Investors are betting on Goldilocks, meaning slow but steady economic and employment growth. This scenario allows the Fed to cut rates further without a recession that frequently accompanies rate cuts. Concurrent with the market’s Goldilocks logic, investors were hoping Friday’s BLS report was weak enough to support a 50 bps rate cut but not too weak to raise recession fears. Historically speaking, threading that needle is a tough order.

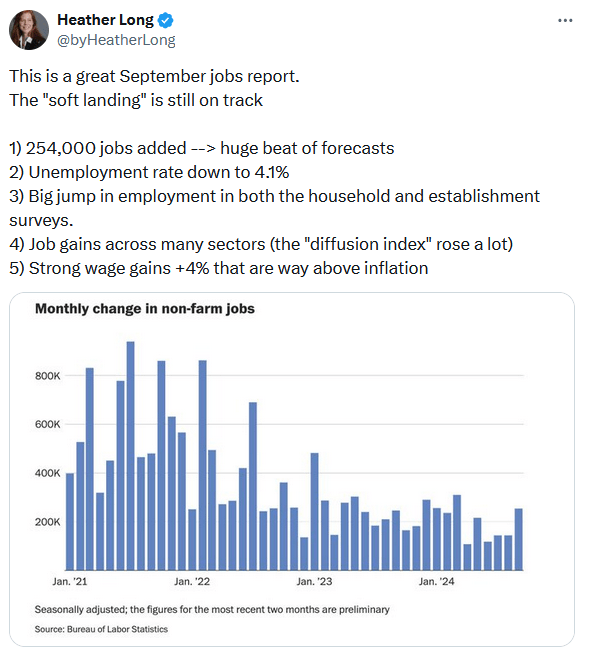

The BLS employment was hotter than expected, but based on the stock market’s initial reaction, the Goldilocks scenario is still in play. The economy added 254k jobs last month, well above expectations of 140k. Accordingly, the unemployment rate ticked lower to 4.1%. In its latest economic and Fed Funds forecast, the Fed thought the unemployment rate would end the year at 4.4%. Therefore, they presumed they would cut rates by 25 bps at the next two meetings. While the market has a similar Fed Funds forecast, it must consider that less than 50bps of rate cuts is possible if the economy and employment markets continue to run hotter than the Goldilocks scenario portends.

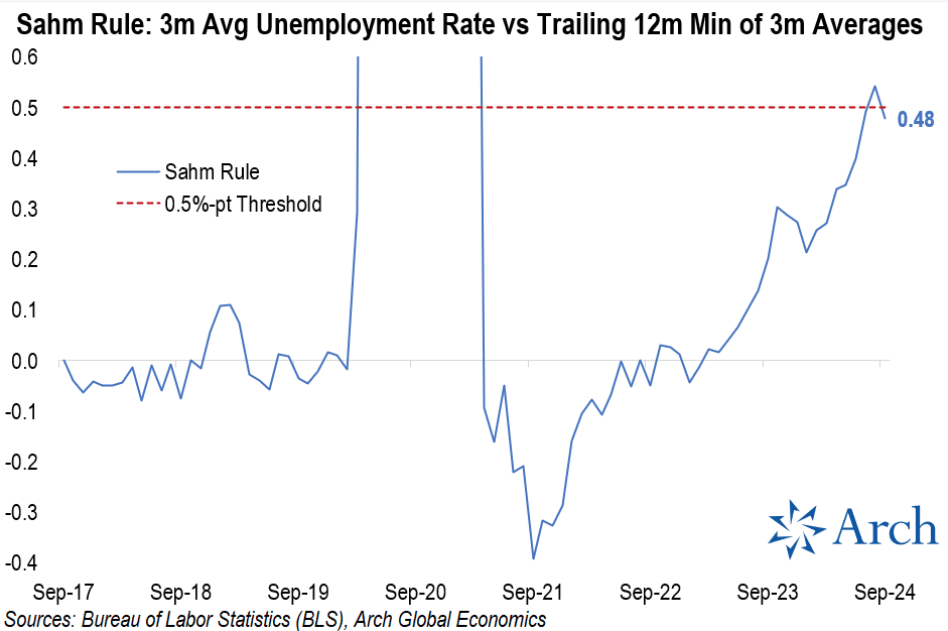

The graph below shows that the Sahm Rule triggered a recession warning last month and backed away from the warning with Friday’s data.

What To Watch Today

Earnings

- No notable earnings releases today.

