Wall Street banks, brokers, and asset managers put out market research, which can be of great value. While valuable, we read their research with skepticism and question its authenticity. Firms like Blackrock, Goldman Sachs, and others have a glaring bias. The industry makes billions in annual profits by selling stocks and bonds to investors. Consequently, at times Wall Street talks out of both sides of their mouths to push their products. For example, Blackrock recently reminded us that Blackrock is in it for themselves, not you or me.

Monday’s Wall Street Journal led with a story on Blackrock that started as follows: “CEO Larry Fink’s U-turn illustrates Wall Street’s growing desire to capitalize on a market long considered the Wild West of finance.” Conversely, Larry Fink said this a few years ago: “Let me just say one thing on Bitcoin. Bitcoin is an index for how much demand for money laundering there is in the world. That’s all it is.“

Not surprisingly, with the recent introduction of bitcoin ETFs and the promise of massive profits, Fink finds value in Bitcoin. As highlighted below, Blackrock’s Bitcoin ETF is the second largest at $13.5 billion. Want more evidence that their wallets drive their opinions? Blackrock leads the market in ESG ETFs. Fink and Blackrock couldn’t speak highly enough of the value of investing for the “good” of society. However, recently, ESG has fallen out of favor with investors. Not surprisingly, Blackrock is dissolving ESG funds and downplaying the value of ESG investing.

What To Watch Today

Earnings

Economy

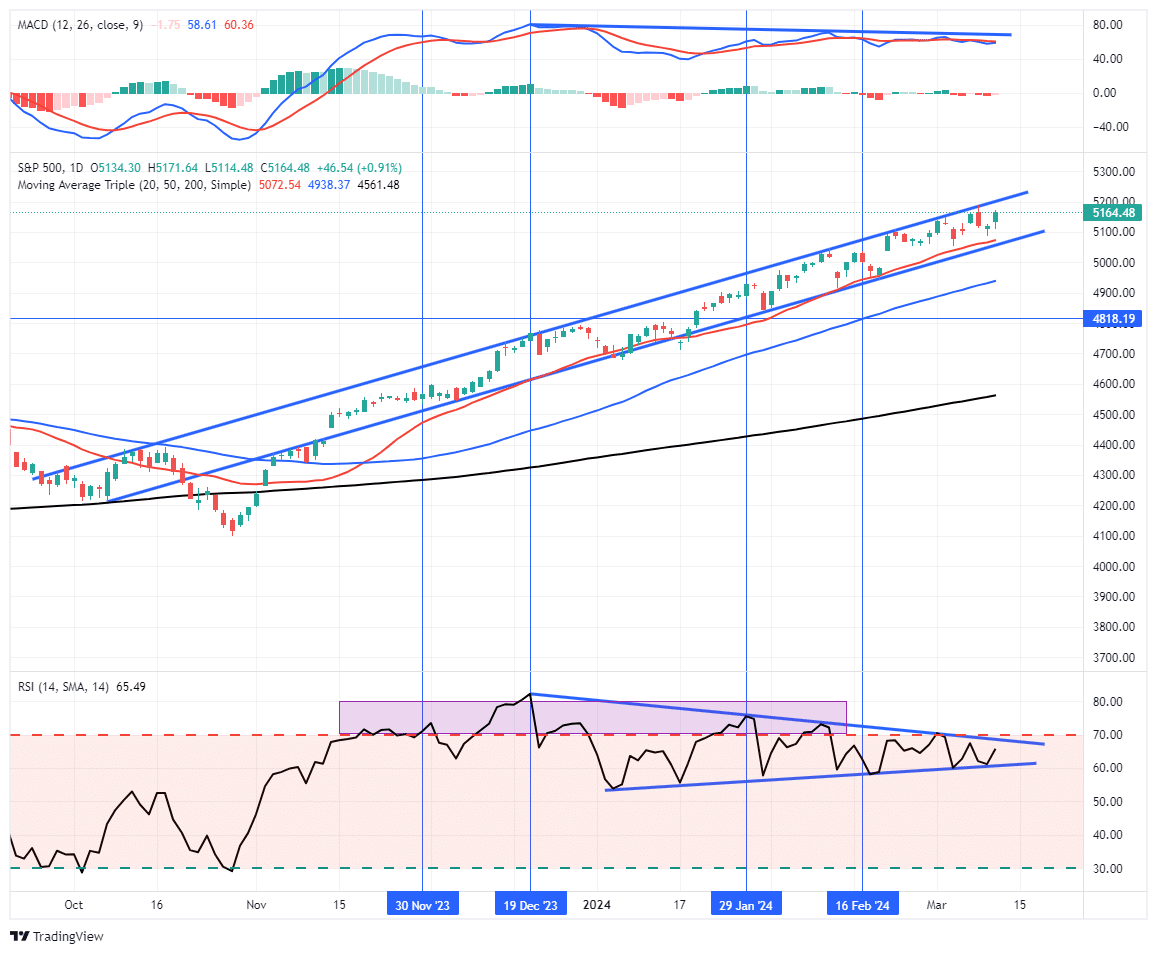

Market Trading Update

Another day….another rally within the bullish trend channel. Such has been the case since the October lows. The low volatility advance continues with the 20-DMA acting as critical support. The algos continue to buy any declines to the 20-DMA and sell at the top of the channel. Despite yesterday’s stronger than expected core CPI reading, the market overlooked the report to focus on when the next Fed rate cut will come. That information may be exposed at the upcoming FOMC meeting.

