The FOMC minutes show Fed members collectively downgraded their economic forecast for 2023. Instead of the “soft landing” we have been warned about for the last year, the Fed is downgrading its outlook to a “mild recession” in the second half of the year. Per the FOMC minutes:

“For some time, the forecast for the U.S. economy prepared by the staff had featured subdued real GDP growth for this year and some softening in the labor market. Given their assessment of the potential economic effects of the recent banking-sector developments, the staff’s projection at the time of the March meeting included a mild recession starting later this year, with a recovery over the subsequent two years.”

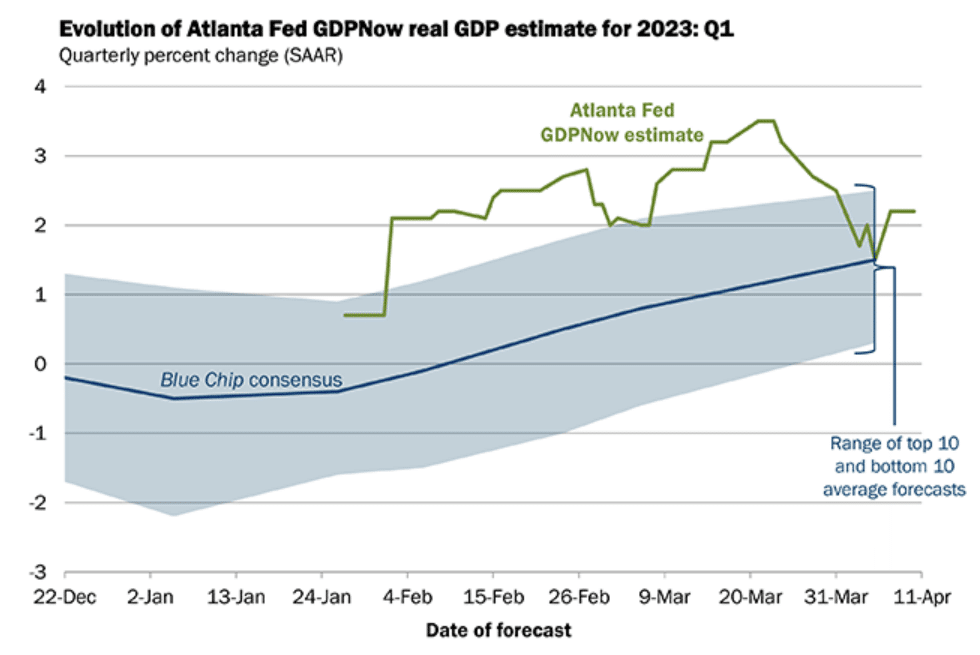

The economic downgrade to mild recession should not be overly surprising. The Fed downgraded its 2023 GDP forecast (dot plots) at the March meeting to a paltry 0.4%. Given the first quarter is likely running around +2.0%, per the Atlanta Fed GDPNow, a negative quarter or two is mathematically required to achieve their mild recession target. A second important line from the statement reads: “Regarding prices for core services excluding housing, participants agreed that there was little evidence pointing to disinflation in this component.” Despite their call for a mild recession, rate cuts may not come nearly as fast as market expectations because inflation remains sticky.

