Starting last Friday, interest began accruing on student loans, and on October 1, payments will be due. Over three years ago, the CARES Act allowed student loan forbearance until September 2020. It was ultimately extended multiple times. As payments begin, the weight of student loan payments will dampen consumption and economic activity. The question is- how much? To help us assess the economic effect, Distill put out an excellent research paper. It starts as follows: “Student loan repayments will sting far more than most folks believe.” Given its economic importance, we summarize a few of their main points.

There are $1.8 trillion of student loans, of which $1.4 are federal and have been in forbearance. 62% of borrowers are under the age of 40 and have an average balance of $32k. Distill estimates that those who will now be making payments will reduce discretionary spending by 9% to 15%. Per their calculations, the payments could impact retail sales by .60% to 1.00%. It’s likely that 20-somethings, which account for about a fifth of the new payees, will pare back on discretionary spending to make their payments. The 30-somethings, the largest cohort, will likely reduce spending on household formation. Distil’s warning: “Consumers don’t spend when they are angry or afraid.”

What To Watch Today

Earnings

Economy

Market Trading Update

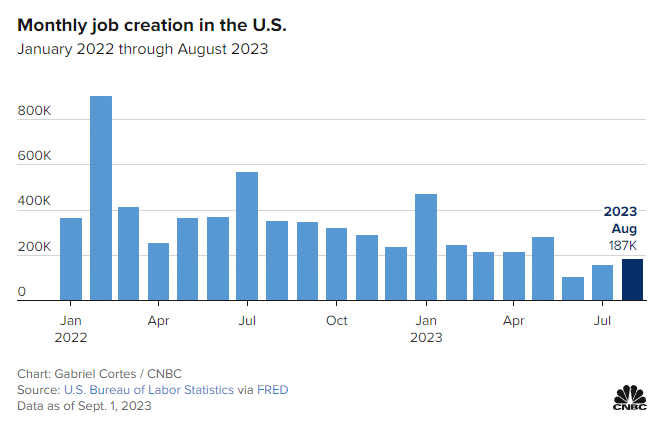

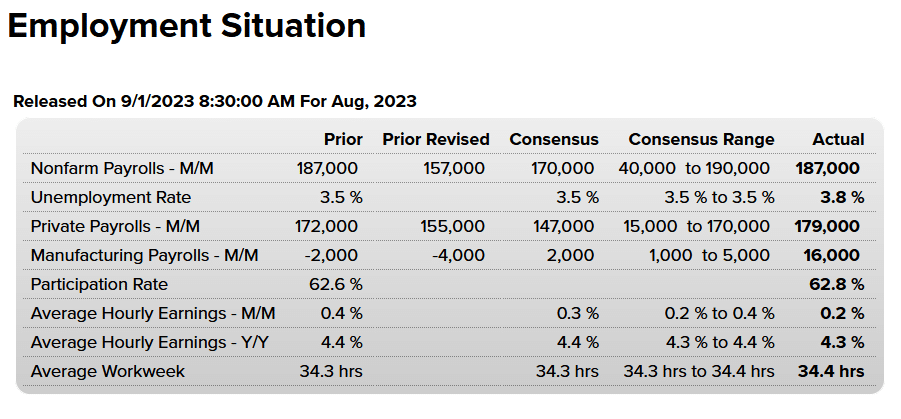

On Friday, the much-anticipated employment report printed a 187,000 job increase, but notably, the unemployment rate rose to 3.8%. The increase in the unemployment rate encouraged the bulls as the goal of the Federal Reserve tightening the financial conditions in the economy was to slow employment and reduce economic demand. Notably, previous months showed fairly significant downward revisions.

