Inside This Week’s Bull Bear Report

- Market Takes A Breather

- Reverse Repo Shows Banks Reluctant Lend

- How We Are Trading It

- Research Report – Banking Crisis Is How It Starts.

- Youtube – Before The Bell

- Stock Of The Week

- Daily Commentary Bits

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

Market Takes A Breather

While today’s missive will explore why “reverse repo” is continuing to cause banking stress, the markets took a bit of a breather this week, as we suggested would be the case.

“After last week’s bullish push higher, every major sector and market is now highly overbought short-term. Look for a bit of correction next week, which will provide an opportunity to increase exposure for the next couple of weeks. April tends to be one of the more robust performance months of the year, and while markets are short-term overbought, they remain on solid bullish buy signals for now.”

This past week, the market did correct a bit but did not resolve the short-term overbought conditions, which can remain overbought during a rally. The good news is that the upside breakout of the downtrend line from the April highs was tested and held. This is the first attempt at turning that previous resistance line into support. I would not be surprised to see more weakness next week, particularly given Friday’s employment report, which showed a slowing in the pace of hiring and suggests economic weakness is becoming more widespread.

As we have discussed over the last several weeks, the market continues to defy the recession calls despite weakening economic data. However, the actual test for the market will start next week as the first quarter earnings season gets underway. Estimates were lowered substantially going into Q1, so expect a high “beat rate” for companies. While the beating estimates will get headlines, it will be the “forward guidance” driving their prices. CEO confidence remains very low. Therefore, weak guidance could knock some of the exuberance out of the markets.

Notably, the first companies to announce earnings will be the major banks. All eyes will be focused on their reports to determine if the banking crisis is behind us. This week will delve into the “reverse repo” program, its massive surge in usage, and what that means for the banks and the markets.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

Reverse Repo Shows Banks Reluctant Lend

While the market has been trading more bullishly over the last few weeks, that rally is based on two primary “hopes.” The first is that the Fed is set to pivot from monetary tightening, and the second, the recent “bank crisis” is contained.

Federal Reserve Bank of Cleveland President Loretta Mester said on Tuesday that the U.S. central bank likely has more interest rate rises ahead amid signs the recent banking sector troubles have been contained.” – CNBC

Interestingly, that statement markedly resembles then-Fed Chairman Ben Bernanke’s infamous declaration before Congress in 2007:

“We do not expect significant spillovers from the subprime market to the rest of the economy or to the financial system.”

It is likely early to be confident the banking crisis is contained. One sign of potential risks in the banking sector is the continued surge in “reverse repo” operations. The chart below shows the complete history of the Reverse Repurchase Program (Reverse Repo) since 2003. The surge in the use of the facility is quite unprecedented relative to previous periods.

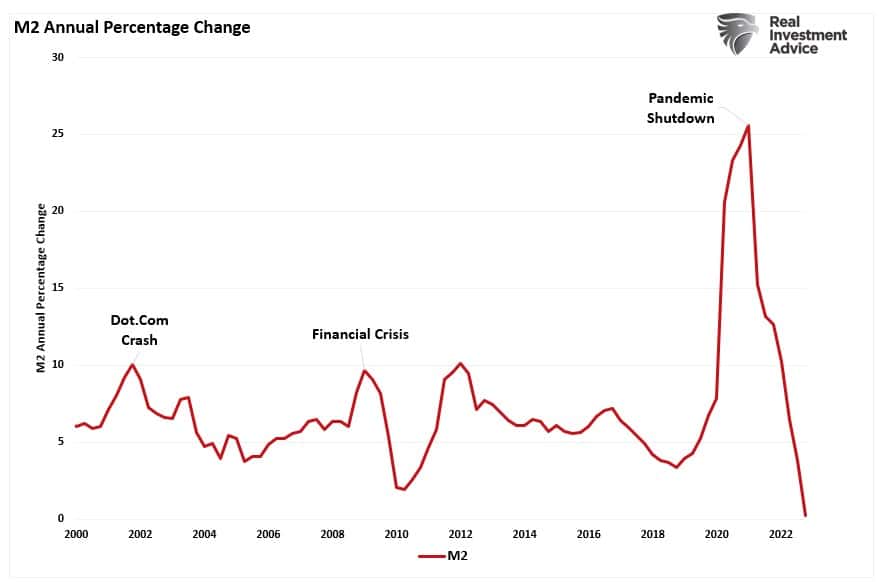

While the surge in the “reverse repo” program is quite startling, the question is whether it signifies any significant risk in the financial sector or is it just another anomaly caused by the massive monetary and fiscal interventions during the pandemic-driven shutdown. That is a substantial difference between the “financial crisis” in 2008 and the pandemic-driven shutdown in 2020. While both events had the Federal Reserve acting to support the financial markets through Quantitative Easing and a “zero-interest-rate” policy, the fiscal policies in 2020 flooded households with cash.

As shown below, the surge in M2 during 2020 wound up in excess savings in banks. But with the rate-of-change of M2 falling at the fastest rate in history, are those stores of cash in “reverse repo” problematic?

To answer that question, we need a basic understanding of what the “reverse repo” program is and what it does.

What Is Reverse Repo?

