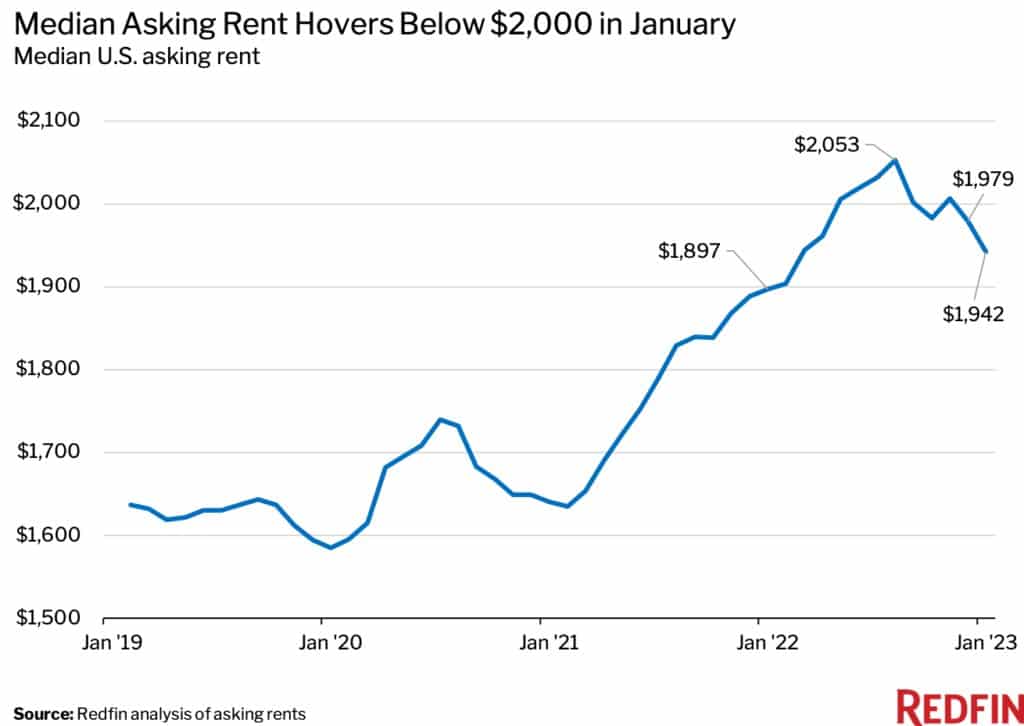

Per a recent Yahoo article: “The average American renter is now paying more than 30 percent of their income on housing, as wages have failed to keep up with rent hikes and affordable units remain scarce, a new report shows.” The government defines those with a rent burden as paying more than 30% of their income on rent. The article further estimates over 40% of low and middle-income citizens are rent burdened. Higher interest rates and low supply are to blame Per Yahoo, “High mortgage rates compound the problem, as those who want to transition to homeownership are locked out of that market, said Nicole Bachaud, a senior economist at Zillow.” From a macroeconomic stance, consider that those with more money allocated to rent have less to contribute to the economy. Like higher interest rates, higher rents also burden the economy.

Fortunately, rental prices have started declining, hopefully easing the growing rent burden in the coming months. We wrote in a recent Commentary that OER will continue to decline. To wit: “the OER price index is over 10% above its 35-year trend line. Therefore we believe the recent increase is an anomaly that will correct as the supply-demand equation normalizes quickly this year.” OER refers to owners’ equivalent rent, the BLS’s rent-based measure to calculate CPI.

