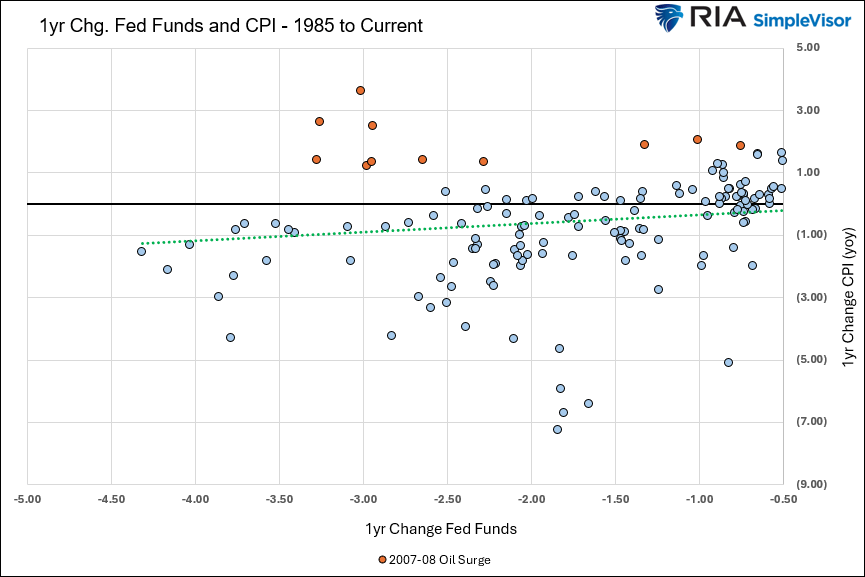

“The Fed will spur another round of inflation with rate cuts.” That line and similar sentiments have been plastered all over social media following the Fed’s aggressive 50 bps rate cut. Given the importance of inflation on asset returns, it is worth looking back at the last 40 years and appreciating the relationship between Fed Fund rate cuts and CPI. The graph below shows every instance in which the year-over-year Fed Funds rate was at least .50bps lower or more over the prior twelve months. It then plots them against the one-year change in CPI. CPI has fallen or remained relatively flat every time the Fed cut rates except for 2007 and 2008. From 2007 to mid-2008, the price of oil tripled to over $150 a barrel. Despite the surge in oil prices, all other prices were tame. To wit, CPI, excluding energy prices during that period, was declining slightly.

There is no evidence that rate cuts have caused inflation since 1985. The rebuttal to this argument recants the inflationary outbreaks of the 1970s and early 1980s. During this period, the inflation rate spiked three times, each higher than the prior instance. We have written a four-part article on the stark differences between then and now and why such a rekindling of inflation is not likely. (Links- ONE, TWO, THREE, and FOUR). We summed up the series as follows:

At its core, inflation is too much money chasing too few goods. That was the case in 2020 through 2022. This is not the case anymore.

The 2020s aren’t the 1970s by any stretch of the imagination!

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, we touched on oil prices and Fed rate cuts. However, the market remains bullishly biased in the short term, with investor sentiment again reaching more exuberant levels. Technically, there is nothing wrong with the market currently. The S&P 500 broke out above its consolidation/correction pattern from August, with the Yen Carry Trade blowup now a distant and non-concerning memory. As is always the case, the market is forward-looking and is focused on improving economic and earnings estimates. As I noted on Twitter/X yesterday, Goldman Sachs has pushed their Q3 economic estimate to 3%.

Furthermore, analysts are pushing their year-end price targets even higher after predictions early this year came far short of reality. The hope is that earnings growth will reach 18% year over year by the end of 2025, supporting much higher price targets.

As the market continues to rack up one new all-time high after another, bullish sentiment builds, dragging more money into the equity chase. The MACD buy signal remains intact, and the markets are not overbought. Given the current deviation from the 50-DMA, further upside is likely limited, suggesting a slower grind higher as the moving average catches up. Such suggests that allocations remain weighted toward equity risk but watch for a pickup in volatility as we get closer to the election. November and December are setting up nicely for a sprint higher into the year-end close with Wall Street analysts now pegging 6000 as the target.

Job Concerns Are Weighing On Consumers

Consumer Confidence fell by the most in three years, as the ZeroHedge chart below shows. Additionally, the index is well below the recent range from the second half of 2021 to earlier this year. Per the Conference Board, the culprit for the sharp drop appears to be increasing concerns about the labor market. To wit:

“The deterioration across the Index’s main components likely reflected consumers concerns about the labor market and reactions to fewer hours, slower payroll increases, fewer job openings — even if the labor market remains quite healthy, with low unemployment, few layoffs and elevated wages,” Dana Peterson, chief economist at the Conference Board, said in a statement.

In a recent article titled Confidence Is The Underappreciated Economic Engine, we discussed confidence’s important role in the economy. We summed it up as follows:

As we led, it doesn’t take much of a change in confidence to tip an economy from running on all cylinders to a recession.

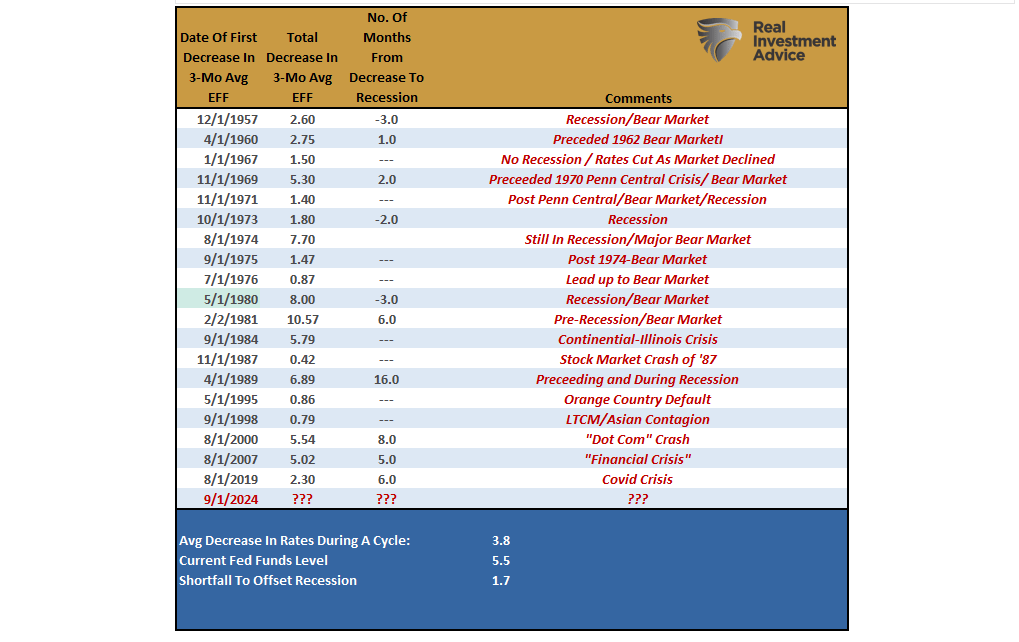

50bps Rate Cut and Outlook

Last week, the Federal Reserve made a significant move by cutting its overnight lending rate by 50 basis points. This marks the first rate cut since 2020, signaling the Fed is aggressively supporting the economy amid a backdrop of softening economic data. For investors, understanding how similar rate cuts have historically impacted markets and which sectors tend to benefit is key to navigating the months ahead.

In this post, we will explore the historical market performance following similar 50-basis-point rate cuts, highlight the best-performing sectors and market factors after such cuts, and outline three critical risks investors should be aware of heading into year-end.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.