The question of Japanization in the U.S. continues as the S&P 500 tracks the Nikkei of 1980. An email question I received recently is worth discussing in more detail.

While it is easy to assume “this time is different,” the “Fed won’t let markets collapse,” or “insert your rationalization here,” there is a lot of history arguing with you. However, amid a speculative driven mania, it is certainly understandable to get an email such as this:

“Recently, the Nikkei was down ~4% premarket, and the BOJ stepped in to buy 70bn Yen of ETFs to save the market. The Fed is doing more than that monthly. So, how can the market ever go down?”

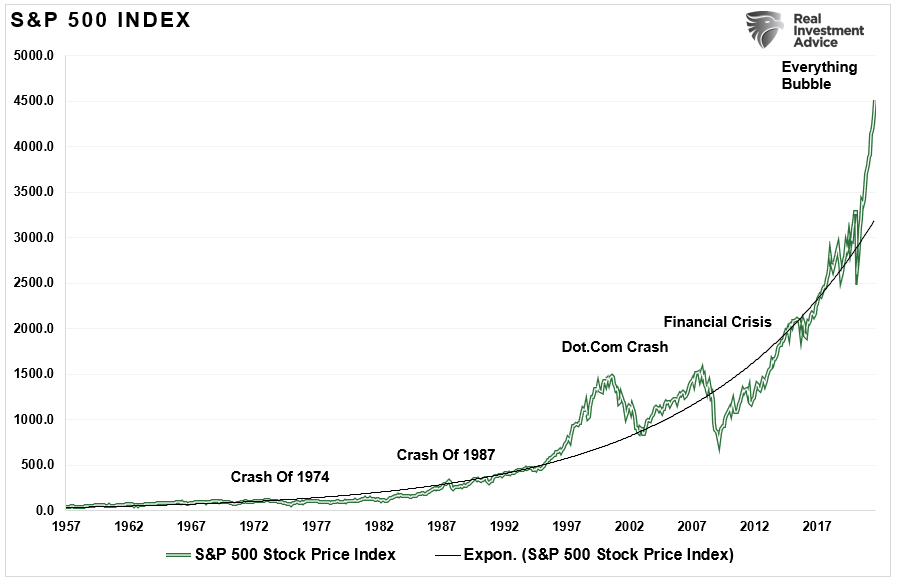

That certainly seems to be the case at the moment. After all, look at this monthly chart of the S&P 500 below.

While the liquidity-fueled rise in the market from the financial crisis low was substantial, it wasn’t as abnormal as it seemed as it tracked along with the exponential growth trend line. Such was also the case from 1957 to 1995.

However, the accelerated rise above the exponential trend line, as seen in 2000 and 2007, is currently of concern. It is also similar to the advance seen in the Nikkei index in 1980.

That bubble in Japan, combined with a rise in debt, an aging demographic, and a massively underfunded pension system, has yet to recover after nearly 30-years.

Is the U.S. destined for the same outcome? There are undoubtedly many similarities to consider.

Demographics & Unfunded Liabilities

“The entitlement state is endangered by improvident promises to an aging population. Like today’s transfer-payment state, is endangered by tardiness in recognizing that demography is destiny.” – George Will

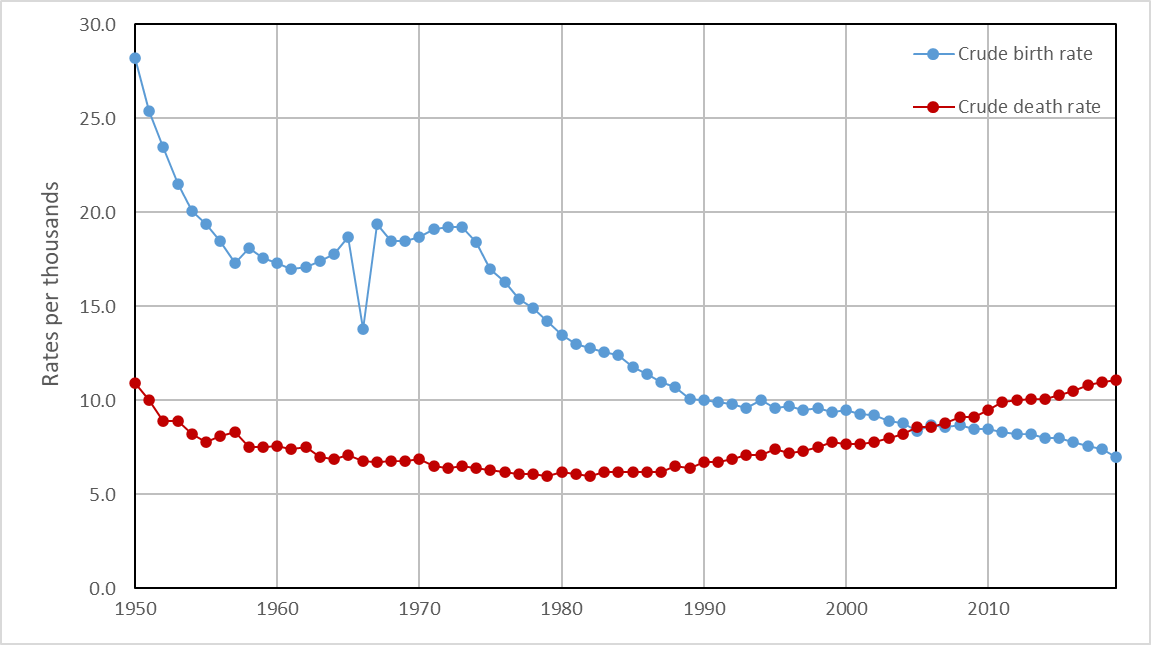

The issue of demography plagues Japan and the U.S. equally. The advancing decades show birth rates dropping as dependency on social welfare climbs. Such means fewer workers paying into a system depended on by an aging population living longer than expected.

