These days the financial media spends a lot of effort linking the Fed’s future actions with the direction of stocks. The rally since last fall is primarily based on hopes for a Fed pivot. Conversely, the recent decline is blamed on higher Fed Funds for longer. Looking beyond the Fed are two crucial factors in profit margins and valuations that investors should watch closely.

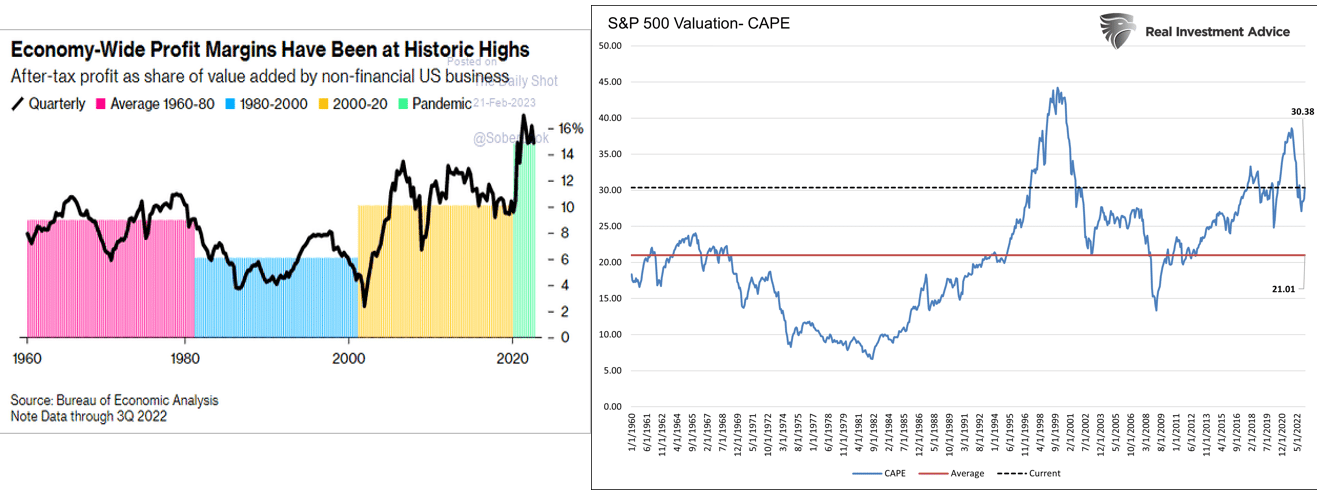

The graph on the left shows that corporate profit margins as a percentage of GDP are almost 5% above the running rate of the last 20 years. As the pandemic’s benefits evaporate, companies will find keeping margins at historical extremes increasingly challenging. Higher wages and softening demand are likely to result in margin reversion. The graph on the right shows that valuations, while not at record levels like margins, are well above historical norms. The combination of the two charts is worrisome. If margins and valuations normalize, stock prices are at risk for a more significant decline. However, both margins and valuations may stay elevated, which could fuel additional stock price gains.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended Feb. 17 (-7.7% prior week)