Nonetheless, despite a continuing deterioration in momentum and relative strength, the market keeps moving toward the 5200 target following the recent breakout. As noted in yesterday’s commentary, there are certainly evident signs of exuberance in the market. Deviations from long-term means remain, and speculative action has returned. However, such environments can remain much longer than logic would predict. Continue to remain long equities for now. There is no evidence that the current bull run will end soon.

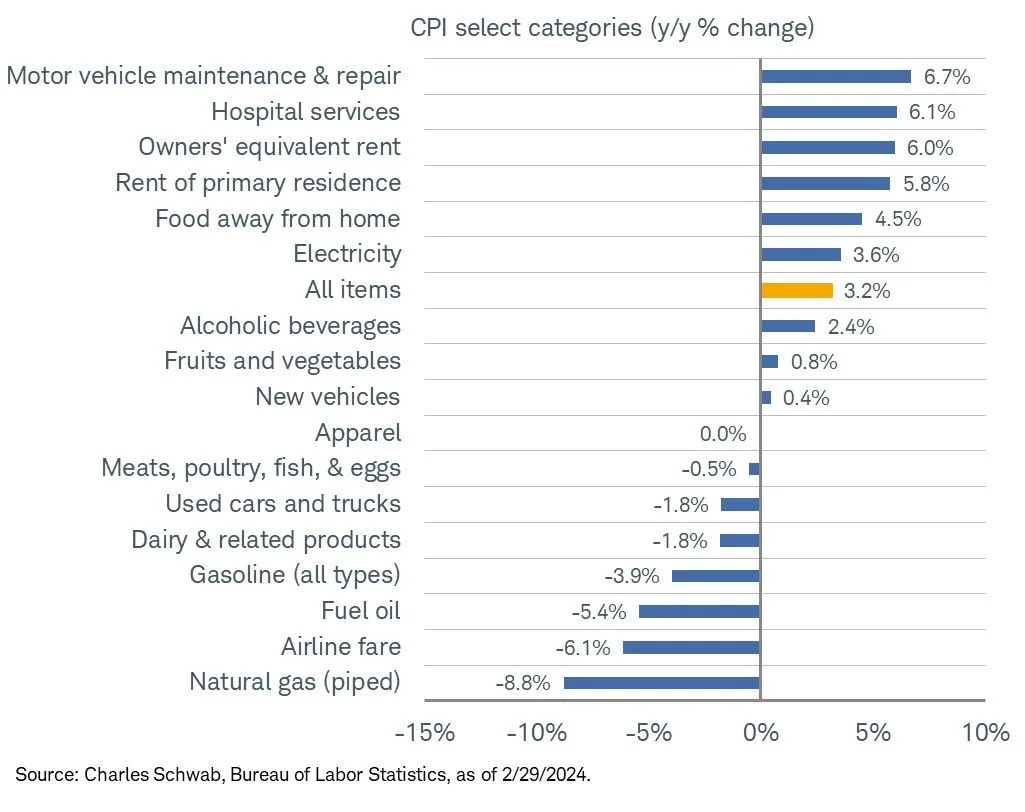

CPI Remains Sticky

As we have seen over the last few months, inflation declines have been put on hold. Headline monthly CPI rose 0.4%, in line with estimates but 0.1% above last month’s reading. Likewise, Core CPI rose 0.4%, a tenth above estimates. The graph below, courtesy of Charles Schwab, shows which sectors added to CPI year-over-year and which took away from it.