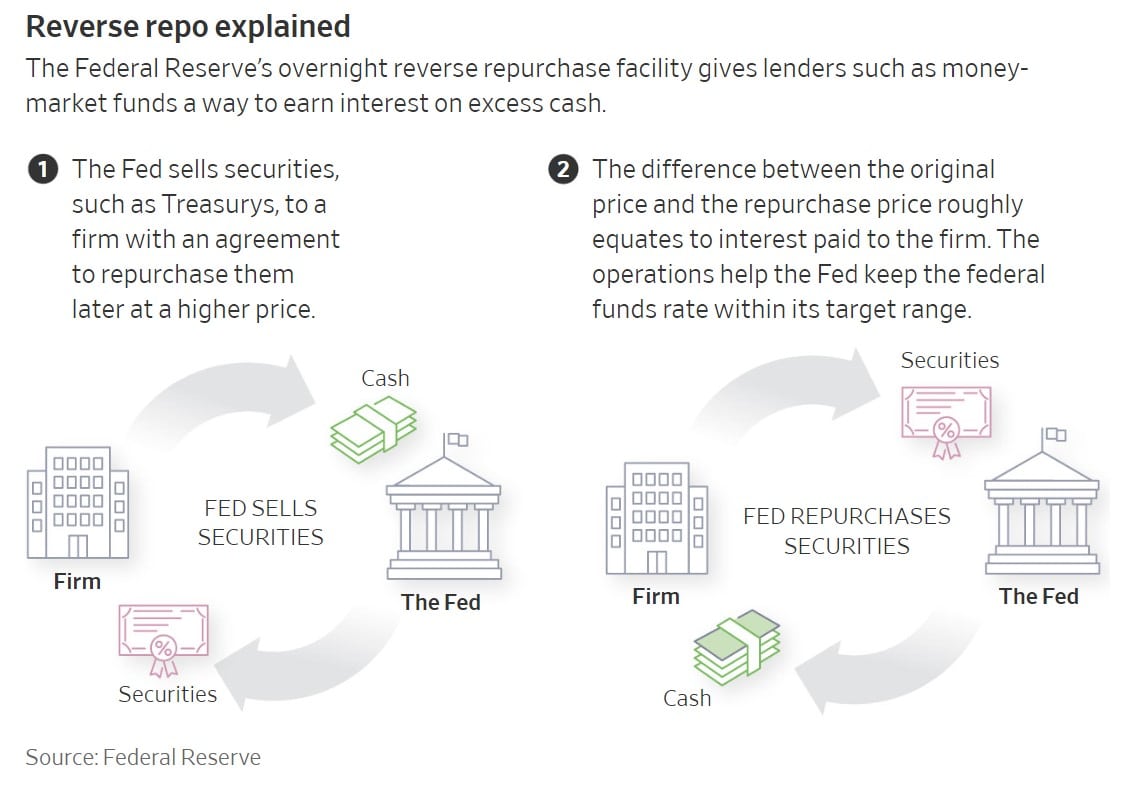

On Tuesday, the Wall Street Journal published an excellent chart explaining the Reverse Repurchase Program. Simply, “reverse repo” is a program whereby the Federal Reserve sells securities to a firm with an agreement to repurchase them at a higher price the next day. The difference between the original and “repurchase” prices, hence the term “reverse repurchase program,” equates to the interest paid to the buyer.

As Michael Lebowitz notes:

“A reverse repurchase occurs when a bank, money market fund, or Fannie Mae and Freddie Mac, lend money to the Fed overnight in exchange for Treasury collateral. The investment is the only risk-free option for said entities. Other overnight investment options like Fed Funds and Repo have counterparty risks.

The Fed initiated the RRP program to help absorb the tremendous number of reserves pumped into the financial system via the massive monetary stimulus campaign following the Covid pandemic economic shutdown.”

That last sentence is the most important. As discussed, banks operate on a “fractional reserve lending” basis. Therefore, when individuals deposit money at the bank, those funds are turned into loans or used to buy securities. As long as there isn’t a “run on the bank” where large numbers of depositors demand their funds simultaneously, banks can either redeem cash demands from cash flows or sell some of their assets. The potential problem arises when withdrawal demands exceed available cash or collateral values. Or, as we learned with SVB when banks have to sell investments at a loss to meet their redemptions.

Importantly, banks have been unwilling to hold extra reserves or readily available cash due to regulators’ decisions following the financial crisis. To maintain the appearance of being well collateralized, banks counted those reserve balances toward the banks’ calculation of a critical regulatory buffer known as the supplementary leverage ratio. That was all fine until the Fed hiked interest rates which lowered the fair market value of those reserves. When collateral is required to be held to maturity, the liquidity to meet withdrawal demands becomes more limited.

