Every January, it happens like clockwork: you drive by gym parking lots that look like a Taylor Swift concert. Go to the store, and the salad aisles are ransacked like there’s a lettuce shortage, and half of your coworkers suddenly start quoting Warren Buffett while buying stock in companies they can’t spell. You got it, it’s “New Year’s Resolution Season.” That time of the year when we all promise ourselves to lose weight, work out, and save money, all before Valentine’s Day.

But by February, reality shows up with a cold slap. Those treadmill you bought is now a clothes rack for the laundry, and your credit card bill looks like you confused “budgeting” with “blowout sale.” Oh, and that investing plan you laid out? It turned into a Coinbase account holding three meme coins, a YouTube guru playlist, and a browser permanently stuck on Reddit’s WallStreetBets.

So why do we do this to ourselves every year? We can blame history and human nature.

The Babylonians started the tradition of New Year’s resolutions by promising their gods they’d return borrowed tools. Not a bad idea, unless you’re the guy who lent out a plow in 1900 B.C. and never saw it again. Then the Romans made it official by swearing oaths to Janus, their god of beginnings. Janus had two faces—one for looking back at last year’s mess, and one for pretending this year’s going to be different. That’s also where we get the name “January.” Fitting for a month built entirely on denial.

Back then, New Year’s resolutions were about crops and keeping your ox alive. Now it’s about washboard abs and beating the S&P 500 by following someone named “CryptoWolf69” on social media.

Why the obsession? Because being average feels like failure. New Year’s resolutions offer a psychological sugar rush by tricking your brain into thinking momentum is action. You say you’ll track your spending, invest consistently, and finally understand how options work. But three weeks later, you’re back to impulse-buying crypto at midnight while watching reruns of Shark Tank.

However, this is where the wheels fall off. New Year’s resolutions don’t fail because you’re weak; they fail because you built them on a foundation of hope, caffeine, and Instagram quotes. You set goals that sound great after two glasses of wine on New Year’s Eve. But you skip the parts that matter—routine, discipline, and not quitting after three bad days. You want the six-pack, but not the push-ups. You want the returns, but not the risk management.

It’s the same with investing.

You swear you’ll “invest for the long term.” Unfortunately, the “long term” only exists until the market drops 5% and suddenly you’re all cash, reading articles with headlines like “Is This the Big One,” and watching YouTube channels with individuals claiming the end has finally come. While you say retirement is a priority, you’ve never run a projection or calculated your savings rate. You make investment decisions based on TikTok, then act shocked when your portfolio resembles one that was managed by a teenager.

Most people don’t destroy their portfolios in one move. They do it slowly, by:

- Building bad habits,

- Assuming motivation will last,

- Confusing effort with consistency.

By the time they realize it’s not working, the damage is already done.

Short-term enthusiasm is not a plan. It’s an illusion.

If your investing goals are tied to the calendar instead of a disciplined process, you’re not managing money; you are chasing a feeling, and just like your unused gym membership, that approach ends in frustration. Every. Single. Time.

So, why do we continue to make bad investment decisions?

