David Rosenberg explores Recession Arithmetic in today’s Breakfast With Dave. I add a few charts of my own to discuss.

Rosenberg notes “Private fixed investment has declined two quarters in a row as of 2019 Q3. Since 1980, this has only happened twice outside of a recession.”

Here is the chart he presented.

Fixed Investment, Imports, Government Share of GDP

Since 1980 there have been five recessions in the U.S.and only once, after the dotcom bust in 2001, was there a recession that didn’t feature an outright decline in consumption expenditures in at least one quarter. Importantly, even historical comparisons are complicated. The economy has changed over the last 40 years. As an example, in Q4 of 1979, fixed investment was 20% of GDP, while in 2019 it makes up 17%. Meanwhile, imports have expanded from 10% of GDP to 15% and the consumer’s role has risen from 61% to 68% of the economy. All that to say, as the structure of the economy has evolved so too has its susceptibility to risks. The implication is that historical shocks would have different effects today than they did 40 years ago.

So, what similarities exist across time? Well, every recession features a decline in fixed investment (on average -9.8% from the pre-recession period), and an accompanying decline in imports (coincidentally also about -9.5% from the pre-recession period). Given the persistent trade deficit, it’s not surprising that declines in domestic activity would result in a drawdown in imports (i.e. a boost to GDP).

So, what does all of this mean for where we are in the cycle? Private fixed investment has declined two quarters in a row as of 2019 Q3. Since 1980, this has only happened two other times outside of a recession. The first was in the year following the burst of the dotcom bubble, as systemic overinvestment unwound itself over the course of eight quarters. The second was in 2006, as the housing market imploded… and we all know how that story ended.Small sample bias notwithstanding, we can comfortably say that this is not something that should be dismissed offhand.

For now, the consumer has stood tall. Real consumption expenditures contributed 3.0% to GDP in Q2, and 2.1% in Q3. Whether the consumer can keep the economy from tipping into recession remains to be seen.

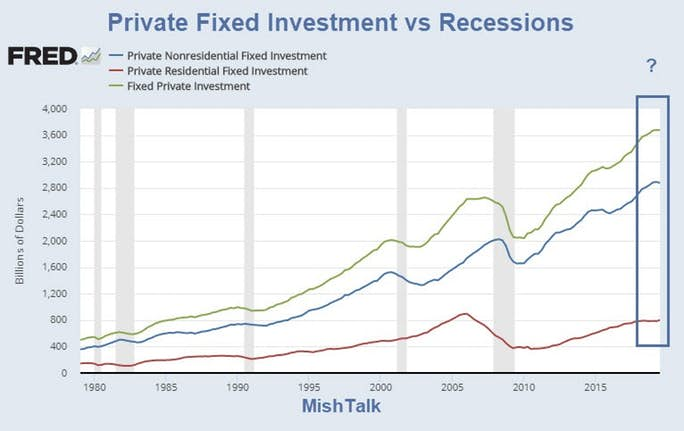

Dave’s comments got me thinking about the makeup of fixed investment. It does not take much of a slowdown to cause a recession. But there are two components and they do not always move together.

Fixed Investment Year-Over-Year

One thing easily stands out. Housing marked the bottom in 12 of 13 recessions. 2001 was the exception.

Fixed Investment Year-Over-Year Detail

Fixed Investment Tipping Point

We are very close to a tipping point in which residential and nonresidential fixed investment are near the zero line. The above chart shows recessions can happen with fixed investment still positive year-over-year.

Manufacturing Has Peaked This Economic Cycle

The above charts are ominous given the view Manufacturing Has Peaked This Economic Cycle

Key Manufacturing Details

- For the first time in history, manufacturing production is unlikely to take out the previous pre-recession peak.

- Unlike the the 2015-2016 energy-based decline, the current manufacturing decline is broad-based and real.

- Manufacturing production is 2.25% below the peak set in december 2007 with the latest Manufacturing ISM Down 5th Month to Lowest Since June 2009.

Other than the 2015-2016 energy-based decline, every decline in industrial production has led or accompanied a recession.

Manufacturing Jobs

After a manufacturing surge in November due to the end of the GM strike, Manufacturing Sector Jobs Shrank by 12,000 in December.

PPI Confirmation

Despite surging crude prices, the December Producer Price Inflation was Weak and Below Expectations

Shipping Confirmation

Finally, please note that the Cass Year-Over-Year Freight Index Sinks to a 12-Year Low

Manufacturing employment, shipping, industrial production, and the PPI are all screaming the same word.

In case you missed the word, here it is: Recession.