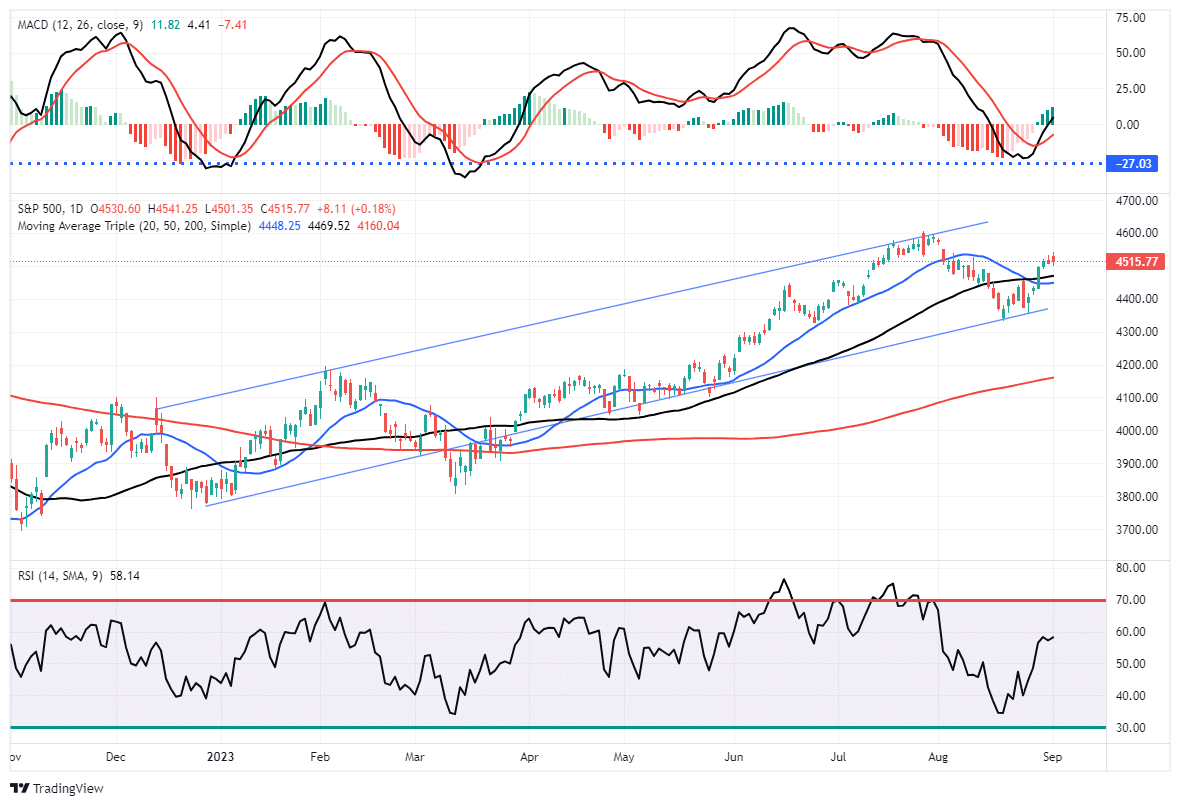

From a market perspective, that “weaker-than-expected” economic data adds to the “hope” that the Fed has tightened financial conditions enough. As we noted last week.

“A correction was needed, given the market was up more than 15% in the year’s first half. Nonetheless, the market continues to trade within its bullish trend and tested and rallied off that level on Friday for a second time. It also remains above critical support levels for now. With the MACD “sell signal” beginning to turn and the RSI index improving, we could see a further rally next week.“

This past week, the market did rally fairly strongly, taking out resistance levels at the downtrend from the July peak and the 50-DMA. The market is now in a technical position to retest the July peak and potentially set new highs for the year. Unsurprisingly, the advance is still dominated by “Mega-7” capitalization stocks.

This all aligns with our analysis over the last couple of weeks wherein:

“As long as nothing ‘breaks,’ when this corrective cycle completes, we expect a rally into year-end. Such will be a function of performance chasing as portfolio managers play catch up into year-end.”

That scenario is still playing out for now. While we could certainly see a pickup in volatility during September, pullbacks to support should still be used to add to equity exposure as needed. Use the current rally to rebalance portfolios, take profits, and neutralize risks accordingly.

With that said, there are certainly risks to remain mindful of. The risk of a recession from tighter financial conditions is one of them.

The Week Ahead

This holiday-shortened week should be quiet, with few earnings reports and little economic data. We will closely monitor the ISM service sector survey on Wednesday and jobless claims on Thursday. We suspect Fed members will start prepping us for the coming meeting on September 20th. The odds of a rate hike at the meeting are currently only 7%.

The BLS Employment Report

Payrolls grew by 187k, slightly above expectations. However, the unemployment rate jumped from 3.5% to 3.8%. That is primarily a function of 525k people who entered the workforce, so it is not overly concerning. Further, August tends to see larger increases due to recently graduated students. Also of note, hourly earnings fell short of expectations at 0.2%. As we saw in the JOLTS report, with the declining quit and job opening rates, employees appear to be losing leverage with their employers.

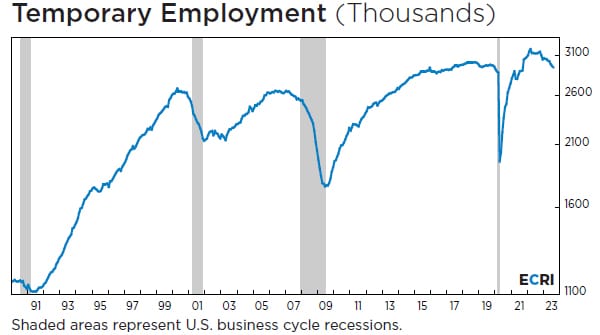

As shown in the second table below, payrolls have been revised lower by 355k jobs this year. June, for instance, was initially reported as +209k and has since been cut in half to +105k. The third graph shows temporary employment continues to decline. Businesses often reduce temporary staff before taking more drastic actions with full-time workers. Consequently, a decline in temporary workers precedes most recessions.

In summary, there are clear signs the labor markets are weakening. But, thus far, we would characterize the recent data as a normalization to pre-pandemic trends. If employment data continues to degrade, our concerns about a recession will rise.

More Auto Loan Delinquencies Are Coming

In Friday’s Commentary, we wrote about the uptick in delinquencies on consumer loans. The repayment of student loans may cause even more delinquencies. Per the Distill report in our lede, almost a third of student loans outstanding are held by those in their 30s. The graph below shows these borrowers have an estimated $3 billion of other consumer debt. Consumer debt can be defaulted on and extinguished. Student loan debt cannot. Therefore, when push comes to shove for struggling borrowers, not paying a consumer loan, as opposed to a student loan, might be the optimal choice.

According to TransUnion, more than a third of consumers with student loans took on new auto loans during the pandemic. To put the debt load on some borrowers in context, the Wall Street Journal writes: “With the average price of a new General Motors vehicle at $52,000 and new car loans with an interest rate of 9.5%, many consumers are struggling to keep up with their payments.” Not only will consumer delinquencies which are at ten-year highs, likely rise, but spending on autos and houses will decline by those now saddled with student loan payments.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.