Many advisors promote passive investment strategies by pointing to studies showing investors fail at “market timing.” Such was a point made recently by Ralph Wakerly. To wit:

“So-called ‘experts are telling us about the coming uber-bear or why the bull market will continue. Yet the data show that trying to predict the market’s direction to time buys and sells is the wrong approach to investing.

Data from the last seven bear markets show that a large percentage of losses and gains happen in very short periods of time, requiring timers to have uncanny accuracy and resolve. Investors are better served to ignore market calls and follow the time-tested practice of holding well-diversified portfolios that meet their goals across long market cycles.”

While Ralph is correct in his statement, his solution is simplistic.

“Investors should set their investment goals, determine an appropriate investment plan and asset allocation, and stick with it for the long term.”

In other words, just “buy and hold” a portfolio of passive index funds and you will be fine.

On the surface, the argument seems sound. If you want to have average market performance, buying a basket of index funds will give you average performance. There is nothing wrong with that, however, you hardly need to pay an advisor a fee to do that job.

However, there are two major problems with the analysis that need clarification.

- There is a major difference between “market timing” and “risk management;” and,

- Suffering large drawdowns of capital during bear market periods destroys financial goals.

In this post, we will explore these two points.

Market Timing Vs. Risk Management

The act of “market timing” is often misconstrued by advisors promoting “passive strategies.” Market timing is the act of being “all-in” or “all-out” of the market at any given time. The problem with market timing, and born out by repeated studies, is that individuals cannot successfully replicate the profitable timing of the buys and sells.

Market timing is usually framed in some manner like below:

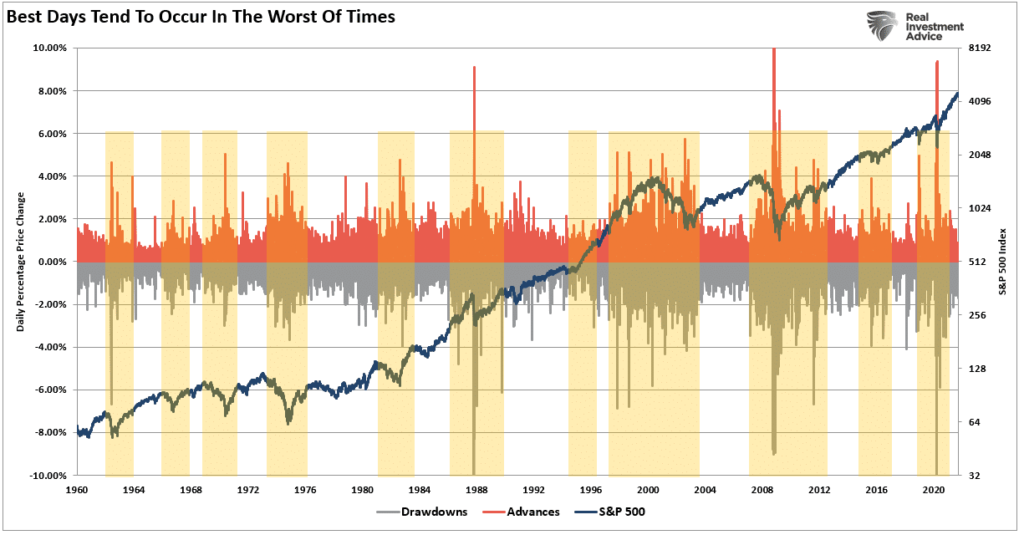

“Looking at data going back to 1930, Bank of America found that if an investor missed the S&P 500′s 10 best days in each decade, total returns would be just 91%, significantly below the 14,962% return for investors who held steady through the downturns.” – Pippa Stevens via CNBC

But here was her key point, which ultimately invalidates her entire premise:

“The firm noted this eye-popping stat while urging investors to ‘avoid panic selling,’ pointing out that the ‘best days generally follow the worst days for stocks.’”

Think about that for a moment.

“The best days generally follow the worst days.“

The statement is correct, as the S&P 500’s largest percentage gain days, tend to occur in clusters during the worst days for investors.

The analysis of “missing out on the 10-best days” of the market is steeped in the myth of the benefits of “buy and hold” investing. (Read more: The Definitive Guide For Investing.)

