We can’t predict the future. If we could, fortune tellers would all win the lottery. They don’t, we can’t, and we aren’t going to try. However, this doesn’t stop the annual parade of Wall Street analysts from putting out forecasts on the S&P 500.

The Problem With Forecasts

In reality, all we can do is analyze what has happened in the past, weed through the noise of the present and try to discern the possible outcomes of the future.

The biggest single problem with Wall Street, both today and in the past, is the consistent disregard of the possibilities for unexpected, random events. In a 2010 study, by the McKinsey Group, they found that analysts have been persistently overly optimistic for 25 years. During the 25-year time frame, Wall Street analysts pegged earnings growth at 10-12% a year when in reality earnings grew at 6% which, as we have discussed in the past, is the growth rate of the economy.

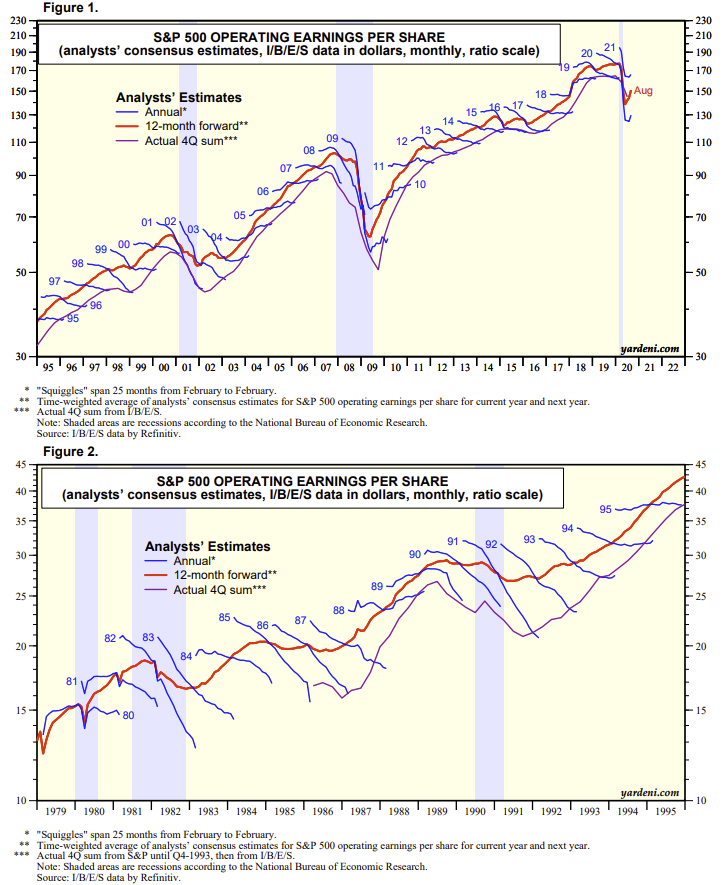

Ed Yardeni annually publishes the two following charts which also show analysts are always overly optimistic in their estimates.

This is why using forward earnings estimates as a valuation metric is so incredibly flawed – as the estimates are always overly optimistic roughly 33% on average.