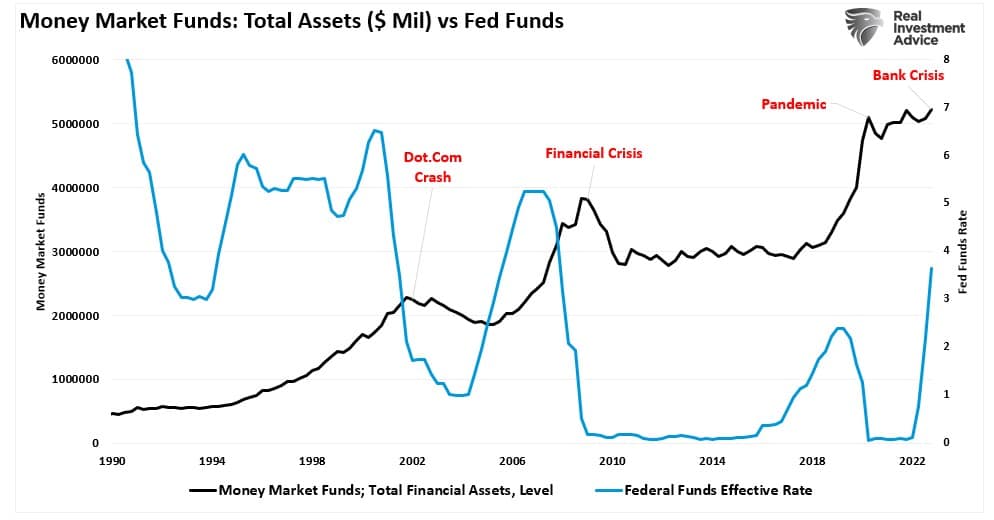

This problem is compounded as banks have come under pressure from depositors’ embrace of money-market funds. With banks paying well below the current short-term fund’s rate, capital is leaving banks, as shown by money market fund balances. This pushed the “reverse repo” program into the spotlight.

Small Banks Are Losing To The Big

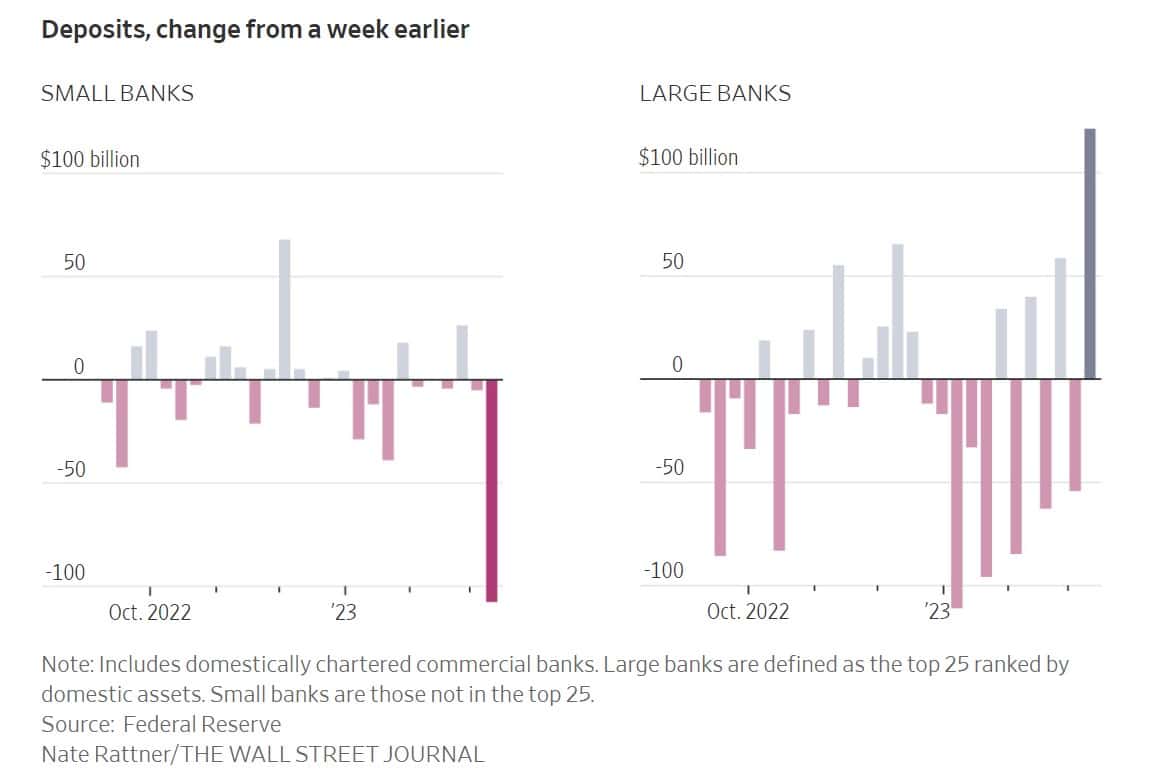

Small to mid-size banks face the most systemic risk from the flow of capital into mutual funds. According to Federal Reserve data, the 25 biggest U.S. banks gained $120 billion in deposits in the days after SVB collapsed. All the U.S. banks below that level lost $108 billion over the same period. It was the most significant weekly decline in smaller banks’ deposits in dollar terms on record.

The mega-banks enjoy the benefits of offering investment banking services, trading operations, and money market funds to their customers. However, small to mid-size banks depend almost entirely on traditional banking services and loan generation. Many loans are for residential mortgages, automobiles, and commercial real estate, all of which have come under pressure from higher interest rates.

That flow of deposits from small banks to big banks and mutual fund companies is problematic. Banks need deposits to make loans; if deposits fall, lending will follow. Furthermore, if banks want to keep current customers, they must pay their depositors higher interest rates, which crimps earnings and further erodes lending capacities.

