The Fed’s tone markedly changed in the weeks preceding the November 1 FOMC meeting. Many Fed speakers offered that higher interest rates will tighten financial conditions, allowing them to take a break from rate increases. The messaging was solidified at the November 1 FOMC meeting. To wit, the following statement from Jerome Powell.

In this case, the tighter financial conditions we’re seeing from higher long-term rates but also from other sources like the stronger dollar and lower equity prices could matter for future rate decisions, as long as two conditions are satisfied. The first is that the tighter conditions would need to be persistent and that is something that remains to be seen. But that’s critical, things are fluctuating back and forth, that’s not what we’re looking for. With financial conditions, we’re looking for persistent changes that are material. The second thing is that the longer-term rates that have moved up, they can’t simply be a reflection of expected policy moves from us that we would then, that if we didn’t follow through on them, then the rates would come back down.

Powell clarifies that recent interest rate increases, a stronger dollar, and weaker stock prices could keep them from hiking rates. He qualifies the statement by emphasizing they want to see the persistence of said market conditions. They do not want to see stock prices and bond yields “fluctuating back and forth.“

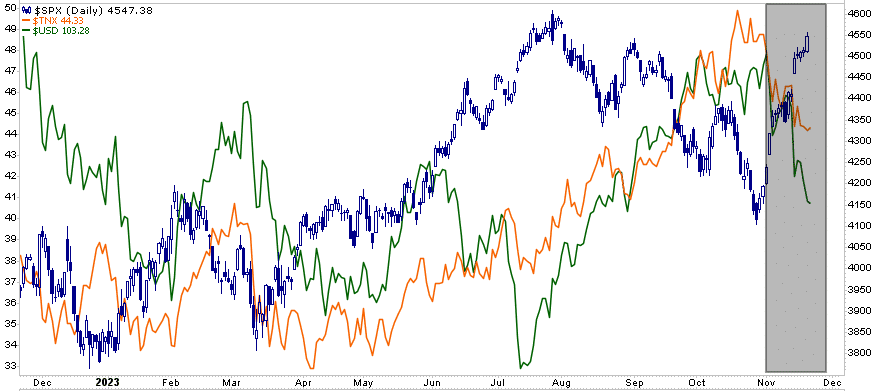

Since the Fed meeting, stocks have risen about 10%, ten-year note yields are nearly .50% lower, and the dollar index has fallen 3%. Needless to say, tighter financial conditions, as the Fed defines, have not been persistent. Will easier financial conditions force the Fed to revert to its more hawkish tone and try to persuade higher interest rates and lower stock prices?