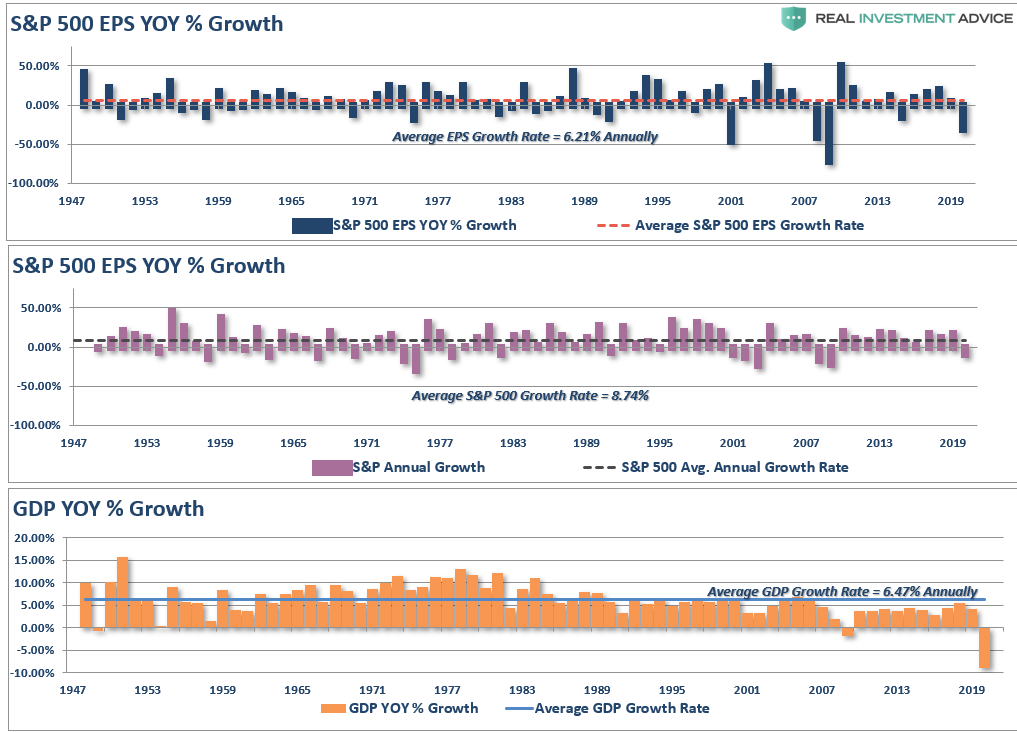

Furthermore, the reason that earnings only grew at 6% over the last 70-years is that the companies that make up the stock market are a reflection of real economic growth. Stocks cannot outgrow the economy in the long term.

“Since 1947, earnings per share have grown at 6.21% annually, while the economy expanded by 6.47% annually. That close relationship in growth rates should be logical, particularly given the significant role that consumer spending has in the GDP equation.”

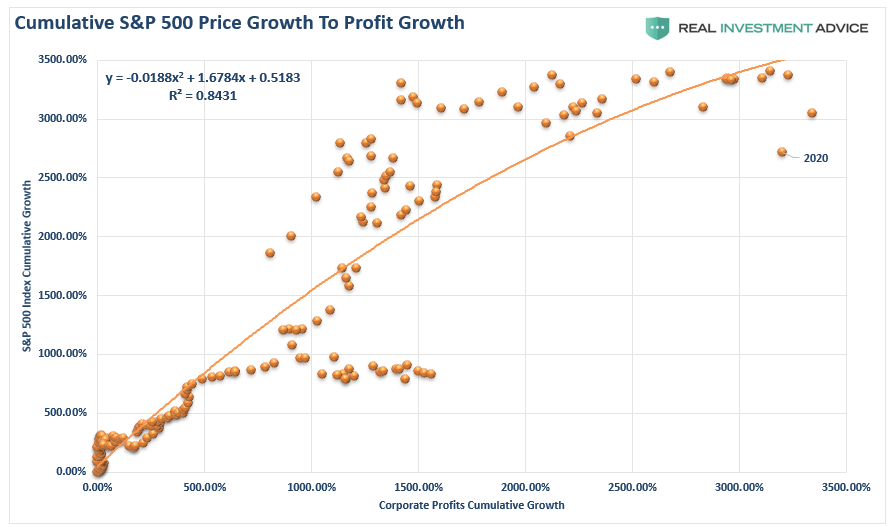

We can see this correlation even better when looking at the corporate profits versus stocks.

Conflicted Forecasters

The McKenzie study noted that on average “analysts’ forecasts have been almost 100% too high” and this leads investors into making much more aggressive bets in the financial markets. Wall Street is a group of highly conflicted marketing and PR firms. Companies hire Wall Street to “market” for them so that their stock prices will rise and with executive pay tied to stock-based compensation you can understand their desire.

