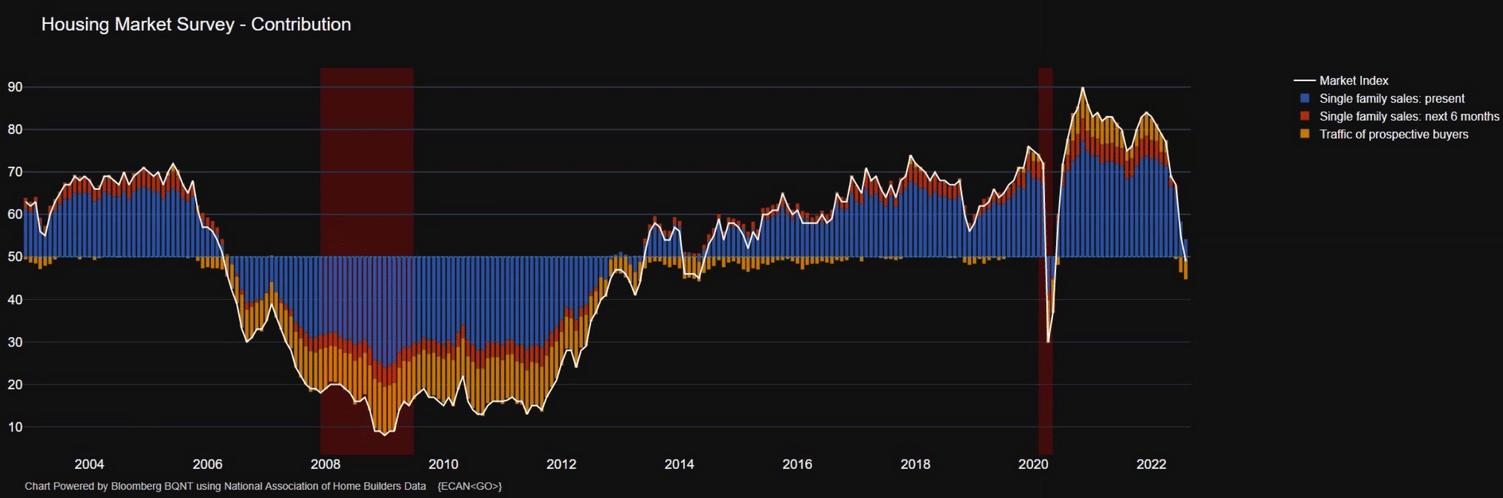

Recent housing data further confirms that the “Great Reopening” housing boom is morphing into a housing recession. Monday’s National Association of Home Builders (NAHB) survey fell below 50, signaling an economic contraction. This year’s 35-point decline is the largest on record. Yesterday’s data further confirms a housing recession is likely. New housing starts fell 9.6% year-over-year versus expectations for -2.1%. That was the sharpest drop in housing starts since the recession of early 2020. Housing permits, an indicator of expected new home construction, fell slightly from last month, but it was above expectations and well above levels of the 2020 housing recession. Permits are being bolstered by multi-family construction. There is a 9.3-month supply of new homes, almost double the average. The good news is that housing constitutes roughly a third of CPI. While bad for homebuilders, a housing recession may be what the doctor ordered to help reduce CPI.

What To Watch Today

Economy

- MBA Mortgage Applications, the week ended August 12 (0.2% prior)

- Retail Sales Advance, month-over-month, July (0.1% expected, 1.0% prior)

- Retail Sales excluding autos, month-over-month, July (-0.1% expected, 1.0% prior)

- Business Inventories, June (1.4% expected, 1.4% prior)