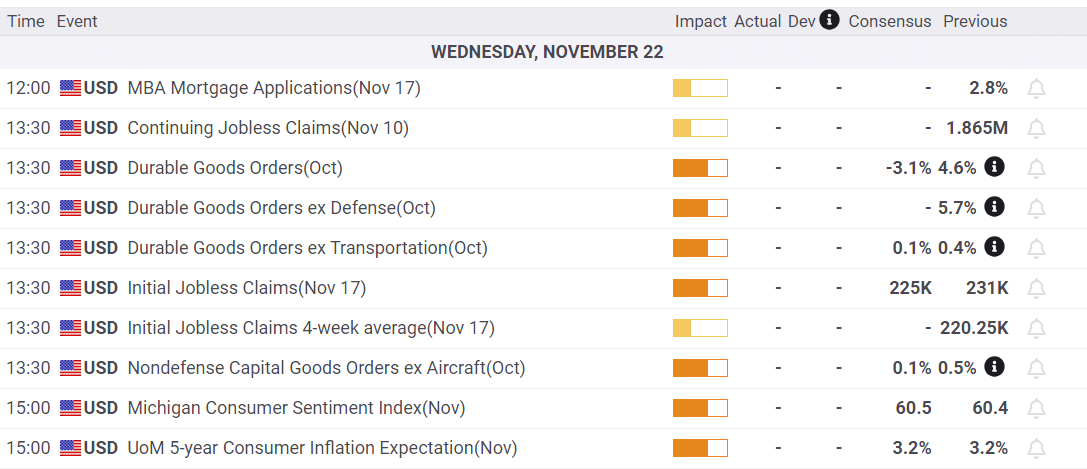

What To Watch Today

Earnings

Economy

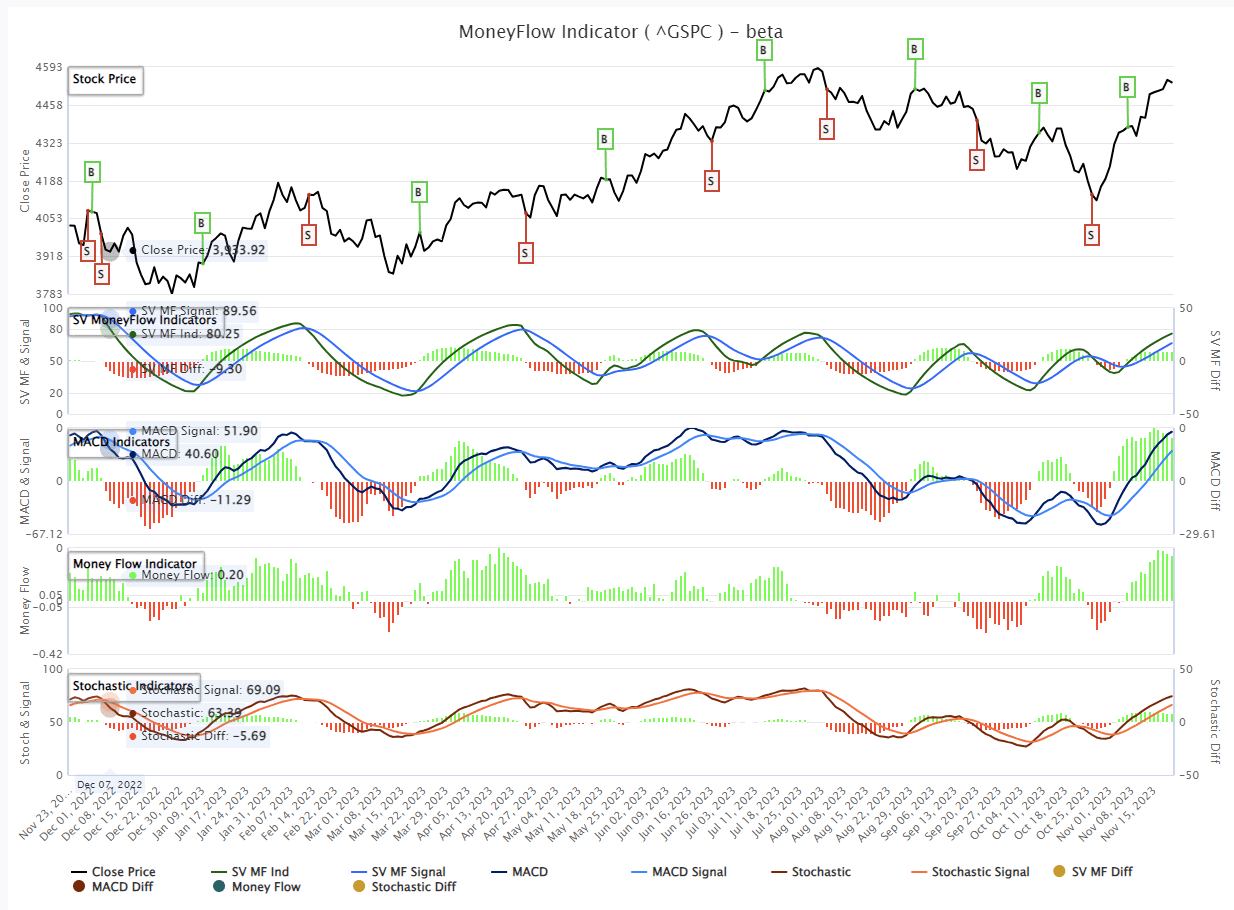

Market Trading Update

As noted in Monday’s commentary, while the market could certainly pull back to the lower of the “Bollinger bands,” corrections will likely remain confined to the 50-dma. As such, we will want to use those opportunities to trade portfolios into higher levels of equity exposure. With the market more overbought and extended currently, we want to remain cautious about committing our cash reverses to the broad market more aggressively.

