A quiet start to the morning in the aftermath of hurricanes Ida and Powell. Prices of Crude oil and natural gas rose on the open last night with over 90% of Gulf of Mexico production shut-in. This morning both energy products are set to open flat. Equities and bonds are also looking to open unchanged in the aftermath of Powell’s dovish speech.

Click HERE to receive our daily market commentary in your email every morning.

What To Watch Today

Economy

- 10:00 a.m. ET: Pending home sales, month-over-month, July (0.3% expected, -1.9% in June)

- 10:30 a.m. ET: Dallas Fed Manufacturing Activity index, August (23.0 expected, 27.3 in July)

Earnings

- 4:05 p.m. ET: Zoom Video Communications (ZM) expects to report adjusted earnings of $1.16 per share on revenue of $990.24 million

Politics

- President Biden is to have meetings and briefings on Afghanistan and Hurricane Ida throughout the day. Biden spent Sunday meeting with the families of American service members killed in Afghanistan.

- FEMA and Louisiana officials will give updates on the damage caused by Ida, one of the most powerful storms to ever hit the U.S. Ida made landfall on Sunday, knocking out power to all of New Orleans.

Courtesy of Yahoo!

Market Outlook To Start The Week

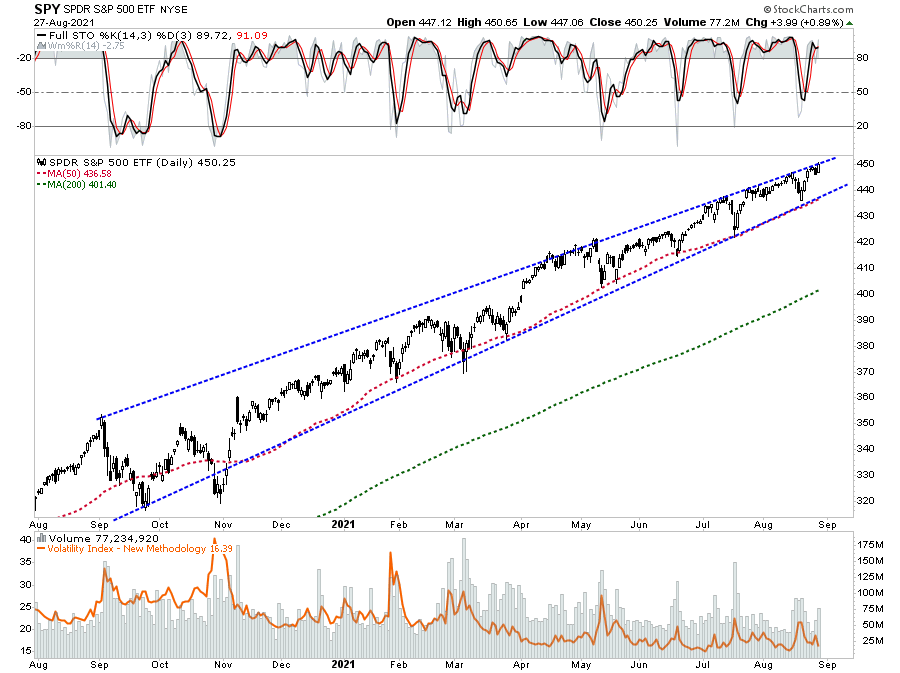

The bulls rushed back into the market on Friday. Heading into this week, there is little upside likely as the market is within an upward trending channel since last September.

With the market very overbought short-term, volatility compressed, and volume and breadth weak, it is likely we may see additional choppiness in price action again. As noted in this past weekend’s #RealInvestmentReport:

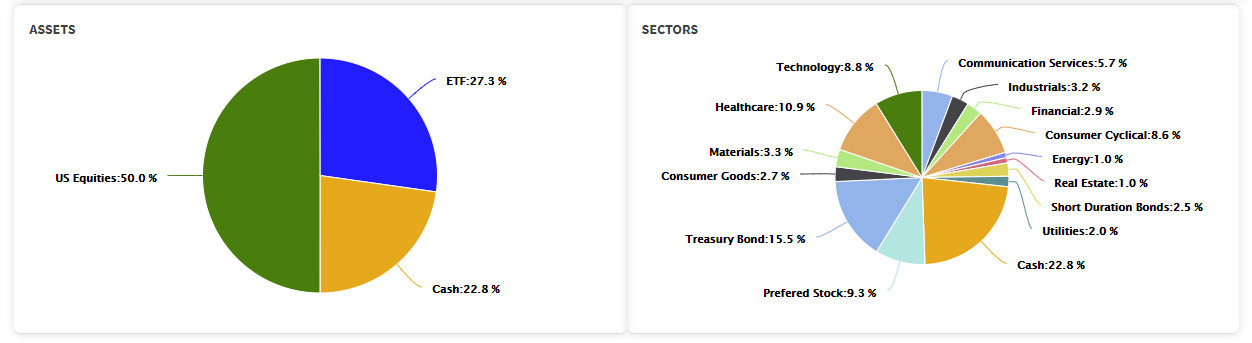

“Heading into the Jackson Hole Summit meeting and not knowing how the market would react, we made some adjustments to our portfolios on Thursday. As we discussed with our RIAPRO subscribers, our goal is to reduce the “volatility” of the portfolio, thereby reducing risk without significantly sacrificing performance. So even though we took profits in stocks like WOOF and replaced FANG with XOM, we held equity allocations essentially flat at 50%.”