What To Watch Today

Economy

- Factory Orders, January

Earnings

Market Trading Update

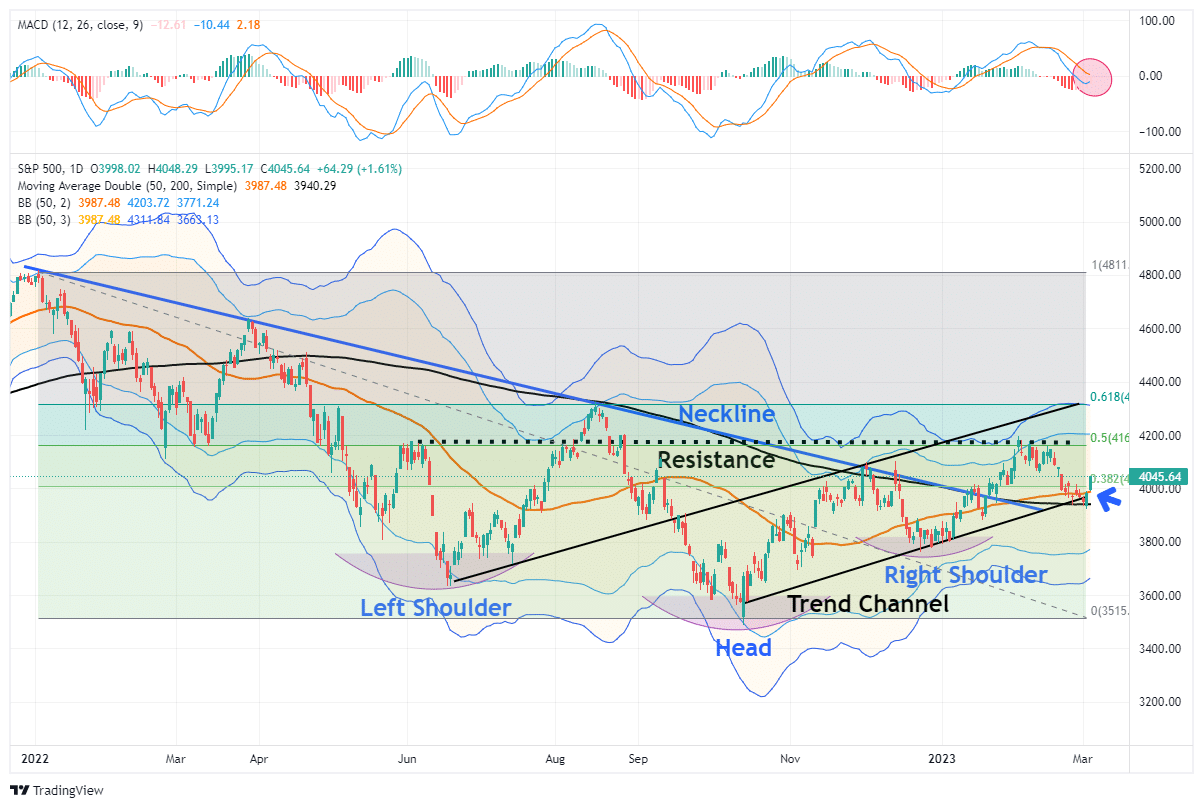

Last week, we stated that the worse-than-expected data on inflation and hawkish Fed minutes sent markets reeling and took out support at the 50-DMA.

“Critical support at the rising trend line from the October lows and the 200-DMA is now getting tested. A failure of those levels next week will put the bears back in charge of the market near term.”

Fortunately, the bulls stepped in on Thursday and Friday to rally the markets off that 200-DMA support, keeping the rising trend intact. However, the rally is now challenging existing resistance at the 20-DMA, but the previous highs around 4200 are the most logical target currently. Importantly the MACD “sell signal,” which warned of the recent correction, is beginning to reverse. However, that reversal occurs midway through normal oscillation, suggesting that the upside is somewhat limited.

While the MACD signal starts to turn, it can fail when our MoneyFlow indicator does not confirm the turn. Such is the case currently, but next week’s action will provide a more definitive outlook. The MoneyFlow indicator is near its cycle lows, similar to what we saw when the MACD turned positive at the December lows.

As such, we recommend selling any rally next week approaching the 4200, which is now important resistance.