2:00 p.m. ET: FOMC Meeting Minutes, Feb. 1

Earnings

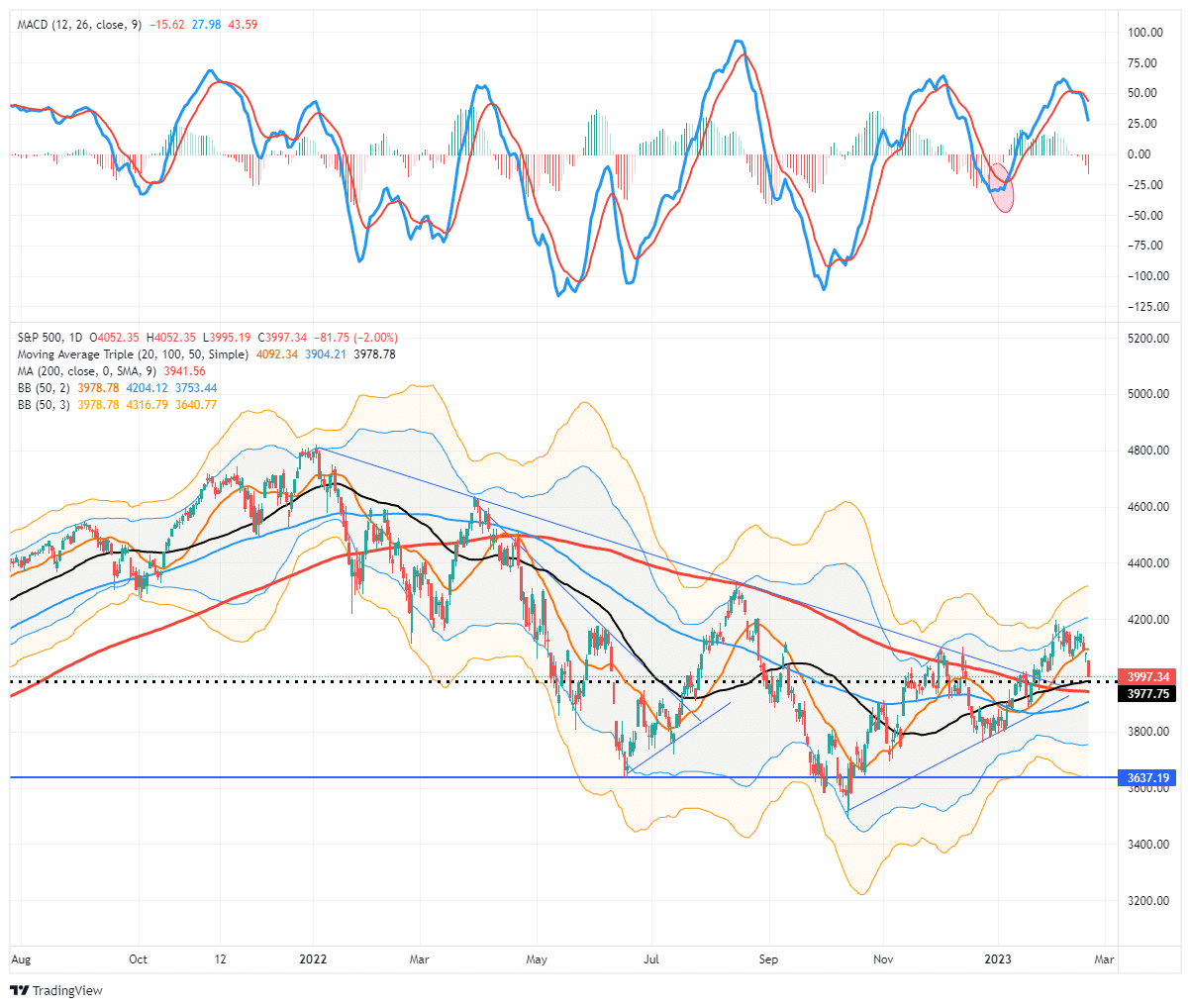

Market Falls To Initial Support

On February 14th, I posted “The Correction May Have Started,“ which laid out several critical support levels IF the bulls are going to remain in control of the narrative. To wit:

While that sell signal does NOT mean the market is about to crash, it does suggest that over the next couple of weeks to months, the market will likely consolidate or trade lower. Such is why we reduced our equity risk last week ahead of the Fed meeting. Notably, our previous analysis remains crucial. There are currently multiple levels of vital support for the S&P 500, as shown in the chart below.

- 4045 is the downtrend line from the June and December rally peaks (dotted black line)

- 4010 is the previous 38.2% retracement level from the October lows.

- 3969 is the rising 50-DMA moving average which has now crossed above the 200-DMA (orange line)

- 3942 is the intersection of both the neckline of the inverse head-and-shoulders bottoming pattern and the 200-DMA (black line)

Yesterday, the market dropped sharply to test initial support at the rising 50-dma. Just below that are the 200- and 100-dma. Crucially, the rising trend line from the October lows also intersect with the 50-dma. As noted then, that cluster of support is vital. If the market takes out those support levels, the bullish narrative from the beginning of the year will end. With the Fed taking on a more hawkish stance and retail earnings reports now showing real signs of consumer weakness, the “no recession” scenario is quickly losing it luster.

