Inside This Week’s Bull Bear Report

- FOMC Pivot Sends Stocks Soaring

- How We Are Trading It

- Research Report – Wall Street Analysts Are Optimistic For 2024

- Youtube – Before The Bell

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

Administrative Note:

Last week, I noted that I was traveling this weekend for business, and there would be NO newsletter. However, with the FOMC pivot on Wednesday, I wanted to provide a brief market trading update. This analysis was written early Friday, with Thursday’s closing data, so some data points will not be of the week’s ending. The full newsletter will return next weekend.

Market Review And Update

Last week, we noted that the current rally was exceptionally extended, and corrective or consolidative action was necessary. That consolidation ended last Thursday, to wit:

“While the market struggled to advance early in the week, on Thursday and Friday, markets climbed to set new closing highs for the year, as shown. However, the combination of overbought conditions and excess bullish sentiment limited gains from weaker-than-expected economic reports that should keep the Federal Reserve at bay next week.”

In that newsletter, we also made a forecast for this week’s FOMC meeting:

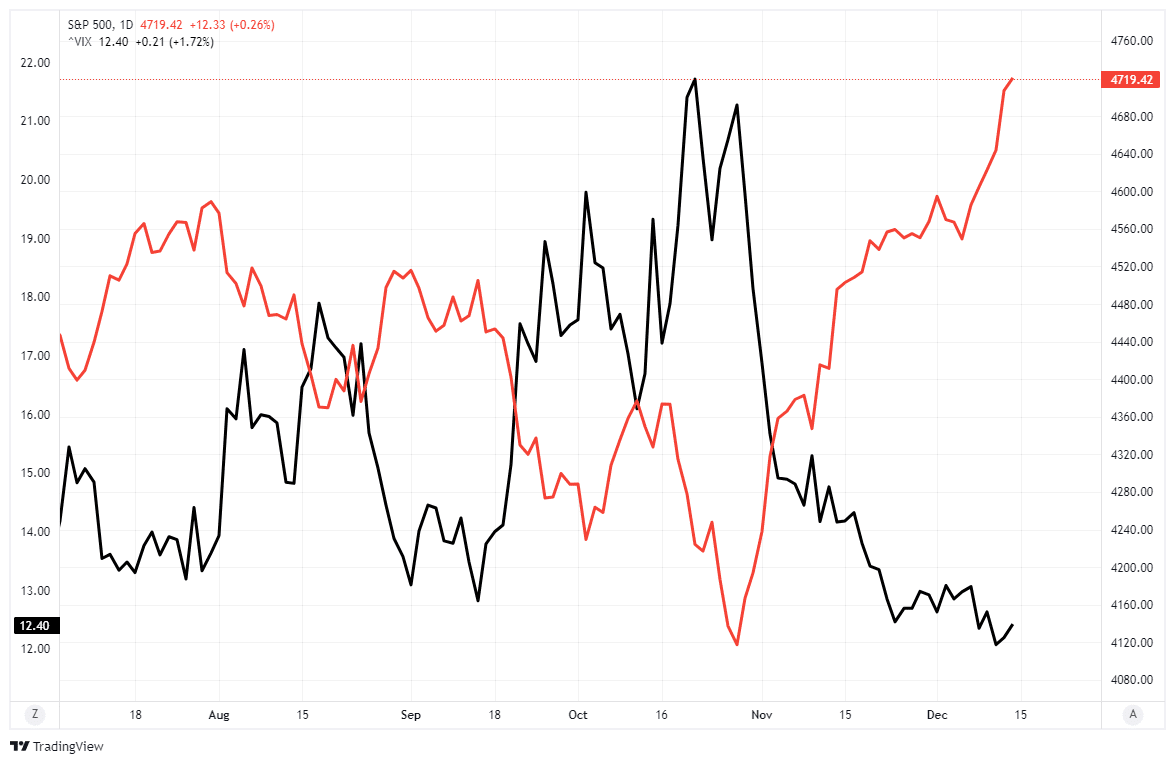

“The jobs report yesterday was weak across the board, which will likely keep the Federal Reserve on hold for now, and next week is the inflation report and the last FOMC meeting for the year. With volatility at extremely low levels, as shown, a hot CPI report or a “hawkish message” from the Fed could cause stocks to stumble.”

