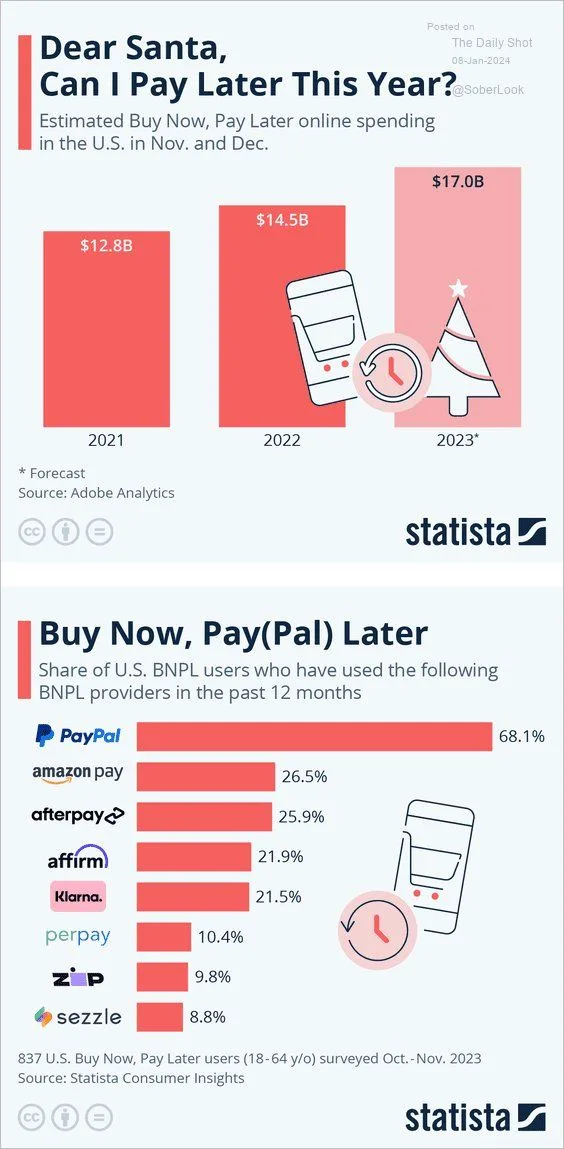

Since 2022, credit card debt has grown 10% annually to a record high of $1.08 trillion. That is double the growth rate prevailing before the pandemic. As banks tighten lending standards and an increasing number of credit card holders max out their cards, some consumers are turning to buy now, pay later loans. Buy now, pay later loans are a little different than credit cards. Unlike credit cards, consumers pay some of the purchase price at checkout. Further, they agree to a series of payment installments. Often, the loan is paid off in three months. Buy now pay later loans typically do not charge interest unless payments are delinquent. Late or rescheduled payments can be costly, typically around 25% of the purchase value. The Statista graphs below show that the amount of buy now pay later loans is relatively small but growing quickly.

The economy continues to hum, but the growth of buy now pay later loans leads us to believe that many individuals, especially lower-income consumers, are in poor financial shape. Per the St. Louis Fed, the credit card delinquency rate is now 3%. Such has been rising steadily since troughing at a record low in 2021. Not only has it turned up and trending higher, but 3% is the highest rate since 2012. The proliferation of consumer credit is not necessarily a problem today. However, if unemployment rises, consumer credit will falter and pressure bank profits and ability to lend. The other factor to consider is that buy now pay later borrowers are now paying off their Christmas purchases and, therefore, consuming less. Such will weigh on economic activity over the next few months.

What To Watch Today

Earnings

Economy

Investing Summit: Early Bird Registration Available Now

January 27th, we are hosting a live event featuring Greg Valliere to discuss investing in the 2024 presidential election. What will a new president mean for the markets, the risks, and where to invest through it all? Greg will be joined by Lance Roberts, Michael Lebowitz, and Adam Taggart for morning presentations covering everything you need to know for the New Year.

Register now, as there are only 150 seats. The session is a LIVE EVENT, and no recordings will be provided.

