More than a few individuals were active in the markets in 1999-2000, but many participants today were not. I remember looking at charts and writing about the craziness in markets as the fears of “Y2K” and the boom of “internet” filled media headlines. It was quite the dichotomy. On one hand, it was feared that the turn of the century would “break the computer age,” as computers could not handle the date change to 2000. However, at the same moment, the internet would turbocharge the world with massive productivity increases.

Back then, the S&P 500, particularly the Nasdaq, rallied harder each day than the last. Market breadth looked pretty weak, as the big names were soaring, forcing indexers and ETFs to buy them to keep their weightings. The reinforcing positive feedback cycle fueled markets higher day after day.

I remember those days clearly. It was the “gold rush” of the 21st century for investors.

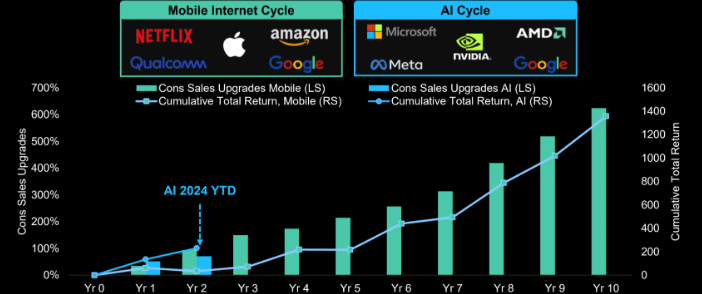

Interestingly, much like then, we are witnessing investors chase anything related to “artificial Intelligence.” Just as the internet had companies adding a “dot.com” address to their corporate name in 1999, today, we are seeing an increasing number of companies announce an “AI” strategy in their corporate outlooks.

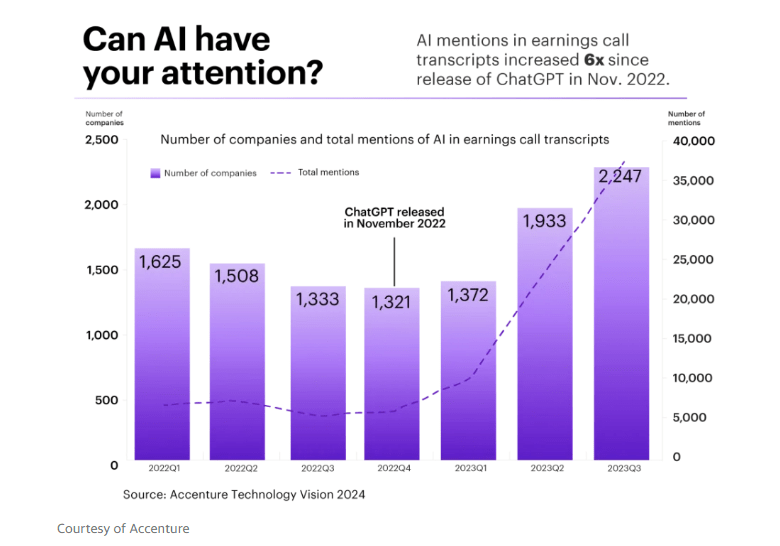

“Execs can’t stop talking about AI. The number of companies that have mentioned AI on earnings calls has rocketed since the launch of ChatGPT. The number of times AI has been mentioned on earnings calls has seen a similar rise.” – Accenture Technology Vision 2024 Report

The difference versus today was that companies would advance regardless of actual revenue, earnings, or valuations. It only mattered if they were on the cutting edge of the internet revolution. Today, the companies racing higher on artificial intelligence have actual revenues and income.

But does that difference remove the risk of another disappointing outcome?