- FOMC Meeting Minutes

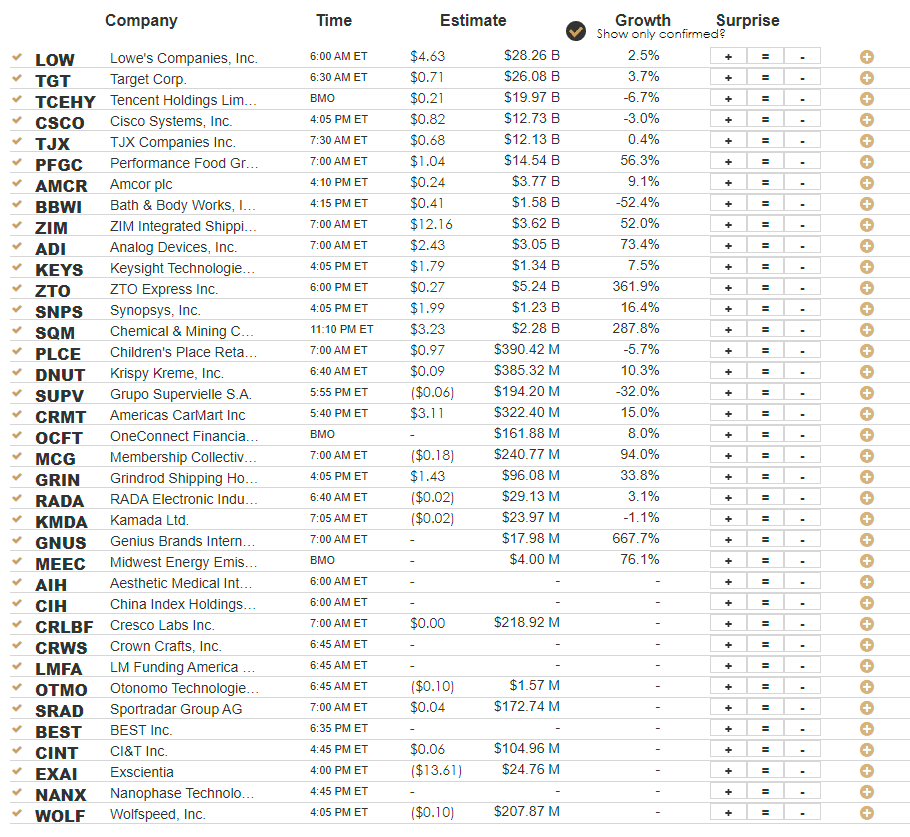

Earnings

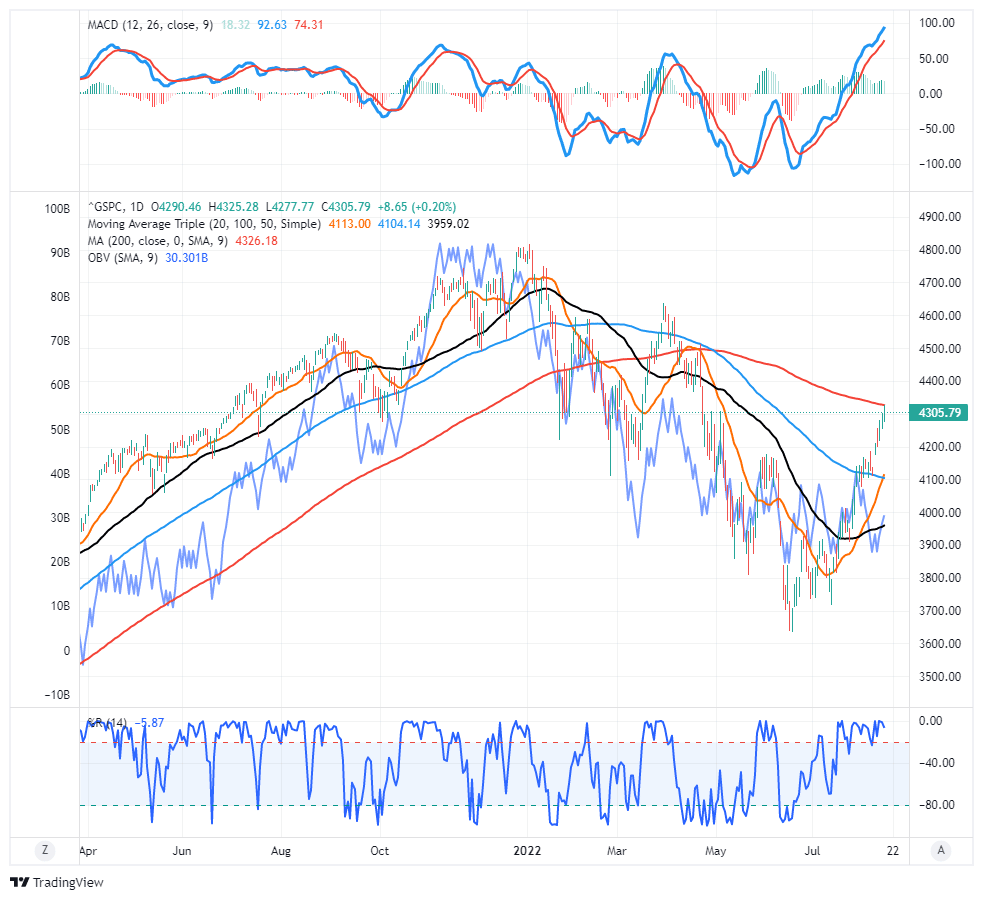

Market Trading Update – On Balance Volume Sends A Signal

The market rallied into the 200-dma yesterday and was rejected at that resistance level. Given such is the first attempt since March, it is not surprising, with markets extremely extended and overbought, that a failure occurred. However, the bullish backdrop to the market has improved as of late, with important levels of support forming at the 20/100 dma crossover and the 50-dma below that. Pullbacks to either of those levels will provide levels to increase equity exposure given the overbought conditions are reversed, and most importantly, those support levels hold. A failure at the 50-dma will suggest a retest of previous lows.

One concern, as noted in the chart below, is On Balance Volume, which, despite the sharp rally in the market as of late, has shown little pickup suggesting the commitment to rally is weaker than many of the technicals suggest. While we will continue to honor the technical backdrop of the market, for now, we will want to see volume pick up, confirming buyers are coming into the market.

A Divergence Between Growth Stocks and Bonds Worth Following

In our article Inflation or Recession, Which Concern is Driving The Market? we noted that growth stocks performed poorly versus cyclical stocks from January to June but then started outperforming in June. Per the article:

The Fed’s aggressive action and hawkish tone on May 4th combined with even stronger anti-inflation language in the following weeks, appear to have persuaded investors the Fed will tame inflation.

