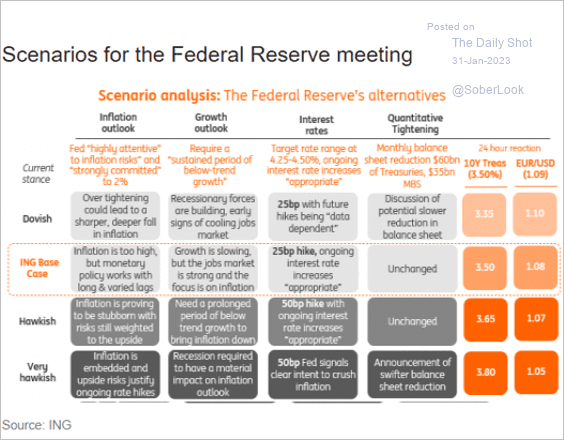

At 2 pm ET, the FOMC releases its Fed Funds rate decision, and Powell will hold a press conference afterward. To help guide you through what might be a volatile afternoon trading session, we present ING’s FOMC cheat sheet, followed by our thoughts. ING presents four scenarios for how the Fed characterizes inflation, growth, interest rates, and QT. As shown to the right of the scenarios, the FOMC cheat sheet also includes expectations for how the various scenarios could play out in the bond and currency markets.

We think the Fed will land somewhere between the base case and hawkish. Here are our expectations on the policy factors:

- Inflation- The Fed will claim it remains too high but show some optimism it has peaked. However, they may offer caution due to concern for a rebound in inflation.

- Growth- ING’s base forecast aligns with our expectations. There are very few indicators the jobs market is weakening.

- Interest rates- A 25bps hike is very likely, and discussion of one or two more at the next two meetings. More importantly, they will stick with their call that Fed Funds stay at their terminal rate for the remainder of 2023.

- Balance Sheet- Like ING, we highly doubt they make any changes.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended Jan. 27 (7.0% prior)

- 8:15 a.m. ET: ADP Employment Change, January (170,000 expected, 235,000 prior)

- 9:45 a.m. ET: S&P Global U.S. Manufacturing PMI, January Final (46.8 prior)

- 10:00 a.m. ET: Construction Spending, month-over-month, December (0.0% expected, 0.2% prior)

- 10:00 a.m. ET: ISM Manufacturing, January (48.0 expected, 58.4 prior)

- 10:00 a.m. ET: JOLTS Job Openings, December (10.300 million expected, 10.458 million prior)

- 2:00 a.m. ET: FOMC Rate Decision (Lower Bound), Feb. 1 (4.50% expected, 4.25% prior)

- 2:00 a.m. ET: FOMC Rate Decision (Upper Bound), Feb. 1 (4.75% expected, 4.50% prior)

- 2:00 a.m. ET: Interest on Reserve Balances Rate, Feb. 2 (4.68% expected, 4.40% prior)

- WARDS Total Vehicle Sales, November (15.50 million expected, 13.31 prior)

Earnings

Market Trading Update

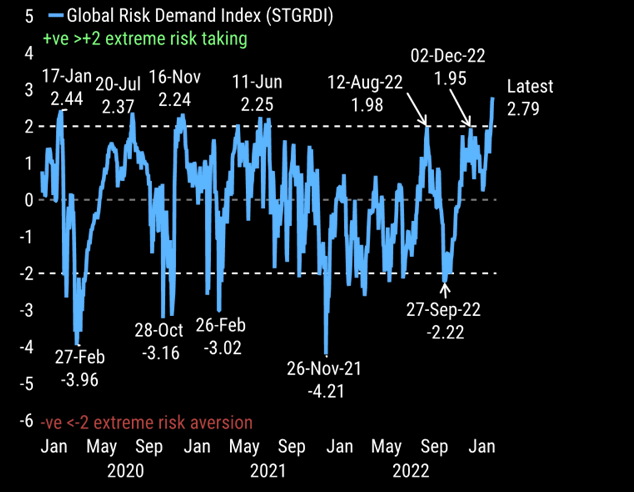

Time for a dollar reversal? Since the beginning of the year, commodities like gold and emerging markets have been strongly outperforming due to the drop in the U.S. dollar. However, now that the dollar decline has gotten very extended, it is due for a fairly strong reversal arguing for profit-taking in the winning trades of January.