The market is technically oversold on several short-term levels, so an initial bounce off of support will not be surprising. However, with the MACD “sell signal” still very elevated, use bounces to reduce risk and raise cash for now.

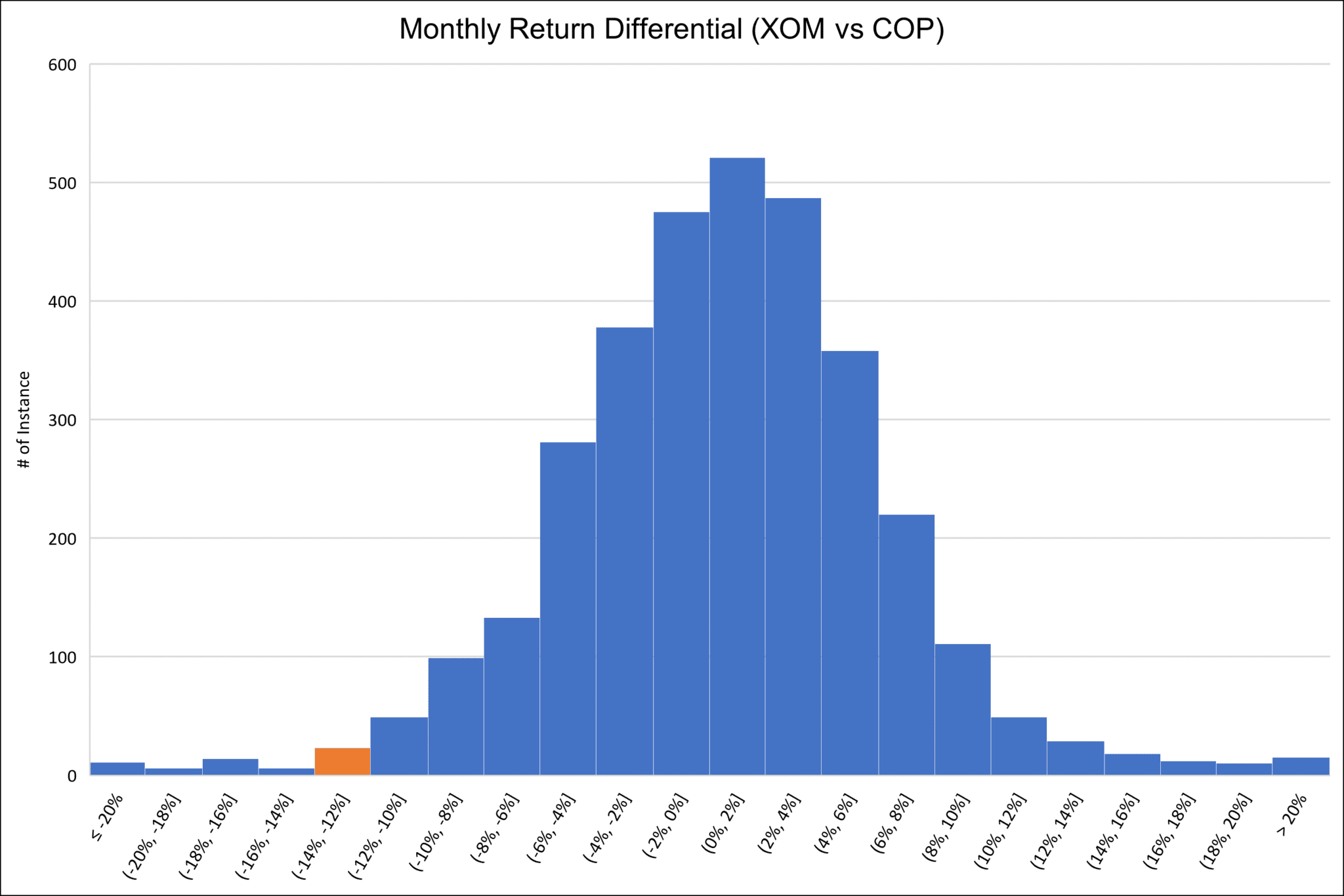

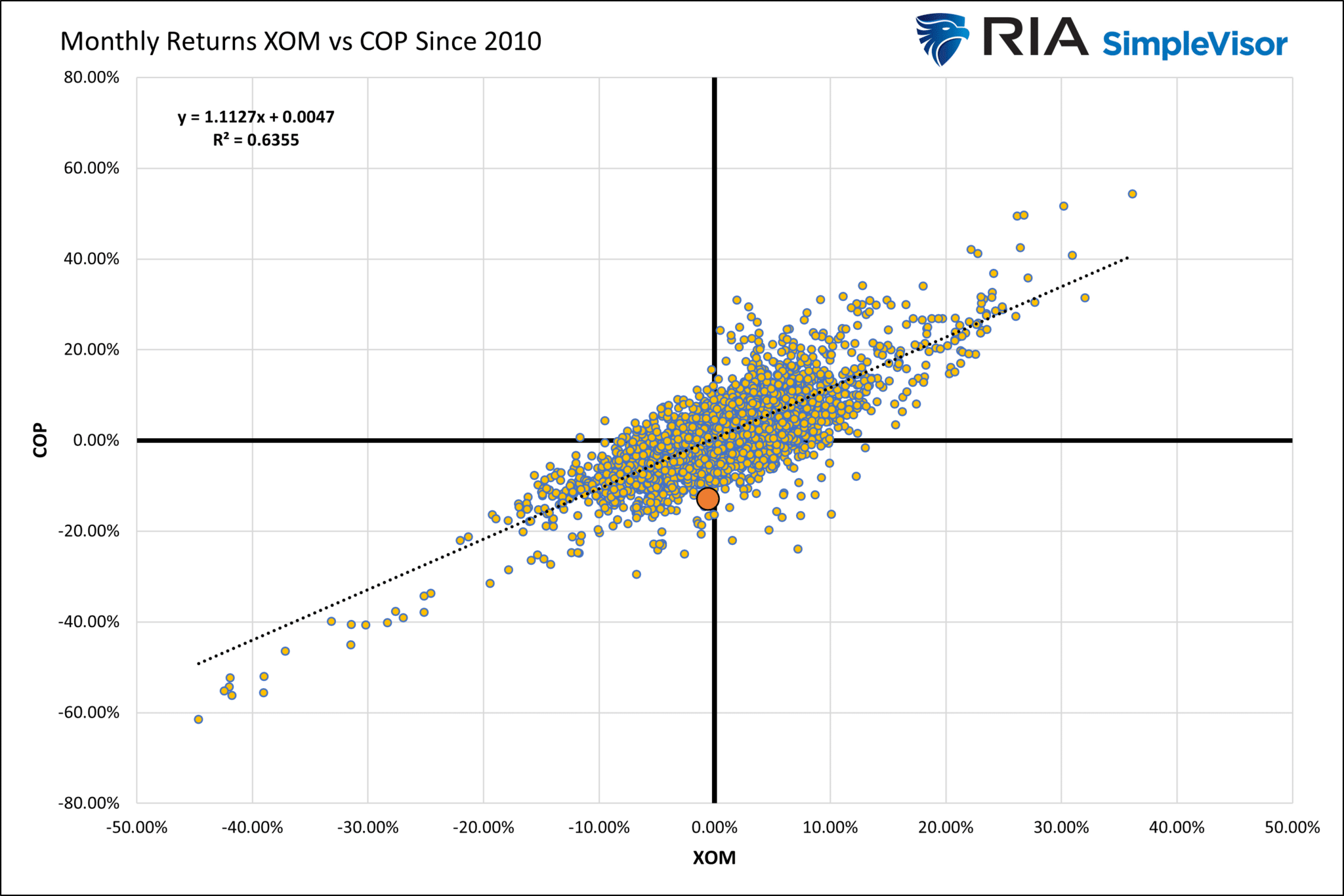

Exxon vs Conoco Phillips

Over the last 20 trading sessions, the price of Exxon (XOM) is flat, while Conoco (COP) has fallen by about 13%. The 13% divergence is interesting