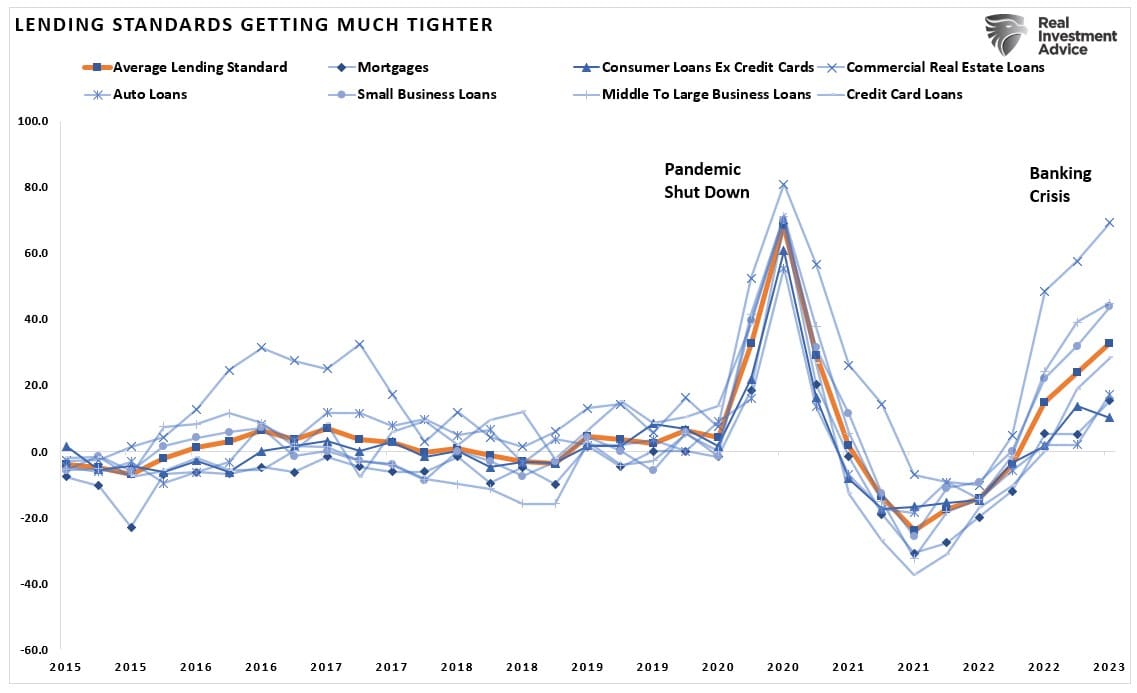

Such is why lending standards are tightening rapidly at small and mid-size banks. Given that credit is the lifeblood of economic activity, it is not surprising tighter lending standards precede recessionary outcomes.

A Tough Spot

The triple whammy on smaller banks is the flight of deposits to money markets for higher yields, higher interest rates reducing collateral values, and slowing economic growth. Furthermore, as noted by William Dudley, former N.Y. Fed Reserve Bank president:

“What’s different this time is the money-market funds aren’t really as good at recycling money back into the banking system.”

The Fed could ease the stress on the banks by changing the terms of the “reverse repo” facility. One way would be to cut the rate paid to money funds. As the WSJ noted:

“In June 2021, the Fed raised the overnight reverse repo rate by 0.05 percentage point. With interest rates near zero, money-market funds were struggling to cover their operating costs, putting a vital part of the financial system at risk. The rate also serves as a floor on short-term interest rates.

With rates well above zero, the Fed has the option to push the overnight reverse repo rate back down to the lower end of the federal-funds target range. That would need to coincide with the Fed’s raising the rate it pays on bank reserves, a move that could encourage money funds to lend to banks rather than the Fed. Interest on reserves is currently 4.9%.”

However, while such a move may reduce the demand for the “reverse repo” facility, demand for bank loans is falling with slower economic growth. Greater competition among banks would raise borrowing costs, hurting profits and further slowing economic activity. The trick will be to reduce the dependency on “reverse repo” and increase more normal financial system functioning. However, that process may not be a smooth one. As Michael Lebowitz concluded:

“The program allows the Fed to remove the funds from the system, thus keeping them from entering the market where they would push the Fed Funds rate below the Fed’s target.

The amount of RRP should be slowly declining as the Fed removes reserves via QT. However, less issuance from the Treasury due to the debt cap and attractive risk-free rates versus alternatives make the program a good alternative for cash. The program is just another tool for the Fed to control the Fed Funds rate. We are not worried by the program per se, but it does speak to the Fed’s overreach in markets.”

While the Federal Reserve is hopeful that the current drain of assets on smaller banks is inconsequential and a “contained” risk, the same was thought about subprime mortgages in 2008. This time is certainly different, but while officials are reassuring the public that the financial sector is stable, the hope that the demand for the “reverse repo” system will return to normal without consequence seems optimistic.

I don’t know the answer, but the risk of “something breaking” in the system remains elevated primarily due to the Fed’s aggressive tightening campaign.

Will it be another banking crisis? Or, just the consequence of an economic recession?

Either way, the return to normalcy does not seem like it will be a smooth journey.

Hopefully, I am wrong.

