The financial world has been buzzing nervously about the rapidly rising risk of a recession as warning signs mount. Though many mainstream economists and commentators are finally starting to concede that a recession in the next year or two is likely, almost all of them downplay the likely severity of the coming recession by saying “but it will be short-lived!” and “we’re due for a healthy slowdown after a ten year expansion!” (economists were saying the same thing in 2006 and 2007 too). My view, however, is that virtually everyone is underestimating the tremendous economic risks that have built up globally during the past decade of extremely stimulative monetary policies. I believe that these unknown risks are going to rear their ugly heads with a vengeance in the coming recession and that heavily indebted governments will have far less firepower with which to rescue their economies like they did during the 2008 to 2009 Global Financial Crisis.

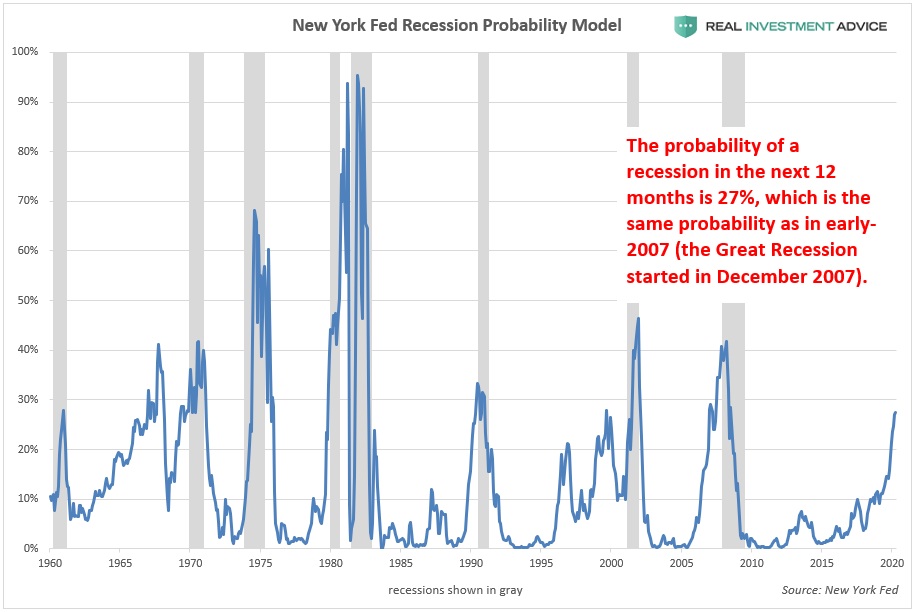

According to the New York Fed’s very accurate yield curve-based recession probability model, there is a 27% probability of a U.S. recession in the next 12 months. The last time that recession odds were the same as they are now was in early-2007, which was shortly before the Great Recession officially started in December 2007 – talk about too close for comfort!

