Why this isn’t 1920 has everything to starting valuations and future returns. While, generally, I’m not too fond of comparisons between today’s markets and the past, Ed Yardeni made a comparison too bombastic to disregard in his blog:

“We live in interesting, though not unprecedented, times. The Roaring 1920s could be a precedent for the Roaring 2020s.

The good news is that the bad news during the previous precedent was followed by the Roaring 20s. So far, the 2020s has started with the pandemic, but there are plenty of years left for the prosperous 1920s to become a precedent for the current decade.

The 1920s ended with a stock-market melt-up followed by a meltdown. The 2020s may already be seeing a melt-up, begun on March 23.”

Ed’s point was the economic and industrial revolution that occurred following WWI is a precedent for the next decade. The urbanization of populations moving from farms to cities, the rise of manufacturing and technological innovations from Henry Ford and the Model T, to the “bulldozer,” to refrigeration and not to mention the radio.

1920 Was The Bottom

Yes, the ’20s marked the start of a period of marvel and rapid change.

1920 also marked the end of a 20-years of economic destruction. A series of events rocked the turn of the 20th century, which deeply suppressed financial markets. ((Imagine 20-years with negative total real returns.)

- Panic of 1907

- Recession in 1910-1911

- Recession in 1913-1914

- World War I ran from 1914-1918

- Economic Depression in 1920-1921

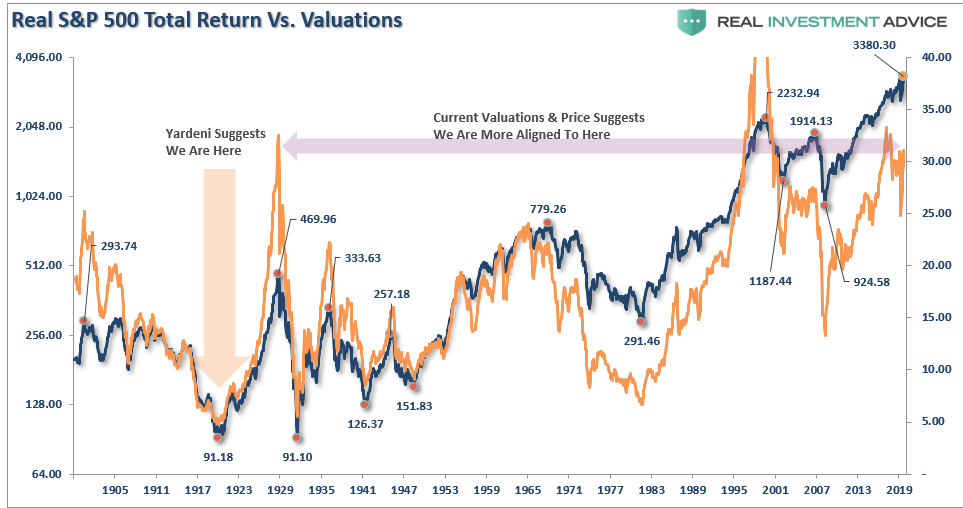

The market “melt-up” was undoubtedly driven by an economic recovery, a surge in innovation, etc. but was supported by historically low valuations. (Current valuations align with 1929 more than 1920.)

While I certainly agree with the fact the companies today are spending a tremendous amount of money on technology and innovation, this is a significant difference.

The innovations in the early 1900s put increasing numbers of people to work. Those increases in jobs led to higher wages and more robust economic growth. Today, companies are spending money on innovation and technology to increase productivity, reduce employment, and suppress wage pressures.