How We Are Trading It

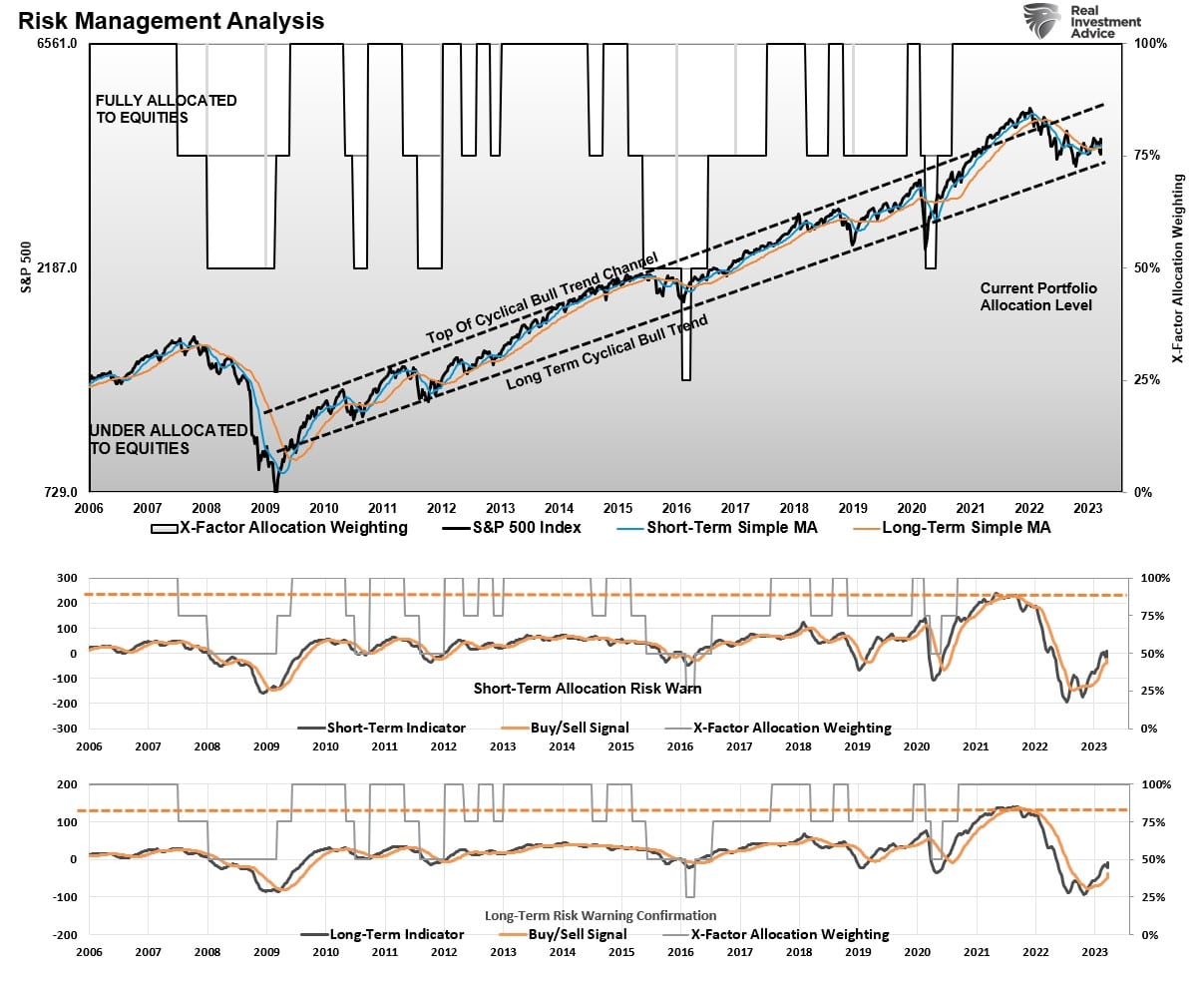

This past week, the market sold off as expected. The overbought Technology sector led the way lower as funds rotated into the more beaten-up and defensive Utilities and Healthcare. However, the market remains bullish despite the near-term correction, with the daily and weekly buy signals intact. Such suggests maintaining exposure, although reduced, to equity risk for now. Our weekly risk-management chart, shown below, confirms that analysis.

Over the last couple of weeks, we have posted our portfolio management guidelines. This pullback is likely a good opportunity to increase exposure short-term, provided our buy signals remain intact. If those signals fail, we will reduce exposure and await the next opportunity.

All we can do is monitor our portfolios, focus on our technical indicators, and monitor short-term risks adjusting allocations accordingly. While we did increase our equity exposure over the last two weeks, we remain decently underexposed to equities. Also, we did increase our bond allocations this past week as the technical breakout provided a more bullish setup suggesting lower interest rates ahead. While the amount of equity exposure we maintain remains uncomfortable, given recessionary risks have increased, we adhere to our discipline accordingly to help offset our base emotional reactions.

While this market rally could have some legs, we want to continue to maintain some control over our portfolio risks. As such, continue working to rebalance portfolios for now.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against significant market declines.

- Take profits in positions that have been big winners.

- Sell laggards and losers.

- Raise cash and rebalance portfolios to target weightings.

On a pullback to support that holds, we will bring our allocations up somewhat and raise stops accordingly. However, we will raise cash levels quickly if the market environment becomes more hostile.

Have a great Easter holiday.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates (Formerly 3-Minutes)

We have set up a separate channel JUST for our short daily market updates. Be sure and subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our Youtube Channel To Get Notified Of All Our Videos

Stock Of The Week In Review

If we piqued your interest in Shorting Zombie Stocks last week, we follow with a screen that seeks stocks that may do well if a recession occurs and a zombie apocalypse weighs on markets.

Last week’s scan focused on stocks with meager interest coverage ratios and flat to negative earnings and sales growth. The result was stocks that may find it challenging to roll over maturing debt if bank lending standards tighten, as we suspect they will.

This week’s report seeks zombie slayers. These are stocks that can weather a recession and tighter lending conditions well. In this scan, we use similar criteria but seek stocks at the opposite end of the spectrum regarding said criteria. For example, we searched for relatively high-interest coverage ratios, solid and consistent sales and earnings growth, and plenty of free cash flow.

