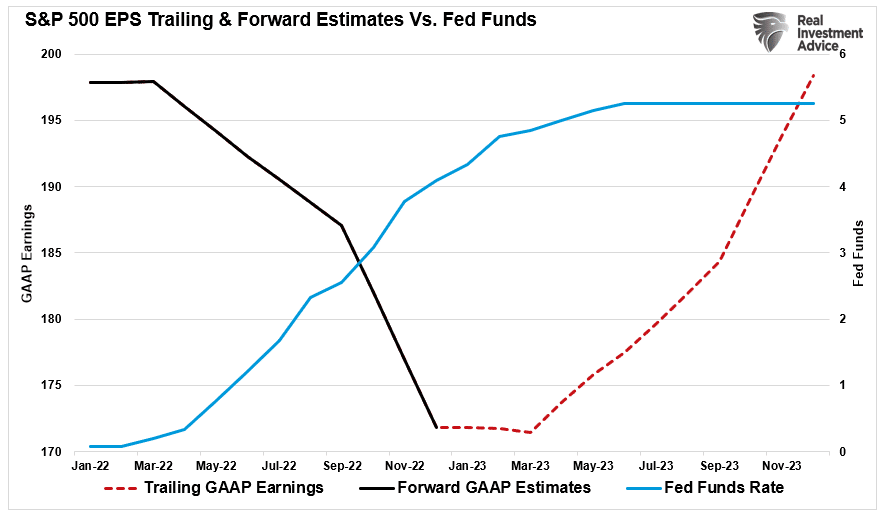

The chart below shows the GAAP estimates (red dotted line) by S&P Global through the end of 2023. Amazingly, they expect earnings to recover to where they were at the bull market’s peak in 2022. Such was when interest rates were zero, and the Federal Reserve provided $120 billion monthly in “quantitative easing.”

However, this view from S&P Global is the same as most Wall Street banks who expect the Fed to “pause” its rate hiking campaign and the economy to avoid a recession. That broad consensus view of a “no landing” scenario has fueled the market’s advance since January but remains at odds with much of the macroeconomic data.

As I discussed in “No Landing Scenario At Odds With Fed’s Goals,”

“Given the recent spate of economic data from the strong jobs report in January, a 0.5% increase in inflation and a solid retail sales report continue to give the Fed no reason to pause anytime soon. The current base case is that the Fed moves another 0.75%, with the terminal rate at 5.25%.”

That type of rhetoric doesn’t suggest a “no landing” scenario, nor does it mean the Fed will be cutting rates soon. Notably, the only reason for rate cuts is a recession or financial event that requires monetary policy to offset rising risks. This is shown in the chart below, where rate reductions occur as a recession sets in.

The problem with that data is that the lag effect of monetary tightening has not been reflected as of yet. Over the next several months, the data will begin to fully reflect the impact of higher interest rates on a debt-laden economy. However, as shown, while the consensus view is that earnings will grow strongly into year-end, higher rates drag on earnings as economic growth slows.

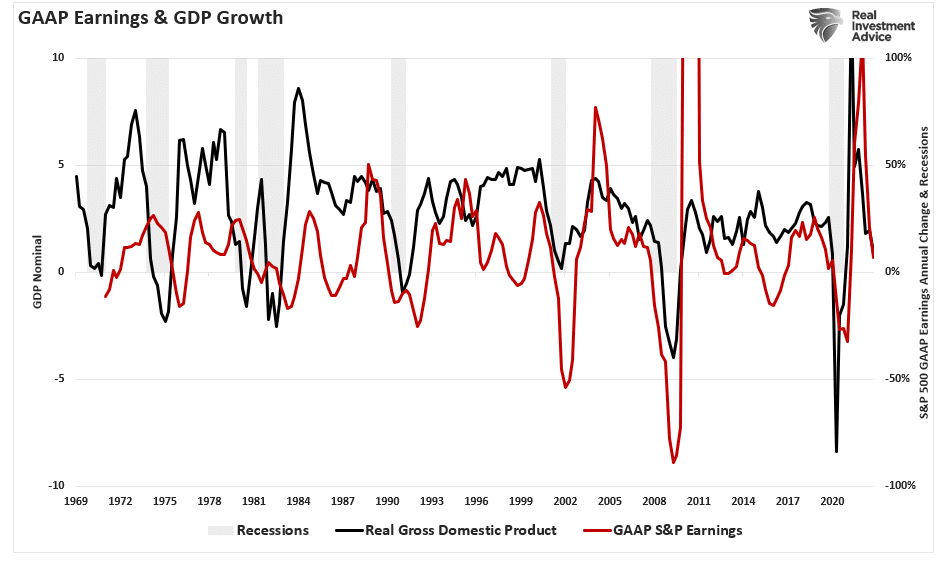

Of course, such is logical, given that earnings are derived from economic activity. As such, there is a decent correlation between economic growth and GAAP earnings.

With the Fed continuing to hike rates, the ability of the economy to start expanding to support earnings growth seems questionable.

However, two other factors also suggest the consensus view is worth questioning.

To Pivot Or Not To Pivot

The problem with the consensus view is that it requires the Fed to revert to monetary accommodation. However, if the consensus view is correct, why would the Fed change policy? As we noted previously:

- If the market advance continues and the economy avoids recession, the Fed does not need to reduce rates.

