On Monday, the markets surged on hopes for a “virus vaccine” and encouraging words for the Federal Reserve that liquidity isn’t going away. Such puts us in the awkward position of having to chase market momentum, knowing fundamentals will eventually matter.

As portfolio managers, we are in the unfortunate position of having to deliver performance for our clients. Such means that while “fundamentals” paint a very an inferior risk/reward environment for investors, momentum continues to trump reason.

As I noted in “The Great Divide:”

“The juxtaposition between economic data and the ‘bull market’ in stocks is quite astonishing.”

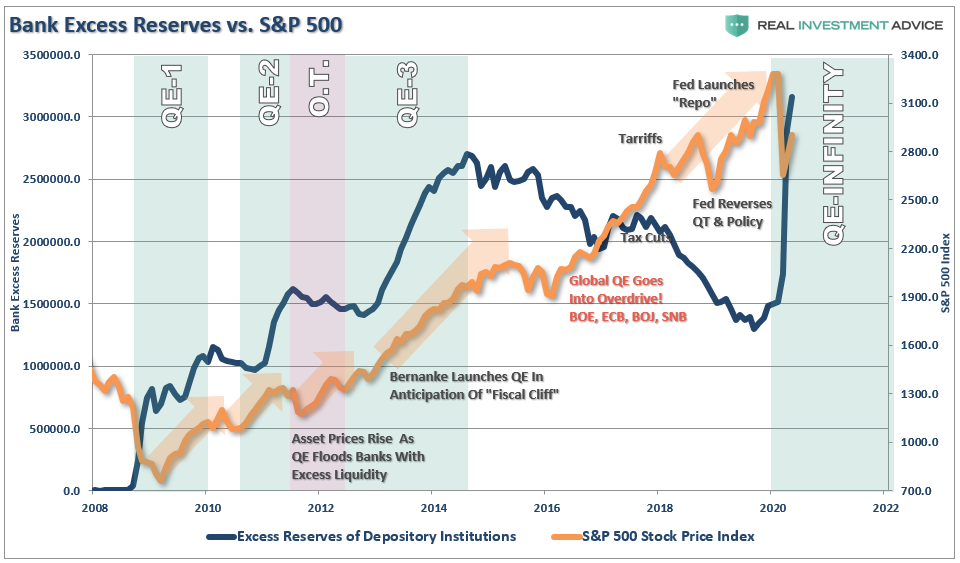

“In other words, to no one’s real surprise, the driver of the market is simply ‘The Fed.’ As the Fed engages in ‘QE,’ it increases the “excess reserves” of banks. Since banks are NOT lending to consumers or businesses, that excess liquidity flows into the stock market.”

Jerome Powell’s promise of “unlimited liquidity” on Sunday’s 60-minutes interview was all the markets needed on Monday to take out the trading range.

Fundamentals Will Matter

I certainly understand it seems like “fundamentals don’t matter.” However, eventually, they will.

For now, the excuse is that markets are looking “past” 2020 and into 2021. While such may indeed be the case, there are two problems with that assessment.

- The current advance is pricing in the best possible outcomes in the future, i.e., a “v-shaped” economic recovery, a successful vaccine, and no secondary viral outbreak. A failure on any, or all, of those outcomes, will leave a void beneath stocks.

- With earnings estimates already dropping for 2020 and 2021, investors who are looking past 2020 are banking on a “hockey stick” recovery in earnings. However, there is more than a substantial risk earnings fall a lot more before they start to recover.