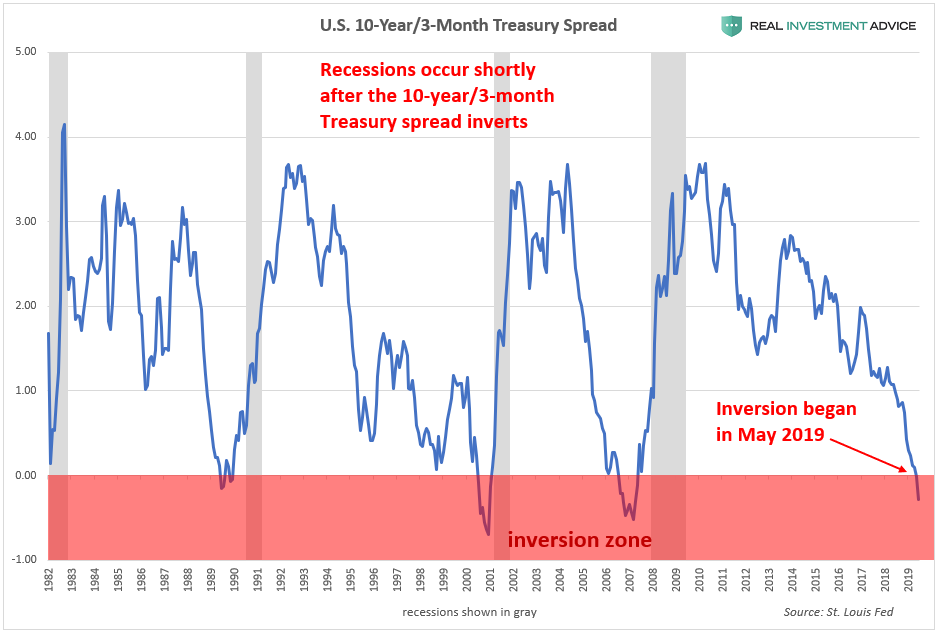

The New York Fed’s recession probability model is based on the 10-year and 3-month Treasury yield spread, which is the difference between 10-year and 3-month Treasury rates. In normal economic environments, the 10-year Treasury yield is higher than the 3-month Treasury yield. Right before a recession, however, this spread inverts as the 3-month Treasury yield actually becomes higher than the 10-year Treasury rate – this is known as an inverted yield curve. As the chart below shows, inverted yield curves have preceded all modern recessions. The 10-year and 3-month Treasury spread inverted in May, which started the recession countdown clock.

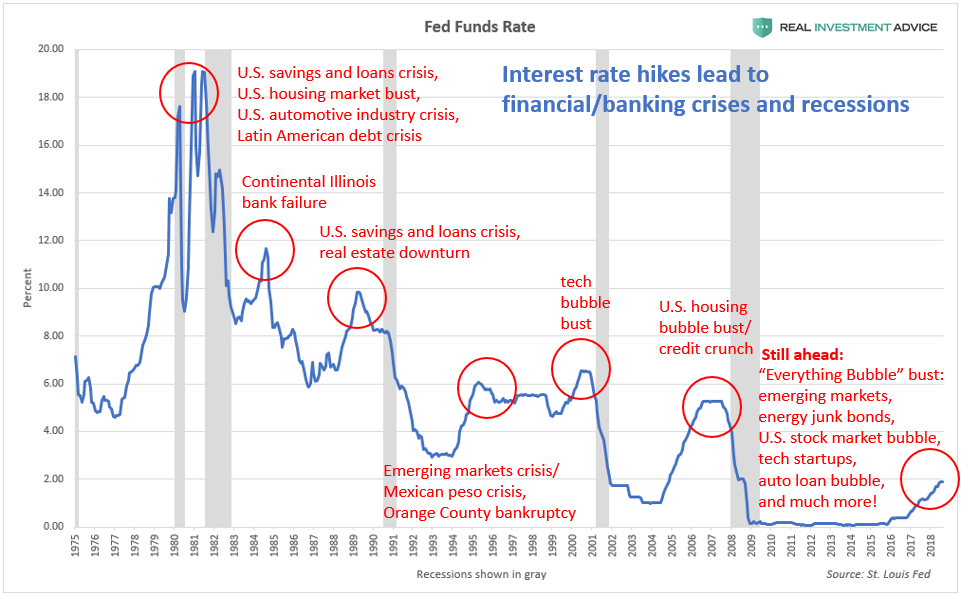

The coming recession is likely to be far more severe than the majority of economists expect because global interest rates have been held at record low levels for a record period of time since the Great Recession, which has completely distorted the global economy and created many dangerous bubbles that most people have no clue even exist (and that includes most professional economists!). Bubbles form during periods of relatively low interest rates and burst when rates rise – that’s why most modern financial crises and recessions have occurred, as the chart below shows. The dot-com and housing bubbles both formed during low interest rate periods and burst when rates started to rise.