However, if analysts are bearish on the companies they cover – their access to information to the company they cover is cut off. This reduces fees from the company to the Wall Street firm hurting their revenue. Furthermore, Wall Street has to have a customer to sell their products to – that would be you.

Talk about conflicted. Just ask yourself why Wall Street spends billions of dollars each year in marketing and advertising just to keep you invested at all times.

Since optimism is what sells products, it is not surprising, as we head into 2021, to see Wall Street’s average expectation ratcheted up another 6.5% this year. Of course, comparing your portfolio to the market is often a mistake anyway.

Comparison Is The Root Of Disappointment

“Comparison” is the root of unhappiness. Perhaps it is inevitable that human beings as social animals have an urge to compare themselves with one another. Maybe it is just because we are all terminally insecure in some cosmic sense. The social comparisons come in many different guises. “Keeping up with the Joneses,” is one well-known way.

But let me give you an example of why you should stop comparing yourself to everything, or everyone, else.

Let’s assume your boss gave you a Mercedes as a yearly bonus. You would be thrilled—right up until you found out everyone else in the office got two cars. Now, you are upset. But really, are you deprived of getting a Mercedes? Isn’t that enough?

Comparison-created unhappiness and insecurity are pervasive if only judging from the amount of spam mail touting everything from weight-loss to plastic surgery. The basic principle seems to be that whatever we have is enough until we see someone else who has more. Whatever the reason, comparison in financial markets can lead to remarkably bad decisions.

It is this ongoing “measurement complex” that remains the key reason why investors have trouble being patient and allowing the investment process to work for them. They get waylaid by some comparison along the way and lose their focus.

If you tell a client that they made 12% on their account, they are very pleased. If you subsequently inform them that “everyone else” made 14%, you have made them upset. The whole financial services industry is constructed to make people upset. When they are upset they will move their money to chase the next promise of riches. Money in motion creates fees and commissions. The constant push of comparison to benchmarks is nothing more than to keep individuals in a perpetual state of outrage.

A Note On Risk Management

What is important is to focus on what is important to you. Your specific goals, risk tolerance, time frames, and conservatively growing your savings to outpace inflation.

Such is why we always focus on the management of risks. Greater returns are generated from the management of “risks” rather than the attempt to create returns. Although it may seem contradictory, embracing uncertainty reduces risk while denial increases it.

Another benefit of acknowledged uncertainty is it keeps you honest.

“A healthy respect for uncertainty and focus on probability drives you never to be satisfied with your conclusions. It keeps you moving forward to seek out more information, to question conventional thinking and to continually refine your judgments and understanding that difference between certainty and likelihood can make all the difference.” – Robert Rubin

The reality is that we can’t control outcomes; the most we can do is influence the probability of certain outcomes. Such is why the day to day management of risks and investing based on probabilities, rather than possibilities, is important not only to capital preservation but to investment success over time.

Shades Of 1999

“Maybe this time is different. Those words, supposedly the most dangerous to utter in the investing realm, came to mind amid the frenzied pops in the highly anticipated initial public offerings recently.”

That quote was from Randall Forsyth discussing why the current market mania reminds him of the “Shades of 1999.”

There are certainly many similarities between today and 1999. From exceedingly high valuations to a rush by private equity investors to IPO overly priced companies as quickly as possible. As discussed previously, “valuations” are a representation of market excesses. However, it requires a supportive underlying narrative, a “siren’s song” to lure “sailors onto the rocks.”

“I discovered what I believe to be the strongest bull case in an article by Rothko Research:

- In the past cycle, the Fed has become very sensitive to a sudden tightening in financial conditions, especially when equities start to fall aggressively

- Another $5 trillion USD is expected to resume in the coming months.

- Such would send US equities to new all-time highs

- Any bear retracement in the near term is a good opportunity to “buy the dip.”

