Yesterday’s Wall Street Journal led with a troubling article on Europe’s economy. Their article, Europeans are Becoming Poorer, leads off as follows: “The French are eating less foie gras and drinking less red wine. Spaniards are stinting on olive oil. Finns are being urged to use saunas on windy days when energy is less expensive. Across Germany, meat and milk consumption has fallen to the lowest level in three decades, and the once-booming market for organic food has tanked.” The combination of an aging population, troubling debt levels, and a desire for fewer working hours has stymied productivity and economic growth for quite a while. The war in Ukraine, high-interest rates, and inflation appears to be Europe’s economic tipping point.

Per the article: The eurozone economy grew about 6% over the past 15 years, measured in dollars, compared with 82% for the U.S., according to International Monetary Fund data. That has left the average EU country poorer per head than every U.S. state except Idaho and Mississippi, according to a report this month by the European Centre for International Political Economy. Negligible economic growth and poorer citizens are highly problematic considering the extreme debt levels that face many European countries. Unfortunately, what is happening in Europe should concern Americans. Not only does Europe purchase a lot of our goods, but more troubling, we face similar economic headwinds. The WSJ graphs below show America doesn’t appear to exhibit Europe’s economic difficulties. However, similarly high debt levels, weakening productivity growth, and an aging population will eventually lead us down the same path if substantive economic and monetary policy changes aren’t made.

What To Watch Today

Earnings

Economy

Market Trading Update

The market continues to drift higher with the MACD “buy signal” in place. With earnings season kicking into full gear today with regional banks set to report, we should get a good taste of whether financial concerns remain. The market is overbought, and many individual stocks are extremely extended. However, momentum and a need to “catch up” with the market are pulling assets in, providing a bid under the markets. This can last a while, so investors will need patience to wait for a pullback to add further equity exposures.

Are Consumers and Corporations Preparing for Problems?

The chart below from Ian Harnett of Absolute Strategy Research shows the robust correlation between the unemployment rate and changes in private sector balances. When private sector balances rise, i.e., consumers increase their savings and or corporations reduce their investments, economic growth tends to slow, and unemployment rise.

Assuming the correlation holds, a significant rise in the unemployment rate within a year should be expected.

What Happened to Zoom?

As shown below, the price of Zoom stock has completed a classic bubble pattern. As is typical, it now sluggishly trades in a directionless tight range around pre-pandemic levels. Is Zoom (ZM) worth taking a chance on? To help answer the question, consider the bullet points below.

- Sales grew over 5x due to the pandemic, but sales growth has slowed considerably over the last year.

- Its once enormous price-to-sales ratio (165) has fallen sharply but remains relatively high at 4.85.

- Despite growing sales, earnings have fallen in half since peaking in Q4 2020.

- Like Price to Sales, its forward Price to Earnings is still costly at 54.

- Zoom became a household name during the pandemic and garners about half of the market for video conferencing in the U.S. However, competition from Google Meet, Microsoft Teams, and others erodes their dominant market share.

With considerably slowing growth and intense competition, Zoom faces many hurdles. Further, while its stock price has collapsed and valuation ratios are more rational, the stock still appears expensive. Barring new technologies or other earnings-enhancing factors we are not considering, Zoom remains pricey. The grind to nowhere may continue.

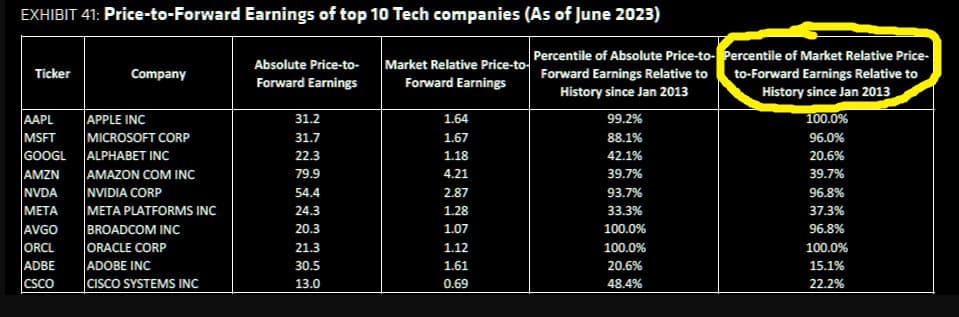

Tech Valuations

The following table by Bernstein shows absolute and relative price-to-forward earnings ratios (P/Ef) for the top ten tech companies. It also provides a 10-year context for the valuations. For example, Apple is trading at its highest P/Ef ratio since 2013, at 31.2. Its P/Ef ratio divided by that of the S&P 500 (1.64) is a hair from the richest it has been in the last ten years. Apple, Microsoft, NVIDIA, Broadcom, and Oracle are expensive. Despite the impressive run-up in tech since last October, relative bargains remain to be owned. Google and Adobe, for instance, are trading with a P/Fe in the lowest quintile of the last ten years.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.