Make no mistake: numerous bubbles have formed during the low interest rate period of the past decade and there is no way of escaping their ultimate popping. These bubbles are forming in global debt, China, Hong Kong, Singapore, emerging markets, Canada, Australia, New Zealand, European real estate, the art market, U.S. stocks, U.S. household wealth, corporate debt, leveraged loans, U.S. student loans, U.S. auto loans, tech startups, shale energy, global skyscraper construction, U.S. commercial real estate, the U.S. restaurant industry, U.S. healthcare, and U.S. housing once again. There are likely even more bubbles than I listed – we just won’t know until they all burst. As Warren Buffett once said “only when the tide goes out do you discover who’s been swimming naked.” I believe that the current bubble situation, when looked at globally, is even worse than it was before the 2008 Global Financial Crisis – that’s why the coming crisis is actually likely to be far worse than 2008. How’s that for an unpopular opinion?!

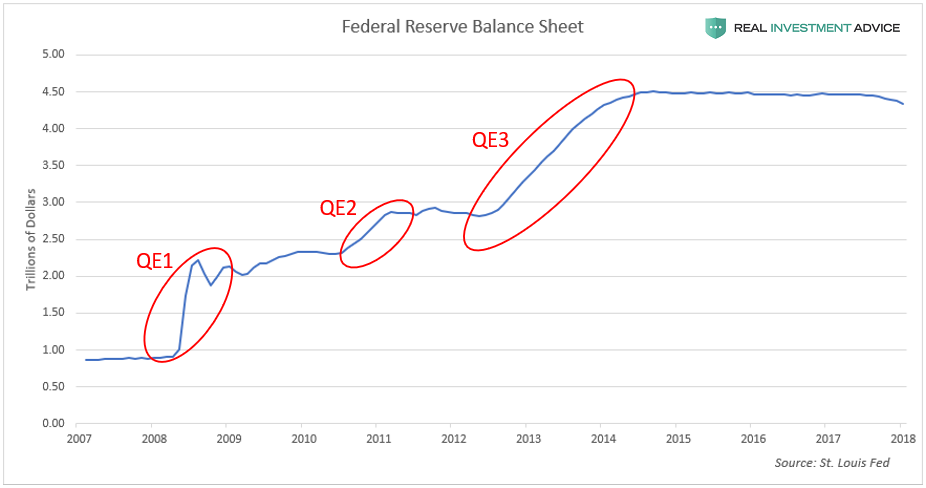

The global bubbles that have formed in the past decade have been exacerbated by an unconventional central bank policy called quantitative easing or QE. QE basically entails creating new money for the purpose of pumping liquidity into the financial system and boosting asset prices. The chart below shows how the U.S. Federal Reserve’s balance sheet grew with each QE program in the past decade (the Fed’s balance sheet grows as it buys assets like bonds to pump more money into the financial system). Of course, the Fed wasn’t the only central bank that conducted QE programs in the past decade – most major central banks did as well, which created a tremendous ocean of liquidity that helped to inflate the numerous bubbles around the world.

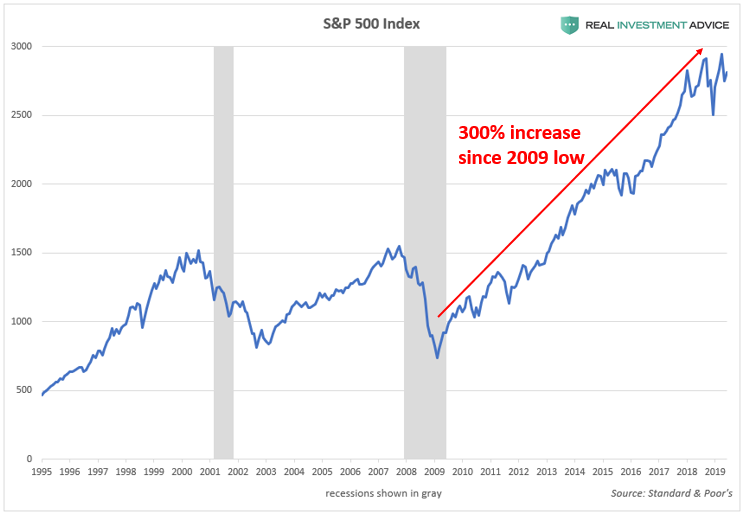

As a result of the Fed’s ultra-low interest rates and QE programs, the U.S. stock market (as measured by the S&P 500) surged 300% higher in the past decade:

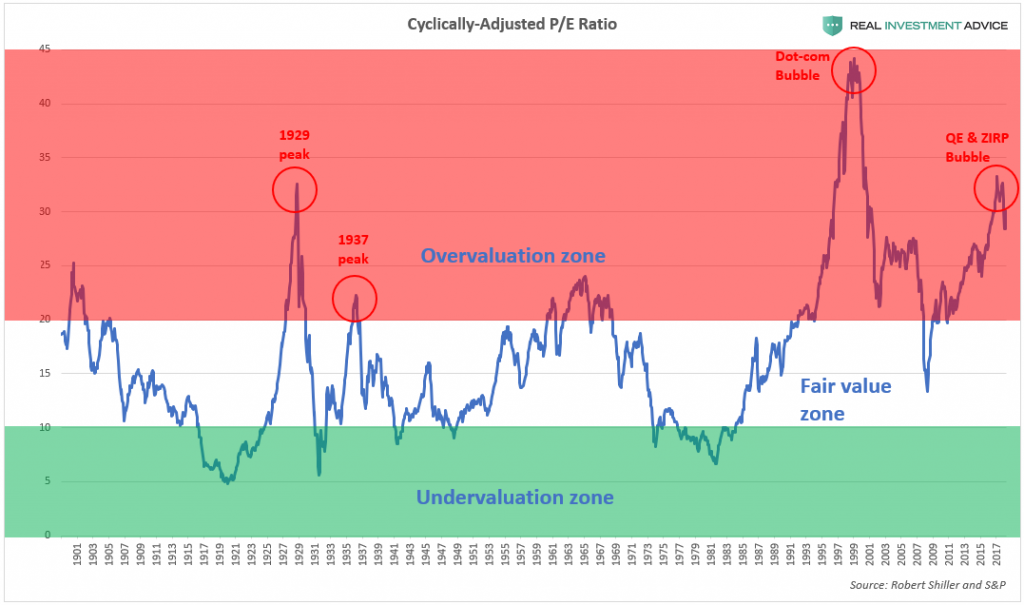

The Fed’s aggressive inflation of the U.S. stock market caused stocks to rise at a faster rate than their underlying earnings, which means that the market is extremely overvalued right now. Whenever the market becomes extremely overvalued, it’s just a matter of time before the market falls to a more reasonable valuation again. As the chart below shows, the U.S. stock market is nearly as overvalued as it was in 1929, right before the stock market crash that led to the Great Depression.

