“The stock market is not the economy.”

Such is the latest rationalization to support the “bull market” narrative. The question, however, is the validity of the statement. As I noted in this past weekend’s newsletter:

“There is currently a ‘Great Divide’ happening between the near ‘depressionary’ economy versus a surging bull market in equities. Given the relationship between the two, they both can’t be right.”

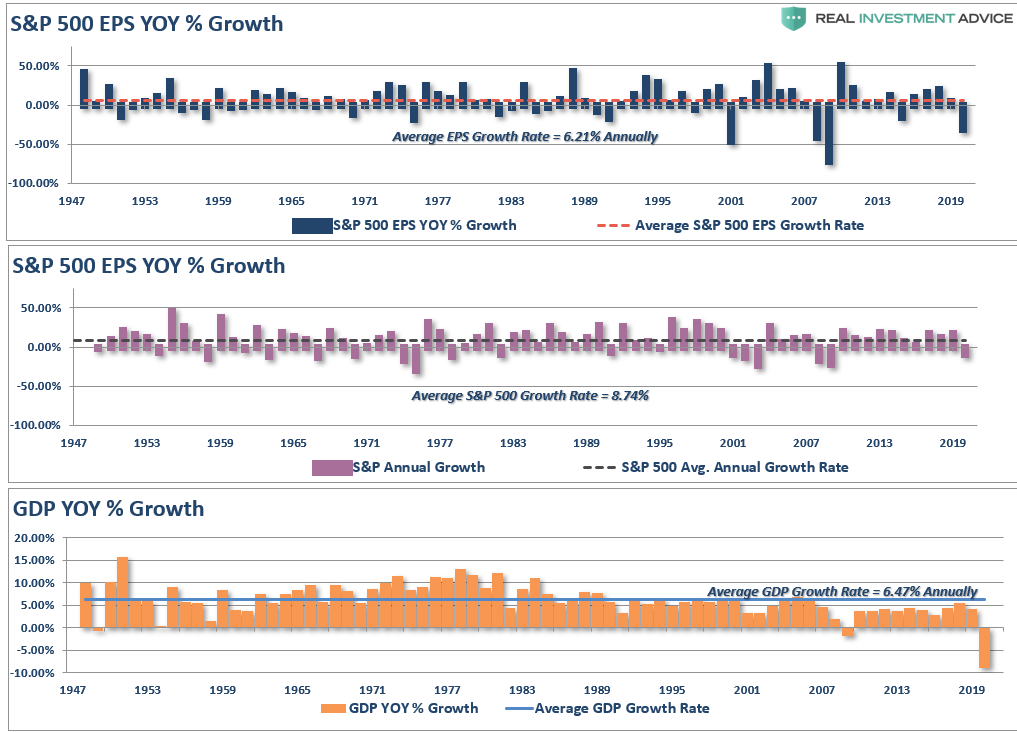

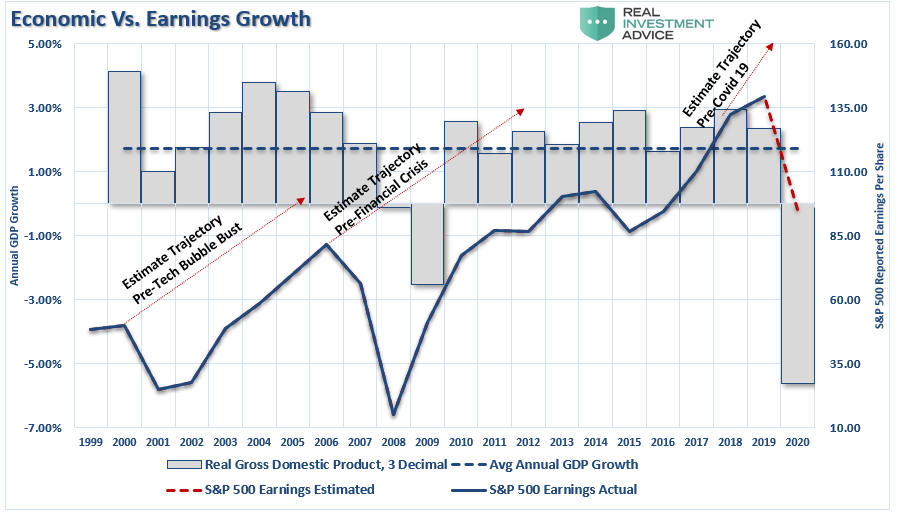

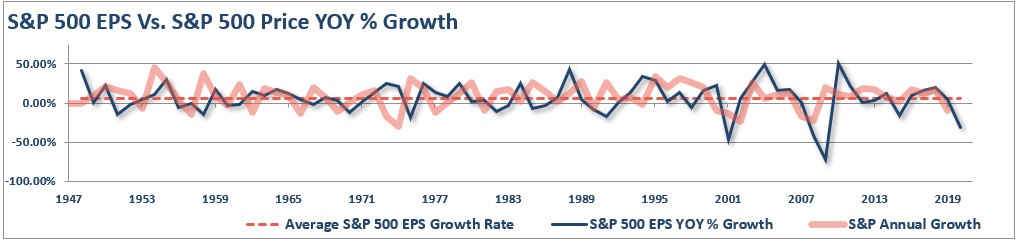

There is a close relationship between the economy, earnings, and asset prices over time. The chart below compares the three going back to 1947 with an estimate for 2020 using the latest data points.

Since 1947, earnings per share have grown at 6.21% annually, while the economy expanded by 6.47% annually. That close relationship in growth rates should be logical, particularly given the significant role that consumer spending has in the GDP equation.

