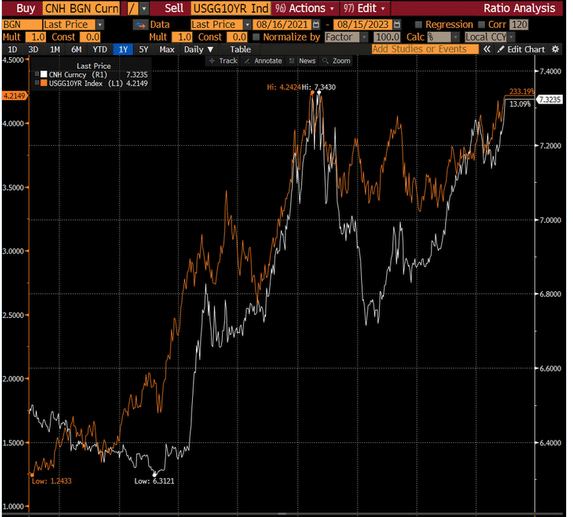

U.S. Treasury yields have been rising recently on varied concerns. One such worry is that China will sell some of its $835 billion stash of U.S. Treasury securities to help bolster its weakening currency, the yuan (CNH). As we share below, China’s yuan and ten-year Treasury note yields have correlated well since 2021. Like U.S. Treasuries reaching yield levels from 15 years ago, the yuan is also approaching its lowest levels versus the U.S. dollar since 2007. Driving the weakness is poor economic growth. Unlike the economic surge following the U.S. reopening of the economy, China’s, which occurred much later, has done little to revitalize growth. On Monday, China unexpectedly cut rates to spur activity, but it weakened the yuan.

Such presents China’s conundrum. They can further stimulate the economy with lower rates and fiscal spending but risk further weakening the yuan. Importantly, a weaker yuan promotes capital outflow from China, which further weakens its currency. Therefore China must balance economic goals with capital concerns. China would need to sell U.S. Treasury securities to strengthen the yuan and address capital concerns. However, doing so would impair export activity. Further, they run the risk that higher U.S. yields, the result of their selling, would entice more capital outflows from China. They have difficult choices ahead that will affect the global assets markets.