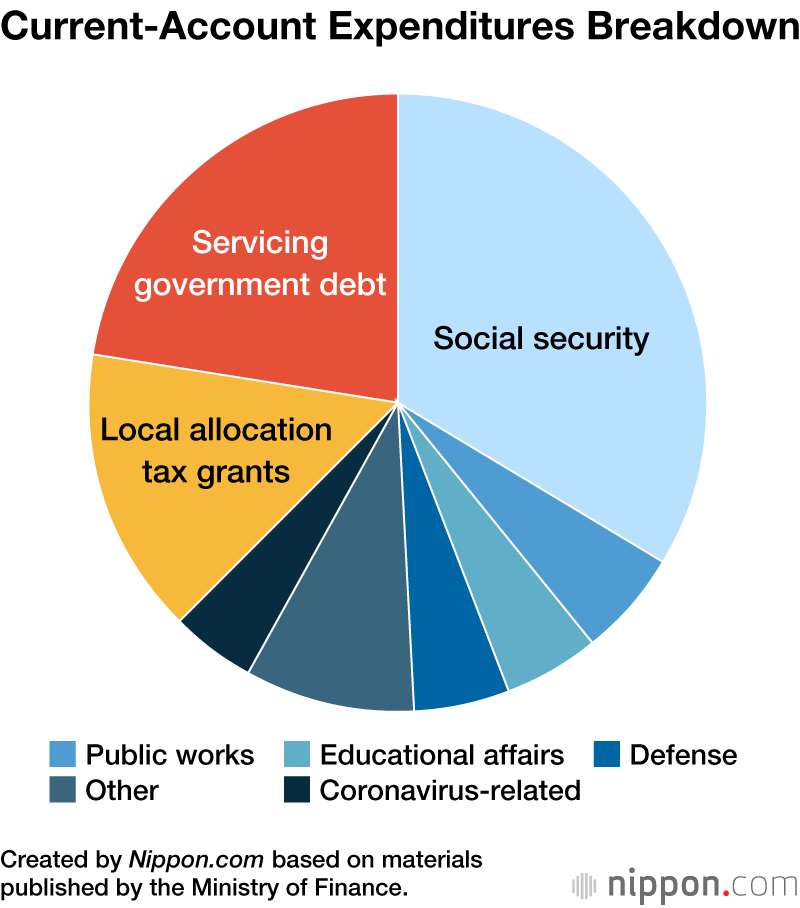

On December 21, 2020, Japan’s cabinet approved a general-account budget totaling ¥106.6 trillion, which was a record high. It was more than ¥4 trillion higher than the initial fiscal 2020 budget. It also marks the ninth consecutive year of record budgets. There is no surprise that more than 50% of the budget funds three items: social welfare, interest on the debt, and tax grants.

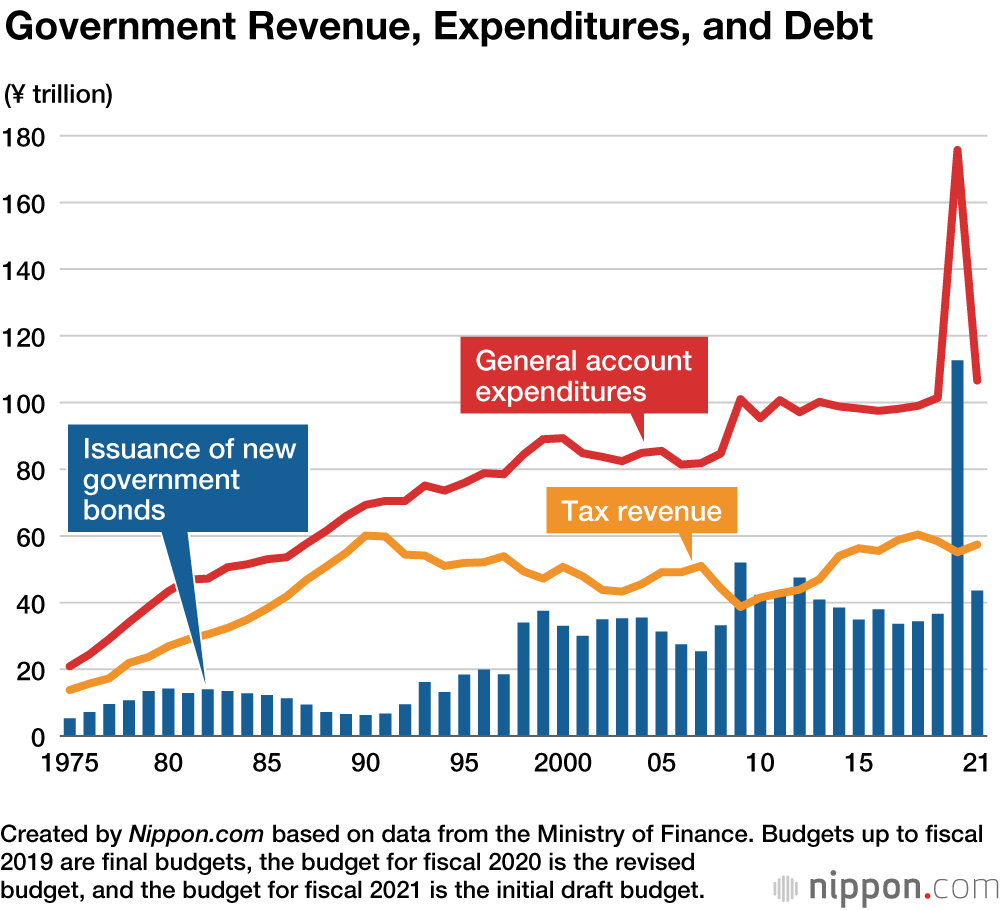

Here is the crucial point. While debt issuance has exploded to service the social welfare system, revenue fell.

“Government revenue, meanwhile, shrank by 9.5% compared to fiscal 2020, to ¥57.4 trillion. In order to make up for the revenue shortfall, the issuance of Japanese government bonds will swell by 33.9% year on year to ¥43.6 trillion. This means that 40.9% of next year’s budget will be funded by debt.” – Nippon.com

But that is just Japan. The U.S. is undoubtedly in a much better position. Right?