The Consumption Function

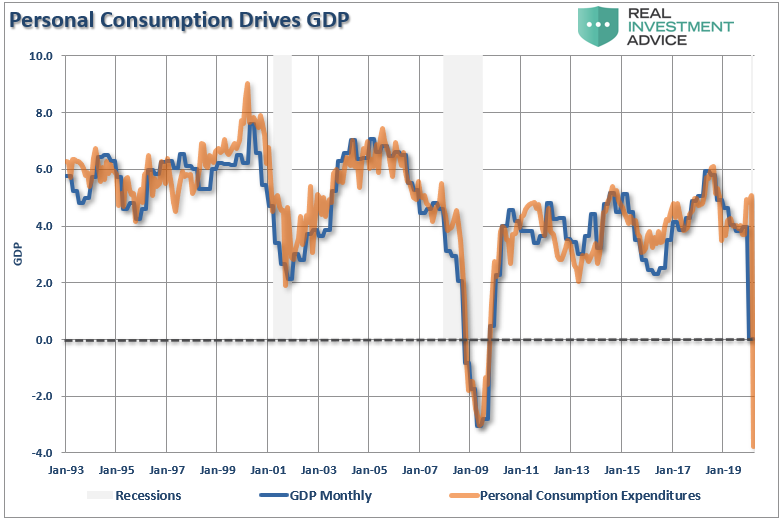

While stock prices can deviate from immediate activity, ultimately, reversions to actual economic growth eventually occur. Such is because corporate earnings are a function of consumptive spending, corporate investments, imports, and exports.

I subsequently received an email discussing the point.

“PCE depends on jobs and wages as well as intact supply chains, neither of which are in good condition. Regarding unemployment, the U6 rate, which is a more reliable indicator of job market health, is at 22.8% currently and rising while the labor market participation rate has dropped to about 60%. These factors do not bode well for growth and earnings for most companies.” – A Brinkley, Jr.

His statement is correct. There is a precise correlation between PCE and GDP. Not surprisingly, if consumption contracts due to high levels of unemployment, then economic growth declines.