What To Watch Today

Earnings

Economy

- No notable economic releases

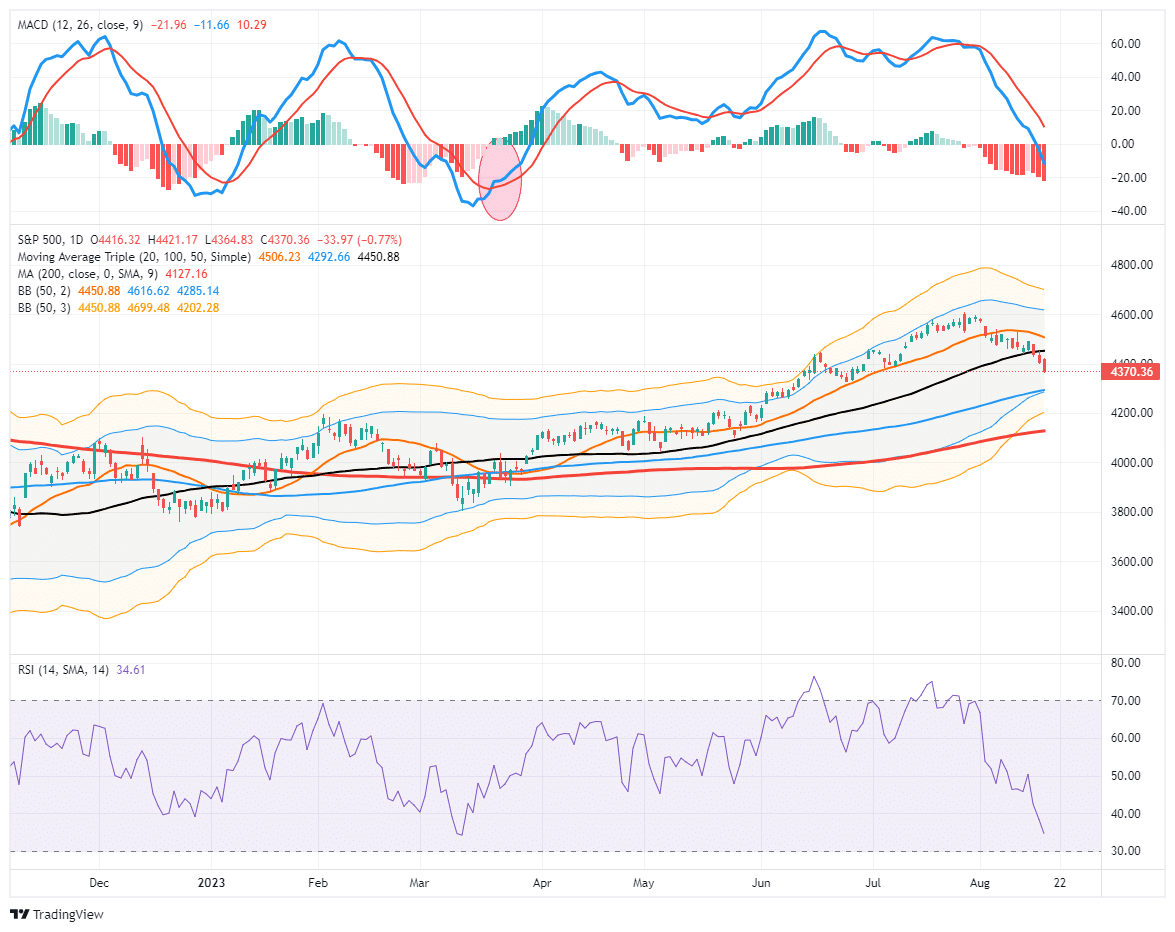

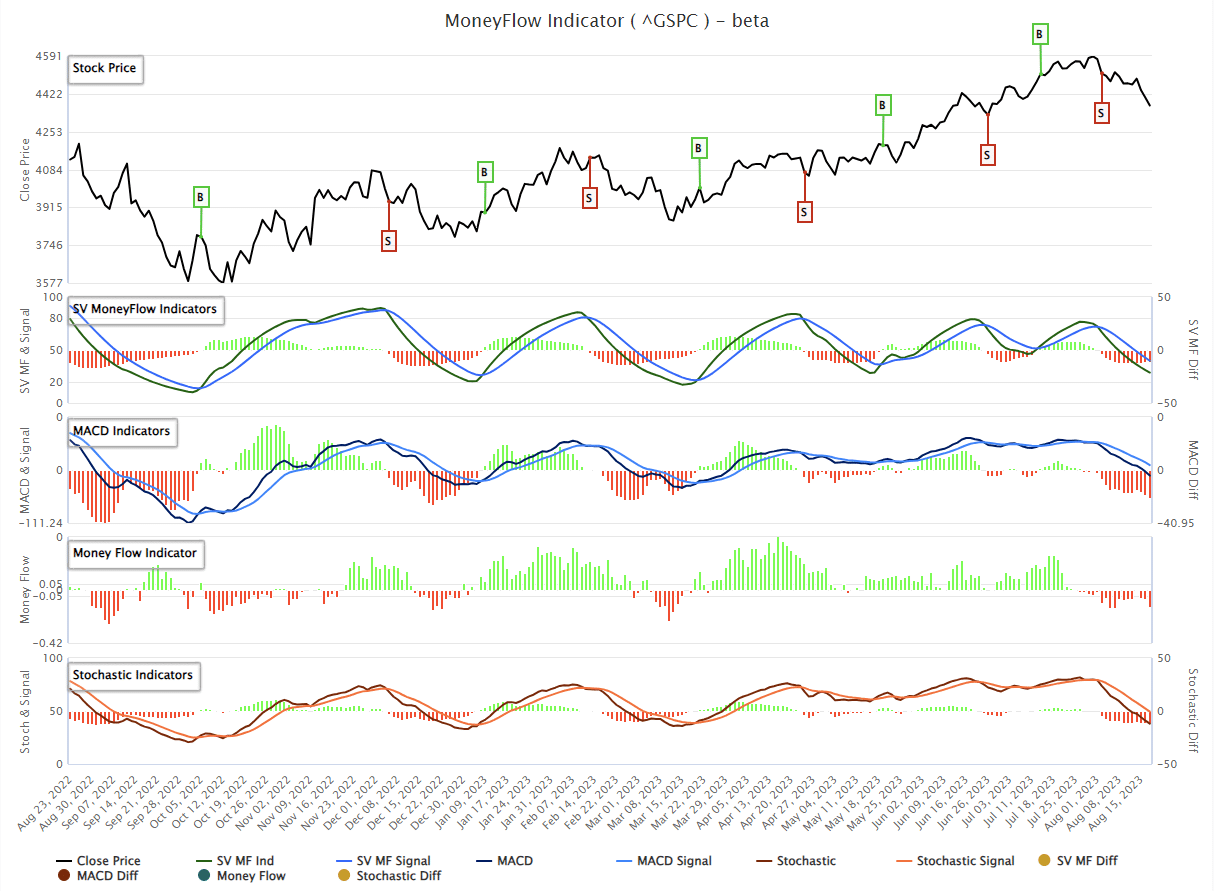

Market Trading Update

The market selloff continued on Thursday, and while the market is oversold enough to bounce, the break of the 50-DMA has been decisive enough to suggest that the 100-DMA is the next logical support level. The MACD, as noted previously, is firmly entrenched in its “sell signal” but is reaching levels that are more normally bottoms during bullish cycle corrections. While I would expect a rally as soon as today, that rally will likely remain contained below the 50-DMA for now. It will be unsurprising for the market to work its way lower over the next month towards that lower level of support. Use rallies to rebalance risk as needed.

Furthermore, our MoneyFlow indicator is also reaching more oversold levels. If the MACD and the MoneyFlow indicator begin to turn positive, such will be the time to more aggressively add exposure for the next market trading cycle. As noted yesterday, the current correction remains very orderly and was needed to fuel a rally into year-end. How we close the trading week will be an important clue for next week.

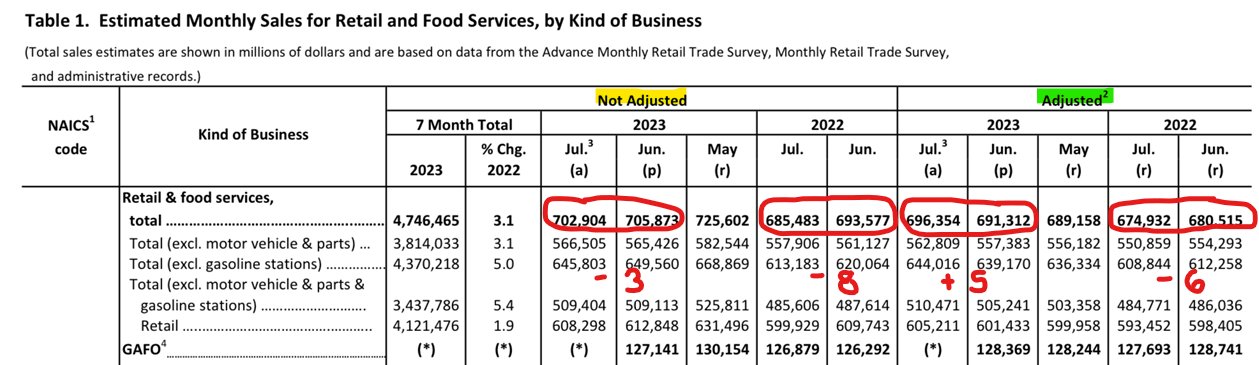

Was Tuesday’s Retail Sales Flawed?

The answer is yes and no. We start with a Tweet from Steph Pomboy. She pointed out an inconsistency after Tuesday’s much stronger-than-expected retail sales report. As we share, she notes that seasonal adjustments made to the data seem peculiar.

