Donald Trump’s frustration with Chairman Powell increases by the day. Consequently, per The Wall Street Journal, expectations are that Trump will announce Powell’s successor sooner than typical. Powell’s term expires May 2026. If Trump goes through with an early nomination, this “shadow Fed Chair” would espose views on the economy and monetary policy until Powell’s retirement. Consequently, this shadow Fed Chair’s opinions may differ from those of Powell and the majority of the FOMC. Given such an unprecedented action, let’s summarize the key points of the article to appreciate the ramifications.

- Market Reaction: Contradictions between Fed members and the shadow Fed chair regarding Fed policy and the economy could create confusion among investors and destabilize markets. Additionally, we wonder if the Fed maintains a more hawkish stance to counteract a dovish shadow Fed Chair.

- Congressional Support: Powell has strong support in Congress. Therefore, Republicans may persuade Trump to wait until Powell’s term expires before introducing his successor.

- Fed Independence: The Fed is independent from the Government. While the President appoints the Chairman, he has no authority over the Fed’s decisions. The shadow Fed Chairman may not have the same independence. Thus, they could become a puppet for the President.

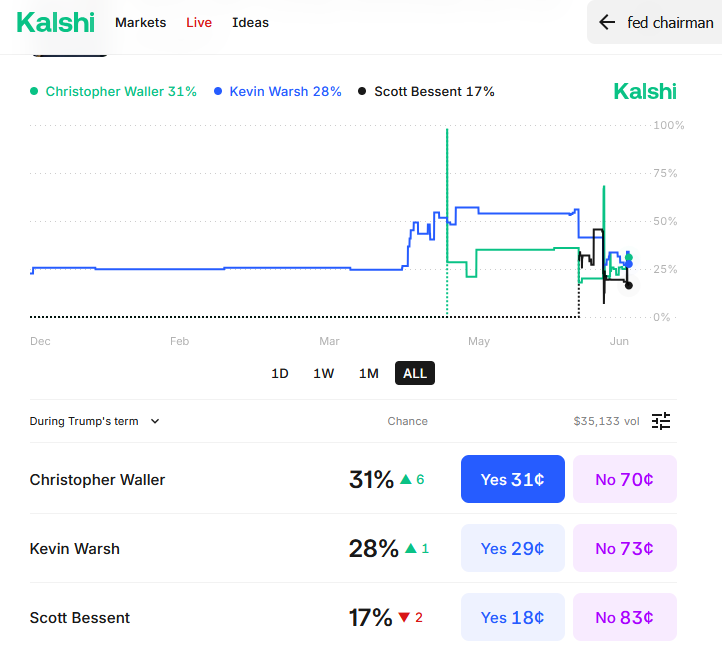

- Potential Candidates: The article lists Scott Bessent, Kevin Warsh, and Christopher Waller, as candidates. Bessent “has raved about the idea of one day becoming Fed Chair.” Warsh is a good candidate but tends to prefer a hawkish policy. Such would clash with Trump’s demands to lower rates. Lastly, Waller is a dove, but he is already a member of the Fed’s Board of Governors. The relationship between Powell and Waller, and with other Fed members, could become complicated if Waller is put in this position.

The Kalshi graphic below shows betting odds favor Waller slightly over Warsh.

What To Watch Today

Earnings

- No notable earnings releases.

Economy

Market Trading Update

The S&P 500 and the Nasdaq both set all-time highs this week. This feat seems remarkable given the barrage of negative headlines, geopolitical risks, and a Federal Reserve intent on not cutting rates. However, the bulls remain decisively in control of the market as it closed above the 6100 level amid a backdrop of weakening economic data, dovish undertones from the Federal Reserve, and continued strength in mega-cap tech. Despite some pockets of sector underperformance, key technical indicators suggest bullish momentum remains intact, but with caveats beneath the surface.

- Price Action: The index broke out from a brief consolidation zone between 6000 and 6050, closing the week at all-time highs with strong follow-through on increasing volume.

