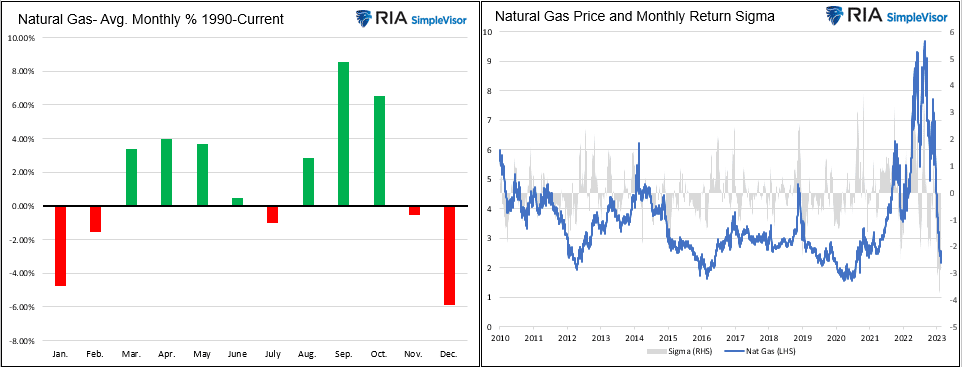

In mid-August, the price of natural gas peaked at $9.33. Forecasts for a cold winter here and in Europe and the Russian-Urkranian conflict led many to foresee natural gas shortages. The winter was generally milder than expected, and supply lines continued to normalize, driving the price of natural gas precipitously lower. Natural gas is around $2, down about 75% in six months. The graph on the right shows the stunning decline in prices. The bar chart on the left shows average returns by month. It is not uncommon for prices to decline during the winter months.

While the current situation may seem extremely bearish, natural gas is approaching 30-year lows. The graph on the right shows the most recent 30-day return is negative four sigmas. Statistically speaking, such an event should occur once every 126 years! Another reason we might expect better performance is seasonal returns. As we share, they tend to be positive from March through October.

What To Watch Today

Economy

- 8:30 a.m. ET: Chicago Fed National Activity Index, January (-0.49 prior)

- 8:30 a.m. ET: GDP Annualized, quarter-over-quarter, 4Q Second Estimate (2.9% expected, 2.9% prior)

- 8:30 a.m. ET: Personal Consumption, QoQ, 4Q Second Estimate (2.0% expected, 2.1% prior)

- 8:30 a.m. ET: GDP Price Index, quarter-over-quarter, 4Q Second Estimate (3.5% expected, 3.5% prior)

- 8:30 a.m. ET: Core PCE, quarter-over-quarter, 4Q Second Estimate (3.9% expected, 3.9% prior)

- 8:30 a.m. ET: Initial Jobless Claims, week ended Feb. 18 (220,000 expected, 194,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended Feb. 11 (1.696 million during prior week)

- 11:00 a.m. ET: Kansas City Fed Manufacturing Activity, February (-2 expected, -1 prior)