Why We Continue To Repeat Our Mistakes

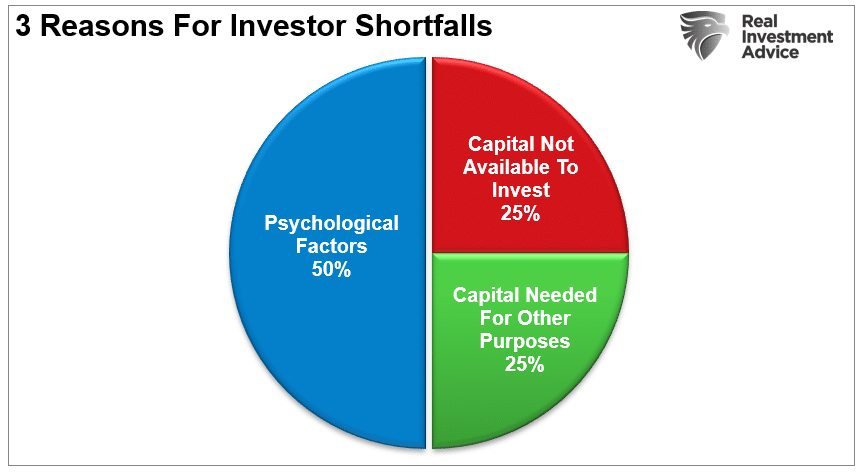

Every year, Dalbar Research releases a report that reads like a horror story for investors. Different year, same conclusion: we are our own worst enemy.

The problem isn’t just a lack of money. It’s what goes on between your ears. Dalbar outlined nine classic investing behaviors that sabotage your returns faster than you can say “buy the dip.”

- Loss Aversion – You fear losing money so much that you sell everything… right before the rebound.

- Narrow Framing – You obsess over one stock while ignoring the rest of your portfolio, slowly imploding.

- Anchoring – You keep waiting for a stock to “get back to even,” like it owes you something.

- Mental Accounting – You treat your retirement fund and crypto wallet like two different worlds, even though both are on fire.

- Lack of Diversification – You think owning five tech stocks is a “balanced strategy.”

- Herding – You invest because everyone else is. It ends exactly how you’d expect.

- Regret Aversion – You don’t act because you’re still haunted by the time you sold Apple in 2012.

- Media Response – You react to financial news like it’s a fire drill, even when it’s just smoke.

- Optimism Bias – You think every investment will “bounce back.” Even the one currently under SEC investigation.

The worst offenders are herding and loss aversion. This is because investors jump in when markets are euphoric, but then panic-sell during every correction. It’s the financial version of eating an entire pizza and then blaming your scale. However, we keep repeating these mistakes because markets can play tricks with your mind. The higher they go, the more you believe the rally is permanent. The lower they drop, the more you’re convinced it’ll never recover. You buy high, sell low, and wonder why your account never grows.

This is why you need a different kind of resolution, one built for the reality of investor behavior, not your fantasy of becoming the next Warren Buffett overnight.

Investor Resolutions for 2026 (That Might Actually Work)

Let’s be honest: emotions ruin portfolios. So in 2026, skip the vague promises and start with specific rules that stand a chance against your worst instincts. Here’s a better resolution list, built for real investors, not fantasy league traders:

In 2026, I will (or at least attempt to):

- Stick with what’s working and cut what’s not. No more “hoping it turns around.”

- Respect the trend. Fighting it is how you get broke.

- Be bullish or bearish—but not greedy. Hogs get slaughtered.

- Accept that paying taxes means I made money. That’s a good thing.

- Buy in stages, use limit orders, and stop chasing like it’s Black Friday.

- Hunt for value, not train wrecks with a PR team.

- Diversify because bad stuff always happens somewhere.

- Set stop-losses. Use them and don’t argue with them.

- Actually do the research before you click “buy.”

- Don’t panic when markets fall. Breathe. Then double-check your plan.

- Treat cash like a position, not an insult.

- Expect market corrections. Act like an adult when they show up.

- Be ready to admit when you are wrong, rather than doubling down due to your ego.

- Leave “hope” out of your investment thesis.

- Stay flexible. Stubbornness isn’t a strategy.

- Be patient. Results take time, not adrenaline.

- Turn off the TV, log off TikTok, and spend more time with data than influencers.

I try to follow this list every year, and, like every year, I screw up a few items. That’s okay. The goal isn’t to be perfect; it’s to make fewer mistakes than last year because investing success doesn’t come from reading motivational quotes or watching market TikToks at midnight.

Like fitness, you don’t get results because you “bought” a gym membership. You get them because you showed up when it was hard. Investing is the same. There are no shortcuts and no magic formulas. There are only basic rules, boring discipline, and the consistency to do them longer than the guy next to you.

Want to be a better investor? Then keep your resolutions, even when the market gives you every reason not to.