What To Watch Today

Economy

Earnings

Market Trading Update

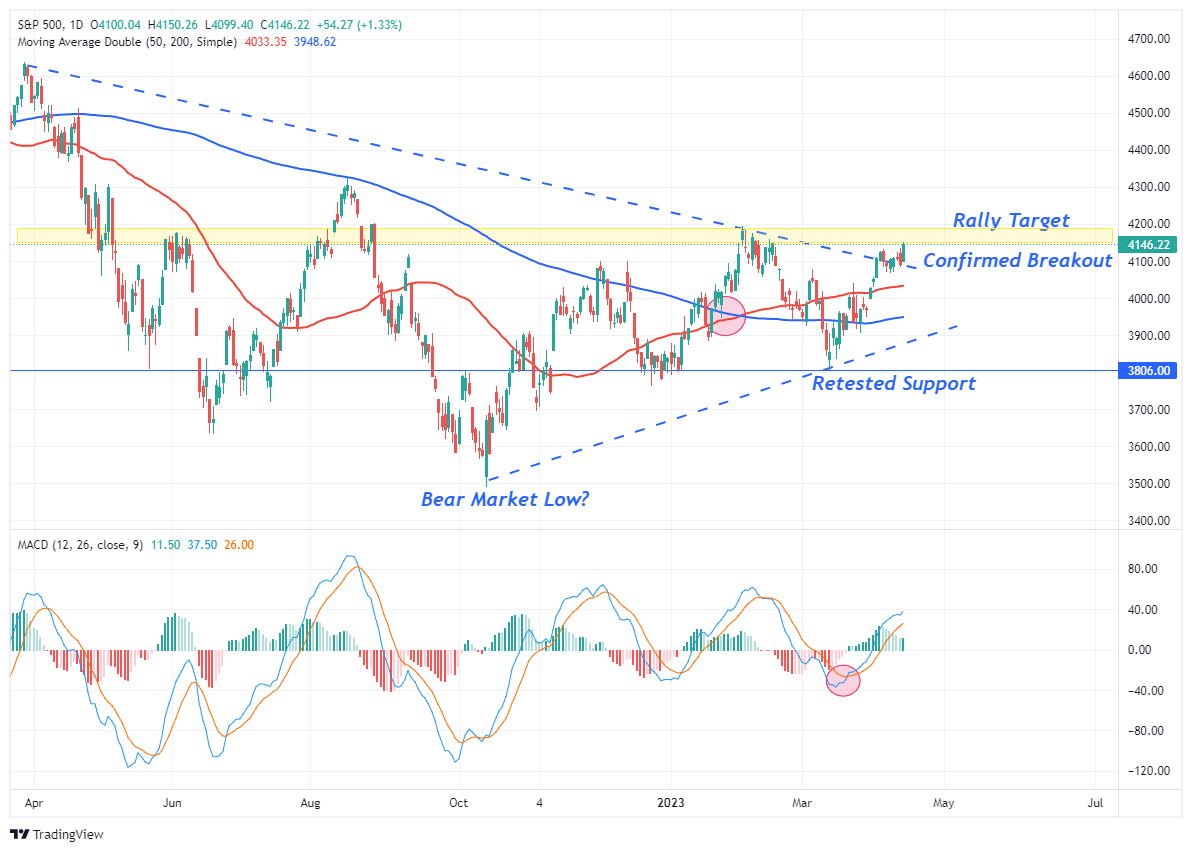

After Wednesday’s softer CPI report, yesterday’s weak Producer Price Index (PPI) sent investors scrambling back into stocks to front-run the Federal Reserve in hopes of a “pause” at the upcoming meeting. Furthermore, earnings season officially begins today, but over the next two weeks will be a deluge of corporate reports. Their earnings growth and profitability outlook will be key in sustaining the current rally.

From a technical view, the market has officially tested and held the downtrend line from the April highs. Yesterday’s breakout of that consolidation suggests higher asset prices near term. We will likely look to increase our trading market exposure near term, as April and May tend to be seasonally strong. Despite a plethora of headlines to the contrary, the market has done nothing wrong to warrant a more “bearish” view. Maintain equity exposure for now and look for opportunities to increase that exposure near term.