Market Trading Update

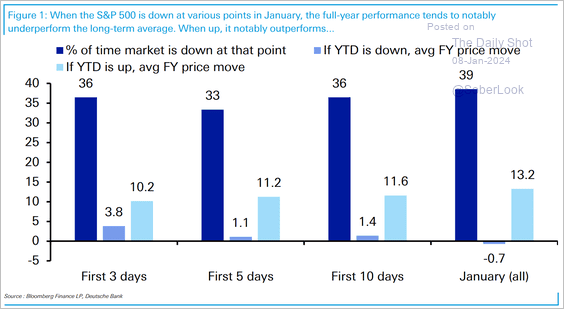

I noted yesterday that the Santa Claus Rally had failed, and the first 5-days of January were at risk. As shown, when the first 5 days of January were negative, which happens 33% of the time, the full-year returns are roughly 1.1%. However, if the full month of January is negative, which happens 39% of the time, the entire year tends to average a negative return.

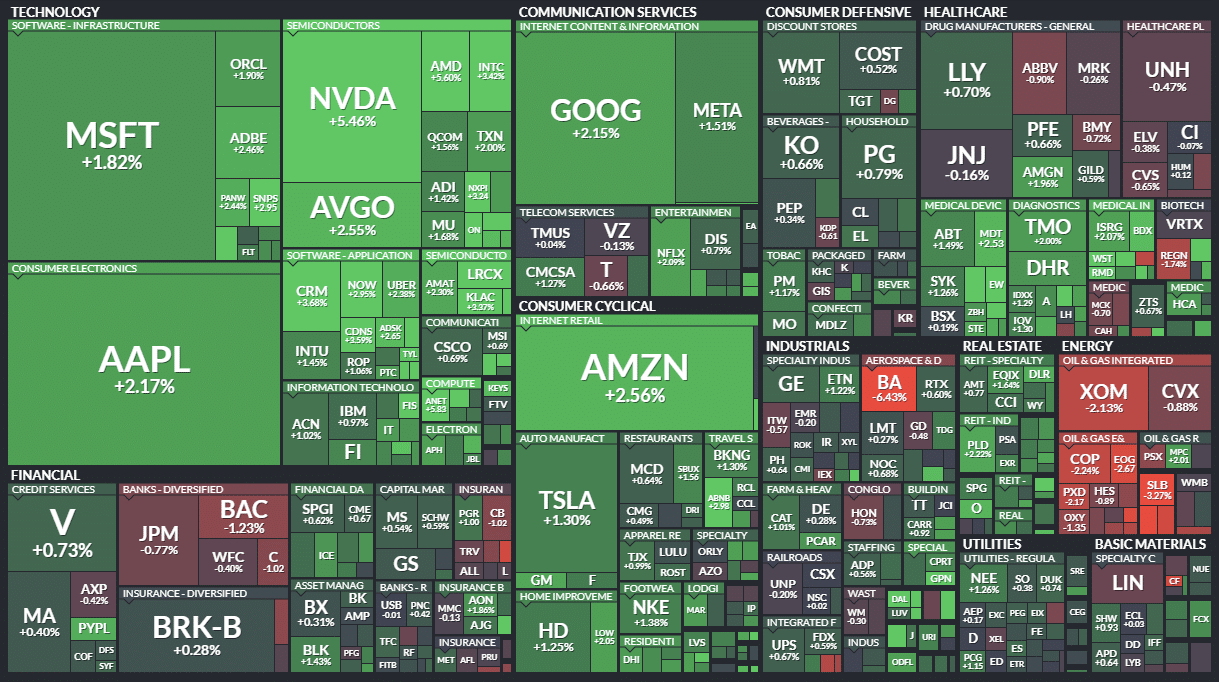

I had stated previously that the market was oversold enough to elicit a bounce, which we got yesterday. That bounce was also enough to push the S&P index into the green for the year, keeping the first 5-days of January positive. Interestingly, the rally was primarily in last year’s leaders as the “Magnificent 7” led the charge once again. You can see this clearly in the heat map of yesterday’s action.

How this month, or year, turns out is anyone’s guess. Everyone initially thought 2023 would be a tough year, but they were dead wrong by the end. Over the next couple of weeks, we will begin to see what markets and asset classes are gaining traction and obtain a better assessment of where to invest capital next. Such is why we continue to hold elevated levels of cash momentarily.

Currently, the market remains overbought and in clear correction territory. However, there are short-term readings reaching more oversold levels, so the bounce yesterday was not unsurprising, and we could see some follow-through. Use bounces for now to rebalance risks accordingly. Once the next set of “buy signals” are triggered, we will have a better entry point to increase equity exposures.