Well, let’s start with demographics.

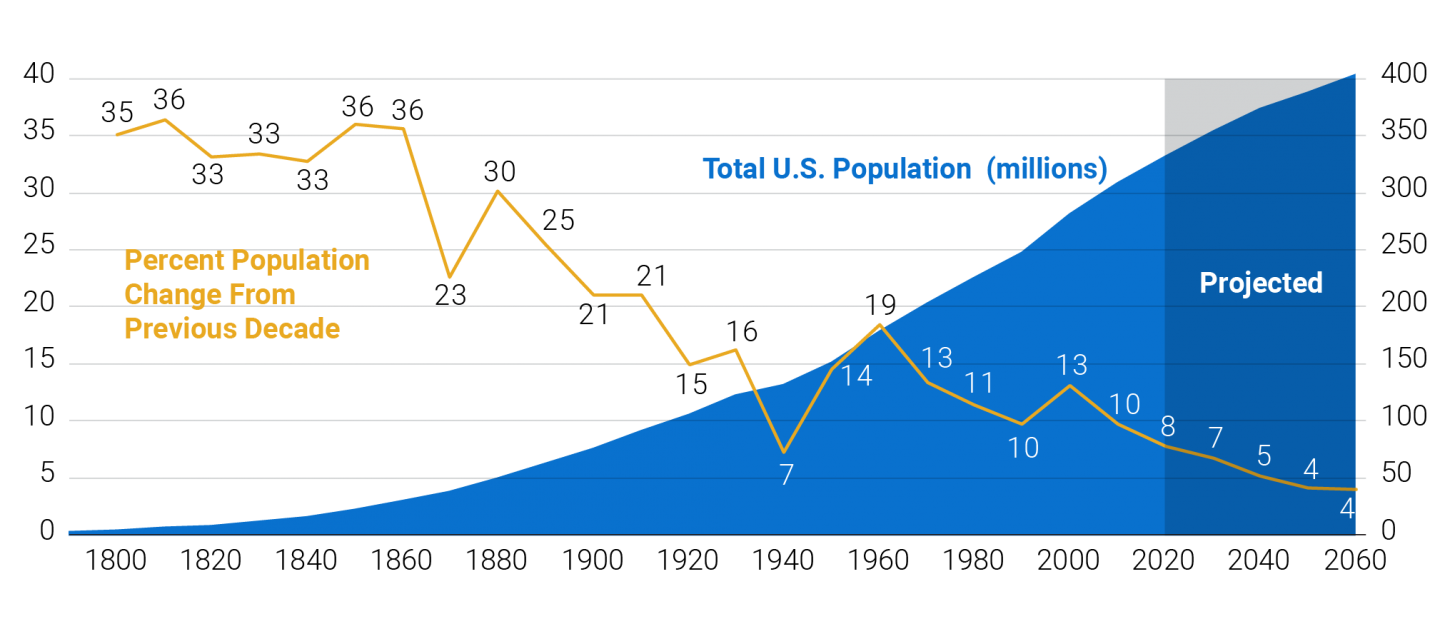

“The pace of U.S. population growth is slowing, according to the Census Bureau’s 2018 estimates and 2020 projections, which provide a preview of 2020 Census results. Unless the rate of population growth increases over the next two years, the United States may not reach the Census Bureau’s projected population size in 2020.” – PRB.Org

Spending Will Be Higher

The problem, as with Japan, is that demographics are undermining the support for the social welfare system. The aging population is currently dependent on a scheme funded by less than 2-workers per retiree.

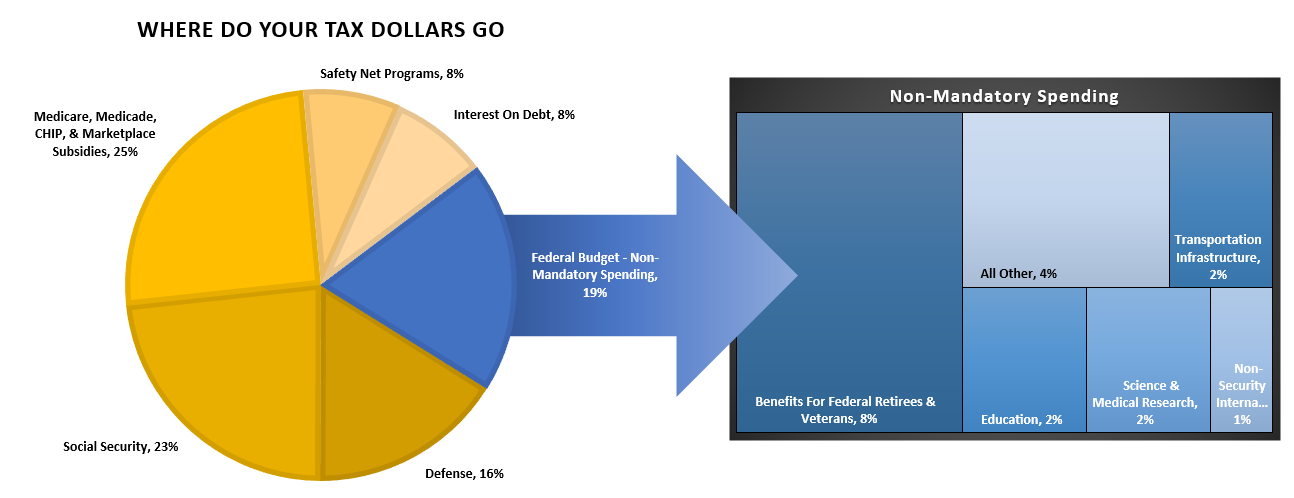

Entitlements and interest on the debt, like Japan, consume the majority of the budget. Also, like Japan, those entitlements require debt issuance to meet current obligations. According to the Center On Budget & Policy Priorities, in 2020, roughly 75% of every tax dollar went to non-productive spending.

