Our title above about Avis Budget Group (CAR) shares is a gross understatement. Since March 20th, CAR has risen nearly 500%, as we share below. While there are, and were, some favorable tailwinds driving the upward trend, such as rising used-car prices and elevated rental-car usage during the TSA-related problems, the most glaring factor is a massive short squeeze on its stock.

With 54% of the float sold short as of the latest reporting period, which ended late March, CAR was the most heavily shorted Russell 1000 stock. As we have seen play out with meme stocks like GameStop and AMC, such a high ratio of short sales makes CAR shares prime for a squeeze. As CAR initially rose, some short sellers were forced to cover their positions by buying shares, thereby accelerating the rally. Moreover, as the stock continued higher, more longs entered the market, further exacerbating the situation. And at the same time, some short traders added to their short position, providing even more upside fodder.

While CAR can certainly go higher, the move is not sustainable. The reason is quite simply that CAR’s fundamentals are horrendous. CAR entered 2026 with over $25 billion in debt, a near-$1 billion net loss, flat-to-declining sales, and just over $500 million in cash.

The risk for short sellers: In late March, Avis launched an offering to sell up to 5 million shares directly into the market. The higher price provided CAR a rare opportunity to chip away at its massive debt load. Don’t be surprised when they issue more dilutive shares now that the stock is multiples of where it was in late March.

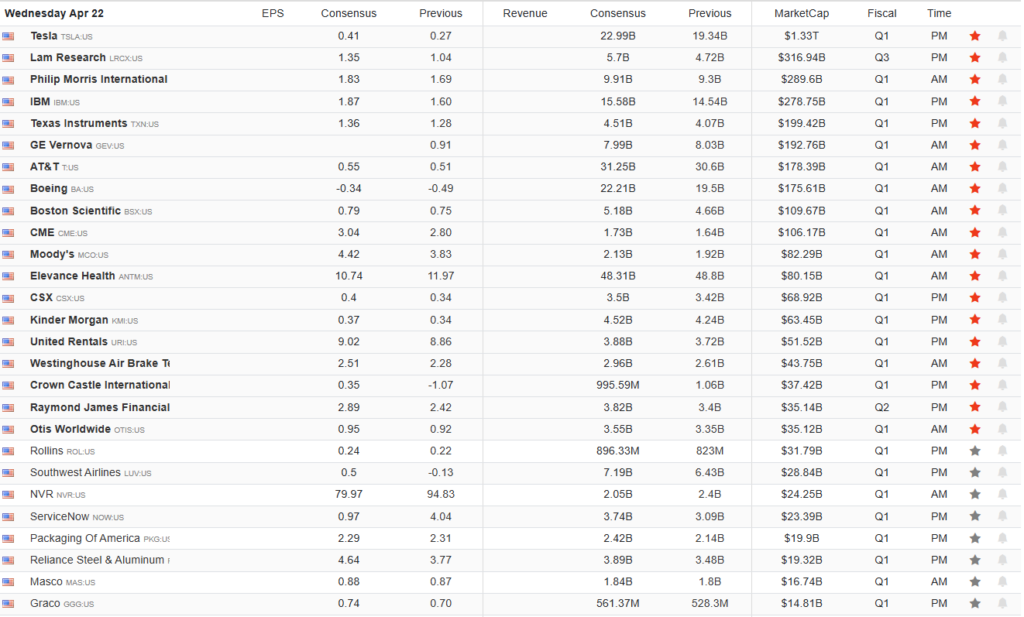

What To Watch Today

Earnings

Economy

- No major releases today

Market Trading Update

Yesterday, we discussed that, on a weekly chart, the recent decline was much like what we have seen in prior correction periods. Two notable points were that 1) such rallies don’t retrace to lows, and 2) denote a completion process of the previous correction cycle and the return to the bullish trend. More importantly, we are in the midst of an earnings cycle that continues to signal stronger earnings growth ahead. This brings us to an important discussion.

Social media has been awash with dramatic proclamations that “the dollar is dying” and “nobody wants the USD.” The narrative has become so pervasive that it risks hardening into a consensus. However, a quick glance at the chart tells a more nuanced story. While the Dollar Index (DXY) has drifted lower over the past two years, it remains near 98 today, essentially flat over the trailing 12 months and still well above its long-term historical averages. That is hardly the collapse being advertised.