That was wrong, as noted by Goldman Sachs:

“Today’s press conference was an endorsement of the Waller view that inflation is moving lower and that the Fed can pivot to a less restrictive policy stance. There was no change to the median neutral rate still of 2.5% – perhaps one thing to call out is by 2026 they are still above that at 2.9% – other years have come down because starting place is 25bps lower. Forward guidance was watered down: instead of ‘extent of policy firming’ we got ‘extent of ANY policy firming’. *POWELL: ADDED ‘ANY’ AS ACKNOWLEDGEMENT OF AT OR NEAR PEAK RATE.“

As we will discuss, the FOMC pivot sent stocks soaring and bond yields lower, as the message was more dovish than even the bulls expected. Notably, as measured by the volatility index, any bearishness was crushed.

The “Santa Powell Rally” came early this year.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

The Santa Powell Rally As The FOMC Pivots

On Wednesday, Jerome Powell shocked the markets with a dovish turn in policy. As noted in the Daily Market Commentary:

“At yesterday’s FOMC meeting, Jerome Powell used the balance of risks between inflation and recession to justify the pause of rate hikes. He notes several times they are still prioritizing getting inflation to its target. At the same time, the Fed remains concerned that the lag effects of the sharp rate increases have yet to impact the economy fully. As Powell states, the “current balance of risks” makes a pause the logical stance. Looking ahead, might they cut rates prematurely to avoid a recession, albeit at the risk of upsetting the bond markets and possibly reigniting inflation? Such is the tightrope the Fed is walking.”

The Fed minutes were essentially unchanged from the prior meeting in November. However, they did acknowledge growth has slowed, and inflation has eased. This December meeting included the Fed’s quarterly economic and rate projections and comparisons from the last forecast in September. As shown below, the Fed’s median estimate is for THREE 25bps rate cuts next year. One participant sees rates falling 1.25% by the end of next year. The minutes and projections are more dovish than the market expected.

Jerome Powell’s press conference did nothing to dispel the slightly dovish tilt within the minutes and projections. Per Powell: “We are likely at or near the peak rates for this cycle.” Powell’s statements and the FOMC projections were the most significant change. As noted by Nick Timiraos in a recent tweet.

Note that in the FOMC’s projections, not only is economic growth expected to slow sharply next year, but the Federal Funds rate is projected to drop by roughly 0.80 basis points.

Of course, such was surprising, at least to us, given the extremely sharp decline in the monetary policy conditions index. That reversal in monetary conditions, which began in October 2022, corresponds with the rally since then.

What surprised us, more than anything, is that the FOMC seems to have given up its fight against inflation. The decline in financial conditions will boost economic activity and consumer sentiment, which historically supports higher inflation rates.

Such was why we expected a more hawkish tone from the Federal Reserve. However, that did not materialize.

Bullish Formation

As we have discussed recently, the surge in the market this week has pushed it into very short-term overbought conditions. At the same time, investor sentiment has reached extreme levels. Such continues to suggest that a pullback to some support level is likely. Any corrective action will provide a better entry point to add portfolio equity exposures. The deviation above the 50-DMA and 200-DMA, with the Relative Strength Index extended, precedes corrective actions.

Notably, our weekly Technical Composite index is approaching 90, which is generally associated with market corrections.