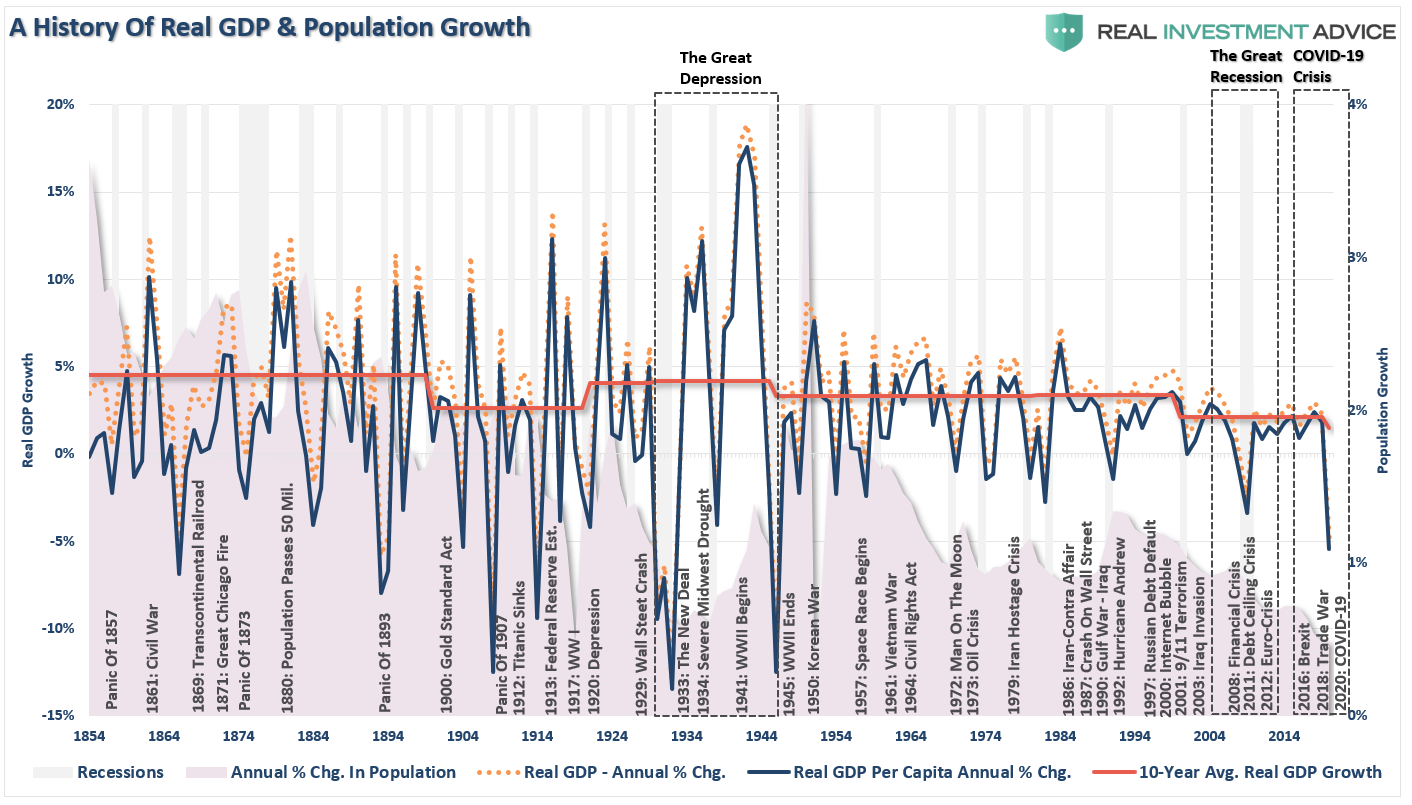

Look at the chart below. The history of the economy and related events shows the difference between then and now. Notice the strong economic growth rates in the 1920-1940 period as compared to today.

Yardeni’s primary point is that history suggests a massive melt-up is coming for the financial markets. There are challenges to this view based on what history tells us about valuations and forward returns.

Valuations Don’t Matter

In the short-term, a period of one year or less, political, fundamental, and economic data has very little influence over the market. Such is especially the case in a late-stage bull market advance where the momentum chase has exceeded the grasp of the risk undertaken by investors.

In other words, in the very short-term, “price is the only thing that matters.”

Price measures the current “psychology” of the “herd” and is the clearest representation of the behavioral dynamics of the living organism we call “the market.”