More importantly, the flow of foreign capital into U.S. assets has not merely held steady; it has accelerated. According to the latest Treasury International Capital (TIC) data, foreign residents purchased a net $101 billion of long-term U.S. securities in February alone, following November’s blockbuster $222 billion print. Over the last five reporting months, foreigners have added roughly $488 billion to U.S. long-term stocks and bonds, a pace that rivals the post-COVID liquidity surge and flatly contradicts the “capital flight” story.

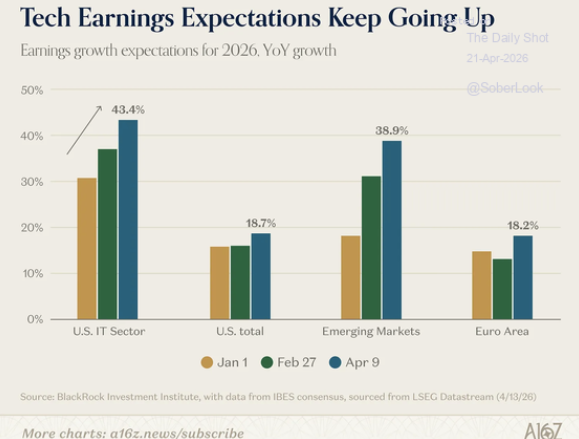

The why behind those flows becomes obvious when we examine earnings. Consensus expectations for the U.S. IT sector have ratcheted higher throughout 2026, with earnings growth now projected at 43.4%, up from 30.9% at the start of the year. Emerging markets follow at 38.9%, while the U.S. total is pegged at 18.7%. More telling still, Info Tech earnings are expected to grow more than 2x faster than the S&P 500 as a whole (40% vs. 18%), with only Energy and Materials meaningfully outpacing the index.

Global capital allocators face a stark choice: accept mid-single-digit growth across Europe and much of the developed world, or own the companies actually building the AI infrastructure layer. That is not really a choice.

As long as U.S. earnings growth remains this differentiated, driven overwhelmingly by the AI capital cycle, foreign flows should continue to underpin both the dollar and U.S. equity valuations, regardless of the “dollar is dying” chorus on social media. Investors should position accordingly.

Narratives make headlines; flows make markets. Trade accordingly.

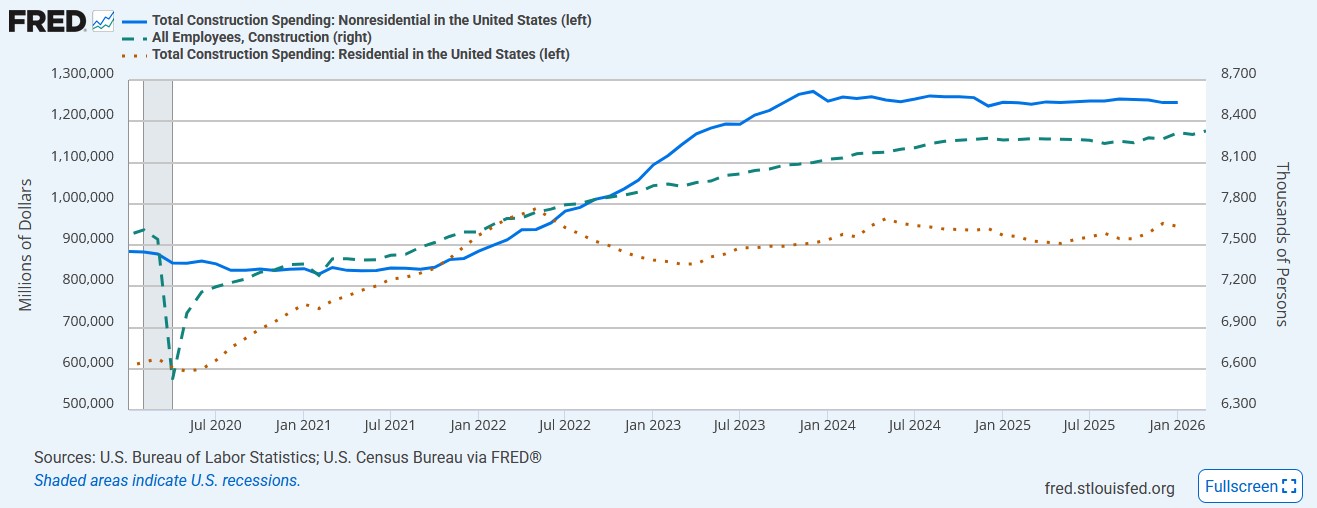

Construction Labor Holds Up

Construction jobs, like construction spending, tend to be highly cyclical, changing with the pace of economic activity. While the economy has held up reasonably well, residential and non-residential construction spending has been flat, as we share below. Yet, the number of employees working in the construction industry has been steadily rising.