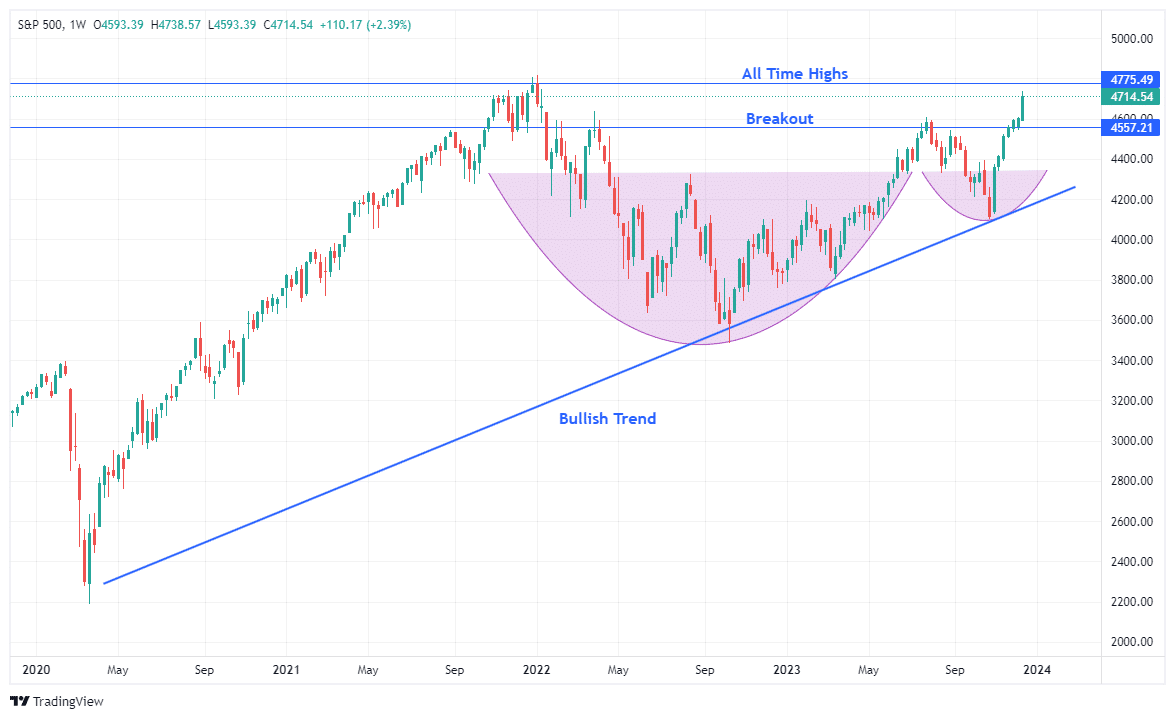

However, while a correction in the short term is likely, as we head into 2024, the market has formed a very bullish formation, which suggests higher asset prices. The decline from the January 2022 peak and the October trough created a “Cup And Handle” formation. As defined by Investopedia:

“The pattern was first described by William J. O’Neil in his 1988 classic book on technical analysis, How to Make Money in Stocks. A cup and handle price pattern on a security’s price chart is a technical indicator that resembles a cup with a handle, where the cup is in the shape of a ‘u’ and the handle has a slight downward drift. The cup and handle pattern is considered a bullish signal, with the right-hand side of the pattern typically experiencing lower trading volume. The pattern’s formation may be as short as seven weeks or as long as 65 weeks.”

That pattern seems quite evident in the following weekly chart of the S&P 500 index. With the breakout of the “cup and handle” formation in place, an attempt at all-time highs seems to be the logical next step. Any subsequent correction to relieve overbought conditions should maintain the bullish trend line from the March 2020 lows.

Of course, with the FOMC pivot in place and markets looking more bullish into next year, the next question is where to invest when the market gives you a buyable opportunity.

What Sectors And Markets Tend To Perform Best During Rate Cuts?

Some apparent candidates should benefit from the FOMC pivot to lower interest rates, which should help stabilize economic activity.

The most obvious is the broad market index, as measured by the S&P 500 index. As discussed in “Markets Front Running Rate Cuts,“ over the last 13 years, investors have been trained that stocks rise when the FOMC pivots to a more accommodative policy. To wit:

“However, since 2008, the Fed has trained investors. Any financial or recessionary event jeopardizing the markets would be met with rate cuts and accommodative policy. That training was completed with the Fed’s response to the “pandemic-era shutdown” that led to massive monetary and fiscal interventions.”

While the S&P 500 previously declined during the FOMC pivot, as the realization of financial or economic pressures arose, as noted, investors are now front-running the market on expectations of more accommodative policies.

Another major market that will likely benefit from an FOMC pivot was discussed by Michael Lebowitz Friday morning:

“Small-cap stocks tend to be more interest-rate sensitive than large-cap stocks. If rates are indeed on a path much lower and Santa Powell navigates the rare soft landing, these stocks may continue to outperform the S&P 500. However, it may be worth waiting to buy or add to small-cap stocks. A short-term pullback is likely in the cards.”

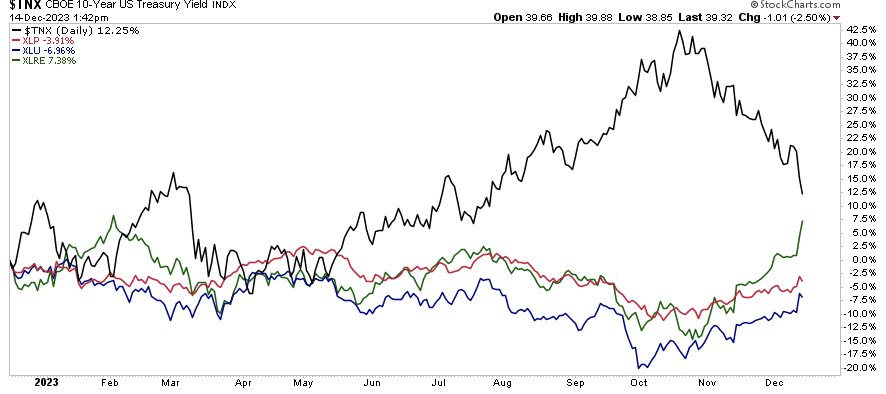

From a sector perspective, the choices are pretty obvious. A lower interest rate environment will benefit those sectors most beaten up by a high-interest rate environment. As shown below, Utilities, Real Estate, and Consumer Staples are likely candidates to lead the way. With the FOMC pivot to help support a slower economic environment, interest rate-sensitive areas should benefit. Staples and dividend-paying stocks also tend to weather economic slowdowns better.