A Forced Feeding Frenzy

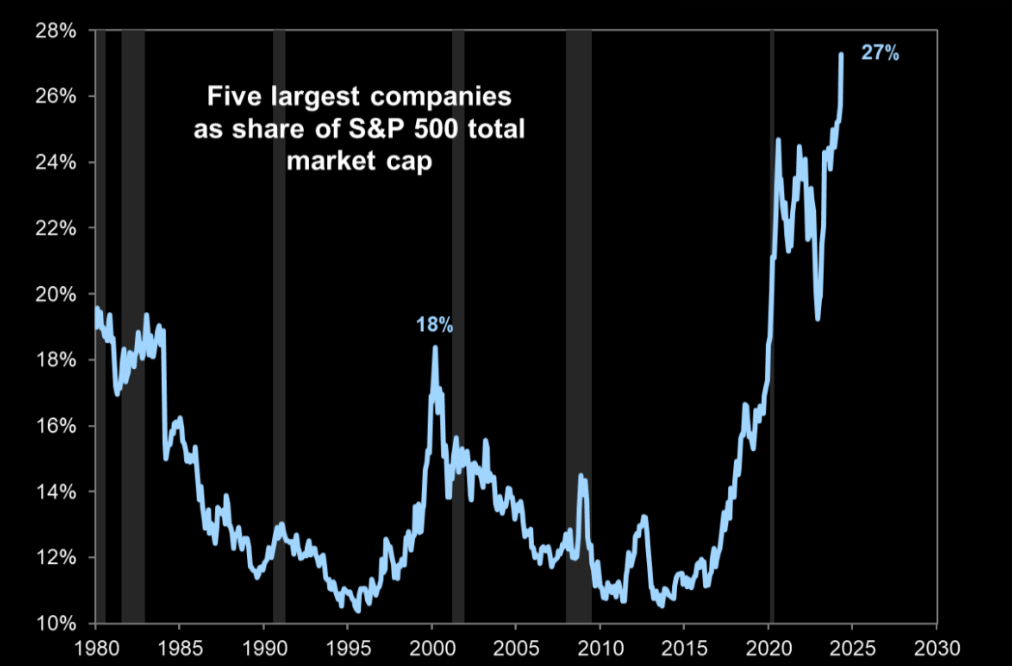

As noted above, in 1999, as the “Dot.com” bubble swelled, ETF providers and index tracking managers were forced to buy increasing quantities of the largest stocks to remain balanced with the index. As we have discussed previously, given the proliferation of ETFs and investors’ increasing amount of money flows into passive ETFs, there is a forced feeding frenzy in the largest stocks. To wit:

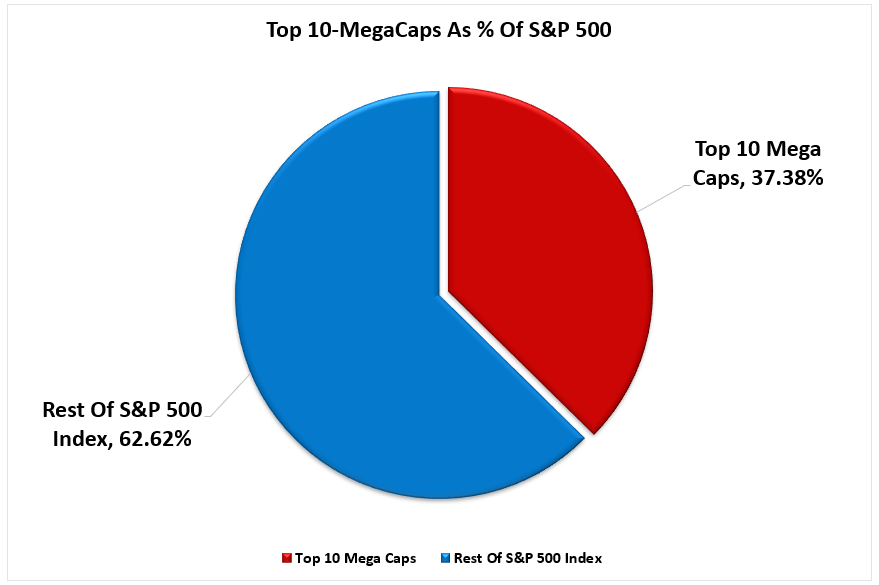

“The top-10 stocks in the S&P 500 index comprise more than 1/3rd of the index. In other words, a 1% gain in the top-10 stocks is the same as a 1% gain in the bottom 90%.

As investors buy shares of a passive ETF, the shares of all the underlying companies must get purchased. Given the massive inflows into ETFs over the last year and subsequent inflows into the top-10 stocks, the mirage of market stability is not surprising.