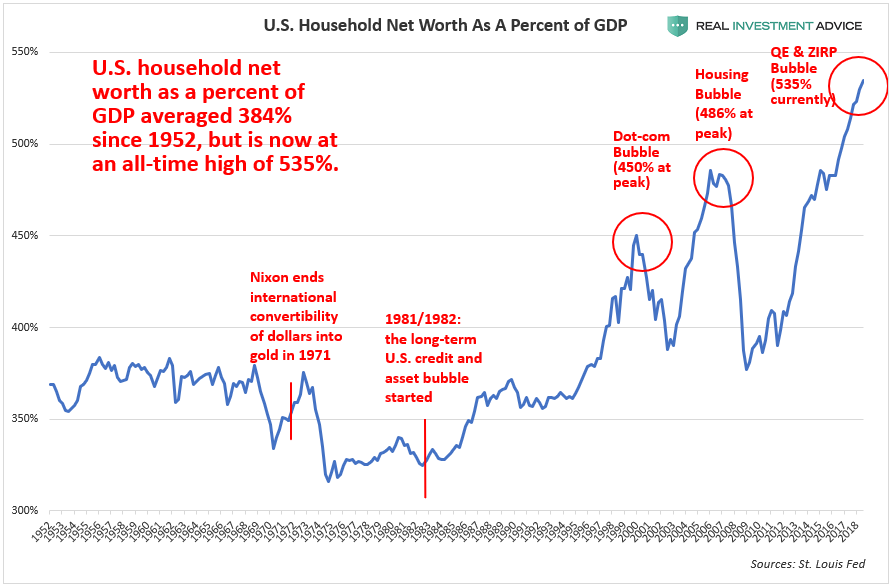

The Fed’s aggressive inflation of U.S. stocks, bonds, and housing prices has created a massive bubble in household wealth. U.S. household wealth is extremely inflated relative to the GDP: since 1952, household wealth has averaged 384% of the GDP, so the current bubble’s 535% figure is in rarefied territory. The dot-com bubble peaked with household wealth hitting 450% of GDP, while household wealth reached 486% of GDP during the housing bubble. Unfortunately, the coming household wealth crash will be proportional to the run-up, which is why everyone should be terrified of the coming recession.

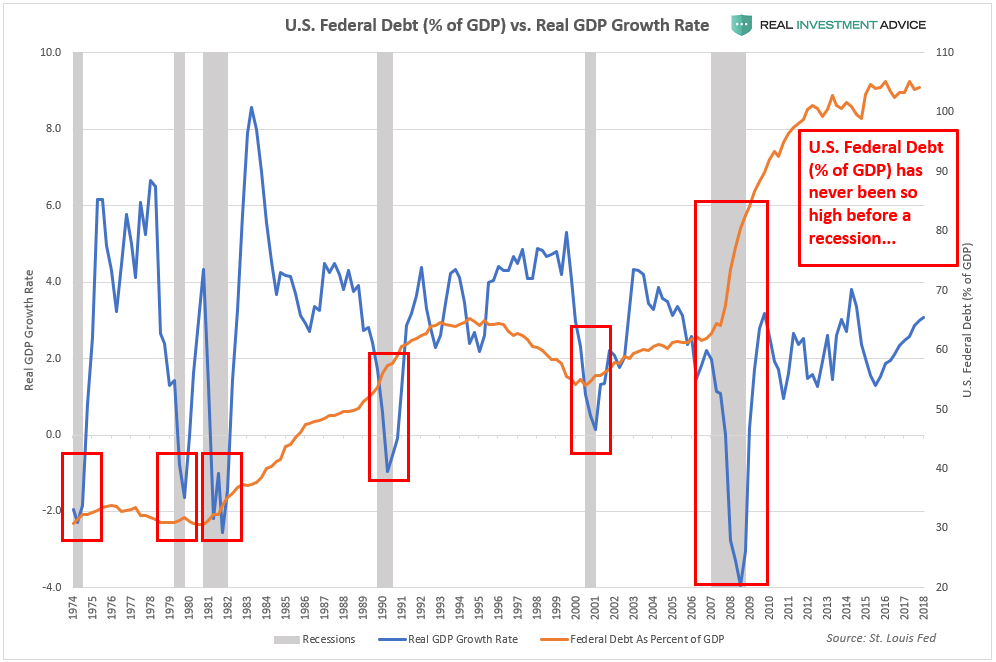

Not only have more bubbles inflated around the world than in the mid-2000s, but governments are far more indebted now (government debt is now at 80% of global GDP), which means that they have much less firepower with which to rescue their economies in the coming crisis. In the case of the U.S., federal debt as a percent of GDP has never been so high before a recession (it’s currently at 100% of the GDP vs. 62% before the Great Recession), so we are truly in unprecedented times.