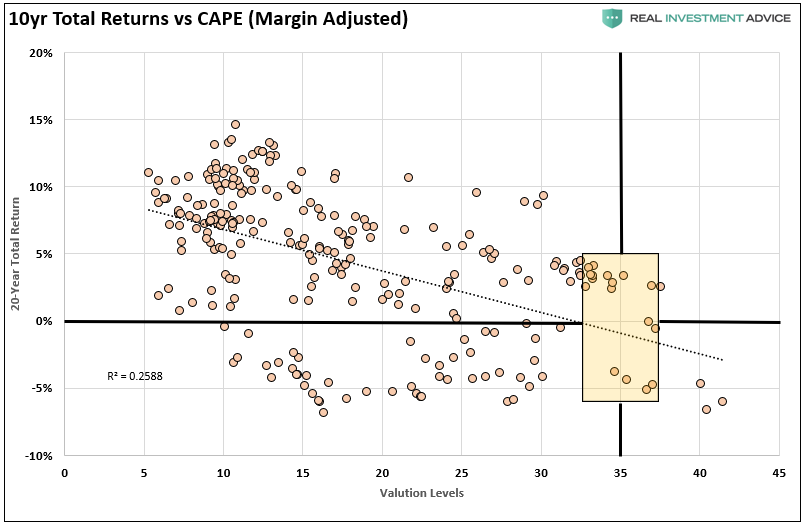

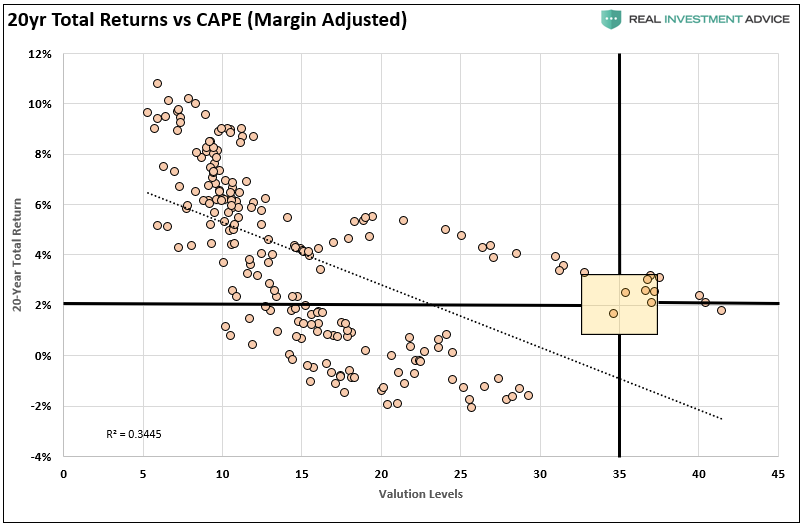

But in the long-term, fundamentals are the only thing that matters. Both charts below compare 10- and 20-year forward total real returns to the margin-adjusted CAPE ratio.

Both charts suggest that forward returns over the next one to two decades will be somewhere between 2-3%.

“P/E’s don’t matter anymore because of Central Bank interventions, accounting gimmicks, share buybacks, etc.”

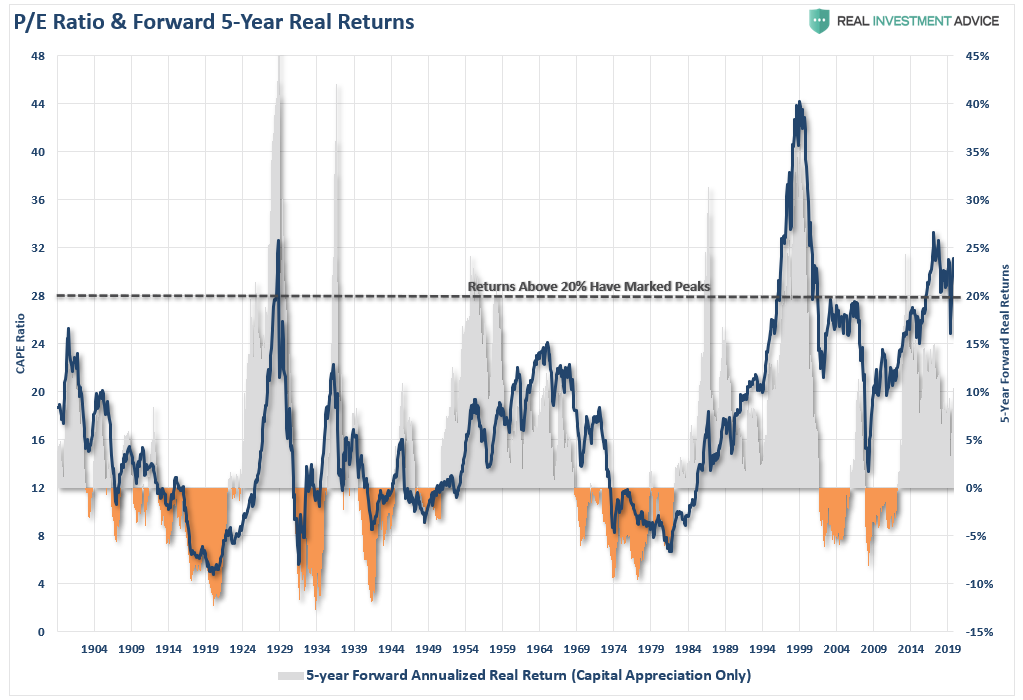

However, as we will discuss in more detail in a moment, they do matter. The chart below compares trailing valuations to forward 5-year returns on stocks. Again, as noted above, the disparity between current CAPE valuations today at 31x versus 5x earnings in 1920 could not be starker.