While “buy and hold,” as a strategy works great in a long-term rising bull market. It fails during a bear market for two simple reasons: Psychology and Destruction Of Capital

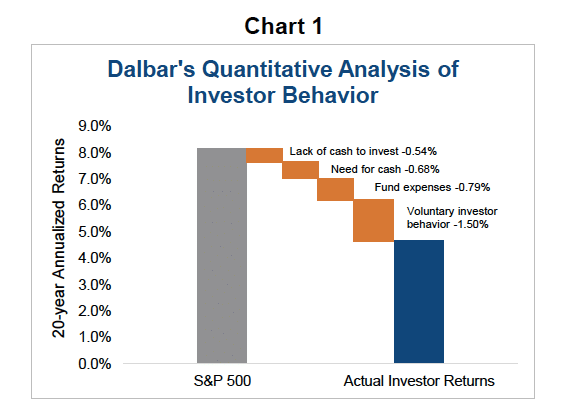

As Dalbar regularly points out, individuals always underperform the benchmark index over time by allowing “behaviors” to interfere with their investment discipline. That psychology also impacts “buy and hold” strategies which often fail at the “first contact with the enemy.”

As is always the case, investors regularly suffer from the “buy high/sell low” syndrome.

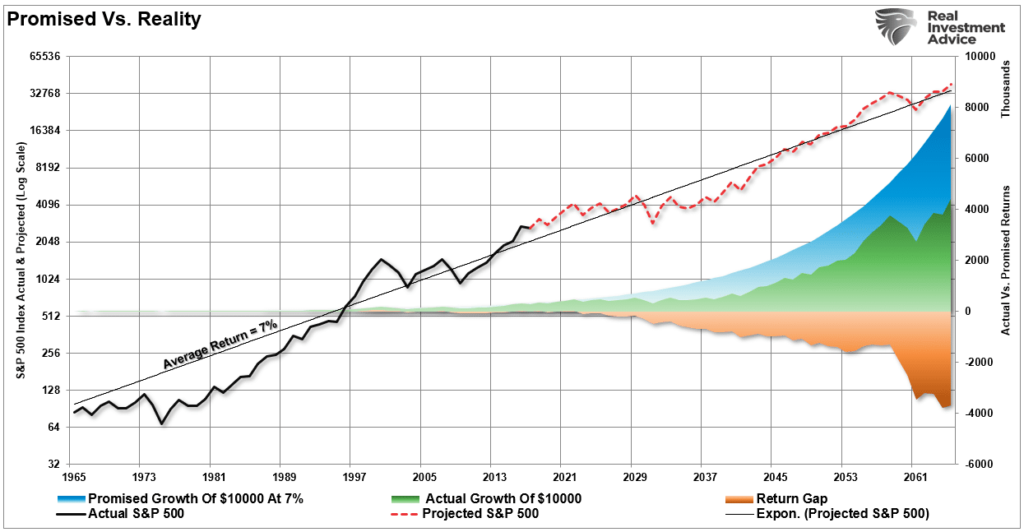

Even if an individual is successful in riding market volatility, the destruction of capital can have devastating consequences on financial goals. As shown below, an investor who expected a 7% “compounded rate of return” over a lifetime, as promised by “buy and hold” strategies, fell very short of financial goals. Such is because losing a significant chunk of capital, and then getting back to even, destroys the compounded return premise.

Such is why “risk management” is key for investors, especially those who employ “buy and hold” strategies.

The Market Timing Myth

Every great investor throughout history from Warren Buffett to Paul Tudor Jones all have one rule in common. That rule, while stated in many different ways, is simply:

“Buy low. Sell high.”

Think about that for a moment. While somewhat obvious, the key to making money in the investing process is to “buy value when it is cheap and sell it when it is dear.”

Yet, such a statement clearly flies in the face of “buy and hold” strategies.

In 2010, Brett Arends wrote an excellent commentary entitled: “The Market Timing Myth” which primarily focused on several points we have made over the years. Brett really hits home with the following statement:

“For years, the investment industry has tried to scare clients into staying fully invested in the stock market at all times, no matter how high stocks go or what’s going on in the economy. ‘You can’t time the market,’ they warn. ‘Studies show that market timing doesn’t work.’

He goes on:

“They’ll cite studies showing that over the long-term investors made most of their money from just a handful of big one-day gains. In other words, if you miss those days, you’ll earn bupkis. And as no one can predict when those few, big jumps are going to occur, it’s best to stay fully invested at all times. So just give them your money… lie back, and think of the efficient market hypothesis. You’ll hear this in broker’s offices everywhere. And it sounds very compelling.

There’s just one problem. It’s hooey.

They’re leaving out more than half the story.

And what they’re not telling you makes a real difference to whether you should invest, when and how.”

As noted above, avoiding major drawdowns in the market is key to long-term investment success. If I am not spending the bulk of my time making up previous losses in my portfolio, I spend more time compounding my invested dollars towards my long-term goals.

As Brett concluded:

“The cost of being in the market just before a crash, are at least as great as being out of the market just before a big jump, and may be greater. Funny how the finance industry doesn’t bother to tell you that.”