Yesterday, the market pulled back a smidge but did little to reduce the current overbought conditions. As shown in our MoneyFlow analysis, all of our current “buy” indicators remain and are stretched. A pullback will occur at some point, just as it did last December before the Santa Claus Rally ensued. Given the more extended and overbought conditions, we continue to suggest rebalancing portfolio risk as needed, but caution against getting to underexposed given the current bullish bias to the market.

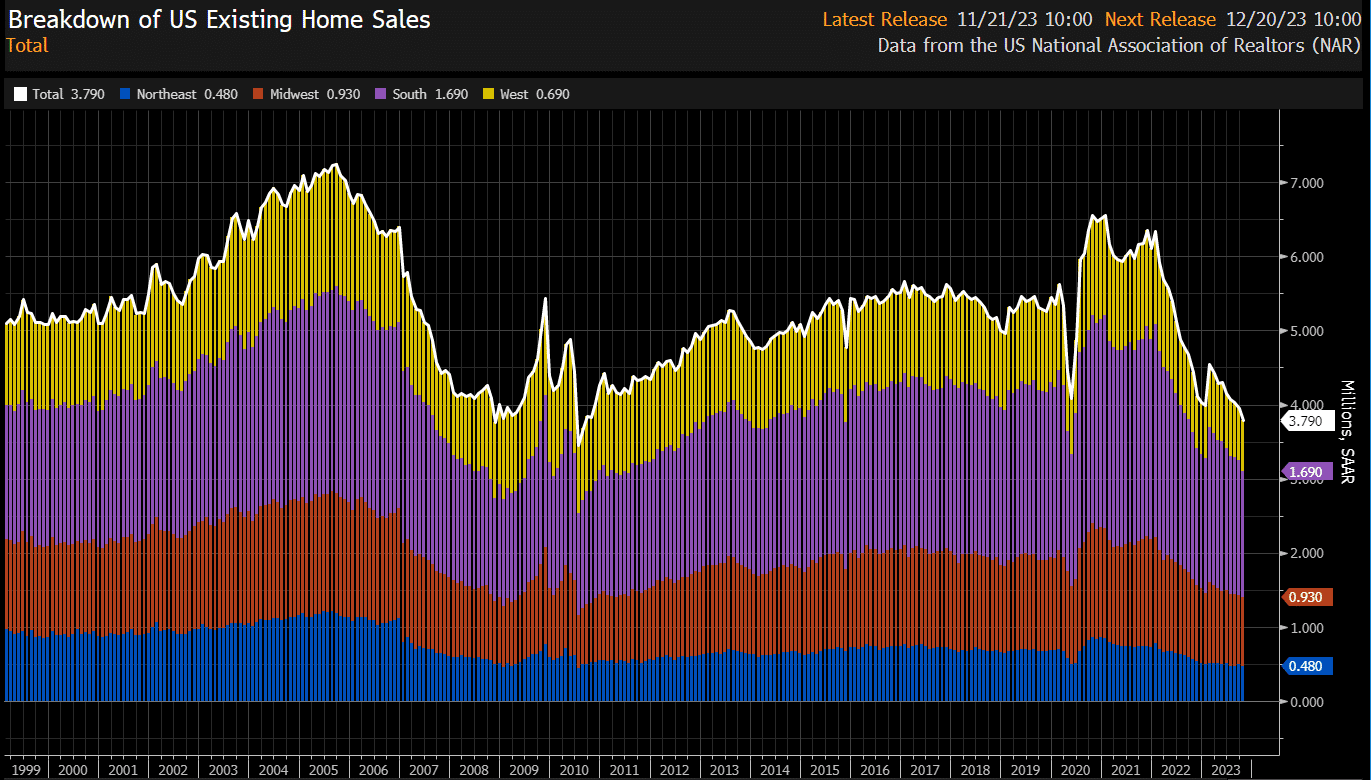

Existing Home Sales Continue To Fall

Existing home sales fell -4.1% in October to a seasonally adjusted annual rate of 3.79 million. That’s the lowest reading in over ten years, as shown below. For perspective, consider the current 3.79 million home sales are lower than during the first months of the pandemic. The data is for homes that settled in October when mortgage rates peaked near 8%. The next few existing home sales reports will help the Fed ascertain if the recent decline in rates is boosting the housing market.