Jobless Claims

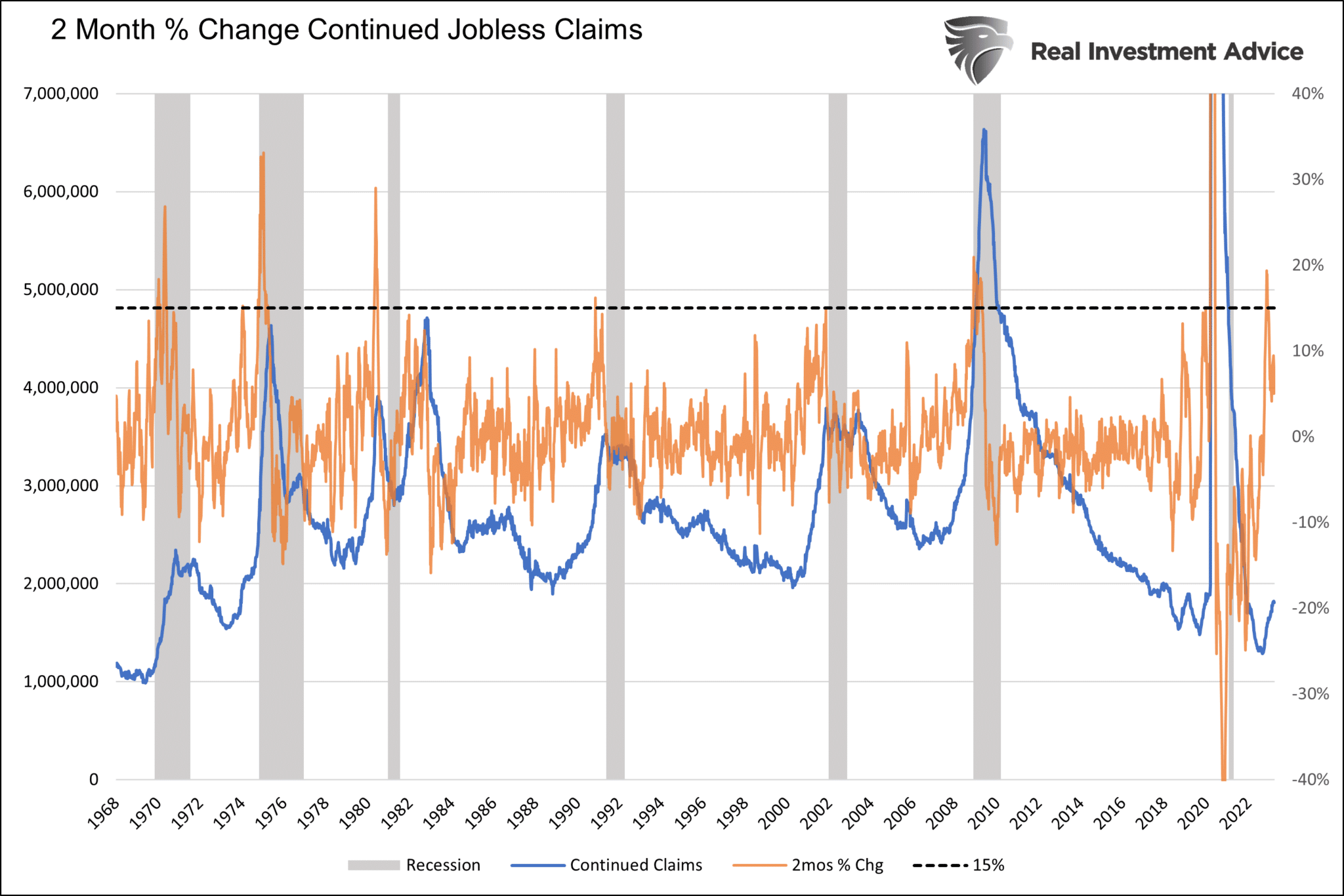

Last week, jobless claims came in at 239k, well above the sub-200k rate of the prior months. However, more concerning, last week, the BLS upwardly revised the prior two months by about 50k each. This week’s data further affirms softening of the labor market. Continuing Claims also point to weakness and increased odds of a recession. The graph below shows that continuing jobless claims, those people that filed claims and cannot find a new job, are increasing but remain well below prior troughs. Per the graph, every time continued claims rose by 15% or more in two months, a recession was in progress or was about to start.

Bullish Bonds But Supply Is Worrisome

We are bullish bonds due to our economic outlook and belief that inflation will continue lower. However, we are concerned that the Treasury’s increased issuance and QT will create a headwind for lower yields. We do not believe the headwind is enough to prevent lower yields, but it will likely slow their progress. The Fed is reducing its balance sheet by $95 billion a month. As a result, $95 billion of bonds need to find a new home every month. Further, that $95 billion is on top of a larger-than-expected $378 billion deficit last quarter. Once the debt cap limit is solved, Treasury issuance will increase to fund the widening deficit. Lastly, remember that the government’s interest expense is up by over $200 billion per year due to higher interest rates.

Retail Sales- What to Expect

Retail Sales, accounting for about two-thirds of economic activity, is expected to show a 0.4% decline in March following a similar decline in February. The graph below, courtesy of @sophiaknowledge, shows that another, more robust, measure of consumer spending is also slowing rapidly year over year. Johnson Redbook is a proprietary index measuring weekly changes in retail sales. The index is often a leading indicator of consumer spending.

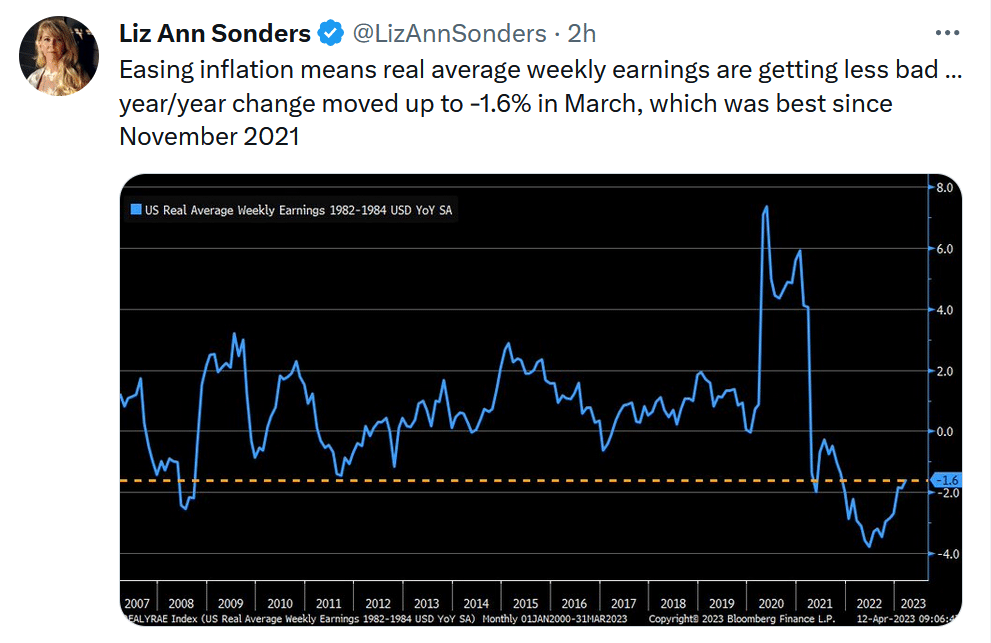

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.