We addressed the second point in “Stuck In The Middle:”

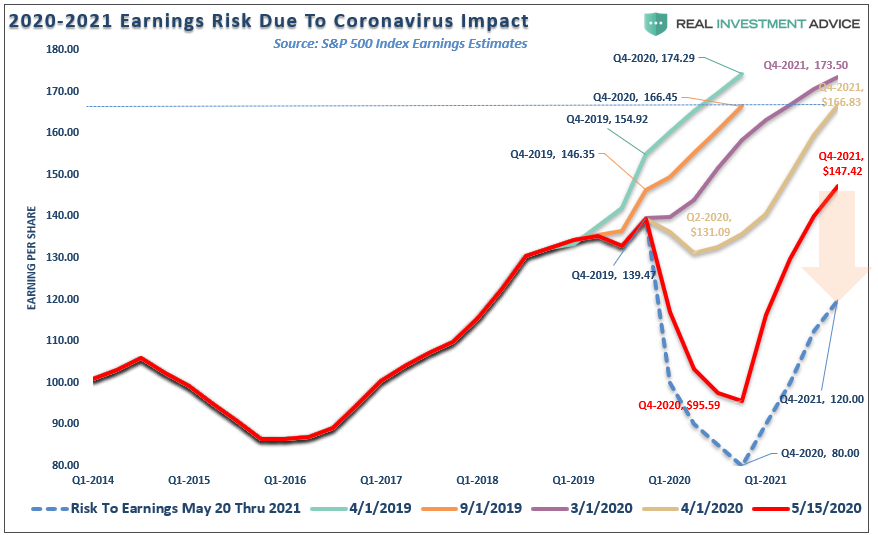

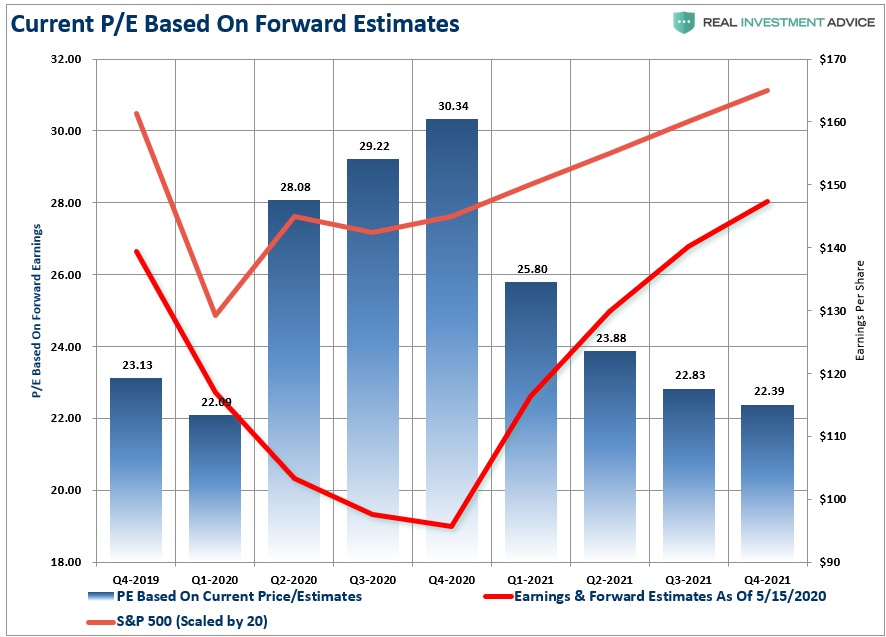

“The other problem is investors remain overly optimistic about the recovery prospects for earnings going into 2021. As shown, in April 2019, estimates for the S&P 500 was $174/share (reported earnings) at the end of 2020. Today, estimates for Q4-2021 now reside at $147/share. Such is a 15% contraction in estimates when we are discussing a 30-40% decline in GDP.”

“With expectations for the S&P 500 to return to all-time highs in 2021, such would mean that valuations currently paid by investors remain at historically high levels.”