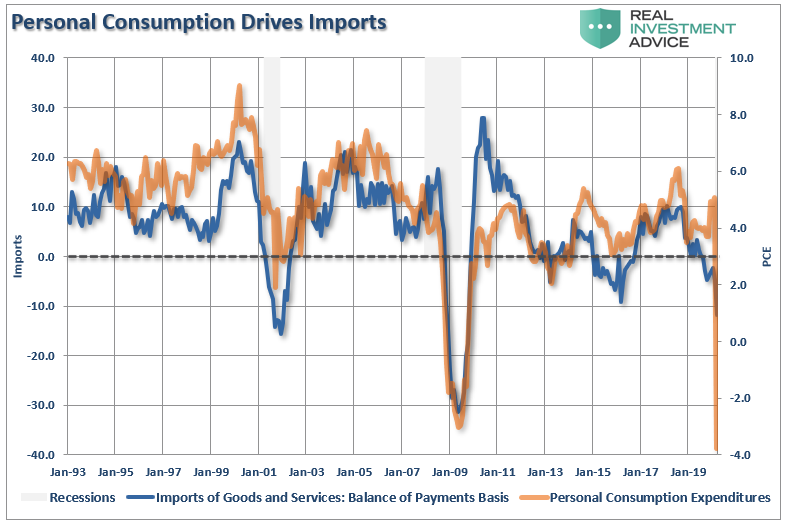

Furthermore, given that consumption drives imports, the correlation also stands.

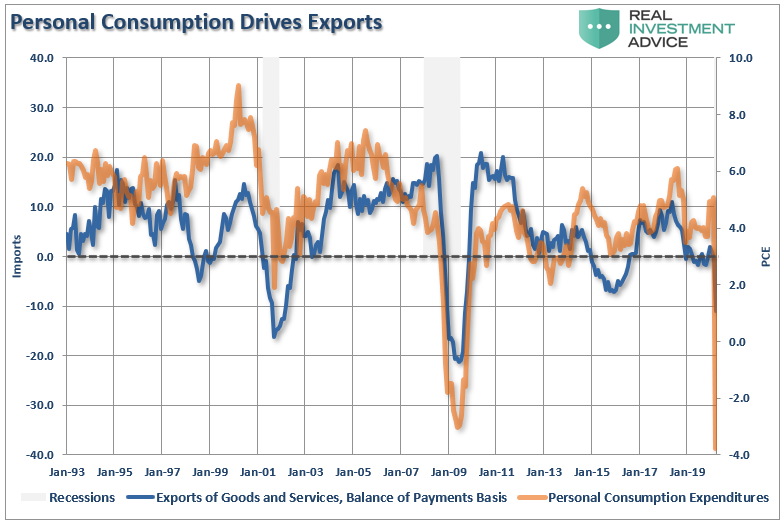

Exports, which comprise roughly 40% of corporate profits, also have a high correlation to consumption and related economic activity.

It should be evident that corporate earnings and profits are highly correlated to economic activity. While Business Investment and Government Spending do have an input into the economy, it is consumption which ultimately drives profits.

Stock Prices & The Economy

As stated, over short-term periods, the stock market often detaches from underlying economic activity as investor psychology latches onto the belief “this time is different.”

Unfortunately, it never is.

While not as precise, a correlation between economic activity and the rise and fall of equity prices does remain. In 2000, and again in 2008, as economic growth declined, corporate earnings contracted by 54% and 88%, respectively. Such was despite calls of never-ending earnings growth before both previous contractions.

As earnings disappointed, stock prices adjusted by nearly 50% to realign valuations with both weaker than expected current earnings and slower future earnings growth. While the stock market is once again detached from reality, looking at past earnings contractions, suggests it won’t be the case for long.