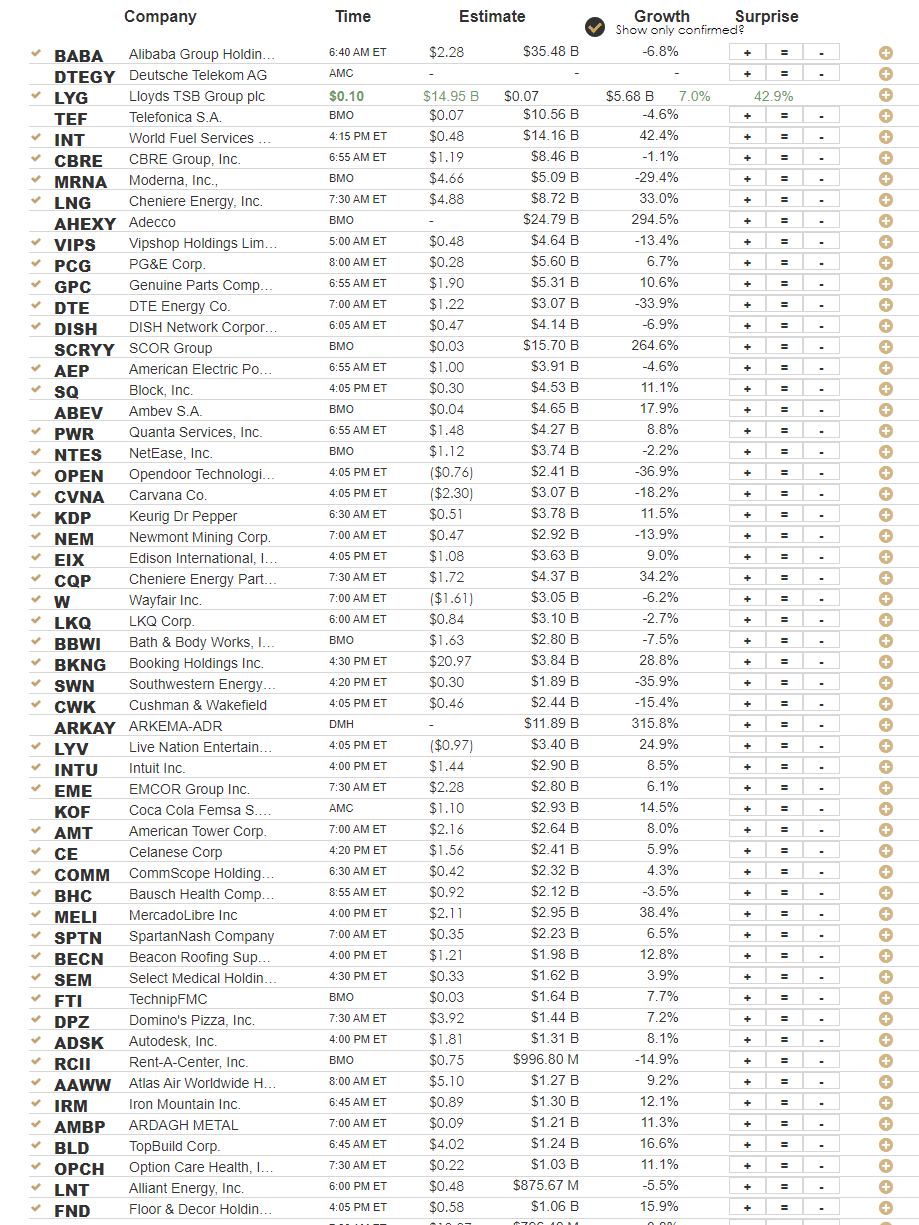

Earnings

Market Sell Off Continues

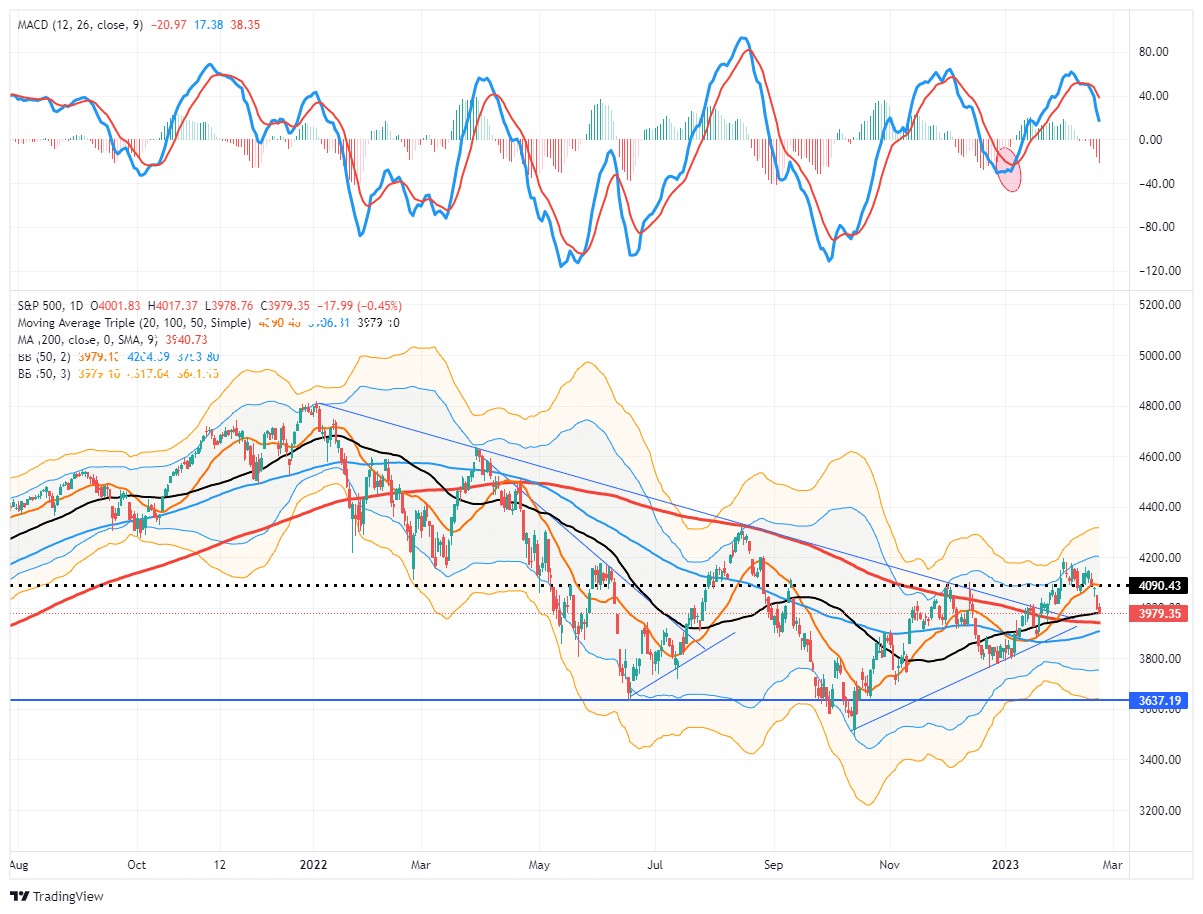

The market sell-off continued yesterday, with the market cracking through initial psychological support at 4000. For now the market is continuing to hold support above the 50- and 200-DMA, as well as the rising trendline from the October lows. As such, the overbought condition continues to reverse, but more time is needed to create the next buying opportunity. One concern remains the Fed’s ongoing hawkish stance, reiterated in yesterday’s release of the latest FOMC minutes. To wit:

“A few participants stated that they favored raising the target range for the federal funds rate 50 basis points at this meeting or that they could have supported raising the target by that amount. The participants favoring a 50-basis point increase noted that a larger increase would more quickly bring the target range close to the levels they believed would achieve a sufficiently restrictive stance, taking into account their views of the risks to achieving price stability in a timely way.“

More importantly, the Fed also acknowledged that financial conditions have decoupled from the Fed’s goal of tightening monetary policy to combat inflation.

“Participants noted that it was important that overall financial conditions be consistent with the degree of policy restraint that the Committee is putting into place in order to bring inflation back to the 2 percent goal.”

That commentary suggests the Fed will remain aggressive in combatting inflation for now, and markets are adjusting the terminal rate higher. All together, this is not stock market friendly, and the markets are starting to come to that realization.

Remain cautious for now.