“In the fiscal year 2019, the Federal Government spent $4.4 trillion, amounting to 21 percent of the nation’s gross domestic product (GDP). Of that $4.4 trillion, federal revenues financed only $3.5 trillion. The remaining $984 billion came from debt issuance. As the chart below shows, three major areas of spending make up most of the budget.”

Think about that for a minute. In 2019, 75% of all expenditures went to social welfare and interest on the debt. Those payments required $3.3 Trillion of the $3.5 Trillion (or 95%) of the total revenue collected.

Given the decline in economic activity during 2020, those numbers become markedly worse. As a result, for the first time in U.S. history, the Federal Government will have to issue debt to cover the mandatory spending.

Here is the real problem as we advance:

“Rising health and retirement costs and insufficient funding also puts trust funds in danger. On a combined basis, CBO estimates the Social Security trust funds will run out in calendar year 2031 and face a 75-year shortfall of 1.6 percent of GDP, or 4.7 percent of taxable payroll.” – CFRB

The aging of the population is a $160 trillion unfunded liability dependent on taxpayers.

Debt & Economic Growth

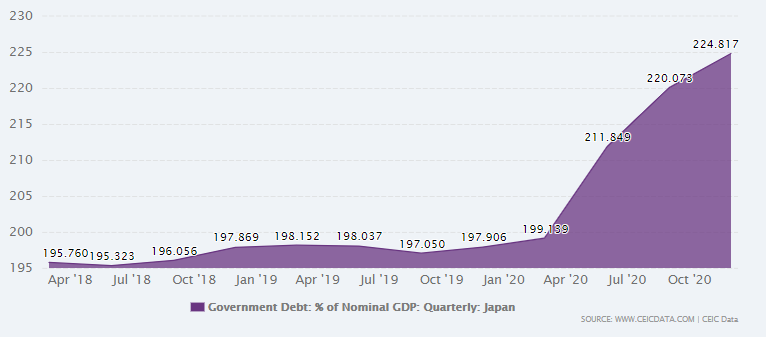

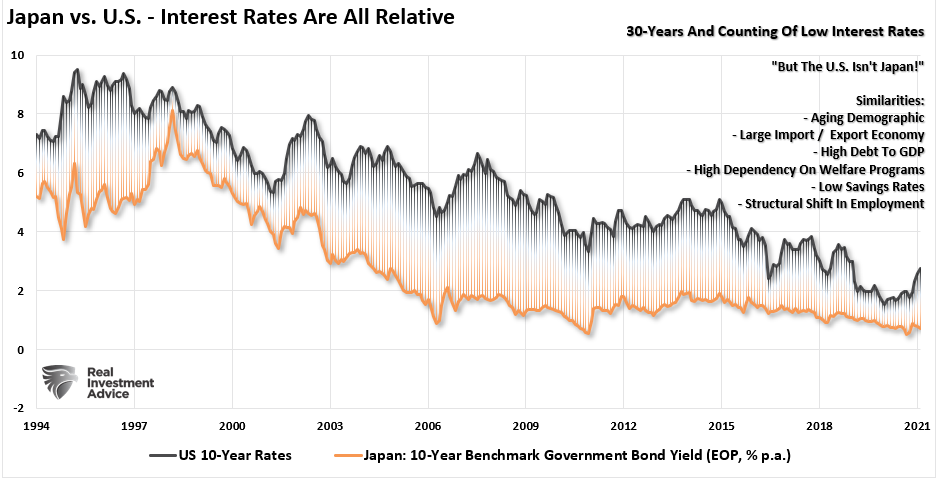

“Japan Government debt accounted for 224.9 % of the country’s Nominal GDP in Dec 2020, compared with the ratio of 220.1 % in the previous quarter. In the latest reports, Japan National Government Debt reached 11,523.0 USD bn in Feb 2021. The country’s Nominal GDP reached 1,318.8 USD bn in Dec 2020.” – CEIC Data

Currently, the U.S. is not at the same level of debt-to-GDP as Japan. However, that is changing as politicians continue to engage in rampant spending sprees in Washington.

“The scale and scope of government spending expansion in the last year are unprecedented. Because Uncle Sam doesn’t have the money, lots of it went on the government’s credit card. The deficit and debt skyrocketed. But this is only the beginning. The Biden administration recently proposed a $6 trillion budget for fiscal 2022, two-thirds of which would be borrowed.” – Reason