Here is a link to the full SimpleVisor Article For Step-By-Step Screening Instructions.

Login to Simplevisor.com to read the full 5-For-Friday report.

Daily Commentary Tidbits

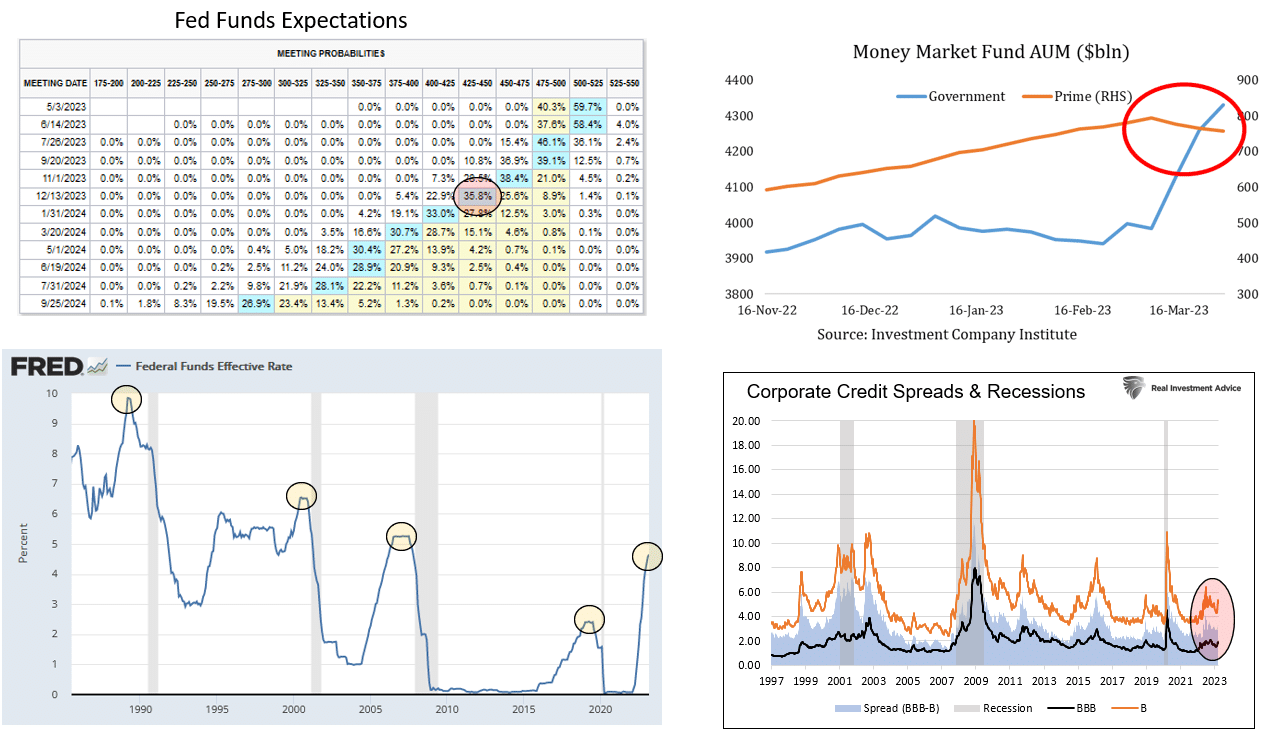

Bond Markets Send Confusing Messages

Our most recent newsletter (Analysts Warn of Recession. Analysts Disagree) discusses confusing signals emanating from the stock and bond markets. To wit: “Currently, 100% of the 10-yield spreads we track are inverted. Historically, a recession follows whenever more than 50% of those spreads are inverted. Every. Single. Time.“ Yet despite a 100% reliable recession warning- “With the market, as shown in the callout, retesting and holding above the 40-week moving average, such confirms both the long-term and short-term bullish trends are intact.“

Unfortunately, the signals from within the bond markets are equally confusing. Fed Funds futures (top left graph) expect the Fed to cut rates by .75 to 1.00% by year-end. The graph on the bottom left shows that Fed Funds peaked and declined, as the market currently projects, before the start of the last four recessions. Despite recession concerns, corporate bond spreads (bottom right), which tend to widen before and during recessions, send no such signal. Lastly, the most risk-averse investors are shifting from prime money market funds to government money market funds. Prime funds, holding short-term corporate bonds, have negligible risk, yet the flight to safety is pronounced, as we show (top right). Investment and mental flexibility will be important this year as diverging signals sort themselves out.”

(Subscribe To The Daily Market Commentary For A FREE Pre-Market Email)