There are two crucial things you should take away from the chart above.

- Market returns are best when coming from periods of low valuations; and,

- Markets have a strong tendency to revert to their average performance over time.

Bogle And Thaler

The late Jack Bogle, the founder of Vanguard, confirmed the same:

“The valuations of stocks are, by my standards, rather high, butmy standards, however, are high.”

[Note: Bogle’s method differs from Wall Street’s. For his price-to-earnings multiple, Bogle uses the past 12 months of reported earnings by corporations, GAAP earnings, which includes ”all of the bad stuff.”]

‘Wall Street will have none of that. They look ahead to the earnings for the next 12 months and we don’t really know what they are so it’s a little gamble.’

[Note: Bogle also noted that Wall Street analysts look at operating earnings, “earnings without all that bad stuff,” to come up with a lower price-to-earnings multiple.]

“If you believe the way we look at it, much more realistically I think, the P/E is relatively high. I believe strongly that [investors] should be realizing valuations are fairly full, and if they are nervous they could easily sell off a portion of their stocks.”

Richard Thaler, the famous University of Chicago professor who won the Nobel Prize in economics, also stated:

“We seem to be living in the riskiest moment of our lives, and yet the stock market seems to be napping. I admit to not understanding it.

I don’t know about you, but I’m nervous, and it seems like when investors are nervous, they’re prone to being spooked. Nothing seems to spook the market.”

Wash, Rinse, & Repeat

As noted, the flood of liquidity, and accommodative actions, from global Central Banks, has lulled investors into a state of complacency rarely seen historically. However, while market analysts continue to come up with a variety of rationalizations to justify high valuations, none of them hold up under real scrutiny. The problem is the Central Bank interventions boost asset prices in the short-term; in the long-term, there is an inherently negative impact on economic growth. As such, it leads to the repetitive cycle of monetary policy.

- Using monetary policy to drag forward future consumption leaves a larger void in the future that must be continuously refilled.

- Monetary policy does not create self-sustaining economic growth and therefore requires ever-larger amounts of monetary policy to maintain the same level of activity.

- The filling of the “gap” between fundamentals and reality leads to consumer contraction and, ultimately, a recession as economic activity recedes.

- Job losses rise, wealth effect diminishes, and real wealth is destroyed.

- The middle class shrinks further.

- Central banks act to provide more liquidity to offset recessionary drag and restart economic growth by dragging forward future consumption.

- Wash, Rinse, Repeat.

If you don’t believe me, here is the evidence.

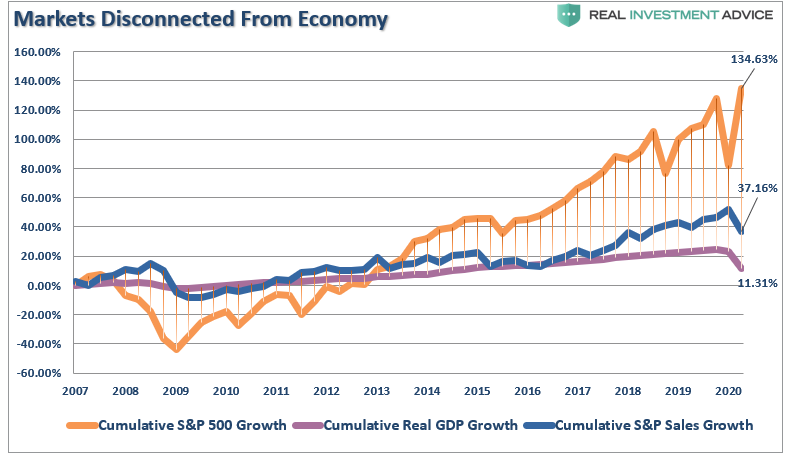

The stock market has returned more than 130% since 2007 peak, which is more than 12x the growth in corporate sales and 3.6x more than GDP.