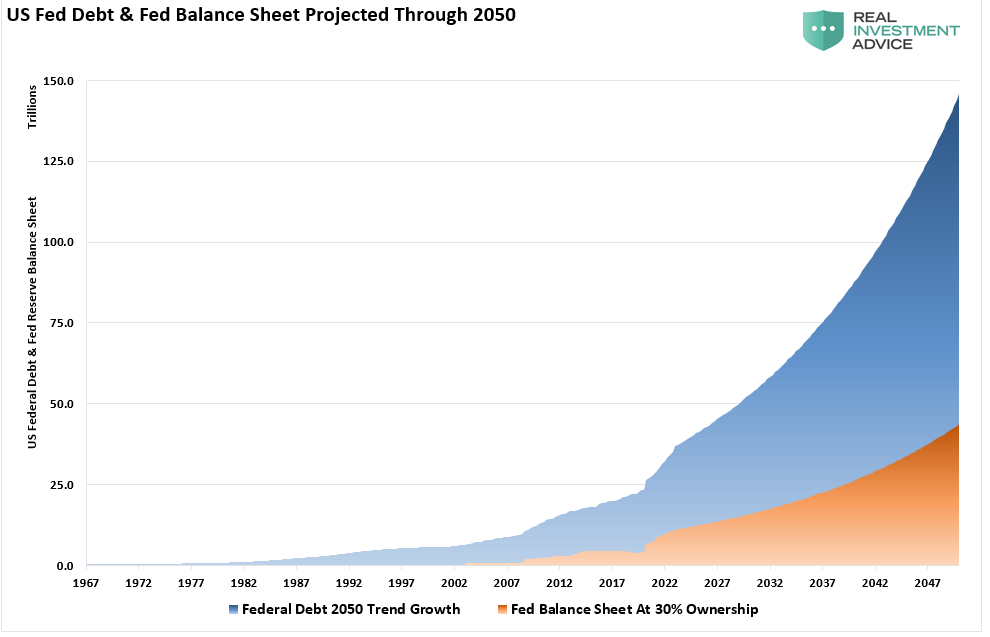

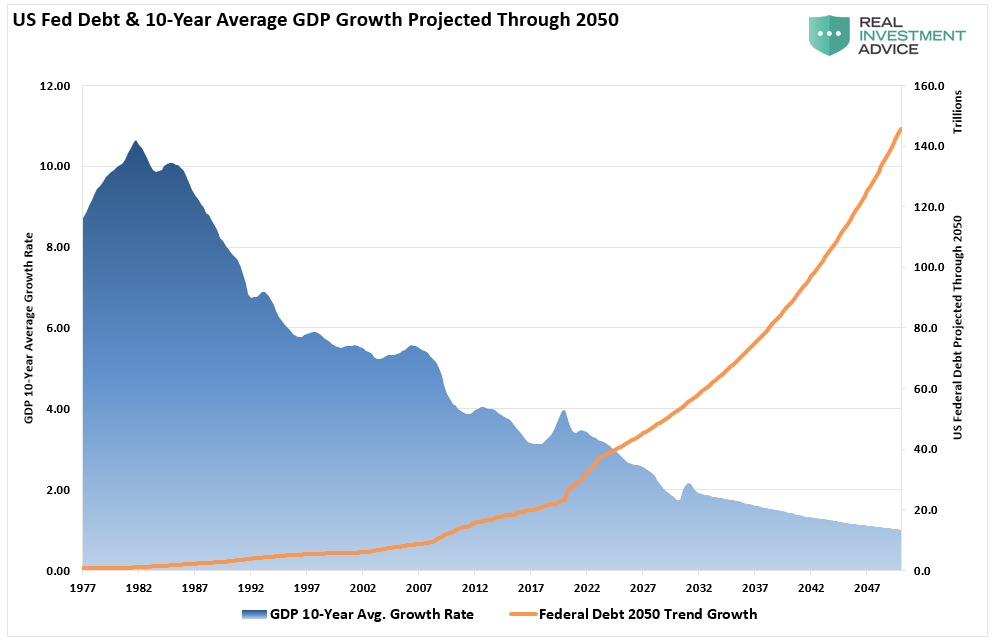

The CBO (Congressional Budget Office) recently produced its long-term debt projection through 2050, ensuring poor economic returns. Therefore, I reconstructed a chart from Deutsche Bank showing the US Federal Debt and Federal Reserve balance sheet. The chart uses the CBO projections through 2050.

At the current growth rate, the Federal debt load will climb from $28 trillion to roughly $140 trillion by 2050. Concurrently, assuming the Fed continues monetizing 30% of debt issuance, its balance sheet will swell to more than $40 trillion.

Let than sink in for a minute.

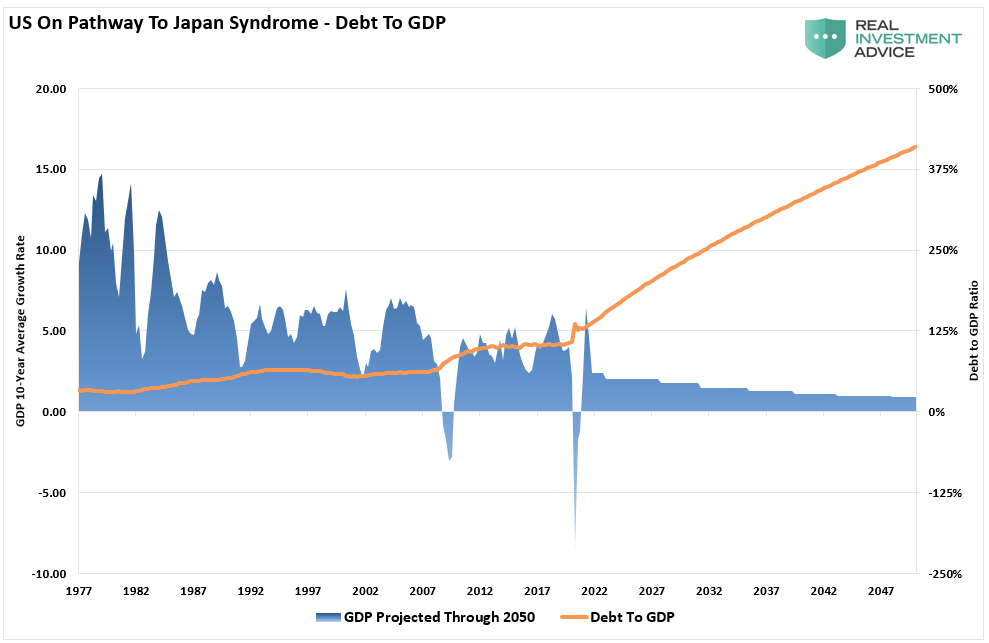

Debt To GDP Will Soar

What should not surprise you is that non-productive debt does not create economic growth.

A long-term historical look confirms the same. Since 1977, the 10-year average GDP growth rate steadily declined as debt increased. Thus, using the historical growth trend of GDP, the increase of debt will lead to slower economic growth rates in the future.

Given the historical correlation of debt to GDP growth, such suggest future outcomes will be no different.

The problem is the economic deficit has never been more significant. From 1952 to 1982, the economic surplus fostered ab economic growth rate averaging roughly 8% during that period. Today that is no longer the case as the debt detracts from growth. Such is why the Federal Reserve has found itself in a “liquidity trap.”

Interest rates MUST remain low, and debt MUST grow faster than the economy, just to keep the economy from stalling out.

While mainstream economists continue to suggest the U.S. can “grow” its way out of debt, history suggests that is not the case. Given that debt is increasing to maintain growth due to non-productive uses, such is another example of the pathway to economic Japanization.

However, as noted above, the Federal Reserve will be a critical participant in the debt issuance.