Bull Bear Report Market Statistics & Screens

SimpleVisor Top & Bottom Performers By Sector

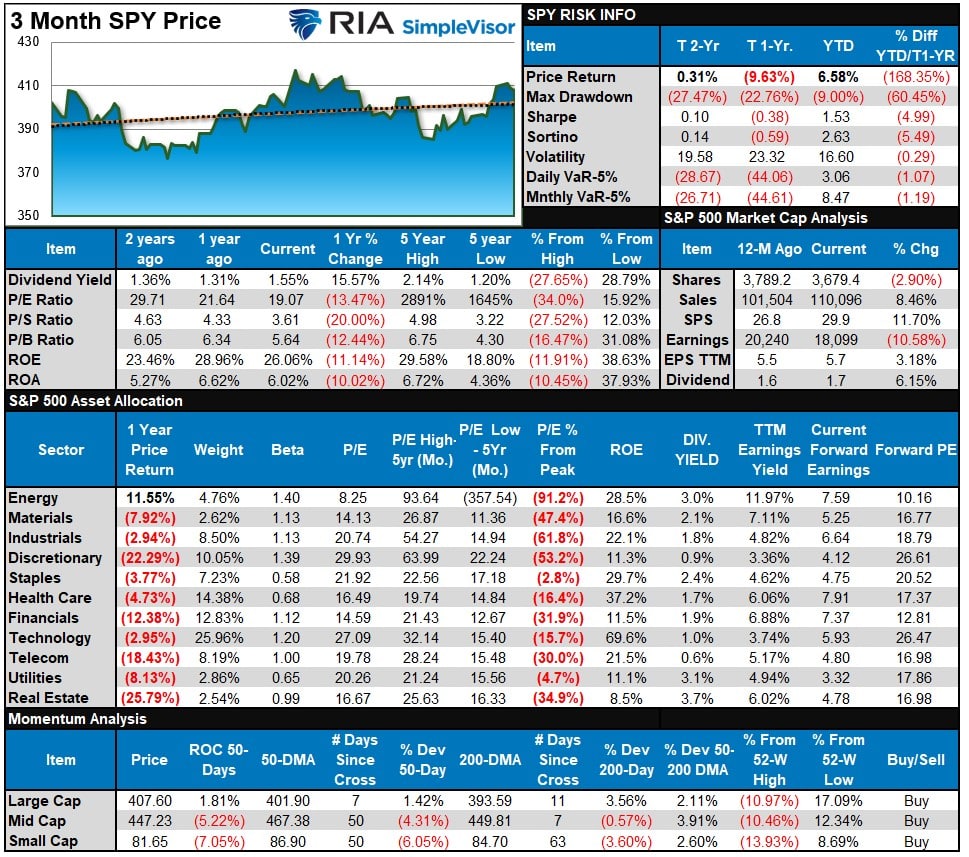

S&P 500 Weekly Tear Sheet

Relative Performance Analysis

As noted last week:

“Every major sector and market is now highly overbought short-term. Look for a bit of correction next week, which will provide an opportunity to increase exposure for the next couple of weeks.”

While the market pulled back some last week, it has not resolved much of the short-term overbought condition. We could see some additional selling pressure next week as a result. However, Technology and Communications are extremely overdone in their rally on a year-to-date basis, and heading into earnings season, I would caution against chasing these stocks in the short term. Profit-taking is likely advisable.

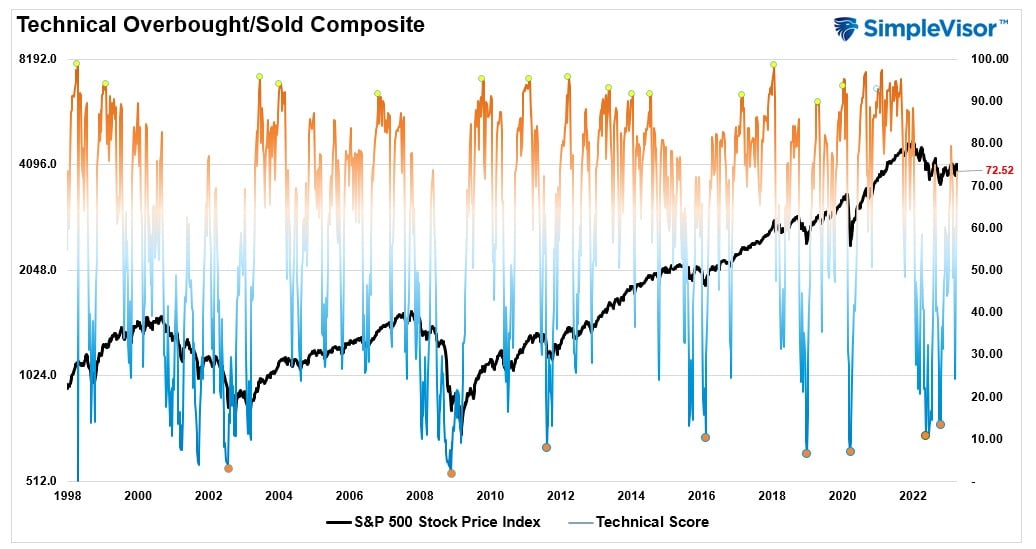

Technical Composite

The technical overbought/sold gauge comprises several price indicators (RSI, Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. Markets peak when those readings are 80 or above, suggesting prudent profit-taking and risk management. The best buying opportunities exist when those readings are 20 or below.

The current reading is 72.52 out of a possible 100.