Bond investors are also finding solace in the Fed’s aggression toward inflation. As we share below, the yield on the 10-year Treasury Note may have peaked in mid-June. It has since fallen by half a percent.

The takeaway is that investors were getting more comfortable that the Fed could successfully fight inflation but at the cost of an economic downturn. In such an environment, growth companies and other interest rate-sensitive companies should outperform cyclical stocks whose earnings are tied closely to current economic activity.

Recently, however, the markets may be losing confidence in this theory. As we share below, the NASDAQ (QQQ) and bond prices (TLT) followed similar paths lower from January to June this year. They also bottomed simultaneously in mid-June. From that point, they both rallied, but TLT is petering out while QQQ continues to run. Bond investors are concerned that the Fed pivot narrative may have some truth, and another price surge could result if the Fed stops fighting inflation too early. Growth investors seem enamored with the pivot story but are not focused on how an early pivot could cause higher inflation and interest rates down the road. This divergence in price and opinion is worth following to help assess what investors are thinking.

Driving With The Rearview Mirror

The following comes from our latest article Economic Slowdown Now, Recession Coming in 2023.

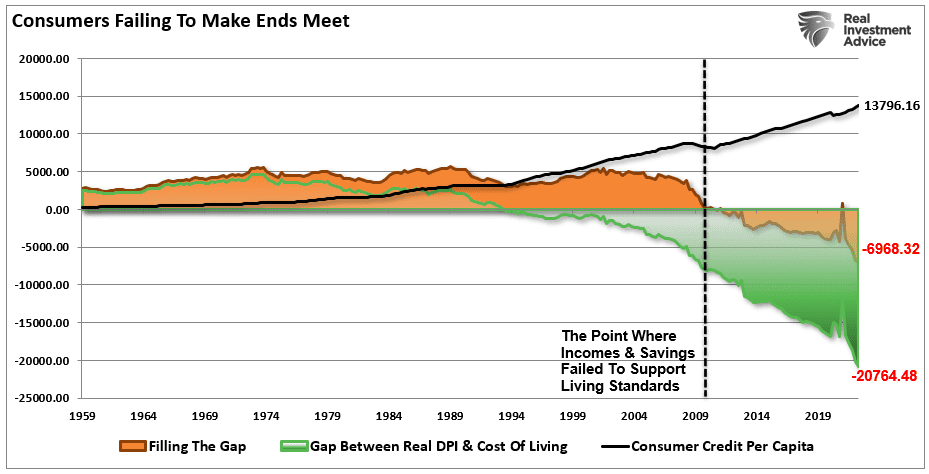

As the Fed continues to hike rates, each hike takes roughly 9-months to work its way through the economic system. Therefore, the rate hikes from March 2020 won’t show up in the economic data until December. Likewise, the Fed’s subsequent and more aggressive rate hikes won’t be fully reflected in the economic data until early to mid-2023. As the Fed hikes at subsequent meetings, those hikes will continue to compound their effect on a highly leveraged consumer with little savings through higher living costs. We have shown previously that the consumer is exceptionally unprepared for such an outcome.

Keep in mind Quantitative Tightening (QT) is ramping up to a $95 billion monthly pace. QT, like interest rate hikes, has a delayed effect on liquidity in the banking system, which flows through to economic activity. Tomorrow’s economy is primarily based on today’s actions. Per the article:

However, given the lag effect of changes to the money supply and higher interest rates, indicators are pretty clear recession risk is very probable in 2023.

NAR- Housing Affordability

As we show below, the National Association of Realtors (NAR) Affordability index recently dropped below 100. The index is based on affordability from the perspective of a median-income family buying a median-priced house. At a level of 100, a median-income family has exactly enough income to qualify for a median-priced home mortgage. Due to the sharp increase in home prices and mortgage rates, median-income families cannot afford a median-income house. Something has to give. Either mortgage rates and/or home prices need to fall to return some balance to the real estate market.

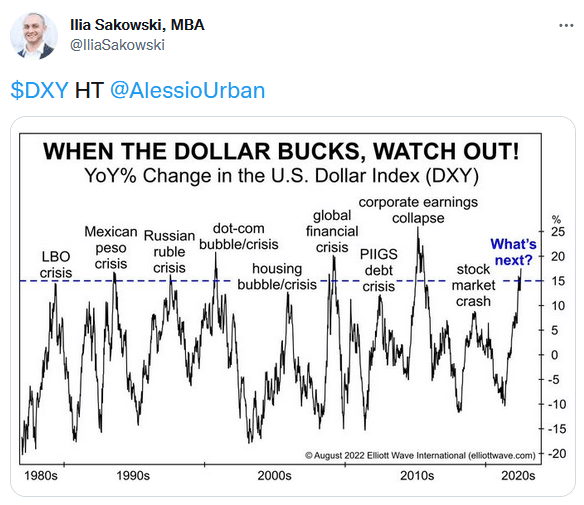

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read