Rates & Quantitative Easing

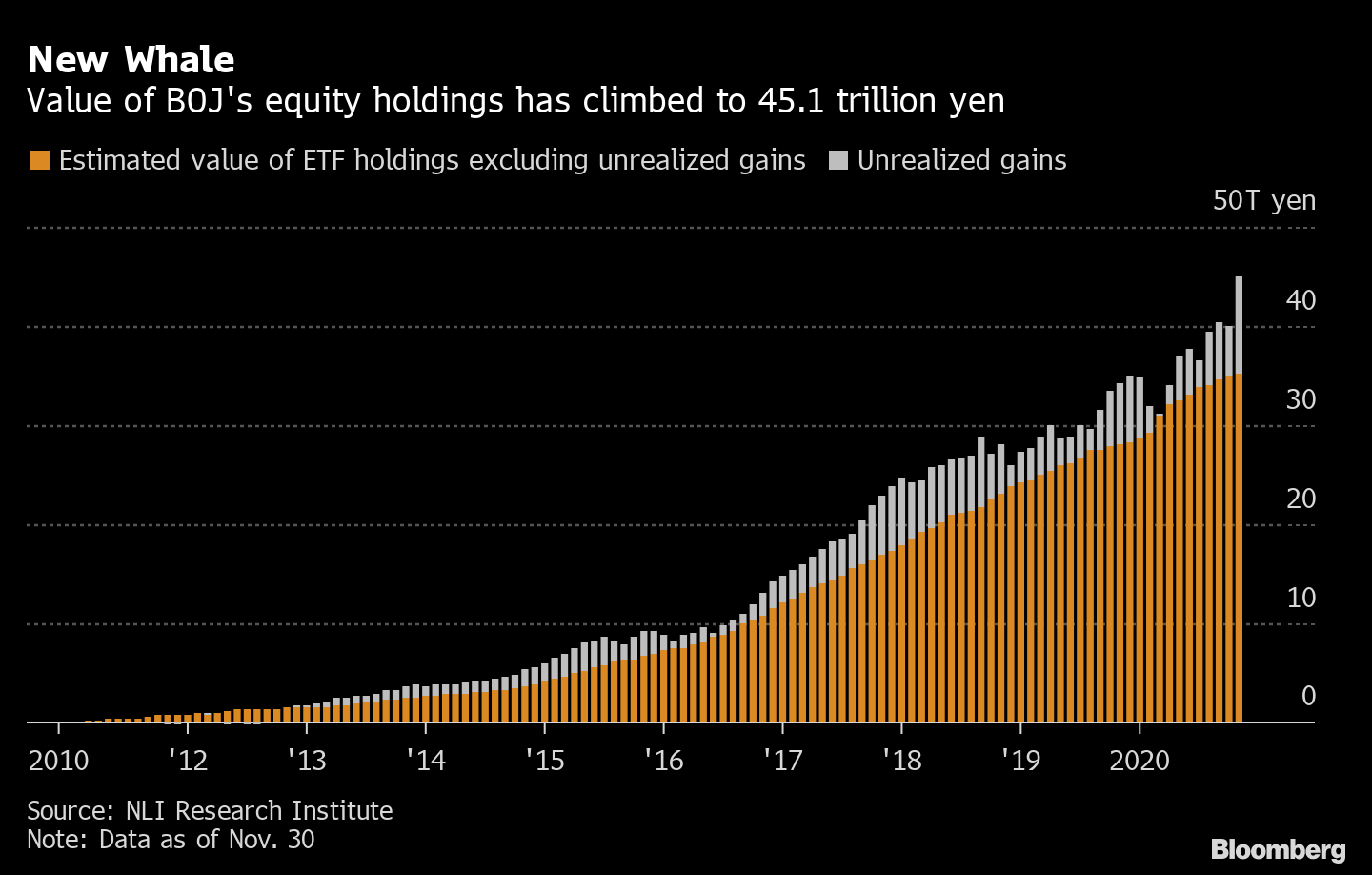

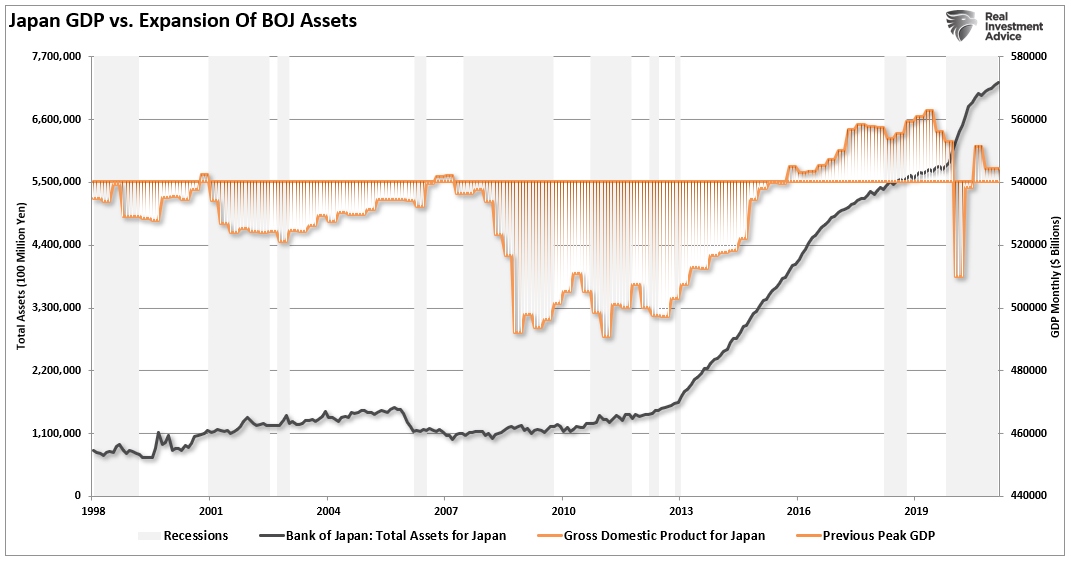

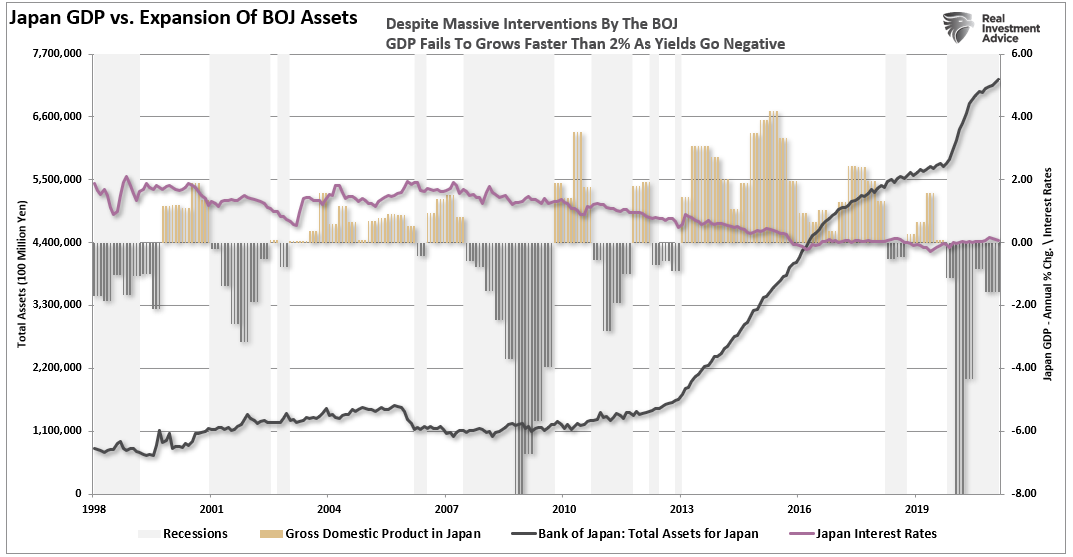

Since the financial crisis, Japan has been running a massive “quantitative easing” program, which, on a relative basis, is more than 3-times the size of that in the U.S.

Despite that massive surge in Central Bank interventions, it, like the U.S., has had little effect on economic prosperity. While stock markets have performed well, economic growth is roughly equal to this century’s beginning.

Furthermore, despite the BOJ’s balance sheet consuming 80% of the ETF markets, not to mention a sizable chunk of the corporate and government debt market, Japan remains plagued by rolling recessions and low inflation, and low interest rates. (Japan’s 10-year Treasury rate fell into negative territory for the second time in recent years.)

Not So Different

Why is this important? Because Japan is a microcosm of what is happening in the U.S. As I noted previously:

“The U.S., like Japan, is caught in an ongoing ‘liquidity trap’ where maintaining ultra-low interest rates are the key to sustaining an economic pulse. The unintended consequence of such actions, as we are witnessing in the U.S. currently, is the battle with deflationary pressures. The lower interest rates go – the less economic return that can be generated. An ultra-low interest rate environment, contrary to mainstream thought, has a negative impact on making productive investments, and risk begins to outweigh the potential return.”

As my colleague Doug Kass noted, Japan is a template of the fragility of global economic growth.