Economy

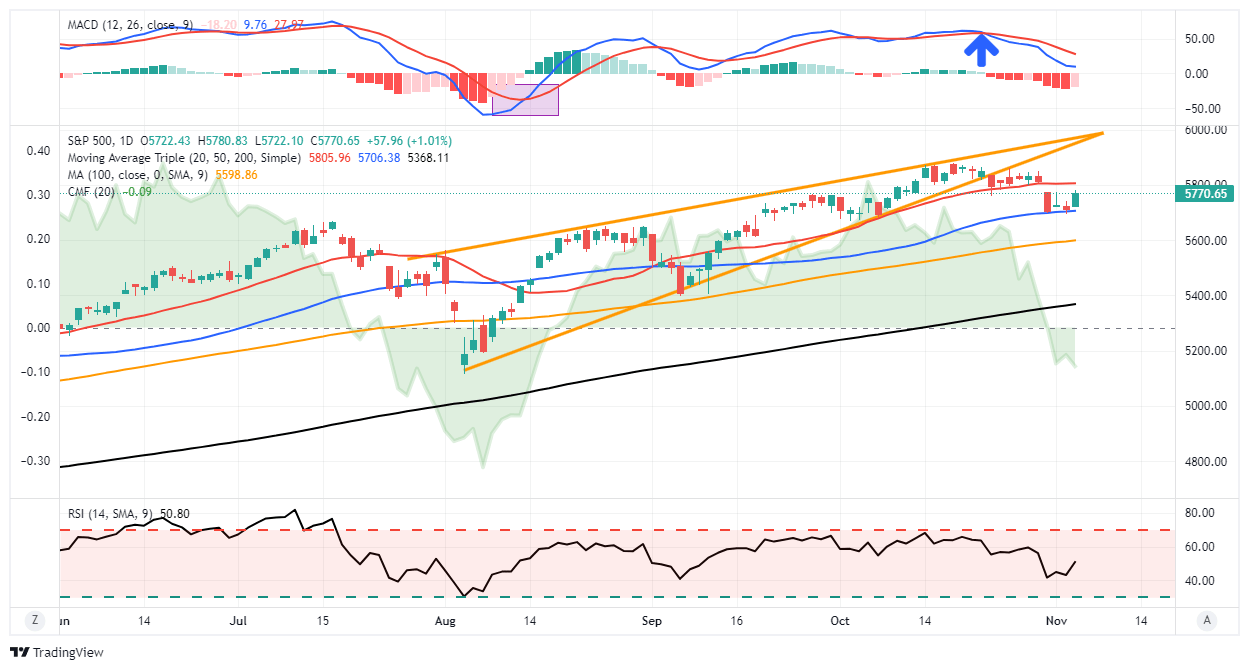

Market Trading Update

As noted last week, the market backdrop remains bullish, with weekly buy signals intact. However, as noted this past weekend, I would be remiss not to mention that the “Millennial Earnings Season” will be a significant market driver over the next month.

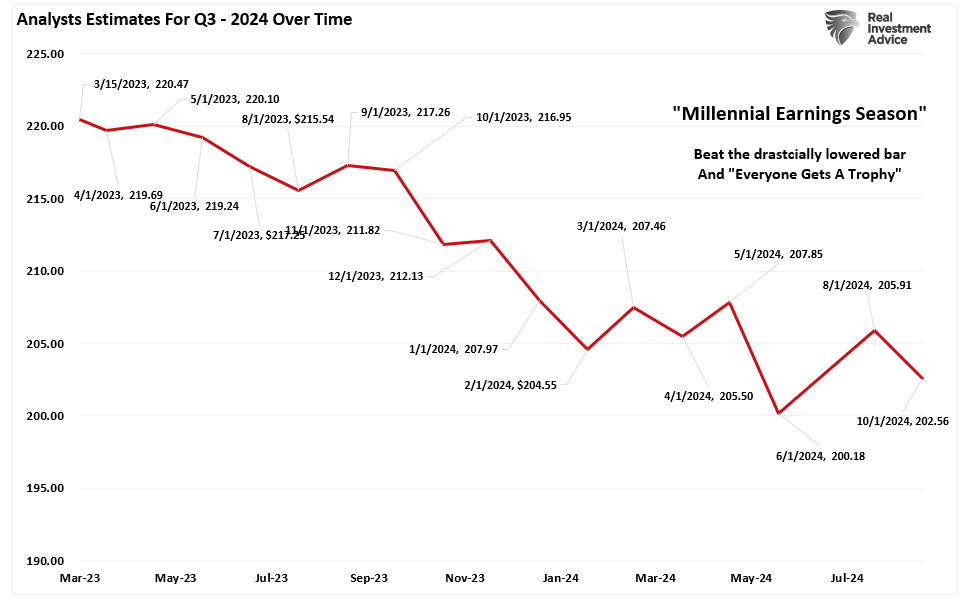

“As we have discussed, it will be unsurprising that we will see a high percentage of companies ‘beat’ Wall Street estimates. Of course, the high beat rate is always the case due to the sharp downward revisions in analysts’ estimates as the reporting period begins.”