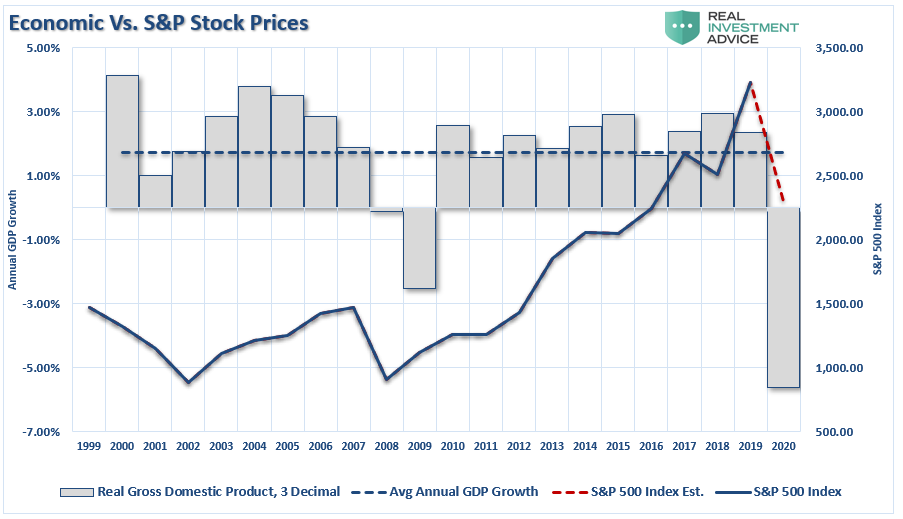

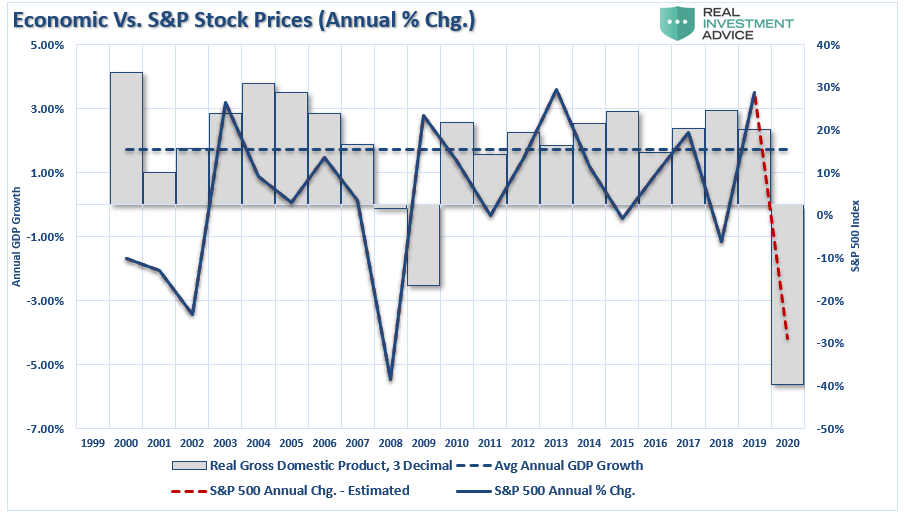

The relationship becomes more evident when looking at the annual change in stock prices relative to the yearly change in GDP.

Again, since stock prices are driven in part by the “psychology” of market participants, there can be periods where markets become detached from fundamentals. However, there is no point in the previous history, where the fundamentals catch up with stock prices.

The Stock Market Isn’t The Economy

When it comes to the state of the market, corporate profits are the best indicator of economic strength.

The detachment of the stock market from underlying profitability guarantees poor future outcomes for investors. But, as has always been the case, the markets can certainly seem to “remain irrational longer than logic would predict.”

However, such detachments never last indefinitely.