“The bigger picture takeaway the fact that financial engineering does not help an economy, it probably hurts it. If it helped, after mega-doses of the stuff in every imaginable form, the Japanese economy would be humming. But the Japanese economy is doing the opposite. Japan tried to substitute monetary policy for sound fiscal and economic policy. And the result is terrible.”

I agree with Doug, as does the data, that while financial engineering props up asset prices, it does nothing for an economy over the medium to longer term. On the contrary, it has negative consequences.

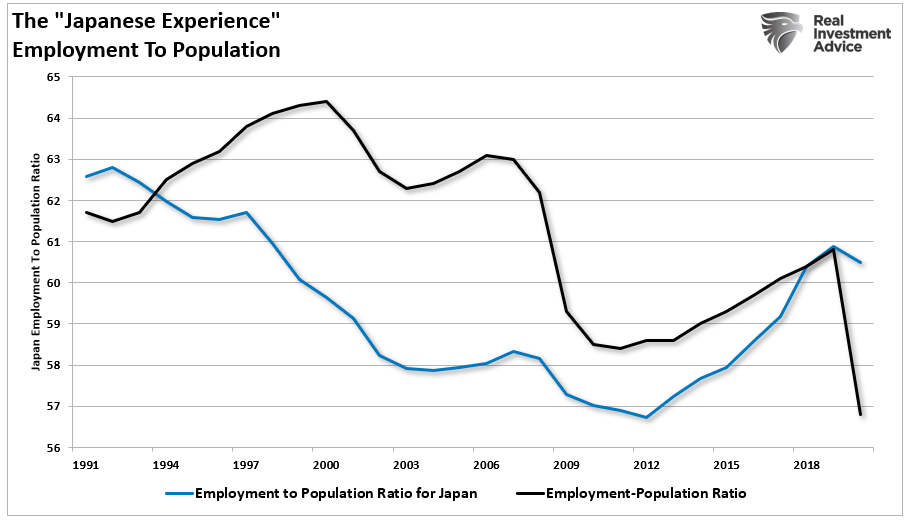

The employment-to-population ratios of both countries show the problem.

Summary

Central Banks continue to inject massive amounts of liquidity to keep economies afloat globally over the last decade. But, unfortunately, there is rising evidence that growth continues to decelerate.

Furthermore, we have much more akin to Japan than many would like to believe.

- A decline in organic savings that depletes productive investments

- An aging demographic that is top-heavy and drawing on social benefits at an advancing rate.

- A heavily indebted economy with debt/GDP ratios above 100%.

- The decline in exports due to a weak global economic environment.

- Slowing domestic economic growth rates.

- An underemployed younger demographic.

- An inelastic supply-demand curve

- Weak industrial production

- Dependence on productivity increases to offset reduced employment

The lynchpin to Japan, and the U.S., remains demographics and interest rates. As the aging population grows, becoming a net drag on “savings,” the dependency on the “social welfare net” will continue to expand.