- It is not a good time to try to short equities

One crucial thing that we have learned over the past 12-years is that the Fed has become very sensitive to a sudden tightening in financial conditions, especially when equities start to fall aggressively.” – Greg Frierman

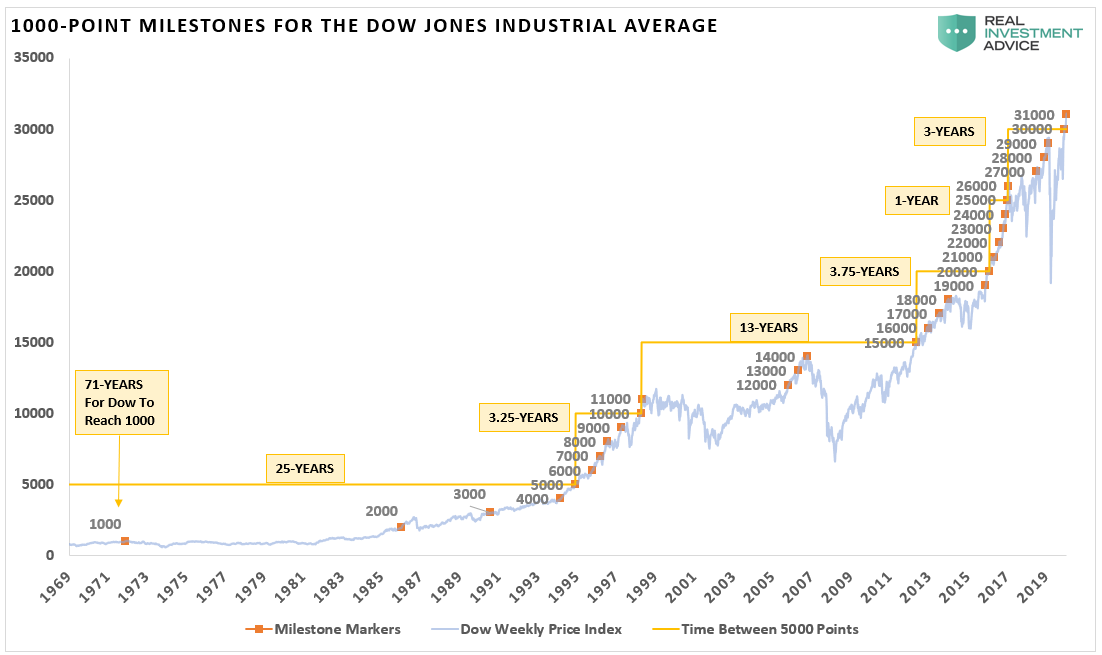

If price acceleration in the market is a sign of investor optimism, then this chart should raise some alarms.

The only other time in history where the Dow advanced this rapidly was during the 1995-1999 period of “irrational exuberance.”

Maybe it’s just coincidence.

Maybe “this time is different.”

Or it could just be the inevitable beginning of the ending of the current bull market cycle.

Risk Is Building

While analysts rushing to “out-predict” the other guys, it is worth noting:

- Markets are pushing historic levels of extreme overbought conditions,

- 2nd highest levels of valuation on record,

- Extreme deviations from long-term growth trend lines,

- Investor sentiment and confidence pushing extreme bullishness,

- Investors fully committed to the market with low levels of cash, and;

- High levels of leverage in terms of margin debt and corporate debt.

In other words, after 11-straight years of a bull market advance, what is the “risk” you are taking to garner additional returns?

While the odds of a positive year in 2021 are more, or less, evenly balanced, one should not dismiss the potential for a decline. With the current market already well advanced, pushing more extreme overvaluations, and significant deviations from long-term means, the risk of a decline is not minuscule.

Conclusion

I read most of the mainstream analyst’s predictions to get a gauge on the “consensus.” This year, more so than most, the outlook for 2021 is universally, and to some degree exuberantly, bullish.

What comes to mind is Bob Farrell’s Rule #9 which states:

“When everyone agrees…something else is bound to happen.”

The real economy is not supportive of asset prices at current levels. The more extended prices become, the greater the potential for a future market dislocation. For investors that are close to, or in retirement, some consideration should be given to capital preservation over chasing potential market returns.

Will 2021 turn in another positive performance? Maybe. But, honestly, I don’t really know.

#PortfolioHedgesMatter