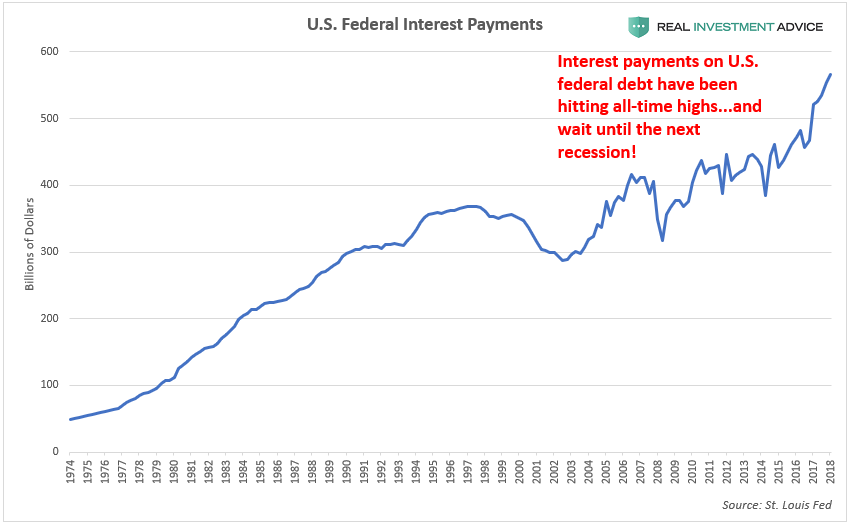

Though interest rates have been at ultra-low levels for the past decade, the sheer amount of U.S. federal debt (over $22 trillion) is the reason why interest payments have spiked over the past couple years. To make matters worse, this debt will eventually need to be refinanced at higher interest rates, which means that interest payments will rise even more. Another recession combined with another ramp-up of federal debt and ensuing debt downgrades will cause these payments to rise even more. This is how sovereign debt crises happen.

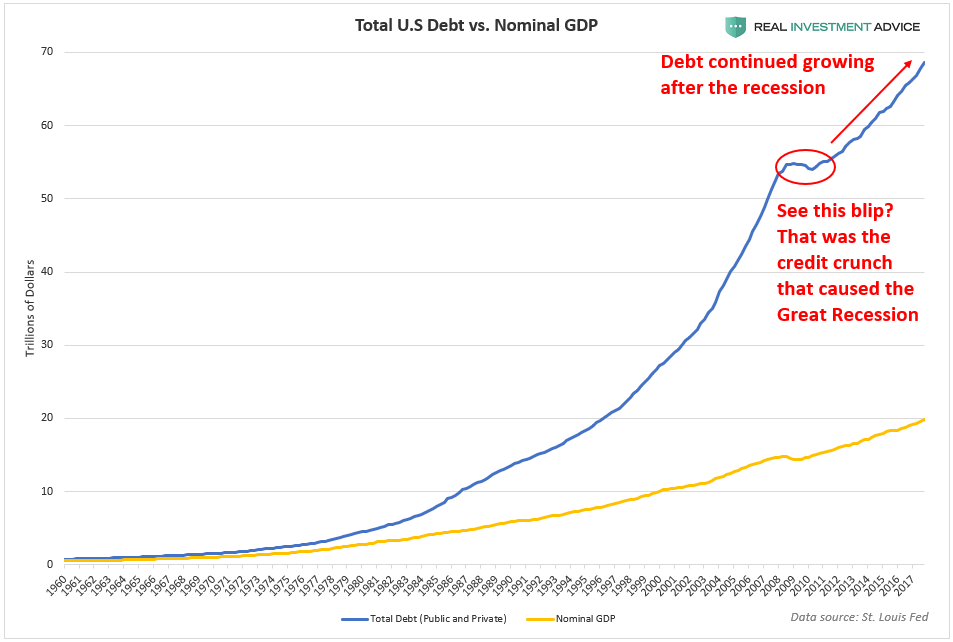

Though the Great Recession was essentially caused by a debt crisis, both public and private U.S. debt have continued to grow since then. The so-called U.S. economic “recovery” didn’t occur in spite of the post-Great Recession debt growth – it occurred because of that very debt growth. What most people don’t understand is that debt creates temporary economic growth by borrowing from the future. We’re making the same mistakes that we made before 2008, yet expecting different results. Unfortunately, the outcome will be the same as in 2008, if not worse, due to the even higher debt load we now have.

