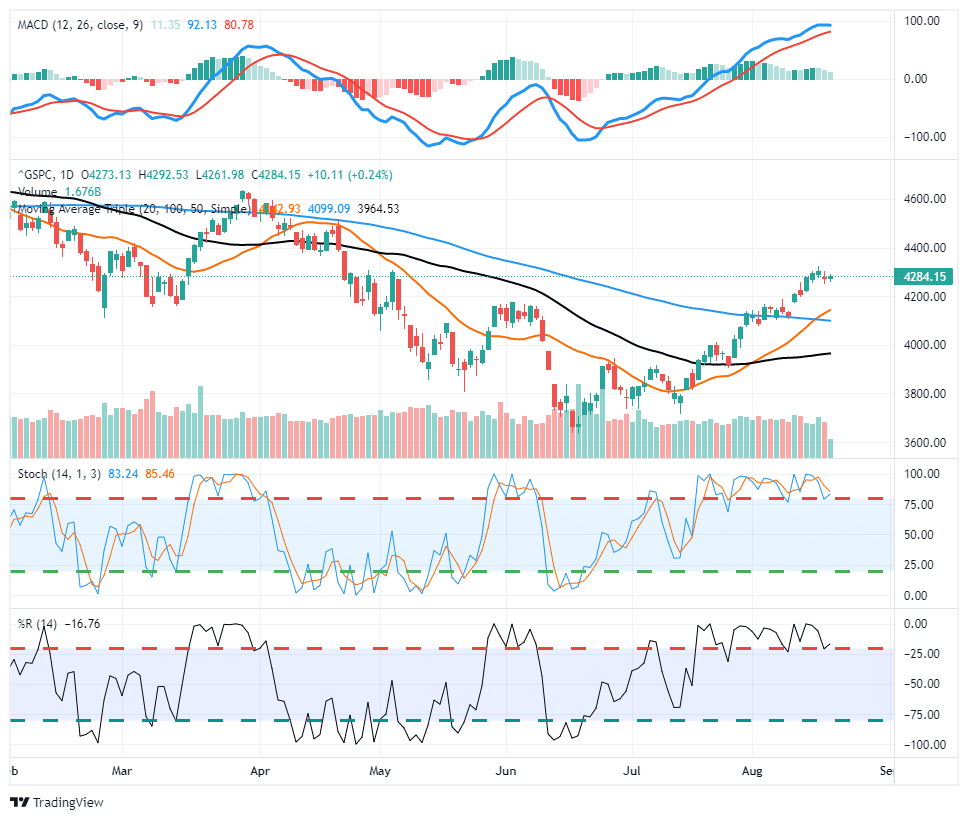

Short covering has stopped. Over the last couple of days, markets have meandered as investors digested the most recent FOMC meeting minutes and what that might mean for monetary policy over the next several months. As we discuss in today’s market trading update, the markets are extremely overbought, limiting the potential further upside for the time being.

Importantly, the massive amount of short-covering that drove the markets 17% higher over the last 9-weeks has halted. As shown below, the lack of short covering, combined with overbought conditions, and a $2-trillion options expiration today, could well see a pick up in volatility that we have not seen as of late.

What To Watch Today

Economy

- No notable reports are set for release.

Earnings

Market Trading Update

The market traded choppy yesterday as traders digested the most recent FOMC minutes and the resistance at the 200-dma. With markets very overbought in the short-term with short covering waning, further upside will become challenging until either the market consolidates or pulls back enough to work off some excess.

In the meantime, continue to trade cautiously; we are seeing a pickup in rotation between sectors, which is usually indicative of a late-stage advance. Again, the overall trends are bullish, suggesting that pullbacks should hold onto key supports currently at the 100-dma and 50-dma below that. Those levels can be used to increase equity exposure accordingly. However, I would be wary of taking extremely aggressive bets with the Fed still hiking rates and tightening their balance sheet. As noted above, if short covering is done, the odds of a leg lower have risen markedly.

Unemployment Set To Increase

While the FOMC minutes noted strong employment data, a new survey from consultancy PwC released this month showed 50% of companies are planning to reduce overall headcount. Additionally, 46% of companies said they are dropping or reducing signing bonuses, while 44% are rescinding offers.

Reducing overall headcount doesn’t mean all of the respondents to PwC’s survey are planning layoffs, but it at least indicates plans similar to what we’ve seen in the tech industry, where backfills are paused or previously allocated heads are cut from a department’s budget.

“Respondents are also taking proactive steps to streamline the workforce and establish the appropriate mix of worker skills for the future. This comes as no surprise. After a frenzy of hiring and a tight labor market over the past few years, executives see the distinction between having people and having people with the right skills.”

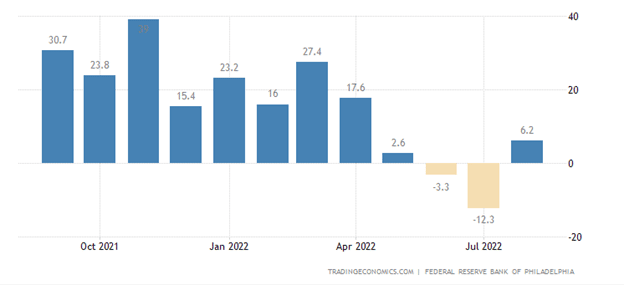

Philly Fed Manufacturing Index

The Philadelphia Fed’s Manufacturing Index beat expectations yesterday in contrast to the Empire State Index’s huge negative surprise on Monday. The Philly Fed’s index came in at 6.2 for August versus the consensus forecast of -5. The new orders component was -5.1, and although still negative, it improved markedly from July’s -24.8.