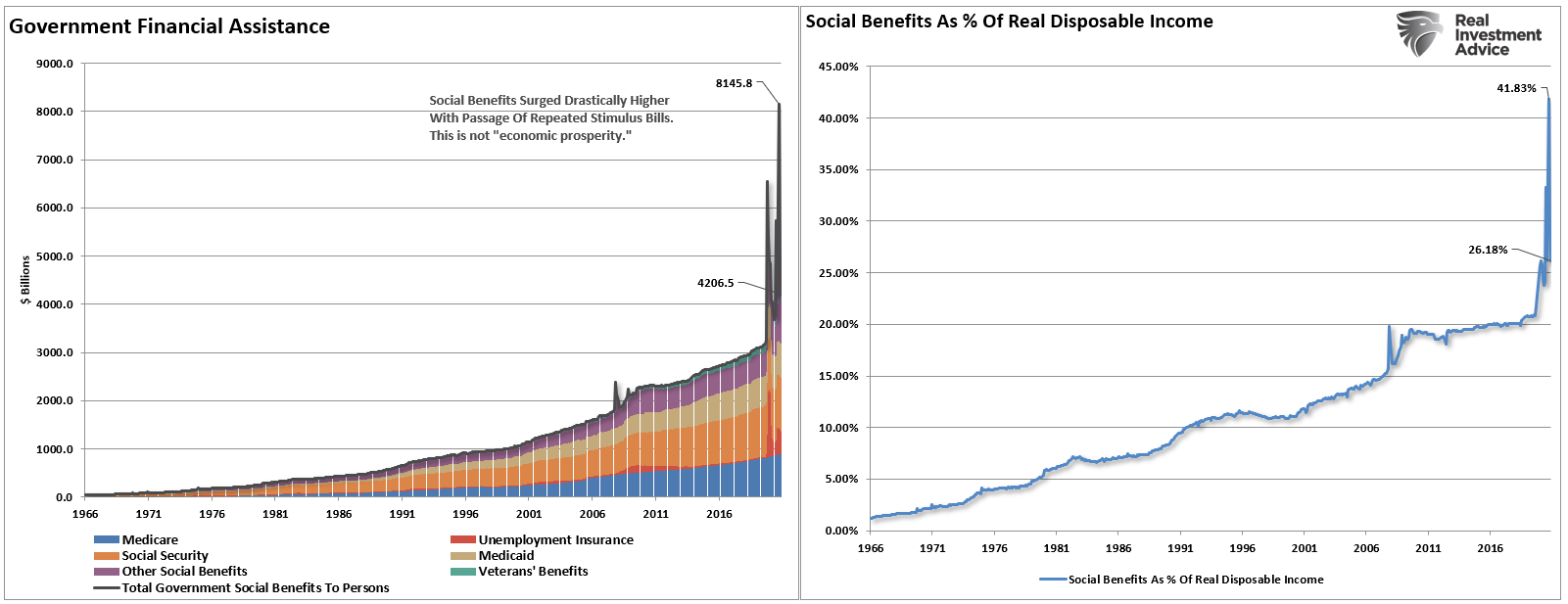

(The spike in social benefits as a percent of DPI was from the various stimulus programs. With those now ending, that support falls back to its previous levels of roughly 25% of incomes. Around 1-in-3 households receive some form of Government assistance.)

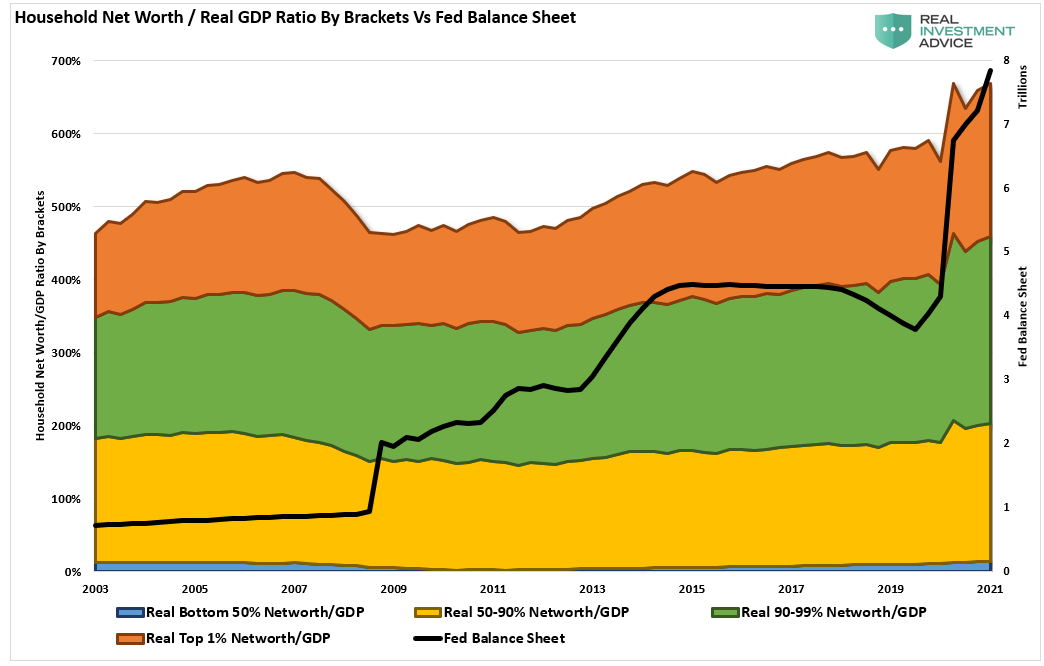

While the Fed can undoubtedly continue injecting liquidity into the financial markets, further inflating the wealth gap, the economic prosperity for the rest of the population will continue to erode.

There is a limit to the ability to continue pulling forward future consumption to stimulate economic activity.

Japan is already there. It is only a function of time until the U.S. reaches the same point as the eventual void becomes too great to fill.

However, in the meantime, Central Banks will continue to repeat the same policies while hoping for a different result.

But isn’t that the very definition of “insanity?”

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read