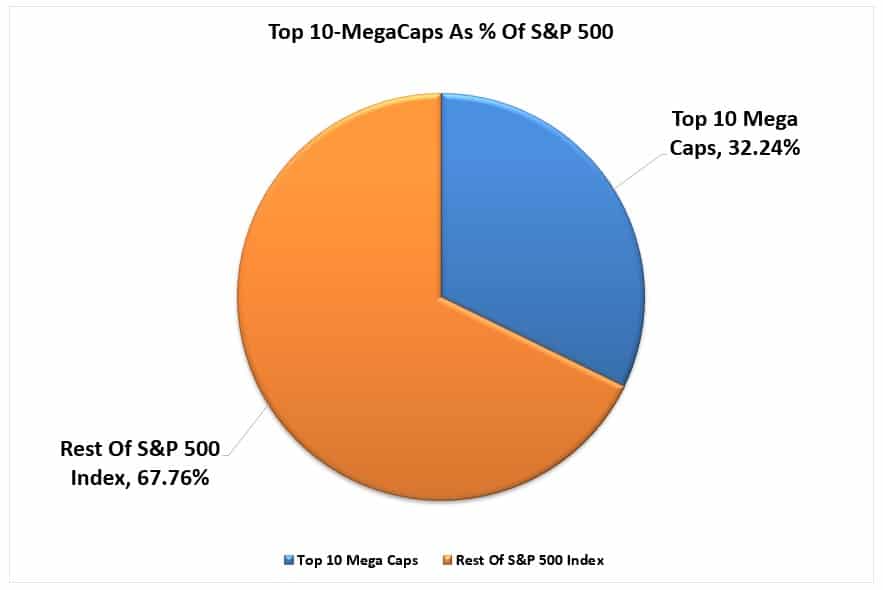

Lastly, and while not entirely unexpected, Technology and Consumer Discretionary should continue to perform well next year for two reasons. First, of all major market sectors, Technology still maintains the highest expected earnings growth rates in a disinflation environment. Secondly, as investors chase the markets, the continued inflows into index ETFs, as discussed previously, will continue to push an outsized portion of those flows into the top 10 stocks.

Oh, and we would be remiss if we didn’t remind you that as economic growth falls and the Fed cuts rates, long-dated Treasury bonds will likely provide outperformance over stocks in terms of total return. As shown, bonds, like stocks, are extraordinarily overbought and need a short-term correction. However, in 2024, the technical upside remains appealing.

However, before adjusting your portfolio, realize the markets are extraordinarily exuberant and overbought. As such, I am reprinting our rules from last week to guide you through the steps to reposition your portfolio for the FOMC pivot.

Rules For “Santa Powell Rally”

If you are long equities in the current market, rebalancing risk is manageable.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Notice, nothing in there says “sell everything and go to cash.”

Remember, our job as investors is pretty simple – protect our investment capital from short-term destruction so we can play the long-term investment game. Here are our thoughts on this.

- Capital preservation is always the primary objective. If you lose your capital, you are out of the game.

- Seek a rate of return sufficient to keep pace with the inflation rate. Don’t focus on beating the market.

- Keep expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4%)

- Higher rates of return require an exponential increase in the underlying risk profile. This tends to never work out well.

- You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

- Portfolios are time-frame specific. If you have a 5-year retirement horizon but build a portfolio with a 20-year time horizon (taking on more risk), the results will likely be disastrous.

As discussed recently, there is a wide range of potential outcomes, based on valuations, in 2024. No one knows with any certainty what next year will hold. However, by focusing on risk controls and the technical underpinnings, we can safely navigate the waters to safety.

Have a great week.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates

We have set up a separate channel JUST for our short daily market updates. Please subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our YouTube Channel To Get Notified Of All Our Videos

Bull Bear Report Market Statistics & Screens

Will Return Next Week

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

No Trades This Week

Lance Roberts, C.I.O.

Have a great week!