Notably, the market remains confined to a rising trend channel, so we must respect that price action until it changes. That channel suggests the markets could rally as high as 4350 over the coming months, which remains in line with the seasonally strong period. However, if that channel is broken, there is roughly an equal amount of downside. In other words, the reward versus the risk from current levels is not great.

The Week Ahead

Labor headlines dominate this week’s economic reports. ADP and JOLTs on Wednesday, Jobless Claims Thursday, and the BLS labor report on Friday will better inform the Fed on the current state of the labor market. Payrolls are expected to grow by 210k, and the unemployment rate is expected to remain stable at 3.4%, a fifty-year low. Outside of the labor market, this is little other economic data. Investors will likely shift focus to the CPI report due next Tuesday.

Fed members will likely remain vocal this week as they head into their media blackout period starting next week as they approach the March 22 FOMC meeting.

The Mortgage Dilemma

The following graph shows that about 75% of mortgages have an interest rate of 4% or below. As a result, many of these homeowners seeking a new job, or those wishing to upsize or downsize will find higher mortgage rates a considerable impediment. We present the following example to show how high mortgage rates limit supply and demand in the housing market and keep the labor market tighter than it should be.

Assume a homeowner has a 3.50% mortgage on a $500,000 house. Their monthly payment is $2,245, excluding taxes and insurance. To incur the same monthly mortgage payment at current mortgage rates, the homeowner can only afford a house worth $335,000. Even if they put $100,000 down, making it a $400,000 mortgage, the monthly payment would still increase by roughly $400. The demand for housing will weaken as a result. Further, the labor market will remain tight as employees may be unable to move for a new job.