from a trading perspective as the two stocks tend to be highly correlated. The first graph below shows that over the last 3300 trading sessions, the monthly return differential between XOM and COP is primarily concentrated between +/- 10%. As highlighted with the orange bar, the most recent monthly period is well outside the norm. The second graph shows the same data in a scatter plot format. The orange dot marks the most recent intersection of XOM’s and COP’s monthly returns. COP needs to outperform XOM by about 14% to return to the dotted trend line. The trendline’s R-squared of .6355 shows the relationship is statistically significant, meaning a normalization should be expected.

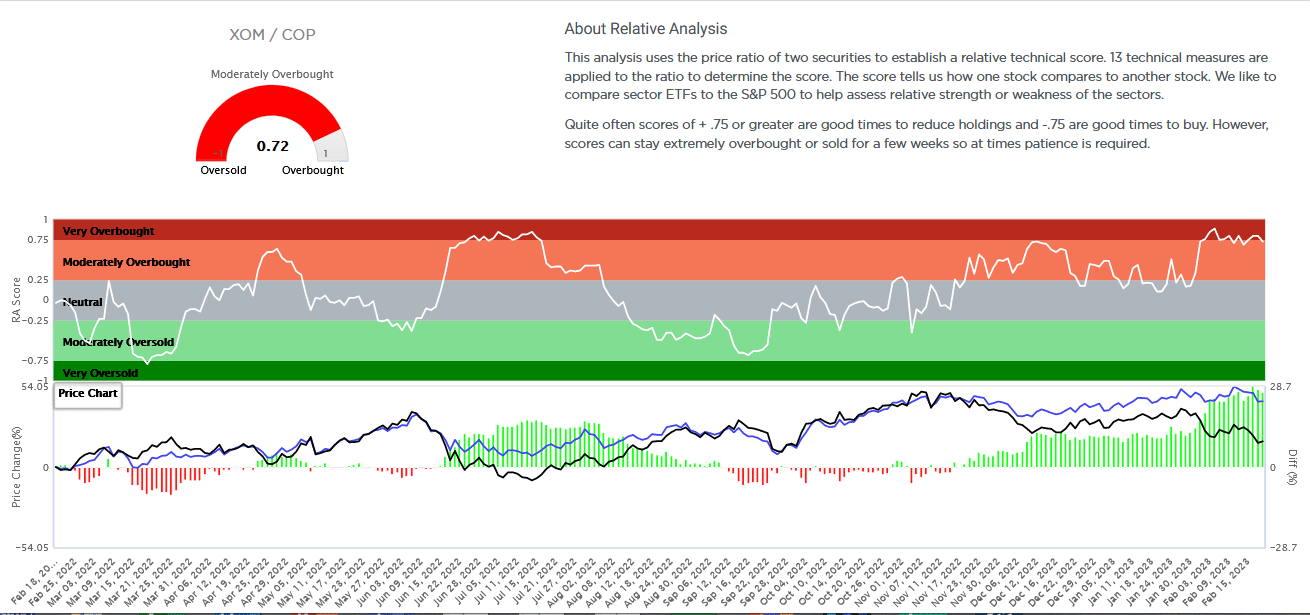

Lastly, the third graph from SimpleVisor analyzes a relative value of the two stocks using 13 different technical studies on their price relationship. Accordingly, it, too, shows that the price ratio of XOM to COP is highly overbought.