“We still hold a slightly higher cash balance in the equity sleeve (~10%) and the fixed income sleeve (~10%). We use the cash as a risk hedge against an equity draw and “shorten duration” in the bond allocation. While we were previously increasing the duration of our bond portfolio to capture the decline in rates, we are holding cash to add longer-duration bonds on upticks in rates.”

Ambiguity

Investors were fretting the Jackson Hole symposium would result in a firm timetable for an aggressive tightening campaign beginning as early as September. As seen in Powell’s comments below, what it got was more ambiguity around timing and amounts. After Powell’s speech, Fed Governor Harker was equally vague: “The Fed has reached an agreement that tapering will begin this year.”

The Oracle Speaks

Chairman Powell’s much-awaited speech is being met with optimism in the markets. In particular, the following line is assuring investors the Fed will not be aggressive in tapering QE. In regards to premature tightening he says: “Today, with substantial slack remaining in the labor market and the pandemic continuing, such a mistake could be particularly harmful.“

Below are two key segments from his speech:

- My view is that the “substantial further progress” test has been met for inflation. There has also been clear progress toward maximum employment. At the FOMC’s July meeting, I was of the view, that if the economy evolved broadly as anticipated, it could be appropriate to start reducing the pace of asset purchases this year. The intervening month has brought more progress in the form of a strong employment report for July, but also the further spread of the Delta variant. We will carefully assessing incoming data and the evolving risks. Even after our asset purchases end, our elevated holdings of longer-term securities will continue to support accommodative financial conditions.

- The timing and pace of the coming reduction in asset purchases will not be intended to carry a direct signal regarding the timing of interest rate liftoff. For which we have articulated a different and substantially more stringent test.

The Fed’s Preferred Measure Of Inflation – PCE

“Congress instructs the Federal Reserve to pursue monetary policies that promote maximum employment and price stability. The Federal Open Market Committee (FOMC) determined that “inflation at the rate of 2 percent, as measured by the annual change in the price index for personal consumption expenditures [PCE], is most consistent over the longer run with the Federal Reserve’s statutory mandate” for price stability.

The Federal Reserve Bank of Dallas trims mean PCE inflation measure to closely to the trend in overall PCE inflation. By omitting price changes for goods and services having the largest or smallest price movements in a given month, extreme values have less impact on the measured inflation rate, which arguably is a better measure of underlying inflation trends than the traditional core measure.

Federal Reserve

PCE, met expectations rising 0.4% in July. The level was 0.1% below the June reading. The year-over-year rate is 4.2%, which is more than double the Fed’s 2% inflation target. Importantly it suggests the Fed should be moving to tighten monetary policy. However, the trimmed-mean PCE was inline at 2% giving the Fed some “wiggle-room” for now, but likely not for long.

Tracing The Nikkei

Parabolic moves have been seen in many market indices throughout history. In the U.S. such was seen leading to the peaks in both 1929 and 1999. In Japan, it was the Nikkei rocketing higher to the peak in 1990. The importance of parabolic moves is they take years to recover from after they burst.

For the Nikkei, despite a QE program 3-times larger than the U.S. on a relative basis, it still remains below its previous peak 30-years later. As discussed in today’s blog post, the U.S. has a lot more in common with Japan than you might think.

Continuing Supply Line Problems

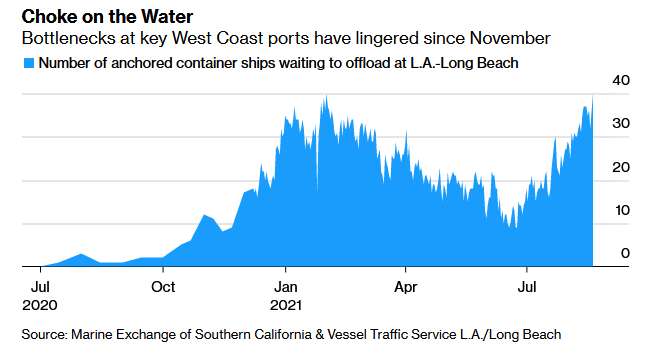

The Fed is complacent about fighting inflation as they believe it’s transitory. They consider temporary impediments to the production and shipping of goods but think these problems will resolve relatively quickly. Bloomberg has an interesting article out which leads one to believe the supply problems may last longer than the Fed believes: The World Economy’s Supply Chain Problem Keeps Getting Worse. Here are a few noteworthy lines and a graph:

- China’s determination to stamp out Covid has meant even a small number of cases can cause major disruptions to trade. This month the government temporarily closed part of the world’s third-busiest container port at Ningbo for two weeks. This was after a single dockworker was found to have the delta variant.

- “Port congestion and a shortage of container shipping capacity may last into the fourth quarter or even mid-2022,” said Hsieh Huey-chuan, president Evergreen Marine Corp. “If the pandemic cannot be effectively contained, port congestion may become a new normal.”

- The cost of sending a container from Asia to Europe is about 10 times higher than in May 2020. While the cost from Shanghai to Los Angeles has grown more than sixfold, according to the Drewry World Container Index.

Also Read