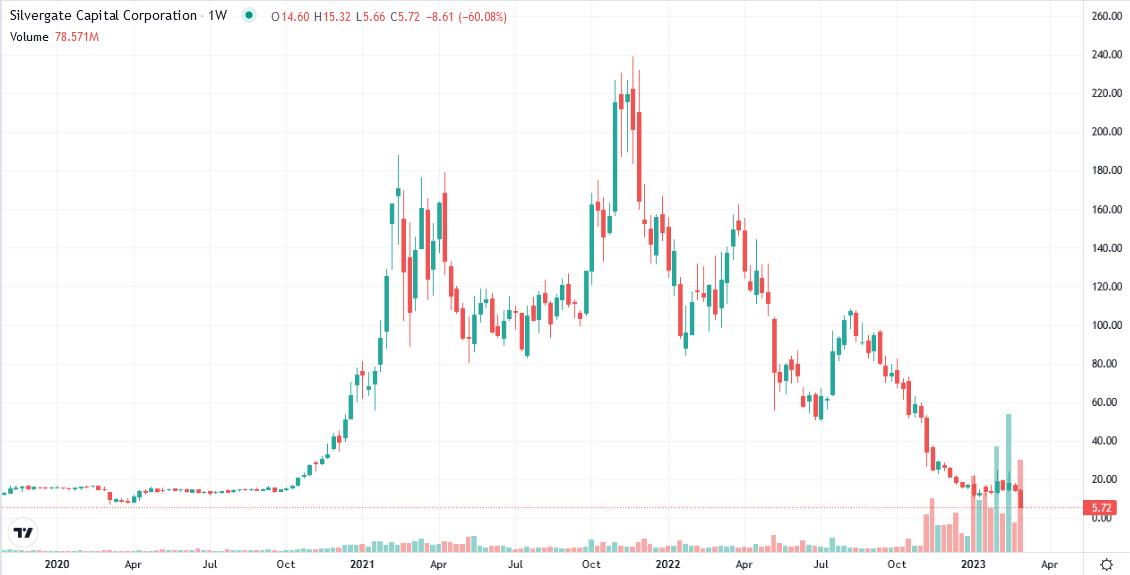

Silvergate Bank is on the Ropes

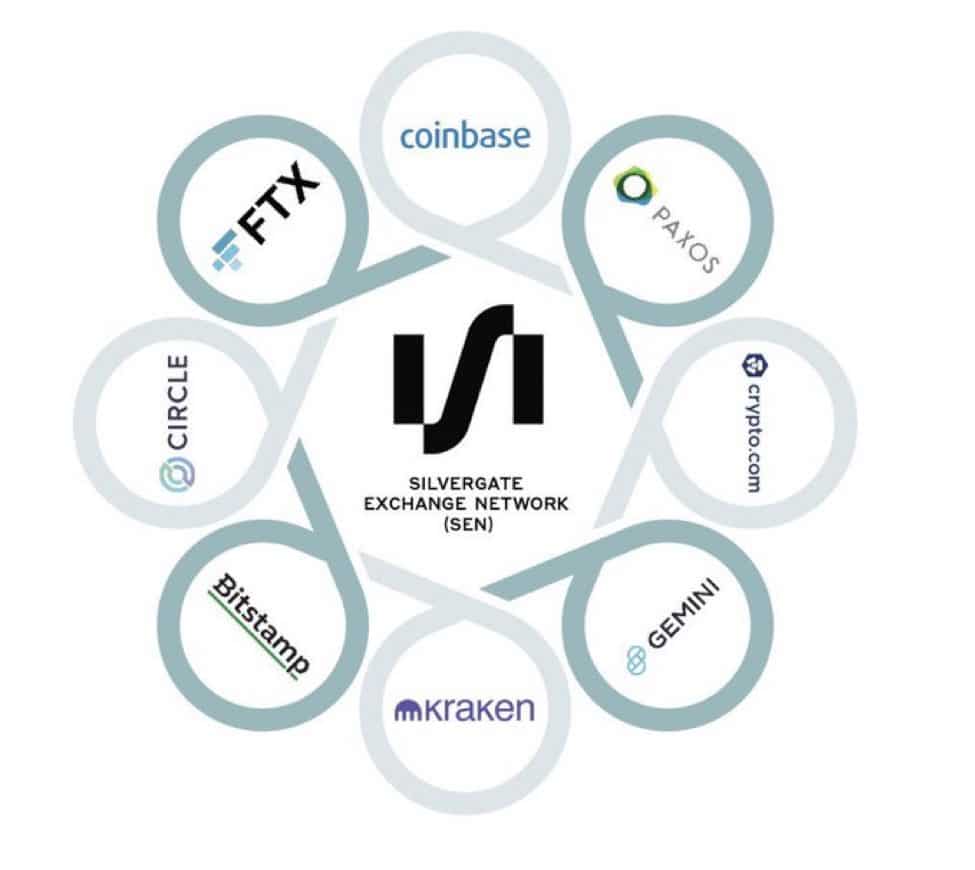

Silvergate Capital Corp, deemed banker to the crypto world (SI), fell 60% on Thursday to just under $6 a share. Silvergate’s fall from grace has been stunning in just over a year. Consider SI traded near $240 to close out 2021. Silvergate is a crypto-friendly bank with ties to FTX and other crypto firms either embroiled in fraud or near bankruptcy, as we share in the second graphic.

Driving Thursday’s sharp decline, the company could not file its SEC 10-K annual report for 2022 on time, nor will it meet the extended deadline in mid-March. Further, the bank said it was not sure it would survive as a “going concern.” Per its Notification of Late Filing:

These additional losses will negatively impact the regulatory capital ratios of the Company and the Company’s wholly owned subsidiary, Silvergate Bank (the “Bank”), and could result in the Company and the Bank being less than well-capitalized. In addition, the Company is evaluating the impact that these subsequent events have on its ability to continue as a going concern for the twelve months following the issuance of its financial statements.

The rumor is that the FDIC will seize SI’s assets and let Wells Fargo take over the customer accounts. The FDIC will bear any losses if the company fails. Silvergate is not large enough to dent the FDIC’s war chest, but its failure will likely bring significant political pressure to regulate the industry.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.