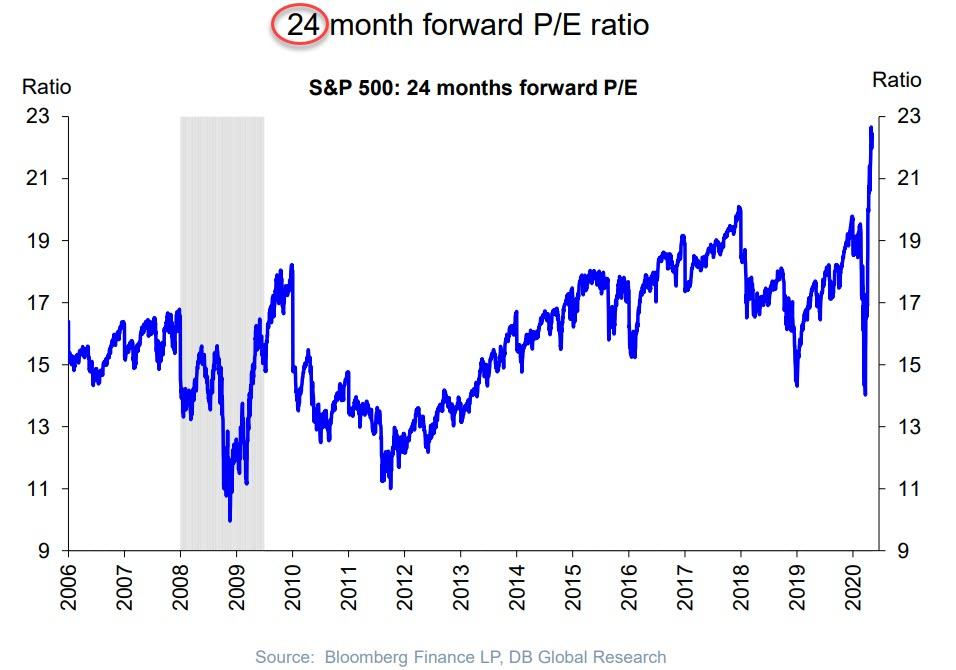

But it isn’t just me, Goldman Sachs is showing the same thing. (Chart courtesy of ZeroHedge)

“Goldman is lowering its EPS growth estimates for 3Q to -30% (from -21%) and no longer sees a full recovery in the fourth quarter, instead of expecting Q4 EPS to be down -17%Y/Y (from +27%) “to reflect a more gradual recovery with quarterly EPS remaining below 2019 levels for the full year.”

All That Matters Is Momentum

Despite the fundamental problems, all that matters currently is the Fed. With momentum pushing stocks higher, as noted above, we have to allow for participation in portfolios while managing inherent risk.