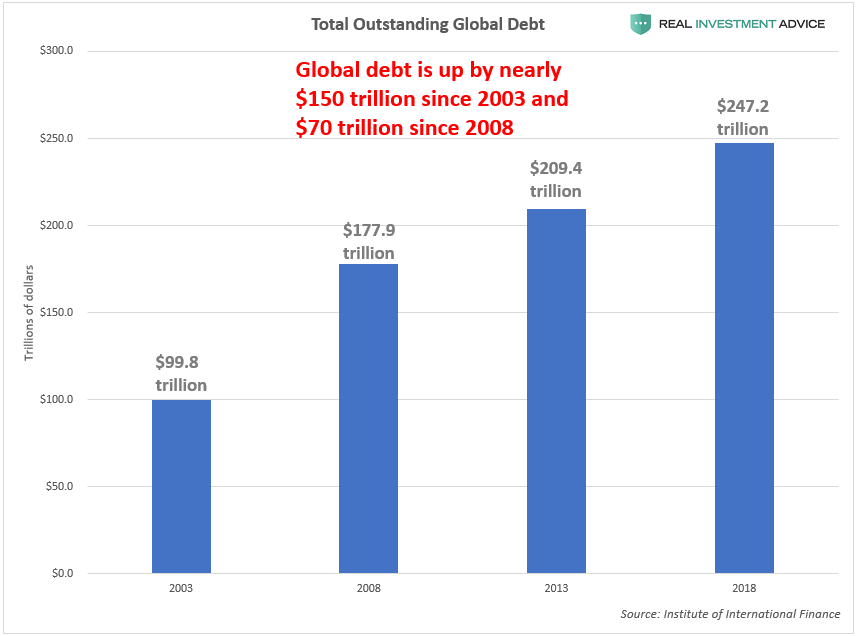

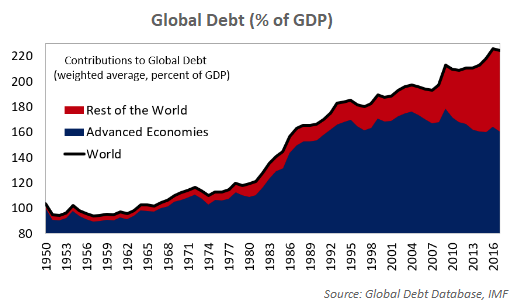

The world has been on an unprecedented debt binge in the past several decades. Global debt is up by $150 trillion since 2003 and $70 trillion since 2008. As bad as the 2008 crisis was, we now have an addition $70 trillion worth of debt to contend with in the coming crisis.