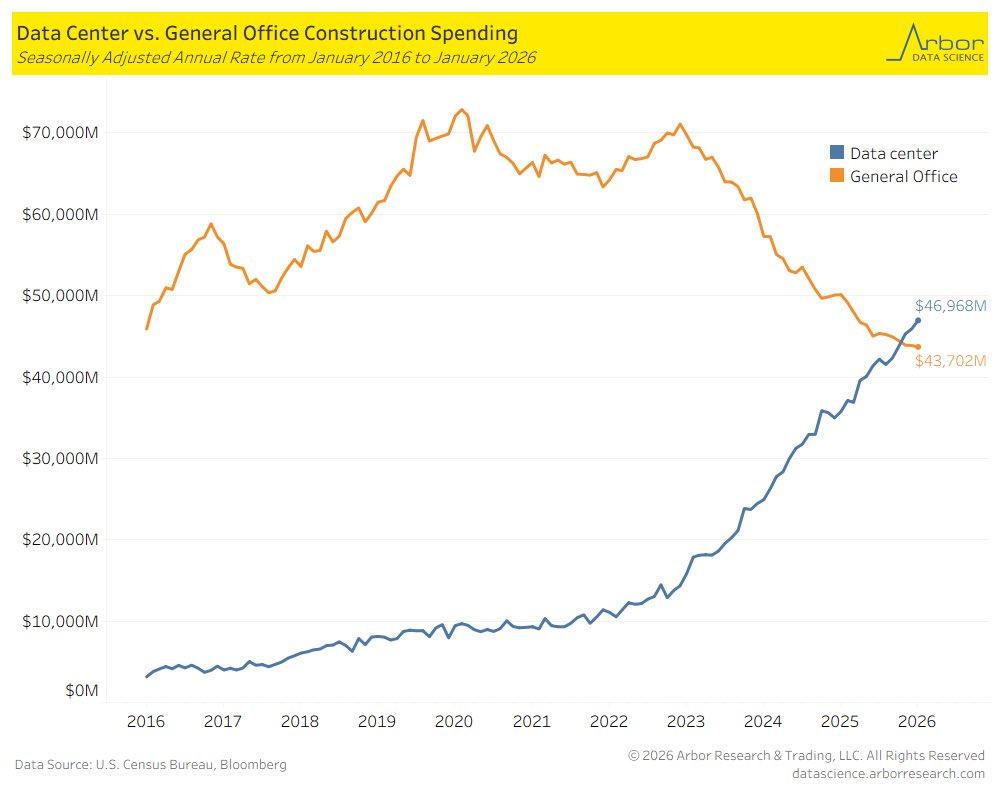

We believe this anomaly is largely due to construction spending in data centers. The second graph shows that data center construction spending has grown from $3 billion in 2016 to $47 billion today. Moreover, spending on data centers has overtaken that spent on offices.

Inflationary Anxiety Boosts Retail Sales

Retail sales, excluding auto and gas prices, rose by 0.6%. While that was slightly below expectations for a 0.8% gain, it was a strong pace. Consider that the data was collected in mid-March, when consumer sentiment was very low, and oil prices were soaring. It appears that the boost in sales may be partly due to front-running. Higher oil prices and related goods are creating some anxiety among consumers, and it’s likely that quite a few have bought items they might have bought later to avoid higher prices. This is similar to the tariff front-running we saw in early 2025. While it boosts sales in the present, it has a dampening effect on future sales.

Per the Conference Board Consumer Sentiment Index:

Unsurprisingly, given the Iran war oil shock, consumers’ average and median 12-month inflation expectations surged in March to levels last seen in August 2025, when US consumers awaited more tariff announcements from the US federal government.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.