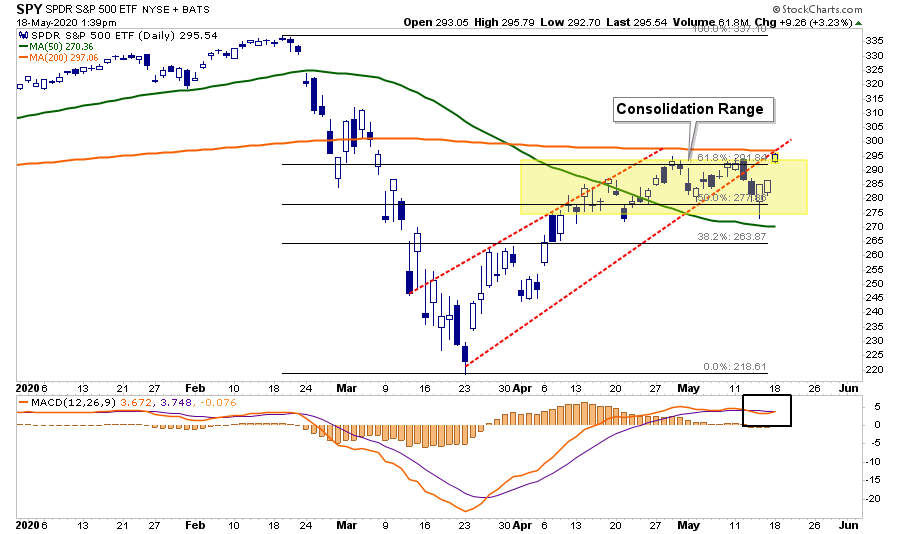

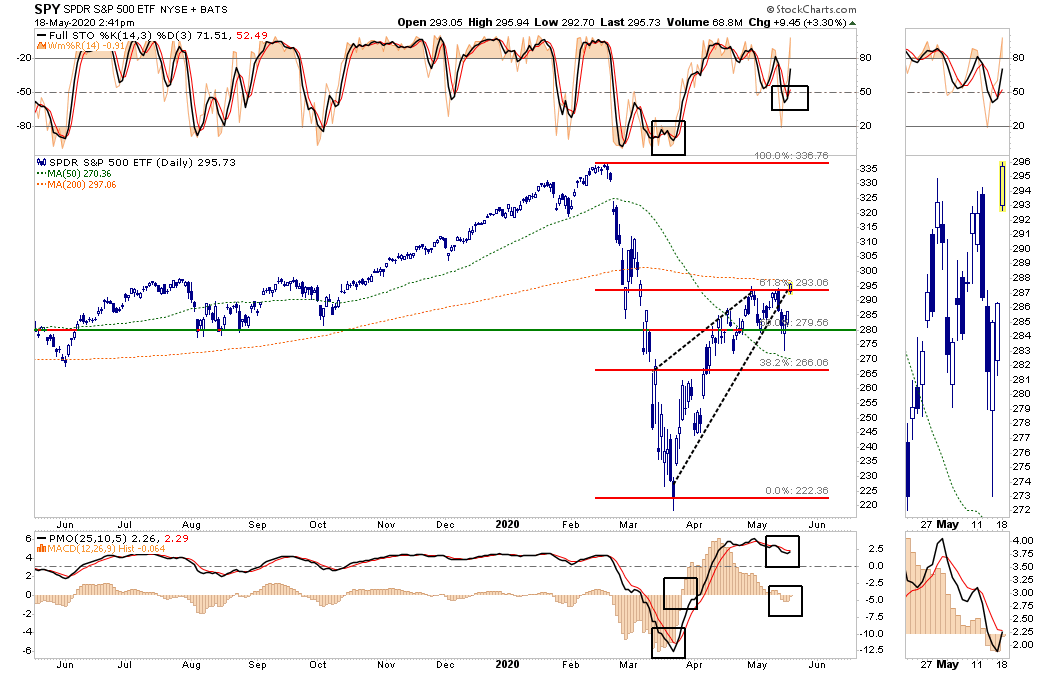

The breakout of the month-long consolidation range to the upside, and above the 61.8% retracement level is indeed bullish.

The “gap up” opening on Monday also flipped the short-term “sell signals” back to “buy,” which suggests we could potentially see some follow-through over the next couple of days.

The “bad news,” if you want to call it that, is the market is now wrestling with both the 200-dma, and the previously broken uptrend line. This level of resistance will be important for the “bulls” to conquer if the markets are going to push higher in the near term.

If the “momentum” trade can indeed break above the 200-dma there is little to stop the market from rallying back to 3100. However, the more extreme overbought conditions will also potentially limit the upside in the short-term.