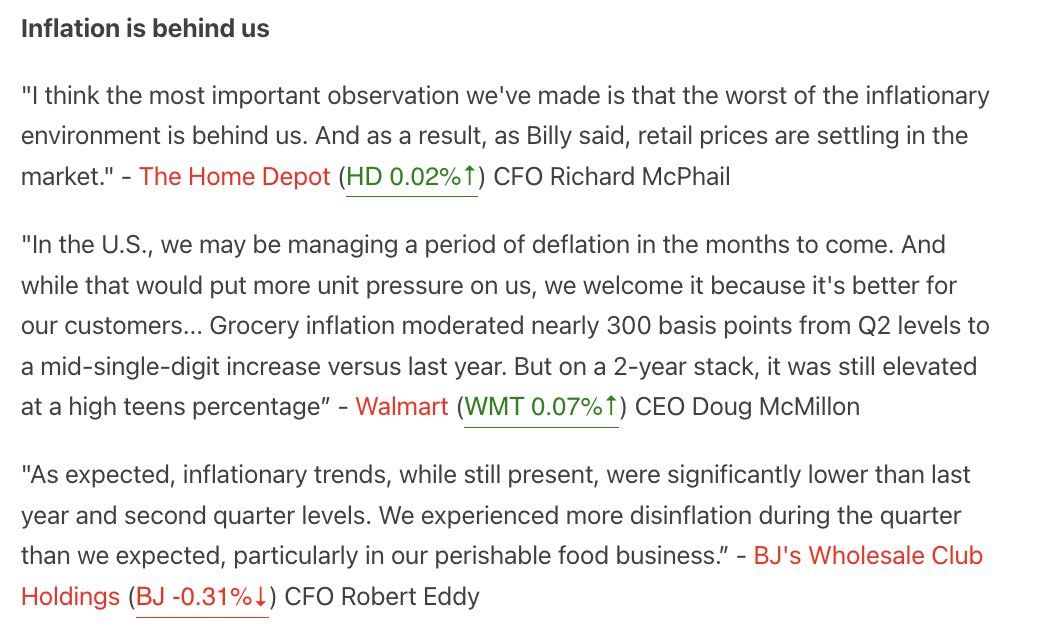

Fickle Consumers And Lower Inflation Weigh On Retail Sales

On Tuesday, Kohls, Best Buy, and Lowes posted weaker-than-expected sales. The companies make it clear that consumers have become more financially constrained. Consequently, equity analysts are starting to downgrade holiday sales forecasts. In their press releases and investor calls, the three companies mention deal-driven fickle consumers. High inflation and increased debt levels are certainly causing consumers to reduce spending. Over the last couple of months, the overriding message from these retailers and others alludes that consumers are not as in good financial health as in prior quarters. Best Buy is “prepared for a customer who is very deal focused with promotions and deals for all budgets…” Lowes opened 5% lower as comparable sales fell 7.4% “due to a decline in DIY discretionary spending…”

Retailer sales are a function of the financial condition of consumers and, often overlooked, inflation. In particular, sales figures over the last two years were significantly boosted due to higher prices. As such, comparisons to prior quarters’ sales become difficult.

The graphic below from The Transcript shows that three of the largest retailers appear confident that high inflation is in the past. Will price changes normalize or keep falling? If the latter, as Walmart warns, sales at retailers may continue to decline. Further, if retailers sense deflation, they are likely to keep inventories low. The consequence will be weaker sales for the manufacturers of goods.

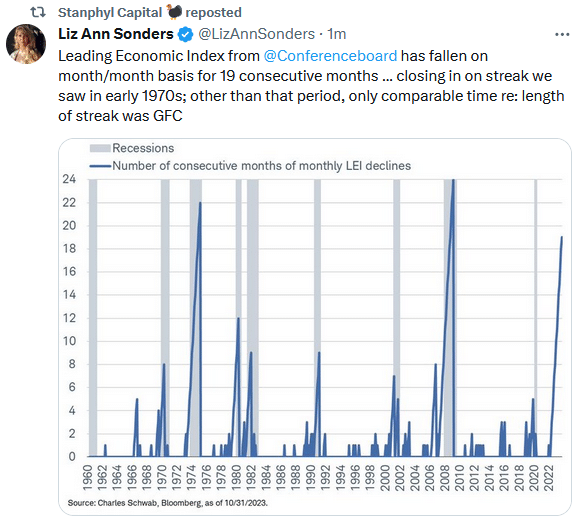

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read