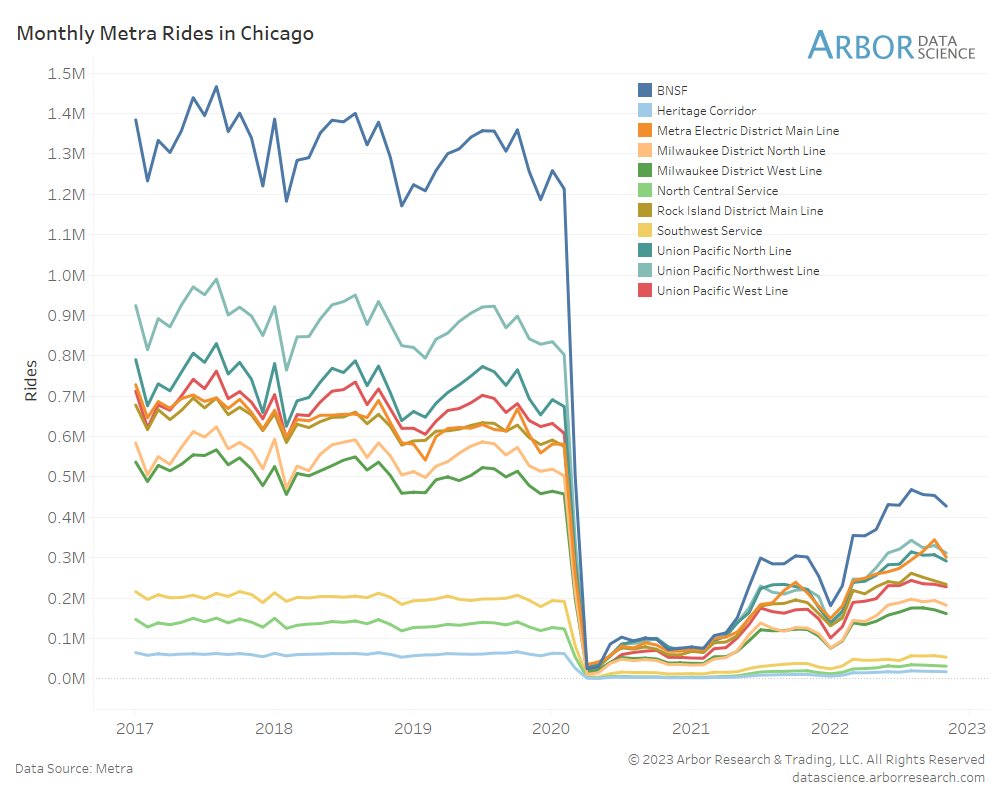

Mass Transit Commuting and Commercial Real Estate

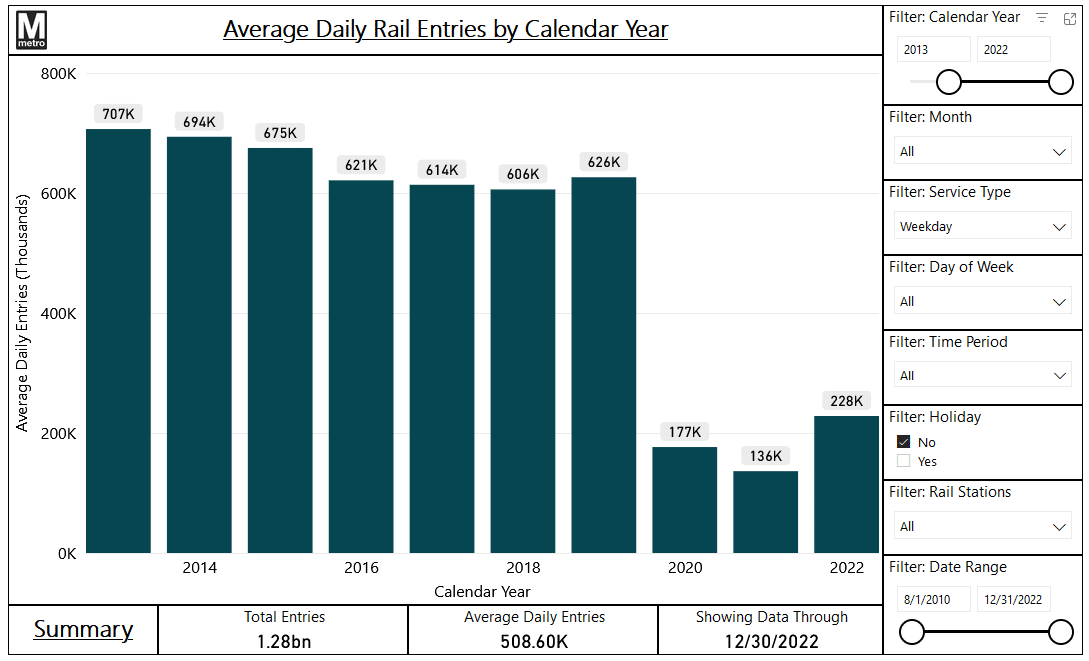

The stunning graph below from Jim Bianco and Arbor Data Science shows that Chicago’s main commuter subway lines are failing to return to normal following the pandemic. Similarly, the second graph from the Washington D.C. Metro shows a similar pattern. Per the New York Post, “Only 31 — or 7.2% — of the city’s 425 subway stations surveyed saw equal or increased ridership since 2019.” The work-from-home option many companies offer their employees is reducing commuter traffic in major cities. More importantly, from an economic perspective, it is also beginning to wreak havoc on the commercial real estate market. The Wall Street Journal recently chronicled rising default rates. Per the article, “The number of big office landlords defaulting on their loans is on the rise, fresh evidence that more developers believe that remote and hybrid work habits have permanently impaired the office market.”

FOMC Minutes

The FOMC minutes from the Fed’s last meeting were mainly in line with the Fed statement from the meeting and recent speeches by Fed members. Per the minutes, a “few” members advocated for a 50 bps rate hike, but most agreed 25bps was appropriate. Fed President Bullard and Mester acknowledged that they thought 50bps was appropriate last week.

There was no mention in the minutes of pausing rate hikes. The most important takeaway for stock investors is that the Fed is concerned that easier financial conditions (i.e., higher stock prices) will force them to raise rates more than expected. Per the minutes:

“A number of participants observed that financial conditions had eased in recent monhts, which some noted could neccessitate a tighter stance of monetary policy.”

Why Own Equities?

The graph below helps highlight an important decision investors should be contemplating. Is a 5% risk-free yield enough to warrant sitting out of the stock market? The blue line is the earnings yield (EPS/price) of the S&P 500. Therefore consider it the market yield if 100% of EPS were paid to investors. The blue line is the yield on the one-year Treasury bill. The gray shading shows the difference. As shown, the difference is now close to zero. Further, it is the lowest since the eve of the dot com crash in 2000. As we shared in yesterday’s Commentary, high valuations and margins argue the 5% bill yield, with no risk, is undoubtedly worth considering.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.