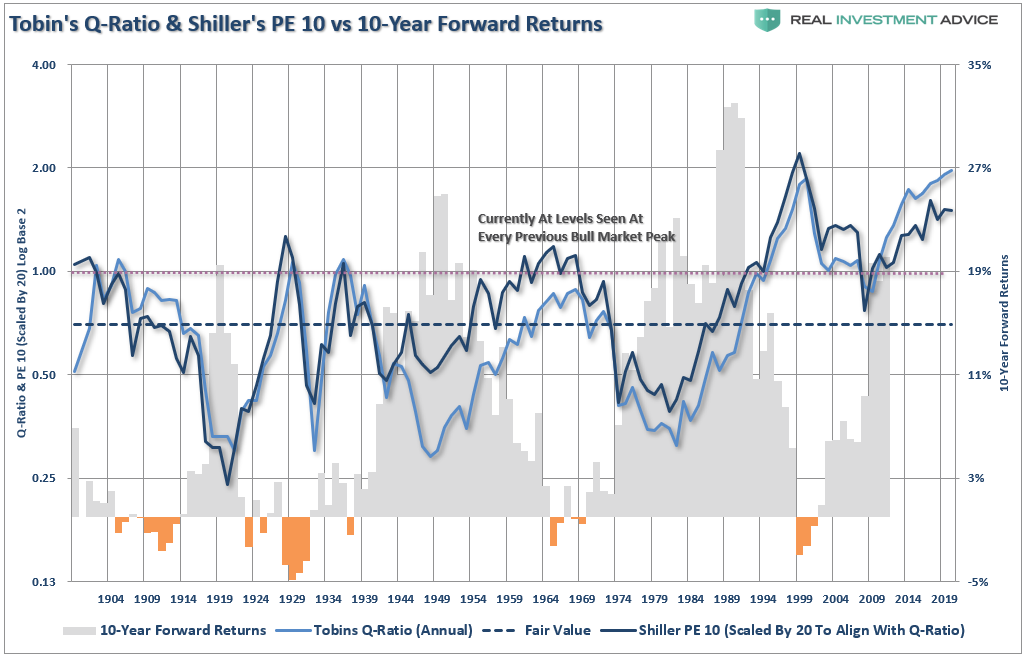

Tobin’s Q

As noted, valuations, by their very nature, are HORRIBLE predictors of 12-month returns should not be used in any strategy that has such a focus. However, in the longer term, valuations are strong predictors of expected returns.

In the following series of charts, I am using forward 10-year returns just for consistency as some of the data sets utilized don’t yet have enough history to show 20-years of forward returns.

The purpose here is simple. Based on a variety of measures, is the valuation/return ratio still valid, OR, is this time different?