- More importantly, there is also no reason for the Fed to stop reducing liquidity via its balance sheet.

- Also, a “no-landing” scenario gives Congress no reason to provide fiscal support providing no boost to the money supply.

See the problem with this idea of a “no landing” scenario?

“No landing does not make any sense because it essentially means the economy continues to expand, and it’s part of an ongoing business cycle, and it’s not an event. It’s just ongoing growth. Doesn’t that entail that the Fed will have to raise rates more, and doesn’t that increase the risk of a hard landing?” – Chief Economist Gregory Daco, EY

As I noted, there are two additional problems with the consensus view of a sharp recovery in earnings.

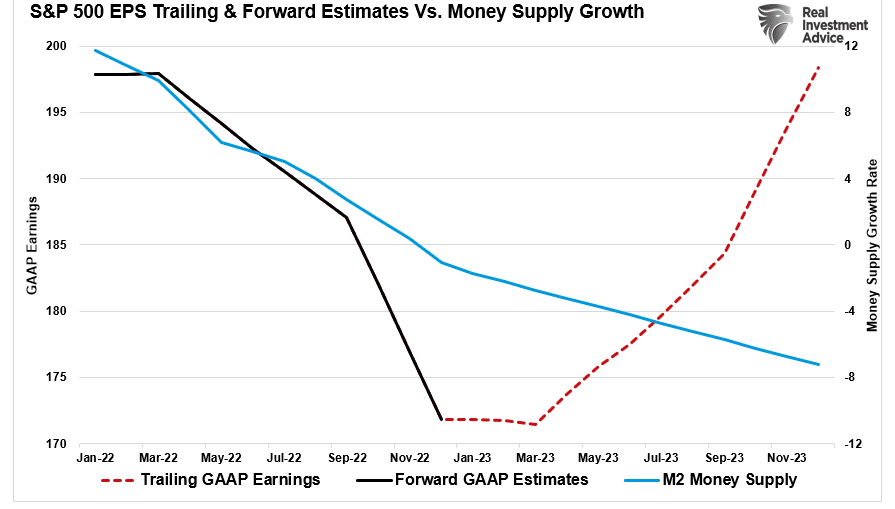

The first is the reversal of the massive stimulus injections into the economy in 2020-2021, which provided for the surge in economic activity and earnings. As shown, money supply growth is reversing, with earnings also slowing. The consensus view expects earnings to buck that correlation in the future.

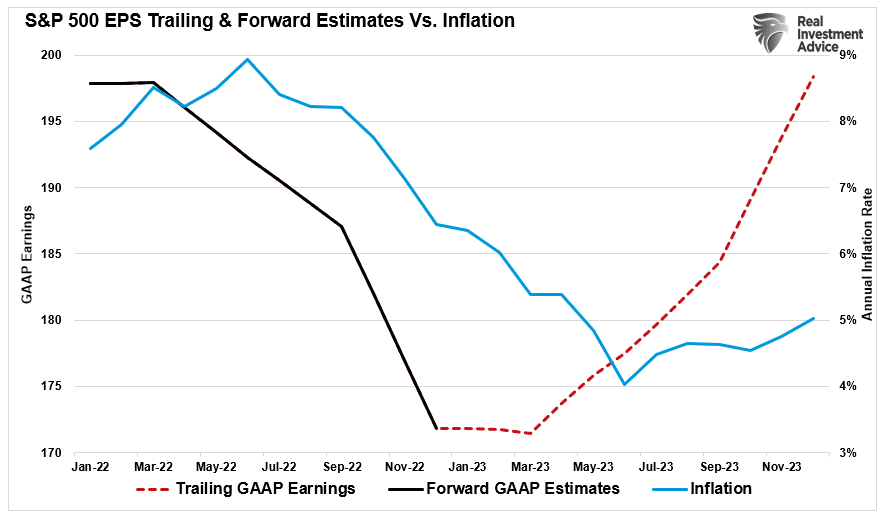

The second problem is inflation. During the pandemic shutdown, the massive supply of monetary stimulus collided with an economic shutdown leading to surging prices. Due to a lack of supply and a massive contraction in employment, surging prices sent corporate profit margins soaring. However, sustaining record margins will be challenging with inflation falling, the economy at full employment, and wages rising.

While the markets are certainly betting on an optimistic scenario, logic suggests many challenges lie ahead.

There is still a lot of money sloshing around the economy from the repeated rounds of stimulus. Also, from the infrastructure spending bill, and increased social security and welfare benefits. The impact of higher rates on economic activity may get delayed but not eliminated.

As Jerome Powell noted in last week’s Senate Finance Committee testimony:

“Inflation has moderated somewhat since the middle of last year but remains well above the FOMC’s longer-run objective of 2 percent… That said, there is little sign of disinflation thus far in the category of core services, excluding housing, which accounts for more than half of core consumer expenditures.

If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes… The historical record cautions strongly against prematurely loosening policy. We will stay the course until the job is done.

That certainly doesn’t suggest a pivot is coming any time soon. This brings us to the one question every investor must answer.

How does the consensus view come to fruition with higher interest rates, less monetary liquidity, and slower economic growth?

I don’t know the answer. However, I am not liking the odds that the outcome will be as positive as Wall Street expects.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read