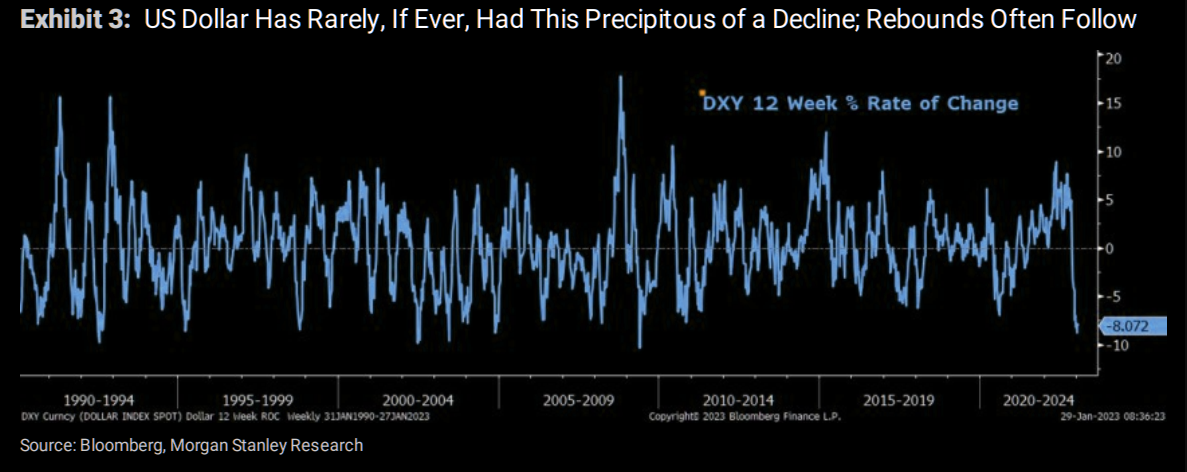

Two more key points that argue for a near-term reversal in the dollar. First, the 12-week rate of change is extreme, and history suggests a rebound will follow.

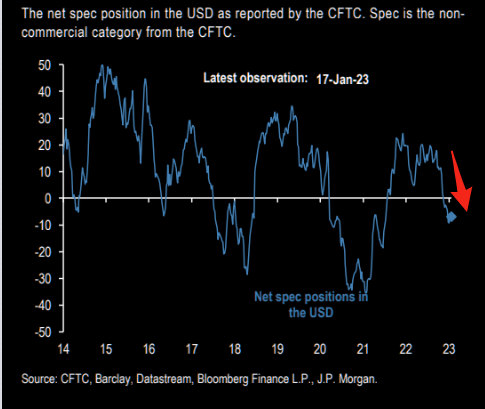

Furthermore, just as with the stock market, when everyone is on the same side of the trade, such provides the fuel for a significant reversal. Currently, there is a decent short position against the dollar.

Why is this important? Because the dollar decline has fueled the asset chase since December from gold to commodities, to emerging markets, and risk assets in general. As shown, the Morgan Stanley “Global Risk Demand Index” (STGRDI) has risen sharply and is nearing +3 standard deviation and is significantly higher than the reading on the 12th of August (4 days before the markets peaked).

If the dollar does reverse, we would also expect to see dollar-denominated trades reverse.

Don’t forget to take profits.’

UPS Struggles While Exxon Prints Money

UPS and Exxon are both solid barometers of the economy. When the economy runs strong, commerce and traffic are on the rise, often boosting profits for companies like UPS and Exxon.