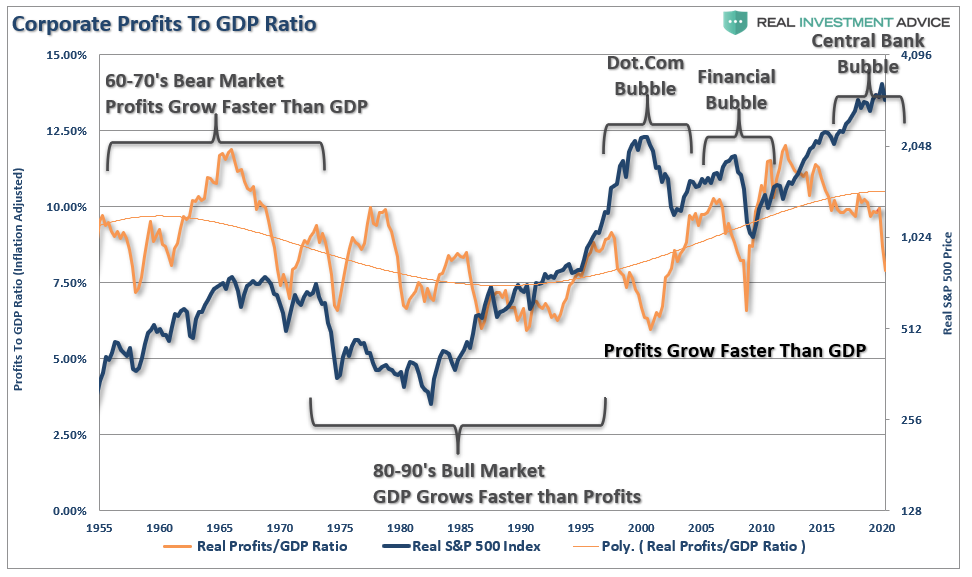

“Profit margins are probably the most mean-reverting series in finance, and if profit margins do not mean-revert, then something has gone badly wrong with capitalism. If high profits do not attract competition, there is something wrong with the system, and it is not functioning properly.” – Jeremy Grantham

As shown, when we look at inflation-adjusted profit margins as a percentage of inflation-adjusted GDP, we see a process of mean-reverting activity over time. Of course, those mean reverting events always coincide with recessions, crises, or bear markets.

As shown below, peaks, and subsequent reversions, in the ratio have been a leading indicator of more severe corrections in the stock market over time. Such should not be surprising as asset prices should eventually reflect the underlying reality of corporate profitability.

More importantly, corporate profit margins have physical constraints. Out of each dollar of revenue created, there are costs such as infrastructure, R&D, wages, etc. Currently, one of the biggest beneficiaries to expanding profit margins has been the suppression of employment, wage growth, and artificially low borrowing costs. The recession will cause a rather marked collapse in corporate profitability as consumption declines.

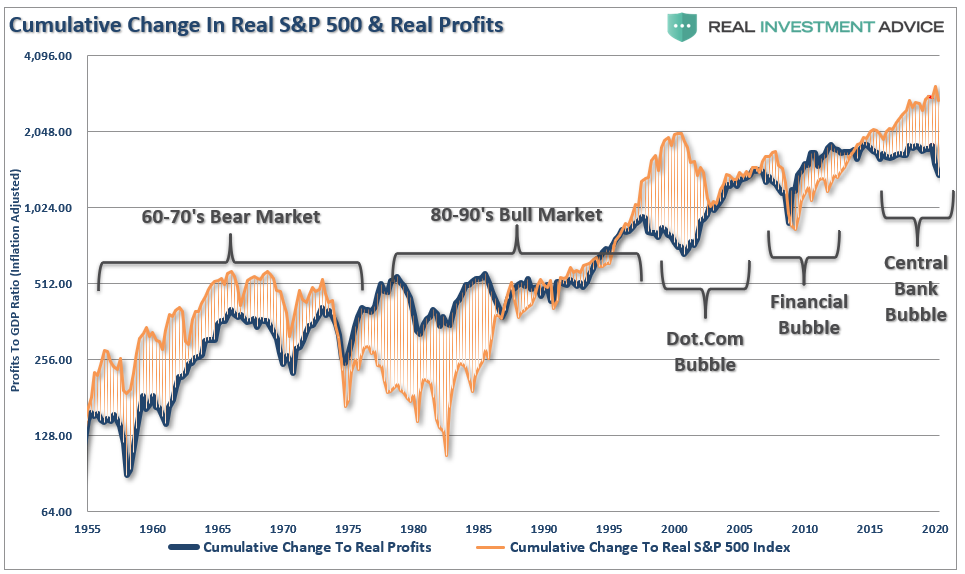

Recessions Reverse Excesses

The chart below measures the cumulative change in the S&P 500 index as compared to corporate profits. Again, we find when investors pay more than $1 for a $1 worth of profits, there is a reversal of those excesses.