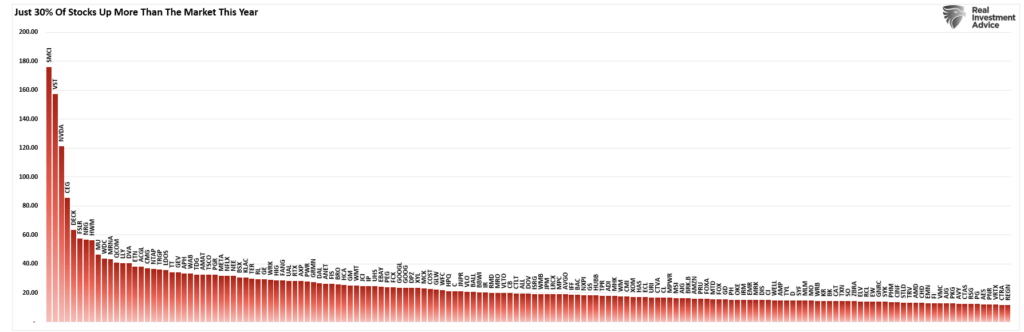

Unsurprisingly, the forced feeding of dollars into the largest weighted stocks makes market performance appear more robust than it is. As of June 1st, only 30% of stocks were outperforming the index as a whole.

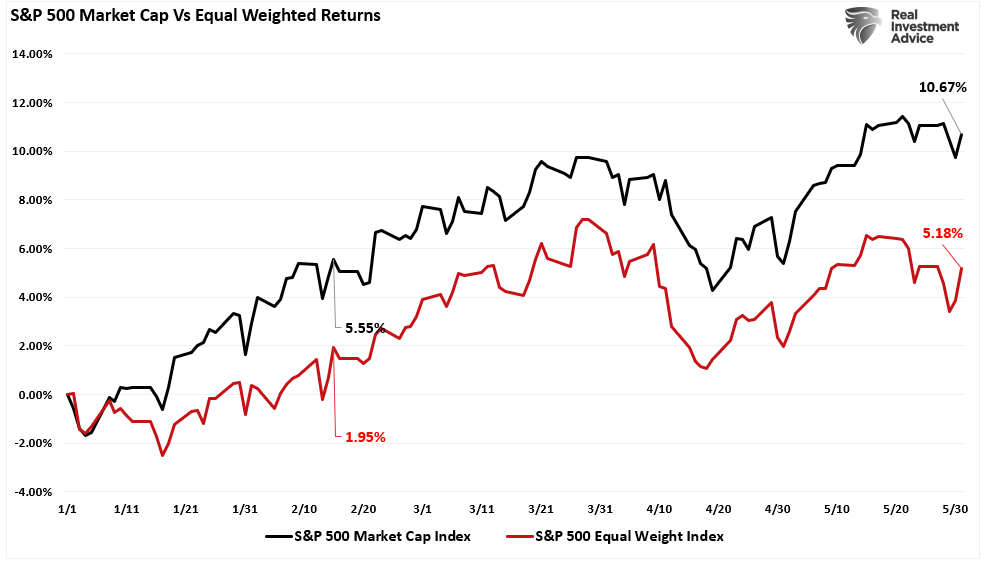

That lack of breadth is far more apparent when comparing the market-capitalization-weighted index to the equal-weighted index.

However, the concentration of flows into the largest market-cap-weighted companies continues to increase the market capitalization of those top stocks to levels well above that of the “Dot.com” bubble.

The forced feeding of the largest companies in the index, while reminiscent of 2000, does not mean there will be an immediate reversal. If this is indeed a bubble in the market, it can last far longer than logic would suggest.

Just as it was in 2000, what eventually causes the market reversal is when reality fails to live up to expectations. Currently, the sales growth expectations are an exponential growth trend higher.

While it is certainly possible that those expectations will be met, there is also a considerable risk that something will happen.

Trees Don’t Grow To The Sky

Just as in 2000, the valuations investors paid for companies like Cisco Systems (CSCO), which was the Nvidia (NVDA) of the Dot.com craze, plunged back to reality. The same could be true for Artificial Intelligence in the future. As noted recently by the WSJ:

“AI has had an astounding run since OpenAI unveiled ChatGPT to the world in late 2022, and Nvidia has been the biggest winner as everyone races to buy its microchips. To see what could go wrong, note that this isn’t the usual speculative mania (though there was a mini-AI bubble last year). Nvidia’s profits are rising about as fast as its share price, so if there is a bubble, it’s a bubble in demand for chips, not a pure stock bubble. To the extent there is a mispricing, it’s more like the banks in 2007—when profits were unsustainably high—than it is to the profitless dot-coms of the 2000 bubble.”

It is a good analysis of the four (4) things that could go wrong with AI:

- Demand falls because AI is overhyped. (Much like we saw with the Dot.com companies.)

- Competition reduces prices.

- Suppliers ask for a more significant share of the revenue.

- What if the scale doesn’t matter?