- Moving Averages:

- The index remains well above its 20-day, 50-day, and 200-day moving averages — a classic bullish configuration.

- The 20-day MA is acting as near-term dynamic support, currently around 6050.

- A “Golden Cross” is approaching with the 50-day set to cross above the 200-day moving average next week.

- RSI (Relative Strength Index): Hovering around 72, indicating short-term overbought conditions, but is consistent with strong market uptrends.

- MACD: Remains is on a bullish crossover, confirming upward momentum.

Flows And Positioning

- Fund Flows: EPFR and Bank of America data showed inflows into large-cap U.S. equity funds this week, particularly in technology and communications sectors.

- Hedge Fund Positioning: Net exposures remain elevated, particularly in concentrated names like Nvidia, Microsoft, and Apple, suggesting institutional conviction and heightened risk if leadership falters.

- Retail Participation: This week, retail flows picked up slightly, driven mainly by options activity, especially in mega-cap tech and AI-related names.

- Equal Weight S&P 500 (RSP): Lagged behind the cap-weighted index and remains under its February highs, reinforcing narrow breadth.

- Small Caps: The Russell 2000 underperformed, weighed down by rising energy prices and concerns about refinancing risk.

Risks To Monitor Next Week

- Breadth Divergences: New index highs not confirmed by the average stock could signal weakening internal strength.

- Overbought Conditions: Short-term technicals suggest a pullback is possible before the next leg higher.

- Earnings Season Ahead: Elevated expectations for mega-cap tech could result in volatility if results disappoint.

Looking Ahead to Next Week

Given the S&P 500’s breakout to new highs amid narrow leadership and overbought technicals, investors should approach next week with a balanced stance. Remain constructive on the broader trend while respecting the potential for short-term volatility.

July tends to be a better-performing month overall; therefore, portfolio positioning should emphasize quality large-cap growth, particularly in sectors demonstrating strong momentum. However, monitor breadth as a cue to trim excess risk as needed. Tactically, this is a prudent time to review stop-loss levels, maintain appropriate diversification, and watch for signs of broadening participation to validate further upside.

The Week Ahead & PCE Data

Core PCE prices rose 0.2% versus expectations of 0.1%, while total PCE prices rose 0.1%. Both are in line with recent CPI and PPI data. However, the personal income and spending data was weaker than expected as highlighted below. Personal income fell for the first time in almost four years. While concerning, the decline was due to decline in Social Security payments which were boosted earlier this year by large retroactive payments. The data affirms other economic indicators pointing to slower growth.

ISM manufacturing and service sector surveys will be released on Monday and Wednesday. Again, traders will focus on the employment and prices subcomponents for clues about how tariffs are impacting the economy and inflation. Also this week will be the JOLTs, ADP and BLS labor data. Due to the July 4th holiday, the BLS report will come out on Thursday. The market expects an increase of 100k jobs.

The Fed’s “Transitory” Mistake Is Affecting Its Outlook

In 2023 and 2024, the Fed was under intense public and media scrutiny for calling the post-pandemic surge in inflation “transitory.” Critics argued that the Fed’s failure to anticipate the persistence and severity of rising prices undermined its credibility. Yet, with the benefit of hindsight and historical context, the Fed’s position wasn’t entirely misguided. Inflation proved temporary in a broader economic sense, and by 2025, the data confirmed a significant cooling of price pressures.

However, the Fed’s mistake wasn’t the “transitory” label—it was the Fed’s late response to raising interest rates and halting quantitative easing. As shown, the combined impact of the massive surge in the Government’s deficit spending (stimulus checks and infrastructure bills) and the Fed’s $120 billion monthly “quantitative easing” campaign caused a massive jump in economic growth and inflation. However, instead of cutting back on stimulus when the economy rebounded, the Fed’s mistake was keeping its “foot on the gas” for too long. These delays allowed the inflationary fire to burn hotter and longer than necessary, exacerbated by an overlooked driver: excessive government spending.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.