Is Financial Stress Brewing?

If you were to lend us money, would you charge a higher or lower interest rate if we provided collateral in case we failed to make good on the loan?

Typically, a lender is willing to charge a lower interest rate for a collateralized loan as their risk is reduced. Such holds true in the most liquid market in the world, the borrowing and lending of money overnight. Leveraged financial institutions often borrow overnight to ensure they end each day cash-positive. A failure to borrow would force an institution to sell longer-term assets or default.

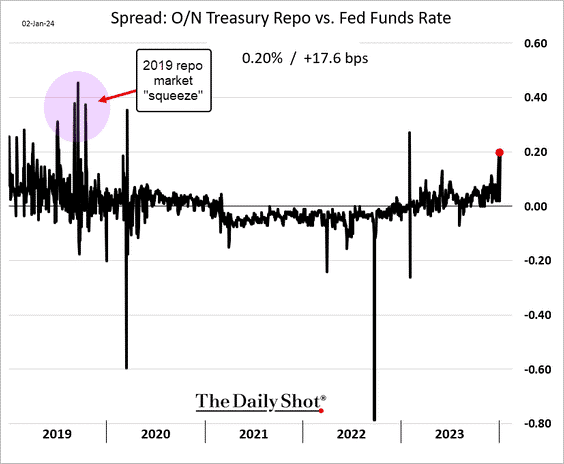

The graph below from our most recent Newsletter, courtesy of the Daily Shot, compares overnight Treasury repo and Fed Funds rates. Fed Funds are uncollateralized loans between banks. Overnight Treasury repo is borrowing and lending amongst banks and non-bank institutional investors for a similar one-day term. However, unlike Fed Funds, the repo loans are collateralized with Treasury securities.

From 2020 through 2023, the difference in the two borrowing rates was negligible. However, the interest charged on collateralized repo trades has recently been about 20bps higher than that on uncollateralized loans. As we note, such is not normal. It points to stress in the financial system.

So why are borrowers paying up to borrow money overnight?

Might There Be A Shortage of Treasury Securities

This is occurring because Treasuries are in short supply or banks are less willing to lend to other non-bank financial institutions. When Treasuries are in short supply, borrowers needing collateral must pay higher than market rates for said collateral. The collateral shortage can be due to a shortage of borrowable Treasury securities, or it can be from an abundance of leverage. Regardless of which, it points to potential stress in the system.

Such stress can occur for short periods and clear up quickly. We typically see such abnormalities at quarter and year ends as borrower and lending needs are often amplified. However, periods of prolonged stress, as we saw in 2019, are meaningful. If you recall, the Fed cut rates by .75% in 2019 despite a robust economy. The culprit, leveraged hedge funds, were unable to borrow money overnight. Had the Fed not provided liquidity, hedge funds would have been forced to deleverage by selling assets, which may have had negative consequences for the asset markets.