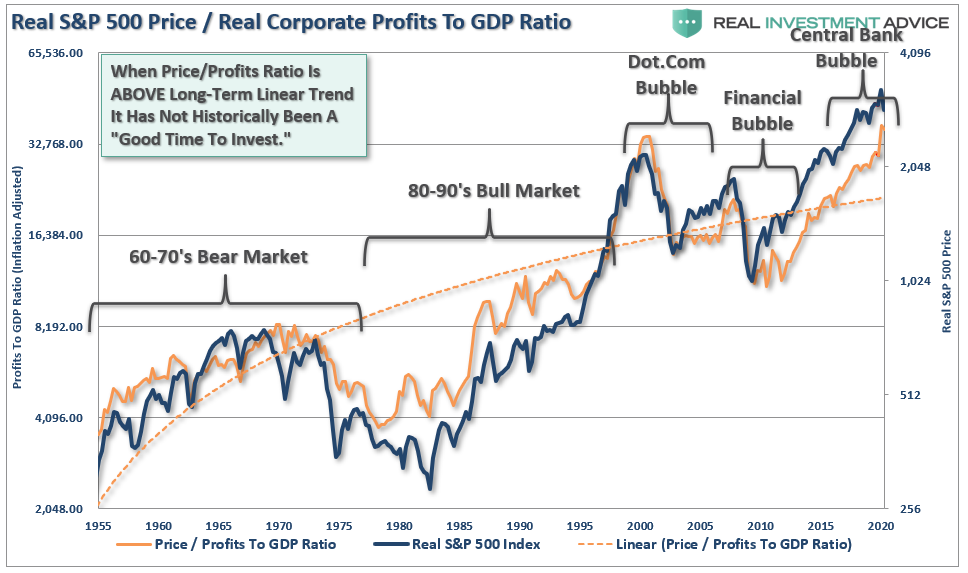

The correlation is more evident when looking at the market versus the ratio of corporate profits to GDP. Again, since corporate profits are ultimately a function of economic growth, the correlation is not unexpected. Hence, neither should the impending reversion in both series.

To this point, it has seemed to be a simple formula that as long as the Fed remains active in supporting asset prices, the deviation between fundamentals and fantasy doesn’t matter. It has been a hard point to argue.

However, what has started, and has yet to complete, is the historical “mean reversion” process which has always followed bull markets. This should not be a surprise to anyone, as asset prices eventually reflect the underlying reality of corporate profitability.

Recessions reverse excesses.

Rallying Into Uncertainty

While it may seem for the moment that stock prices can remain detached from the economic devastation, it is likely not the case indefinitely. Such is especially the case given stocks are rising into a increasing list of uncertainties. (Adapted from Doug Kass.)

- The “value proposition” no longer exists.

- A summer swoon? Seasonality is coming into play.

- Corporate profits have been flat since 2014 and are likely to deteriorate markedly.

- My S&P EPS estimates are well below consensus at $80-90/share.

- Economic challenges going forward will absorb a vast majority of the Fed’s liquidity.

- The Federal Reserve is already rapidly slowing the rate of QE

- 5-stocks dominate the market and are responsible for the rally.

- Small- and Mid-caps stocks are sorely lagging.

- Market participants have rapidly returned to exuberance during the rally.

- No one wants to buy a “bear market” bottom.

- Surging debts and deficits are economic retardants, which will eventually reflect in earnings, profits, and weaker economic growth.

- A Democratic Presidential Win Could Be “Market Unfriendly”

- Buyback activity, which has comprised almost the entirety of the markets advance over the last several years, is slowing markedly.

- Pension plans problems are likely to become even larger problems, as discussed previously.

- Bonds do not agree with the stock market. Bonds, more often than not, are right.

- Trump is on the verge of restarting the “Trade War” with China.

Conclusion

There are a tremendous number of things that can go wrong in the months ahead. Such is particularly the case of a surging stock market against weakening fundamentals.

While investors cling to the “hope” that the Fed has everything under control, there is more than a reasonable chance they don’t.

Regardless, there is one simplistic truth.

“The stock market is NOT the economy. But the economy is a reflection of the very thing that supports higher asset prices – corporate profits.”