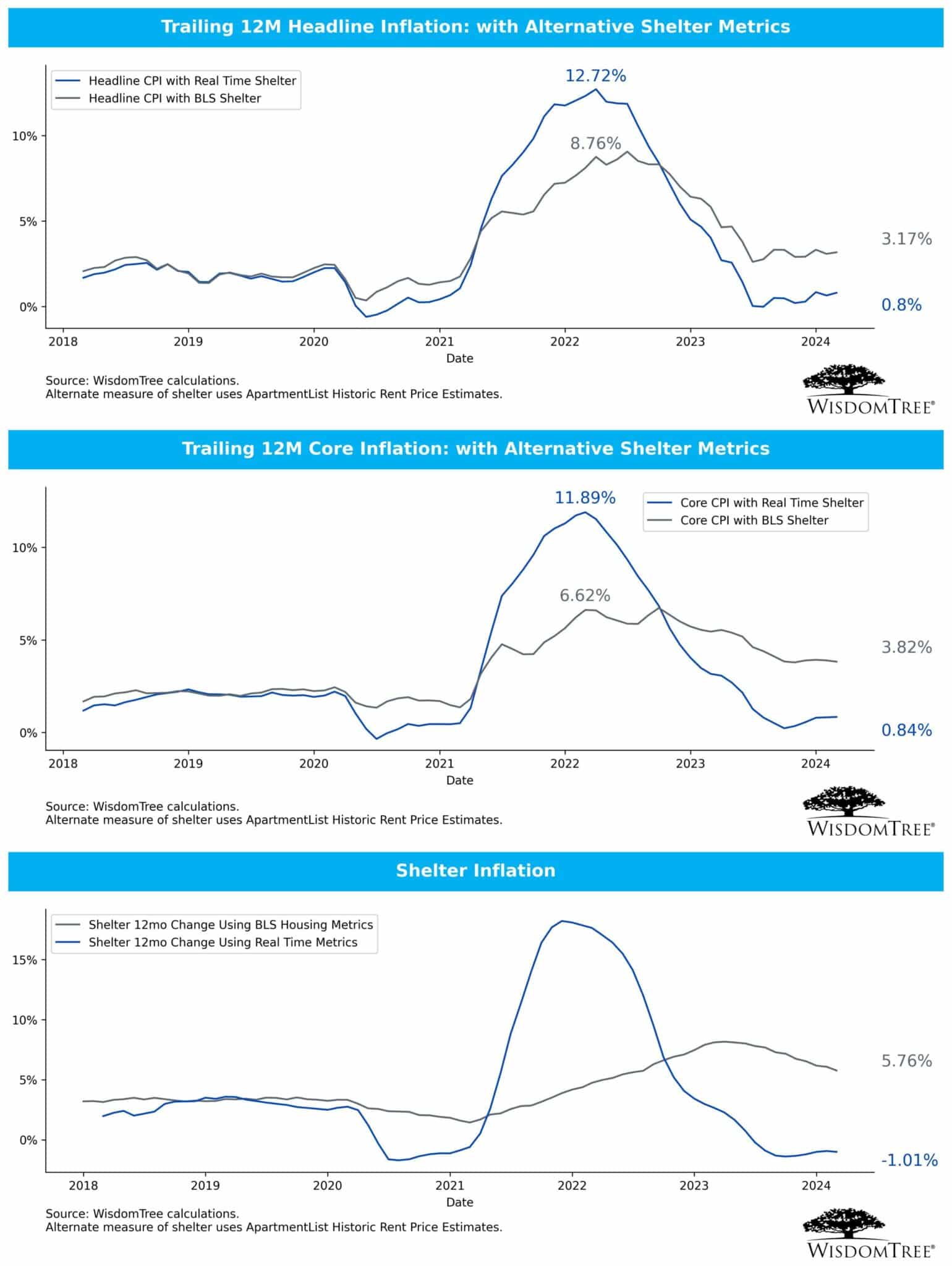

The graph above highlights a flaw in CPI that we have discussed numerous times. Shelter costs, including Owners’ equivalent rent and Rent of primary residence, accounting for 40% of CPI, are the biggest drivers of inflation. Year over year, shelter costs are running near 6%, well above the near zero percent that many market-based indicators point to. As a result, if you adjust CPI shelter costs to market, the headline and core CPI would be below 1%. The graphs below, courtesy of Wisdom Tree, show that CPI is well below the Fed’s 2% target when using real-time shelter costs.

Shelter CPI has moved down for 11 consecutive months. It stood at 8.2% a year ago, the highest in forty years. Given its long lag versus market-based rent data, we think CPI shelter costs will continue to contribute less to CPI. Consequently, the trend in CPI will also likely be lower.

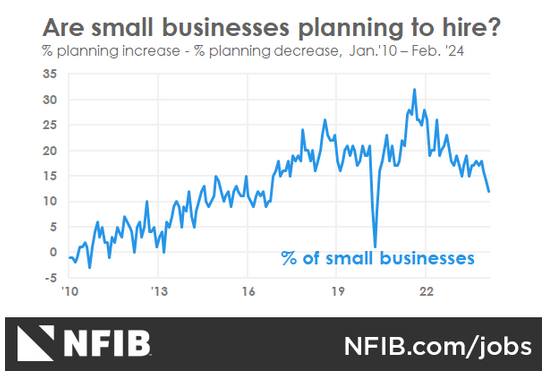

The Labor Outlook Is Deteriorating

Yesterday morning, the NFIB small business survey fell to 89.4. As a result, it has been below the average (98) for over two years. Small businesses account for over half of employment. Therefore, some of the comments and stats in the report are concerning. Per the survey:

- Reports of labor quality as the single most important problem for business owners decreased five points to 16%, the lowest reading since April 2020.

- Small business owners’ plans to fill open positions continue to slow, with a seasonally adjusted net 12% planning to create new jobs in the next three months, the lowest level since May 2020.

- Thirty-seven percent (seasonally adjusted) of all owners reported job openings they could not fill in the current period, down two points from January and the lowest reading since January 2021.

Further evidence of the deteriorating jobs market is found below in the Tweet of the Day.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.