As Rober McNamee, a Silicon Valley investing legend, stated:

“There are corporations and journalists that have completely bought into this [the AI hype.] Before investors buy into this we should just ask: How are you going to get paid? How are you going to get a return on something that is effectively a half million dollars each time you do a training set… in a 5% environment.”

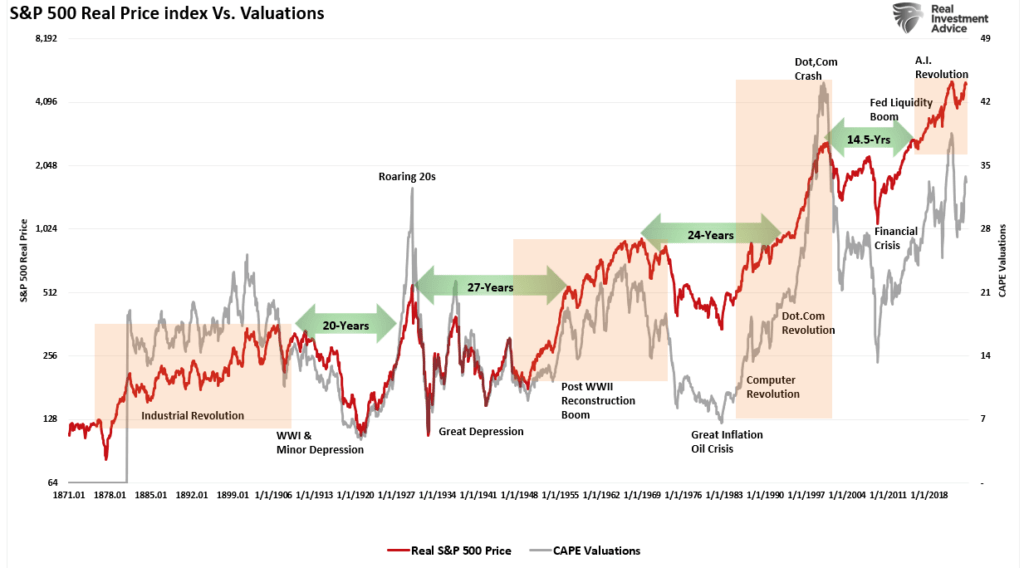

As is always the case, the current boom of “artificial intelligence” stocks is just another in a series of “investment themes” over the market’s long term.

“But if we learned nothing else during the SPACs, the crypto, the meme stocks, and whatever else fueled the market’s last run – you know, the one when stocks were the only place to put your money because rates were so low – it’s that when this stuff reverses, it’s always brutal.” – Herb Greenberg

And, as we noted previously:

“These booms provided great opportunities as the innovations offered great investment opportunities to capitalize on the advances. Each phase led to stellar market returns that lasted a decade or more as investors chased emerging opportunities.”

We are again experiencing another of these speculative “booms,” as anything related to artificial intelligence grips investors’ imaginations. What remains the same is that analysts and investors once again believe that “trees can grow to the sky.”

“Trees don’t grow to the sky is a German proverb that suggests that there are natural limits to growth and improvement.

The proverb is associated with investing and banking where it is used to describe the dangers of maturing companies with a high growth rate. In some cases, a company that has an exponential growth rate will achieve a high valuation based on the unrealistic expectation that growth will continue at the same pace as the company becomes larger. For example, if a company has $10 billion in revenue and a 200% growth rate it’s easy to think that it will achieve 100s of billions in revenue within a few short years.

Generally speaking, the larger a company becomes the more difficult it becomes to achieve a high growth rate. For example, a firm that has a 1% market share might easily achieve 2%. However, when a firm has an 80% market share, doubling sales requires growing the market or entering new markets where it isn’t as strong. Firms also tend to become less

efficient and innovative as they grow due to diseconomies of scale.

Modeling how quickly a growth rate will slow as a firm becomes larger is amongst the most difficult elements of equity valuation.” – Simplicable

The internet craze in 1999 sucked in retail and professionals alike. Then, Jim Cramer published his famous list of “winners” for the decade in March 2000.

Such is unsurprising, as endless possibilities existed of how the internet would change our lives, the workplace, and futures. While the internet did indeed change our world, the reality of valuations and earnings growth eventually collided with the fantasy.

No, today is not like 2000, but there are similarities. Is this time different, or will trees again fail to reach the sky? Unfortunately, we won’t know for certain until we can look back through the lens of history.