In round numbers, last July sales fell -$8b, which was reported as a -$6b decline after seasonal adjustment. That implies the seasonal assumption was for a -$2b decline. This year July sales fell -$3b before adj. Had last year’s seasonal factor (of -$2b) been used, the headline would have been -$1b (as it was $1b weaker than a normal July). Instead, sales were reported UP +$5b. the seasonal factor is actually calculated as a %, not $…but you get the gist.

Is Stephanie correct that this year’s seasonal adjustment vastly differs from last year’s? We do the math a little differently and agree and disagree with her.

Over the last five years, the Census Bureau applied a -1.96% seasonal adjustment to July’s non-adjusted retail sales data. This year the adjustment was only -0.93%. Had the average seasonal adjustment been used, adjusted retail sales would have been 689,127, representing a 0.4% decline in retail sales and not the 1% gain. While such may seem strange, it’s not. Seasonal adjustments shift based on when holidays fall within a month and other seasonal factors.

Over time, the adjusted and non-adjusted data tend to be identical as said adjustments even out. For example, for all of 2022, the seasonally adjusted number was only 0.1% above the non-seasonally adjusted data. Through July 2023, the seasonally adjusted data is running 1.6% greater than the actual data. While the July data adjustment may seem off per Steph’s analysis, the total +1.6% adjustment thus far for 2023 is on par with the last ten years. Consequently, seasonal adjustments should weaken actual retail sales in the coming months. But, it does not appear the Census Bureau is deliberately making retail sales look better than they are.