Yesterday, Q4 revenues at UPS came up short of expectations, although its EPS beat slightly on better margins. The company guided 2023 revenue guidance lower as well. Despite the weak revenue and poor outlook, the stock rose. Fueling the gain, the company authorized up to $5 billion in stock buybacks and raised its dividend.

Exxon, on the other hand, bolstered by high oil prices and strong demand, posted a record annual profit of $59 billion. The profit far exceeded the prior high from 2008 ($45.2 billion). Revenues fell short of estimates, but EPS was better than expected. Unlike UPS, XOM did not accelerate share buybacks.

The companies’ earnings reports point to the economy’s confusing state. While Exxon is recording record profits, revenues are declining at UPS, despite increasing the prices they charge their customers. Some sectors and bits of economic data point to a recession, while others point to robust growth. The graph below shows the stunning divergence between the performance of the companies stock prices.

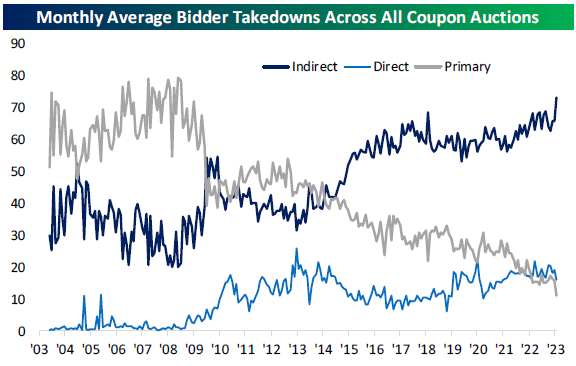

Treasury Sales are Red Hot

Bespoke Investmentment Group put out a great piece showing that the U.S. Treasury auctions in January were well-demanded by investors. Per Bespoke, January was a record month for Treasury sales. Every auction and bond reopening occurred at a lower yield than where the bond was trading before the respective auctions. The second graph below shows that the auctions occurred 2.3bps below the then-market yield. Such is much better than any month in at least ten years. Indirect bidders, often foreign investors, bought approximately 75% of January’s issuance. The graphs and commentary below are all courtesy of Bespoke.

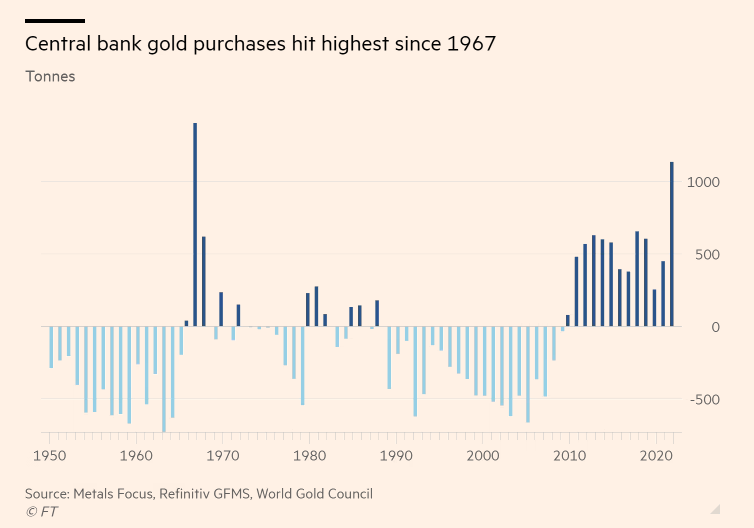

Foreigners are Buying Gold

The FT notes that the central bank purchases of gold in 2022 rose to a level last seen in 1967. Why? The FT quotes an analyst that claims that a “lack of counterparty risk” as compared to currencies “under the control of foreign governments” was a key reason. In other words, after the U.S. froze Russia’s dollar reserves, other central banks wanted to move some of their assets somewhere they would be out of reach from other governments.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.