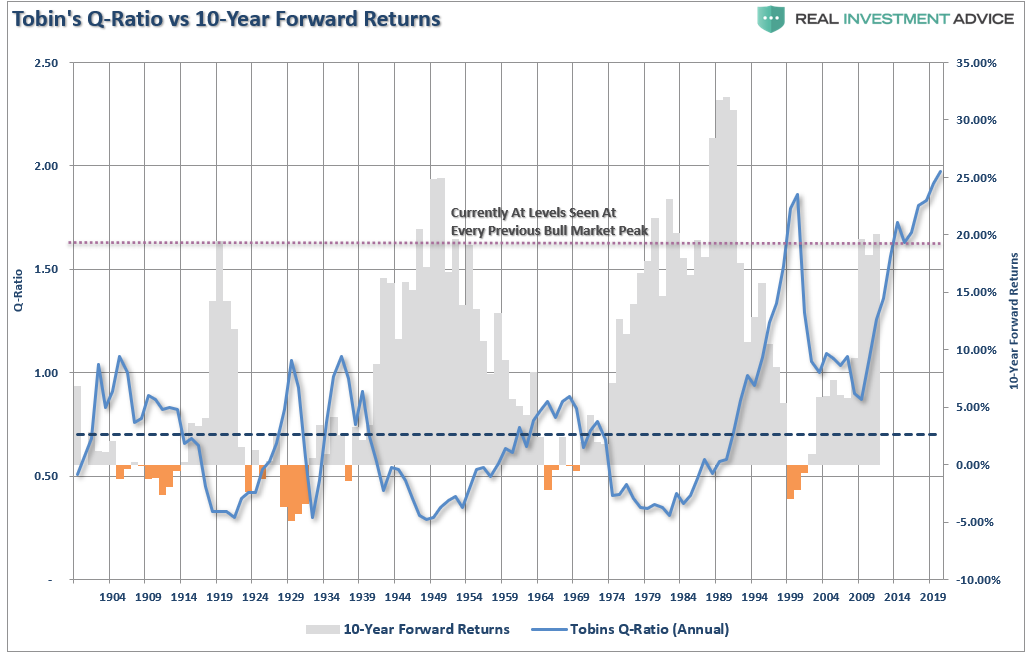

Tobin’s Q-ratio measures the market value of a company’s assets divided by its replacement costs. The higher the ratio, the lower the future returns.

Just as a comparison, I have added Shiller’s CAPE-10. Not surprisingly, the two measures not only have an extremely high correlation, but forward return outcomes remain the same.

Importantly, notice that when both measures are low, as in 1920, 1950, 1980, and even 2009, forward returns for investors were strong. Forward returns from high valuations have not been so beneficial.

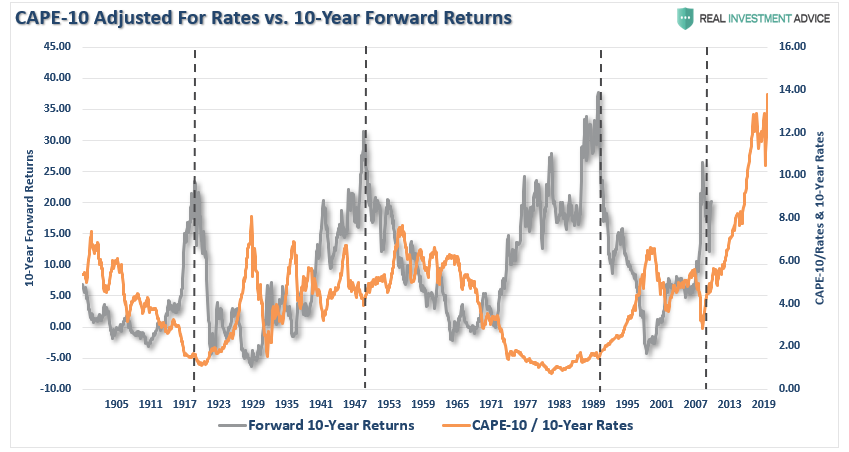

Rates, Sales & Buffett

One of the arguments has been that higher valuations are okay because interest rates are so low. Okay, let’s take the smoothed P/E ratio (CAPE-10 above) and compare it to the 10-year average of interest rates going back to 1900.

The analysis that low rates justify higher valuations does not withstand the test of history.

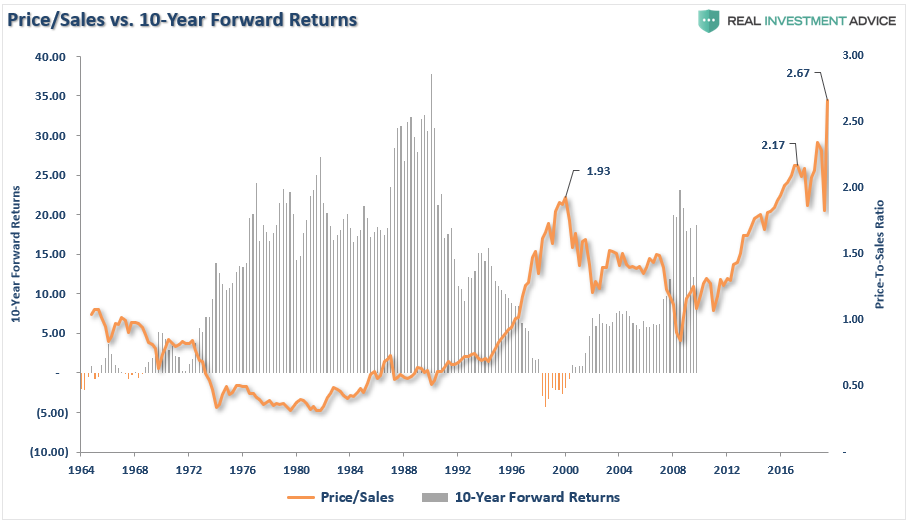

But since earnings are manipulated through a variety of accounting gimmicks, we can look at “sales” or “revenue,” which occurs at the top-line of the income statement. Not surprisingly, the higher the level of price-to-sales, the lower the forward returns have been. You may also want to notice the current price-to-sales is pushing the highest level in history as well.