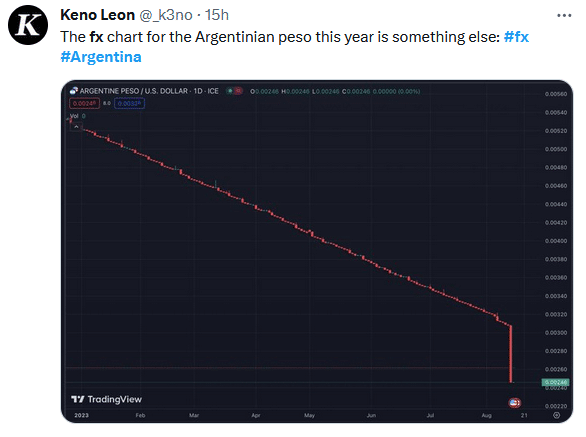

DeDollarization- Argentina Reminds Us Why It’s Not Likely

We have written a few times on de-dollarization and why we think the odds of the U.S. dollar losing its reserve currency anytime soon are zero. In April 2023, we wrote two articles on the topic- The Dollar’s Death, Not So Fast, and Four Reasons The Dollar Is Here To Stay.

The summary of both articles: there is no alternative. In May, we provided an example in a Daily Commentary entitled Saudi Arabia Says Phooey to Dedollarization. To wit:

For a country that seems intent on getting rid of dollars, they are as attached to dollars as any country. Even more interesting, Saudi Arabia has the one export almost every country needs, oil. Of all countries, Saudi Arabia has the most leverage in dictating trade terms away from the dollar. Why are they talking loudly about de-dollarization but further tieing themselves to the dollar’s value? Simply, there is no viable large-scale alternative.

Argentina reminds us of what happens when a country tries to move away from the U.S. dollar. Argentina is struggling to pay its debts. Its currency is collapsing as a result. To potentially remedy the situation, they recently swapped their currency with China for the yuan. Per Reuters:

BUENOS AIRES, June 2 (Reuters) – Argentina has signed a deal to renew its currency swap line with China and double the amount it can access to near $10 billion, the South American country’s central bank said in a statement on Friday, a boost to its dwindling foreign currency reserves.

As a result, Argentina now has a significant portion of its reserves in yuan. Unfortunately, the IMF and other debt holders will not accept yuan. Argentina can default on its dollar debts but will be largely shut out of dollar trade markets in the future and become heavily dependent on China. Odds, they are unwilling to deal with the economic ramifications and potential shortages of critical imports of ditching the dollar.

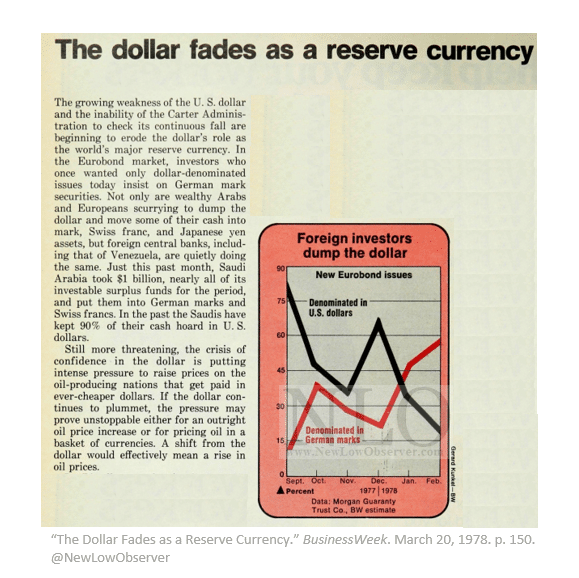

De-dollarization is not a new warning. To wit, consider the Business Week headline below from 1978.

More on Argentina

Javier Milei, a staunch libertarian, is currently the front-running candidate to become Argentina’s next president. One would think a libertarian would want to further separate Argentina from the dollar. Such is not the case. Per the New York Times:

Javier Milei, who wants to abolish the central bank and adopt the U.S. dollar as Argentina’s currency, is now the front-runner in the fall general election.

Milei touts a lot of non-traditional economic plans to resurrect Argentina’s economy, but he aims to make the U.S. dollar Argentina’s official currency. Milei understands there is no viable alternative!

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read