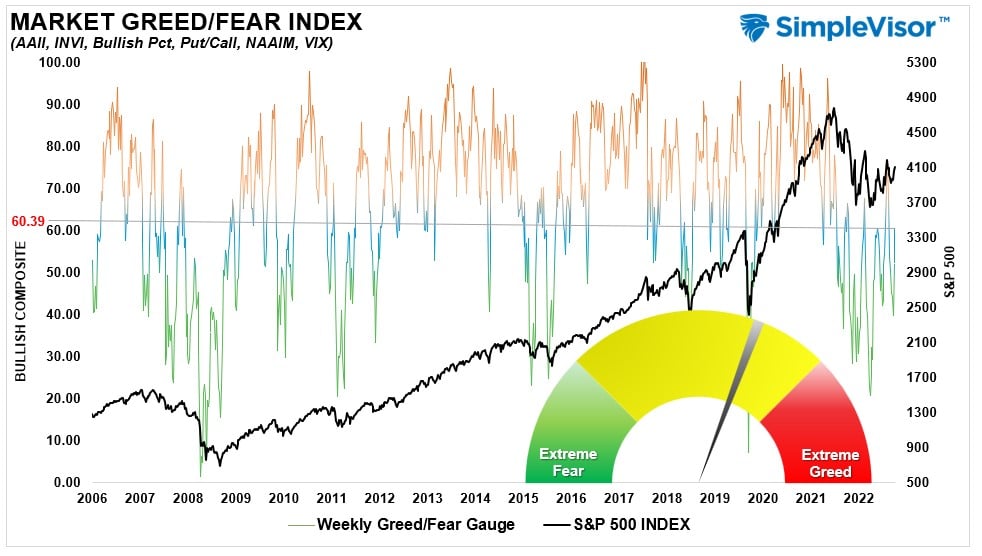

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” Gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 60.39 out of a possible 100.

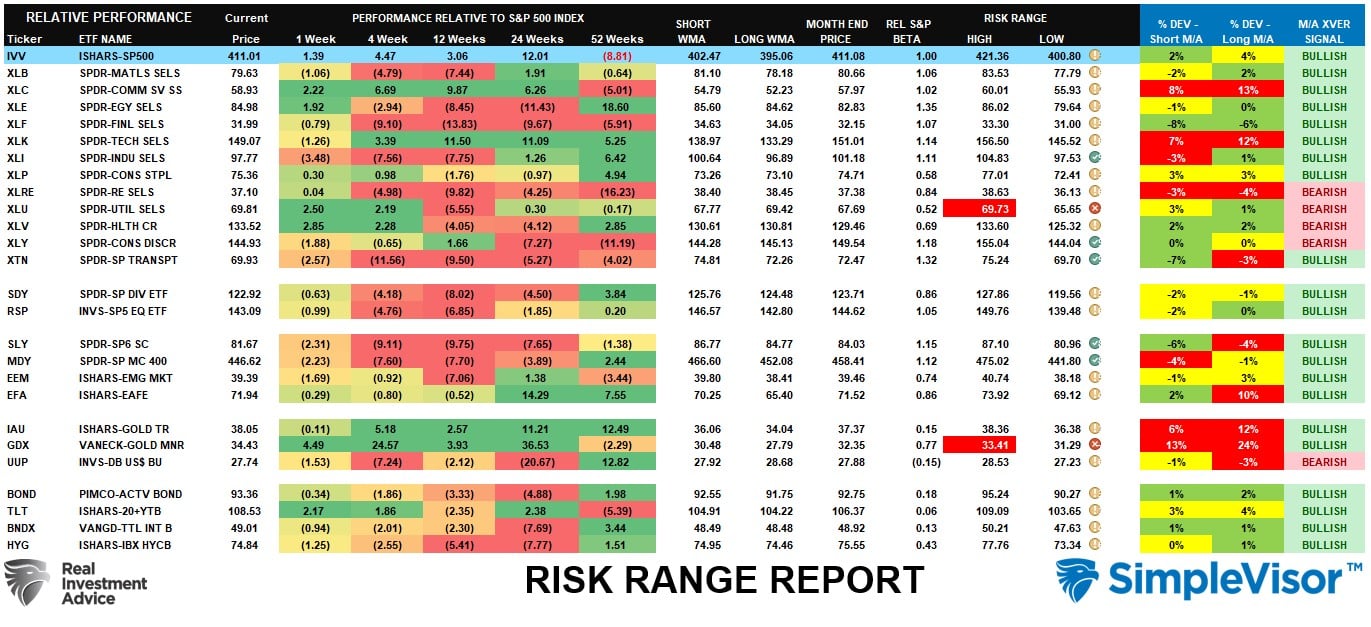

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “M” XVER” “Moving Average Cross Over) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

The rally in “defensive” areas last week, Utilities and Gold Miners, was not surprising as the rotation from Technology and Communications started. As noted last week, with most markets and sectors on bullish moving average crossovers, the most likely path for asset prices is higher over the near term. Maintain equity exposures, but watch for further rotations from grossly overbought areas into oversold.

Weekly SimpleVisor Stock Screens

We provide three stock screens each week from SimpleVisor.

This week we are searching for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Fundamental And Technically Strong Stocks

(Click Images To Enlarge)

RSI Screen

Momentum Screen

Fundamental Stocks With Strong Technicals

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

April 5th

This morning we added 2% of the portfolio value to our current iShares 20-Year Treasury bond ETF (TLT) holdings to all models. After turning on a sell signal a few days ago, it flipped and is back on a buy signal, albeit from higher than preferred levels. More importantly, bonds are breaking above a resistance level that has capped the market thrice since December. Weaker JOLTS, ADP and ISM, appear to be the main factor for the recent uptick in bonds.

We are not yet at full target weights for our bond holdings, so while we are lowering our current cost basis, we hope to get one more pullback in bonds to bring our duration to target and increase our bond holdings to full allocations.

Both Equity And ETF Models

- Add 2% to the iShares 20-Year Treasury Bond ETF (TLT)

Lance Roberts, CIO

Have a great week!