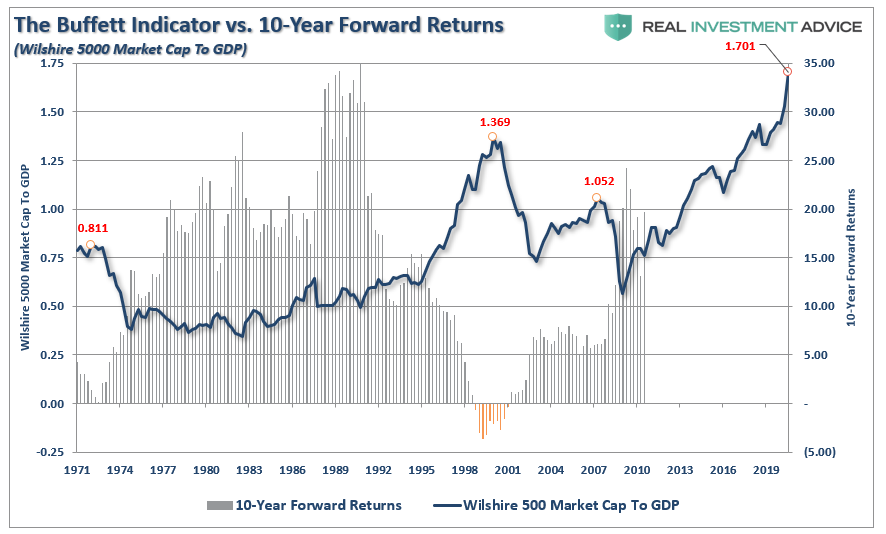

Even Warren Buffett’s favorite indicator, market cap to GDP, clearly suggests that investments made today will have a rather lackluster return over the next decade.

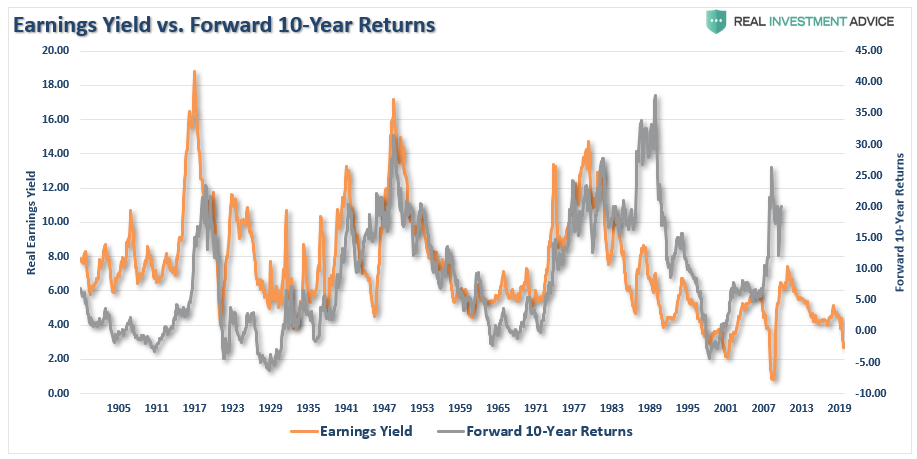

If we invert the P/E ratio, and look at earnings/price, or more commonly known as the “earnings yield,” the message remains the same.

Conclusion

No matter how many valuation measures you use, the message remains the same. From current valuation levels, the expected rate of return for investors over the next decade will be low.

There is a large community of individuals who suggest differently, as they make a case as to why this “bull market” can continue for years longer. Unfortunately, any measure of valuation does not support that claim.

Such does not mean that markets will produce single-digit rates of return each year for the next decade. The reality is there will be some great years to be invested over that period. There will likely also be a couple of tough years in between.

That is the nature of investing. It is just part of the full-market cycle.

While I certainly hope Mr. Yardeni is correct in his thesis, valuations suggest differently.

The economic cycle, demographics, debt, and deficit, also suggest his optimistic view is unlikely.

Mr. Yardeni is correct on the point he made with his quote from Mark Twain:

“History doesn’t repeat itself, but it often rhymes.”