The report offered encouraging data on the inflation front. It pointed to further price declines in August, as did the Empire State index. The prices paid component saw relief for the fourth straight month as it fell to 43.6 from 52.2 in July.

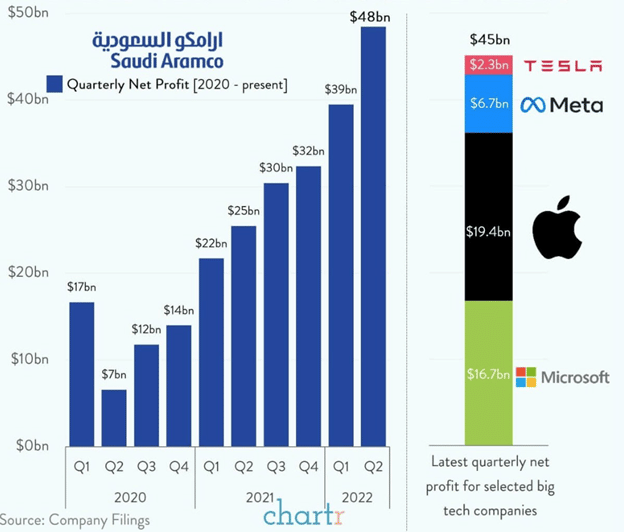

Saudi Aramco is Raking It In

Saudi Arabia’s massive state-owned oil company, Saudi Aramco, is raking in profits lately. It reported earnings of $48.4B (+89.8% YoY) on the back of high crude prices, refining margins, and sales volumes. As shown below, Aramco reported higher earnings than Apple, Microsoft, Meta, and Tesla combined. In addition, Aramco’s second-quarter profit was almost equal to the five largest western energy majors’ earnings combined.

Jobless Claims Signal Strength

Weekly jobless claims were slightly below expectations yesterday at 250k versus a consensus of 265k and a prior 252k. Claims have held relatively steady over the past month at levels that are not particularly concerning. This week’s data is another testament to continued strength in the labor market. Once again, it provides a green light for a data-dependent Fed to continue tightening monetary policy.

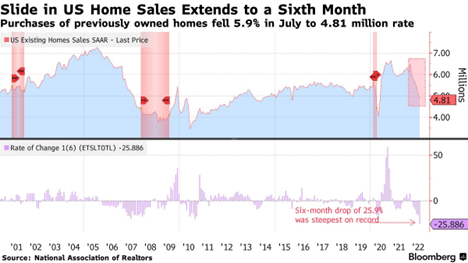

Existing Home Sales

Existing home sales fell in July, for the sixth straight month, to an annualized rate of 4.81 million. According to Bloomberg,

“The nearly 26% decline in previously owned home sales since January marks the steepest six-month plunge in records back to 1999 and underscores a housing market that’s reeling from elevated mortgage rates and prices.”

This is not surprising. As noted in Wednesday’s commentary, NAR’s housing affordability index fell below 100 in June. The index is the lowest it’s been since 1989. Despite sharply declining sales volumes, median sales prices are not yet showing signs of retreat. While weakening demand has contributed to rising inventory metrics thus far, the market for existing homes remains tight at 3.3 months’ supply. Demand will likely fall further for the month’s supply of existing homes to reach pre-pandemic norms.

Not So Fast

Following July’s CPI report and the Fed minutes, there is increasing chatter of subsiding inflationary pressures with implications that the Fed might revert to an easy policy stance faster than expected. Investors seem to be embracing this narrative. The S&P 500 is up over 4% since the CPI report despite overbought conditions heading into it. While July’s CPI report showed zero increase in prices MoM, a large driving force was falling energy commodity prices. With this in mind, here are some quotes taken from the Fed minutes released on Wednesday:

“Participants remarked that, although recent declines in gasoline prices would likely help produce lower headline inflation rates in the short term, declines in the prices of oil and some other commodities could not be relied on as providing a basis for sustained lower inflation, as these prices could quickly rebound.”

“Participants agreed that there was little evidence to date that inflation pressures were subsiding.”

“Participants also observed that in some product categories, the rate of price increase could well pick up further in the short run, with sizable additional increases in residential rental expenses being especially likely.”

Perhaps the most dovish aspect of the report was that the Fed acknowledged for the first time the possibility that it could over-tighten financial conditions. This received a lot of attention. However, many are ignoring the two sentences prior. Here is the expanded quote:

“Participants judged that a significant risk facing the Committee was that elevated inflation could become entrenched if the public began to question the Committee’s resolve to adjust the stance of policy sufficiently. If this risk materialized, it would complicate the task of returning inflation to 2 percent and could raise substantially the economic costs of doing so. Many participants remarked that, in view of the constantly changing nature of the economic environment and the existence of long and variable lags in monetary policy’s effect on the economy, there was also a risk that the Committee could tighten the stance of policy by more than necessary to restore price stability.”

Notice the difference in language there. “Significant risk” vs. “also a risk.” Investors have been conditioned to the likes of an easy policy and uber-accommodative Fed over the past decade-plus. But are they too quick to assume things will be the same this time? Yesterday, the Kansas City Fed’s George said it’s not clear where the stopping point for rate hikes will be, but the Fed will need to be “completely convinced” inflation is coming down. Considering the current strength of the labor market, the level of inflation, and the quotes above, might bulls be jumping the gun?

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read