The chart below shows the changes for the Q3 earnings period from when analysts provided their first estimates in March 2023. Analysts have slashed estimates over the last 30 days, dropping estimates by roughly $3.40/share, but nearly $18 lower than their initial estimate.

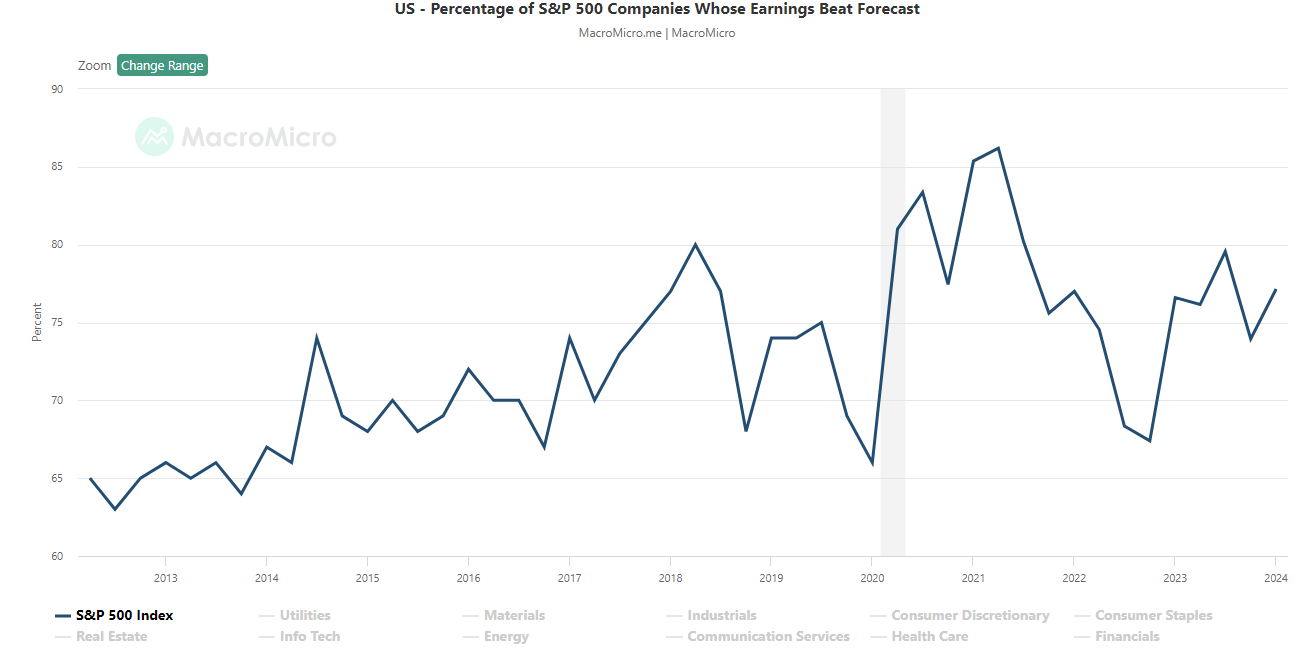

That is why we call it “Millennial Earnings Season.” Wall Street continuously lowers estimates as the reporting period approaches so “everyone gets a trophy.” An easy way to see this is the number of companies beating estimates each quarter, regardless of economic and financial conditions. Since 2000, roughly 70% of companies regularly beat estimates by 5%, but since 2017, that average has risen to approximately 75%. Again, that “beat rate” would be substantially lower if investors held analysts to their original estimates.