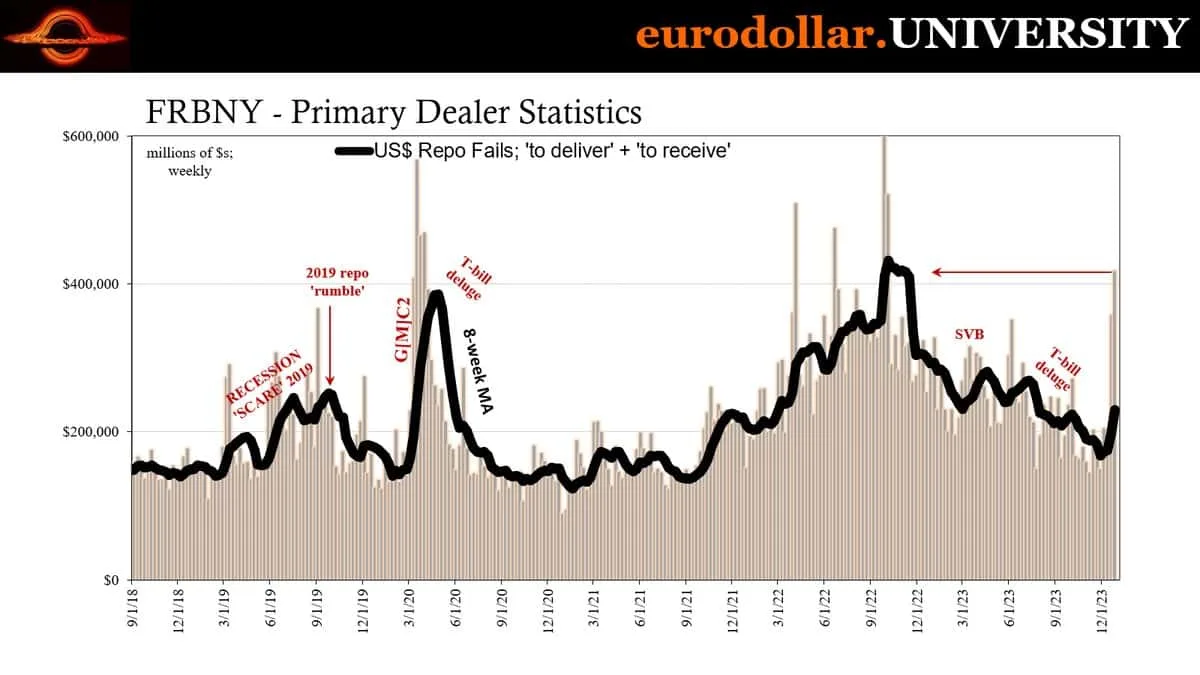

The graph below, courtesy of Jeffery Snider, shows that repo fails are increasing. This is another indication that something is amiss in the financial system.

The current rate discrepancy is just a warning at this point. There is no imminent crisis. But, if the yield difference between repo and Fed Funds remains high or increases further, the Fed will likely be forced to cut rates sooner than many think.

Small Cap Growth Versus Value

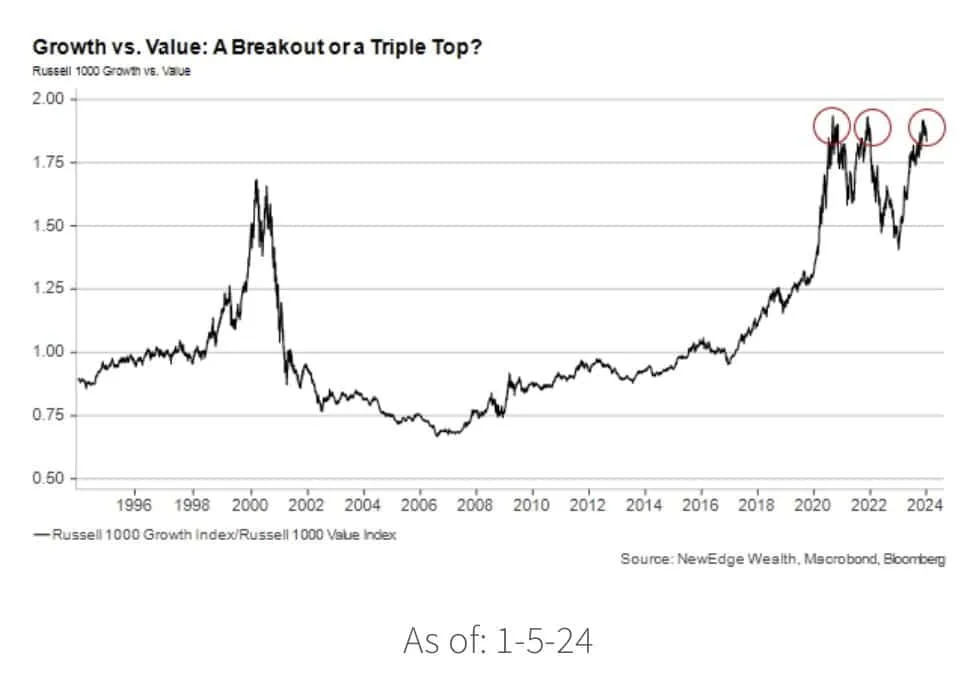

The graph below from Cameron Dawson at New Edge shows that small-cap growth stocks have grossly outperformed small-cap value stocks over the last six to nine months. In the long term, the ratio of growth to value appears to form a triple top. Either growth stocks continue to outperform value stocks, breaking above the pattern, negating the triple top warning, or value stocks outperform growth stocks, and the ratio falls to more normal levels.

The second graph shows the ratio of large-cap growth to value. The ratio rose decently in 2023, but the broader pattern does not compare to the small-cap ratio.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.