The reason that the finance industry doesn’t tell you the other half of the story is because it is NOT PROFITABLE for them. The finance industry makes money when you are invested – not when you are in cash. Since a vast majority of financial advisors can’t actually successfully manage money, they just tell you to “stay the course.”

However, you DO have options.

A Simple Method

Let me repeat, I do not endorse “market timing.” Market timing is specifically being “all-in” or “all-out” of the market at any given time. The problem with market timing is consistency.

You cannot, over the long term, effectively time the market. Being all in, or out, of the market will eventually put you on the wrong side of the “trade,” which leads to a host of other problems.

However, there are also no great investors in history who employed “buy and hold” as an investment strategy. Even the great Warren Buffett occasionally sells investments. True investors buy when they see the value and sell when value no longer exists.

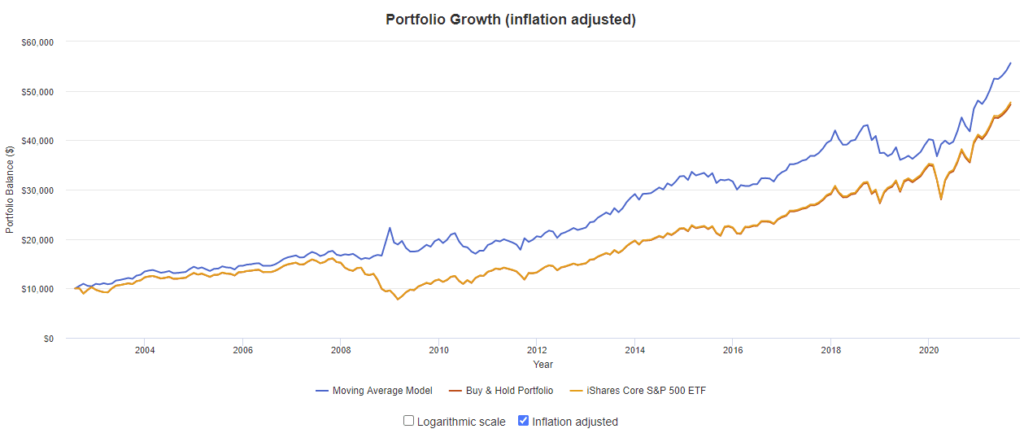

While there are many sophisticated methods of handling risk within a portfolio, even using a basic method of price analysis, such as a moving average crossover, can be a valuable tool over the long-term holding periods. Will such a method ALWAYS be right? Absolutely not. However, will such a method keep you from losing large amounts of capital? Absolutely.

The chart below shows a simple 12-month moving average crossover study. (via Portfolio Visualizer)

What should be obvious is that using a basic form of price movement analysis can provide a useful identification of periods when portfolio risk should be REDUCED. Importantly, I did not say risk should be eliminated; just reduced.

Here are the comparative results.

Again, I am not implying, suggesting, or stating that such signals mean going 100% to cash. What I am suggesting is that when “sell signals” are given, that is the time when individuals should perform some basic portfolio risk management such as:

- Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

Small Adjustments Can Have A BIg Impact

By using some measures, fundamental or technical, to reduce portfolio risk as prices/valuations rise, or vice versa, the long-term results of avoiding periods of severe capital loss will outweigh missed short-term gains.

“Anyone who followed the numbers would have avoided the disaster of the 1929 crash, the 1970s or the past lost decade on Wall Street. Why didn’t more people do so? Doubtless, they all had their reasons. But I wonder how many stayed fully invested because their brokers told them ‘You can’t time the market.”‘ – Brett Arends

There is little point in trying to catch each twist and turn of the market. But that also doesn’t mean you simply have to be passive and let it wash all over you. It may not be possible to “time” the market, but it is possible to reach intelligent conclusions about whether the market offers good value for investors.

There is a clear advantage of providing risk management to portfolios over time. The problem, as I have discussed many times previously, is that most individuals cannot manage their own money because of “short-termism.”

Despite their inherent belief that they are long-term investors, they are consistently swept up in the short-term movements of the market. Of course, with the media and Wall Street pushing the “you are missing it” mantra as the market rises – who can really blame the average investor for “panic” buying market tops, and selling out at market bottoms.

Yet, despite two major bear market declines, it never ceases to amaze me that investors still believe they can invest their savings into a risk-based market, without suffering the eventual consequences of risk itself.

Despite being a totally unrealistic objective, this “fantasy” leads to excessive speculation in portfolios, which ultimately results in catastrophic losses. Aligning expectations with reality is the key to building a successful portfolio. Implementing a strong investment discipline, and applying risk management, is what leads to the achievement of those expectations.

As Brett concluded:

“It does mean you that you shouldn’t let scare stories dominate your approach to investing. Don’t let yourself be bullied. Least of all by someone who isn’t telling you the full story.”

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read