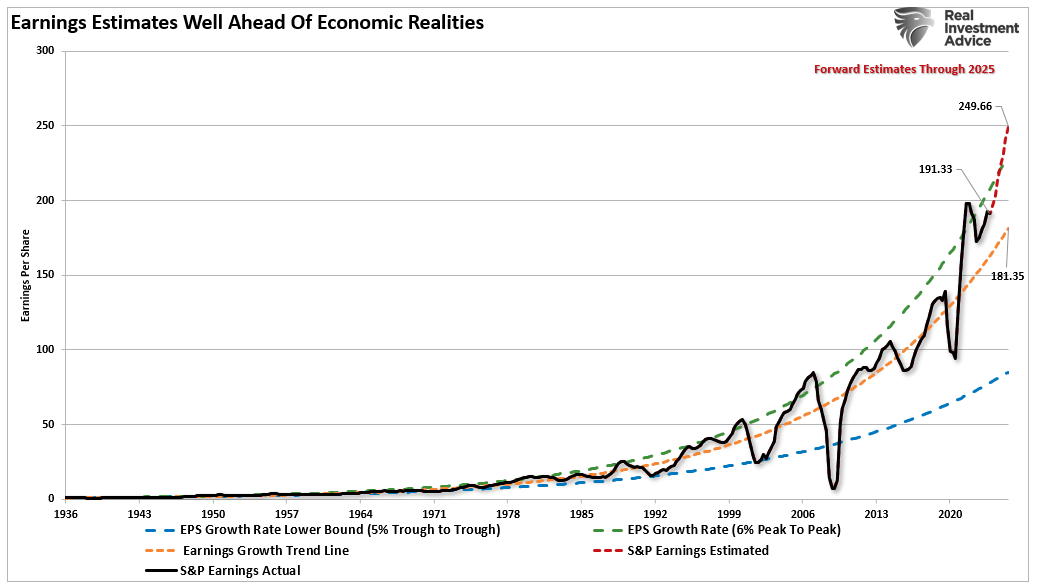

While stock markets are hitting all-time highs, and analysts are very optimistic about earnings into 2025, actual earnings have fallen well short of previous estimates. In other words, investors have overpaid for promised earnings growth that was not delivered.

However, even with the earnings bar lowered going forward, earnings estimates remain detached from the long-term growth trend.

As discussed previously, economic growth, from which companies derive revenue and earnings, must also strongly grow for earnings to grow at such an expected pace.

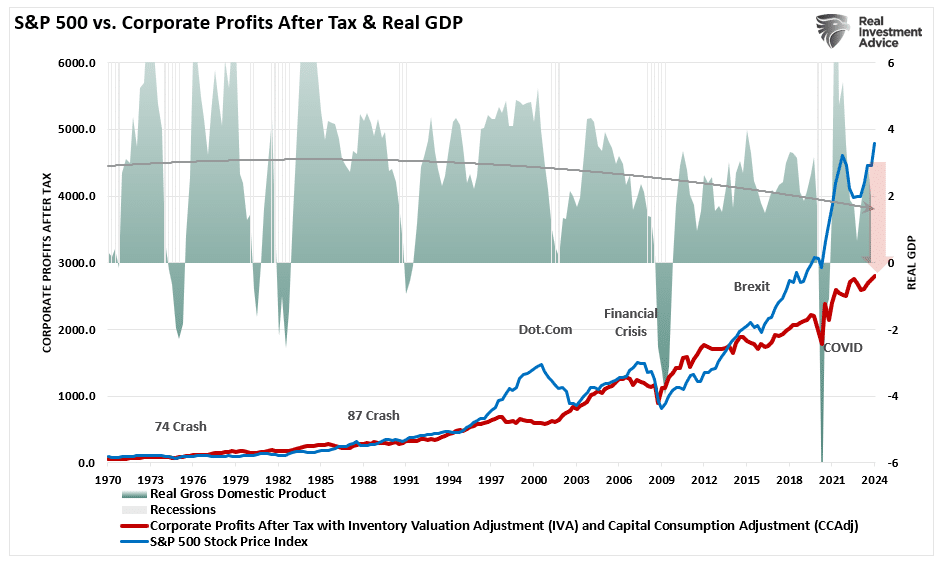

Since 1947, earnings per share have grown at 7.72%, while the economy has expanded by 6.35% annually. That close relationship in growth rates is logical, given the significant role that consumer spending has in the GDP equation. However, while nominal stock prices have averaged 9.35% (including dividends), reversions to underlying economic growth will eventually occur. Such is because corporate earnings are a function of consumptive spending, corporate investments, imports, and exports. The same goes for corporate profits, where stock prices have significantly deviated.

Such is essential to investors due to the coming impact on “valuations.”

Given current economic assessments from Wall Street to the Federal Reserve, strong growth rates are unlikely. The data also suggest a reversion to the mean is entirely possible.

Trade accordingly.

The Week Ahead

With the labor market on solid ground, investors will turn their focus to this week’s CPI and PPI reports. Stronger-than-expected inflation numbers would likely keep the Fed from easing at both meetings this year. Thursday’s CPI is expected to show a 0.3% increase in the core CPI and 0.2% in the headline CPI. The year-over-year CPI rate is expected to fall to 2.3%, closing in on the Fed’s 2% target. PPI is expected to rise by 0.1%.

The bond market will contend with the Treasury’s ten and 30-year bond auctions on Wednesday and Thursday. Given the recent data, these auctions may perform weakly. Accordingly, bond yields may rise further this week.

Lastly, earnings season kicks off in earnest this week. The large banks will lead the way, with JPM, Wells Fargo, and Bank of New York announcing on Friday.

Election Outcome Presents Opportunity For Investors

As the November 2024 election draws near, the election outcome will profoundly affect the financial markets. Whether Donald Trump or Kamala Harris wins the presidency, each administration will bring distinct policies creating investment opportunities and potential risks for investors. With a divisive political landscape, it is crucial to understand how these potential outcomes can shape the stock market and your portfolio strategy.

Let’s break down the key sectors that stand to gain from a Trump or Harris presidency and explore the risks investors should be aware of heading into this election outcome.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.