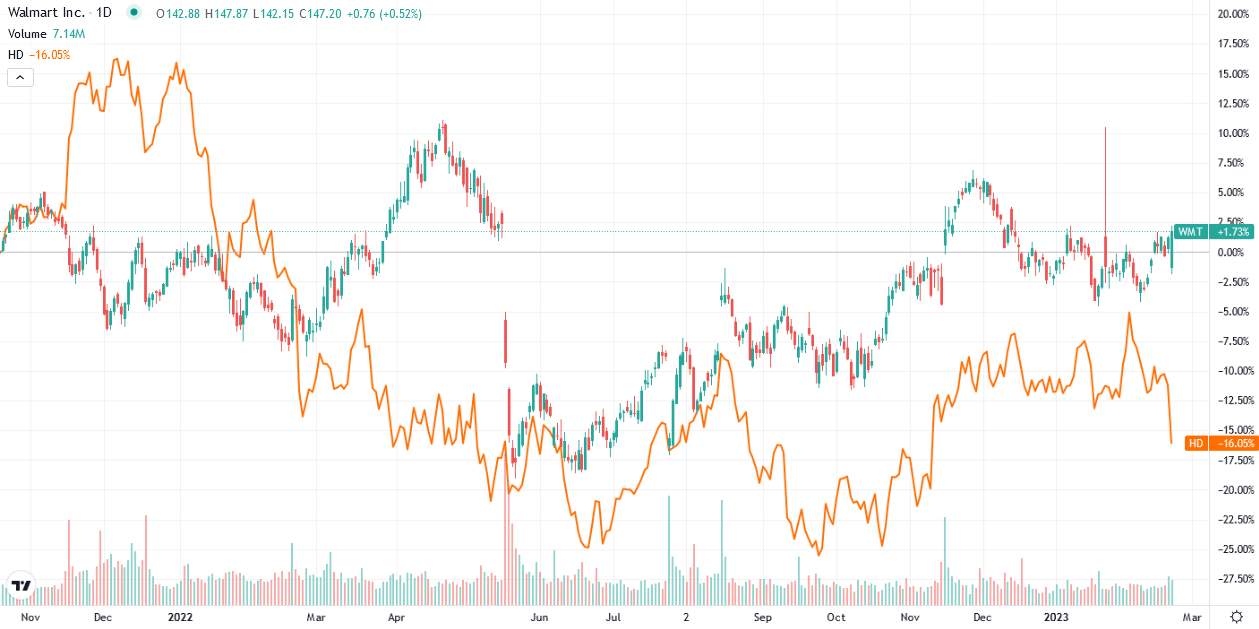

Walmart and Home Depot

The two large retail operations reported earnings on Monday, shedding light on the state of the consumer and their 2023 economic outlooks.

Walmart beat earnings and revenues estimates and, equally importantly, said their inventories are back to normal. The Q3 and Q4 bump in GDP and personal consumption helped Walmart on the earnings front and reduce its inventory. Despite the seemingly positive news, the company decreased 2023 earnings expectations to $5.90-$6.05 per share, down from $6.50. Walmart lowered expectations as they are cautious on the economy.

Home Depot missed revenue forecasts for the first time since 2019. Earnings, however, did beat estimates by a few cents. Like Walmart, Home Depot guided down earnings expectations as they are concerned about a recession. Further, they will be adding $1 billion in “annualized compensation for frontline, hourly associates.” Higher rates on home equity loans coupled with greater employee expenses also weigh on the company’s earnings expectations.

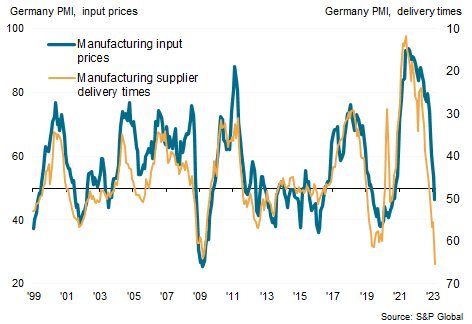

Germany Signals The Supply Chain Normal is Back to Normal

Germany is world’s third largest exporter behind the United States and China, accounting for nearly 7% of world trade. They are a significant supplier of vehicles, vehicle parts, machinery, chemical products, and computer/electrical equipment. Therefore, given the reliance many global manufacturers have on German exports, it worth considering the graph below. According to the latest PMI survey, Germany’s supplier delivery times shortened to the greatest extent on record in February. The decline marks a significant reversal of the pandemic-related supply chain constraints. More importantly, as the graph below shows, it bodes well for industrial prices pressures to fall further.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.