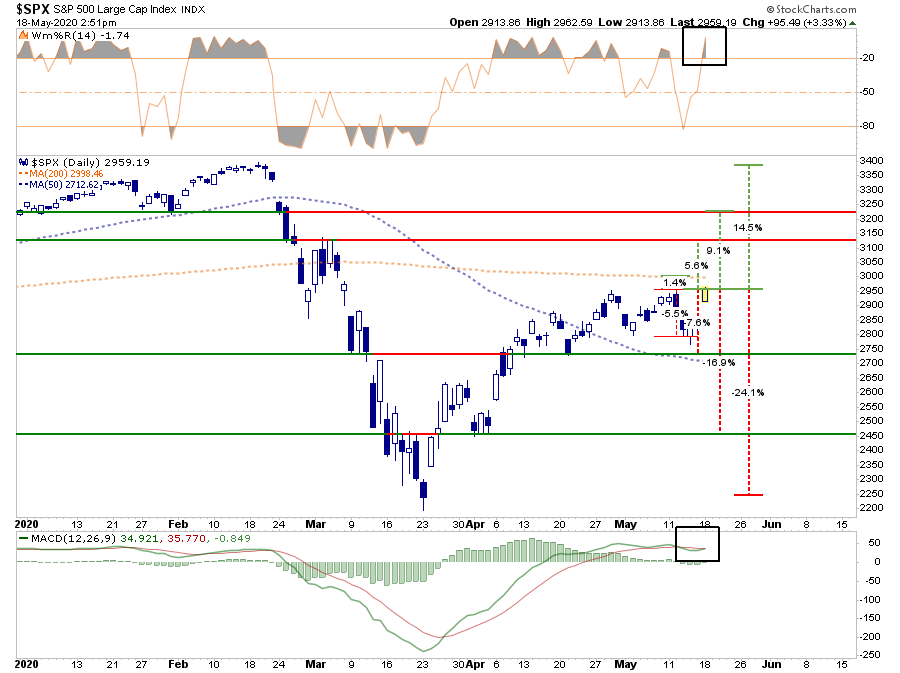

Re-Evaluating Risk & Reward

The last time the market was at 2900, we laid out the risk/reward suggesting there was downside risk to the 50-dma. The sell-off last week approached that level of support. With the rally and breakout, yesterday, we can re-evaluate those risk/reward brackets.

- -5.5% to last week’s lows vs. 1.4% to the 200-dma. Risk/reward negative.

- -7.6% to the 50% retracement/50-dma vs. 5.6% to the March peak. Risk/reward negative.

- -16.9% to the April 1st lows vs. 9.1% to January’s bottom. Risk/reward negative.

- -24.1% to the March 23rd low vs. 14.5% to all-time highs: Risk/reward negative.

While it may not seem like it at the moment, the risk of a downside retracement, as we head into summer months, outweighs the current upside. Importantly, this does NOT mean the markets can’t rally to all-time highs. It is possible. It is also just as likely that things do go as smoothly as planned, and we wind up retesting March lows.

Such is why we have to weigh the risk and reward of chasing markets.

Positioning Changes

With seasonal sell signals in place, we are very focused on our positioning. Over the last couple of weeks, we have continued to increase our equity exposure. However, as noted previously, we continue to do so in areas that remain defensive, currently out of favor, or opportunistic.

We also balanced our increases in “risk” exposure with matched weights in shorter-duration Treasury bonds, gold, or dollar hedges to reduce our risk.

Yes, we are clearly chasing momentum at the moment. However, we do so with a clear understanding of our risk, reward, and overall net positioning. We continue also to hold a larger than normal level of cash to mitigate volatility risk.

As portfolio managers, we have an obligation to our clients to “make money” when we can. We have a “fiduciary duty” to protect them from significant declines that would destroy their financial plans.

The Pin That Pricks The Bubble

The problem for the market going forward, as noted, is that markets have priced in a speedy recovery back to pre-recession norms, no secondary outbreak of the virus, and a vaccine. If such does turn out to be the case, the Federal Reserve will have a very big problem.

The “unlimited QE” bazooka is dependent on the Fed needing to monetize the deficit and support economic growth. However, if the goals of full employment and economic growth are quickly reached, the Fed will face a potential “inflation surge.”

Such will put the Fed into a very tight box. The surge in inflation will limit their ability to continue “unlimited QE” without further exacerbating the inflation problem. However, if they don’t “monetize” the deficit through their “QE” program, interest rates will surge, leading to an economic recession.

It’s a no-win situation for the Fed.

It’s worse for consumers as the Fed’s actions have historically operated as a “wealth transfer” system from the middle-class to the rich.

The only outcome that allows the Fed to monetize the deficit without an inflationary surge is for fundamentals to matter ultimately. A reversion in asset prices will provide the cover needed to continue monetary interventions, but it also means “bullish case” didn’t work out as expected.

Of course, this has always been the case historically. Just as the “Coyote” always wound up going over the cliff when chasing the “Roadrunner,” excessive bullish optimism is always met with disappointment.