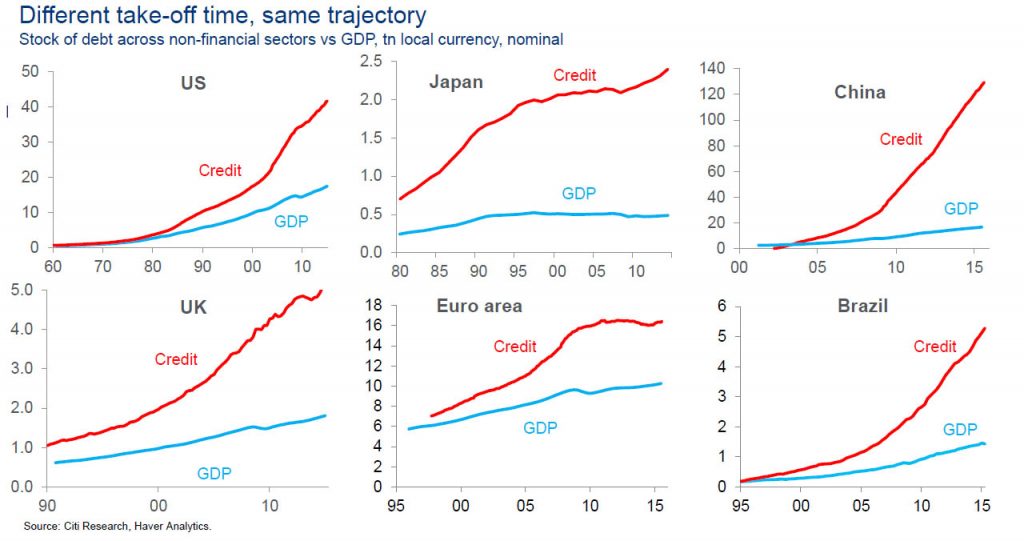

In virtually every major economy, debt has grown at a much faster rate than the underlying GDP in the past several decades:

As a result of debt growing faster than the underlying economies themselves, global debt as a percent of GDP has increased quite substantially in the last several decades. The global economy is now saturated with debt, which will make it much harder to grow out of the coming recession by taking on even more debt like we did in the past.

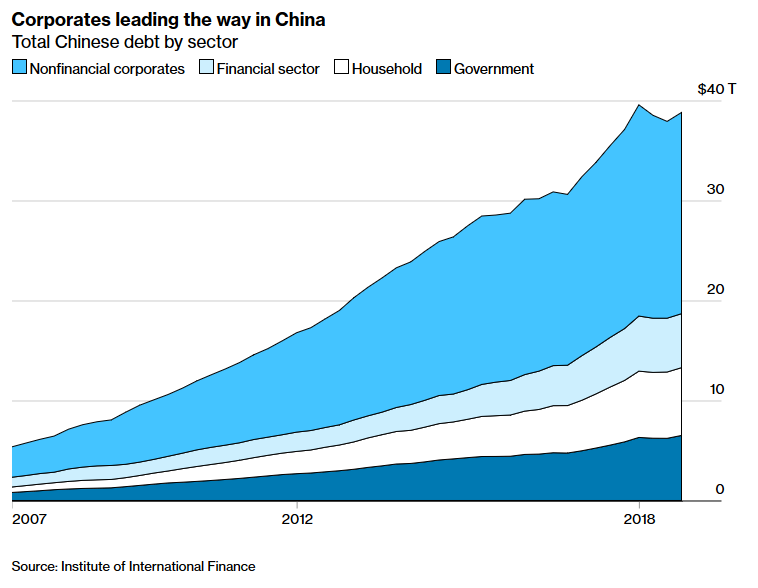

In particular, China has binged harder on debt than any other country since the Great Recession. China’s gigantic debt mania of the past decade greatly helped to boost its economic growth, which made it one of the most important global engines of economic growth in turn. Essentially, China’s debt bubble helped to carry the global economy for the last ten years. Unfortunately, China is nearly tapped out and is heading for a bust of its own, which will drag down the entire global economy with it. There will be no “new Chinas” to binge on debt and carry the global economy after the next global financial crisis – no other country has the capacity to throw such a wild debt party.

To summarize, the vast majority of economists and commentators are assuming that the coming recession will be a garden-variety recession – a mere ebb of the business cycle. They’re expecting a walk in the park relative to the massive debt and bubble tsunami that I see on the horizon. Remember, this is the exact same crowd who downplayed or completely missed the warning signs of the U.S. housing bubble and global financial crisis as well. Apparently, this group still has not learned their lesson, so they will be taught it once again – and we’re all going to suffer as a result of their ignorance. If you are not terrified by the thought of the coming recession, you have no clue about the tremendous risks that have built up in the past decade. The risk of a full-blown global depression cannot be discounted.

Also Read