Earnings from the big banks were generally good, but the banks expressed concern about the economy. JP Morgan initially traded lower despite beating expectations on earnings and revenues. Of concern, the bank built its loss reserves by $1.4bn. While more than expected, it pales compared to the $18 billion added in 2020. The bank warned its net interest income would be slightly lower than expected. Such is not surprising, given the steeply inverted yield curve. Per Jamie Dimon, courtesy Zero Hedge: “Commenting on the results, JPM CEO Jamie Dimon said “the US economy currently remains strong with consumers still spending excess cash and businesses healthy,” but warned that “we still do not know the ultimate effect of the headwinds coming” with the bank warning of “modest deterioration” in the macro outlook.”

Bank of America (BOA), like JPM, beat on earnings and revenues. They also increased their provision for credit losses and reserves more than was expected. The bank has similar concerns as JP Morgan. Concerning their reserves building: “(it was)primarily driven by loan growth and a dampened macroeconomic outlook.“

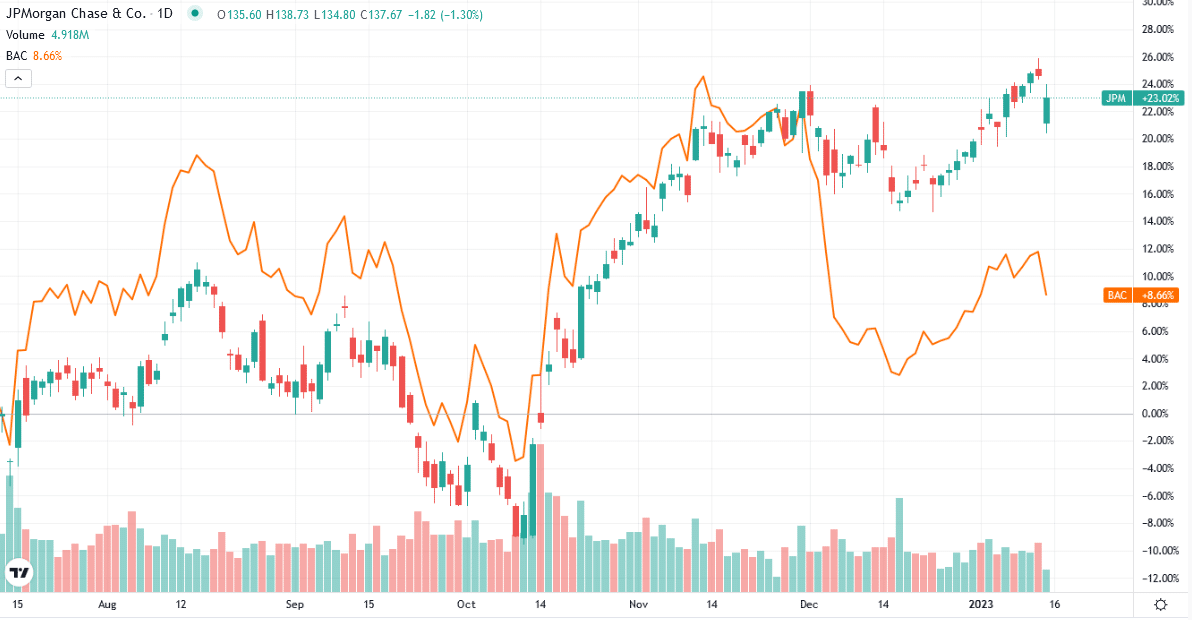

The critical issues in 2023 for banks are the potential for “deterioration” of the economy leading to credit losses and the dampening of net interest income due to inverted yield curves. As we share below, JPM shares have handily beaten BAC over the last six months.

What To Watch Today

Economy

- 8:30 A.M. ET: Empire Manufacturing, November (-8.6 expected, -11.2 prior)

Earnings

The Pain Trade Is Higher

Interestingly, despite the Fed continuing to send warnings, “Fighting the Fed” has become the bull’s new mantra. From one economic report to the next, bullish investors continue to look for any reason to buy stocks in hopes the Fed will pivot soon. Such was the case this past week as the markets rallied again, heading into the much-anticipated inflation report.

However, before we dig further into that topic, a review of this week’s market action reveals some decidedly bullish developments but also some risks.

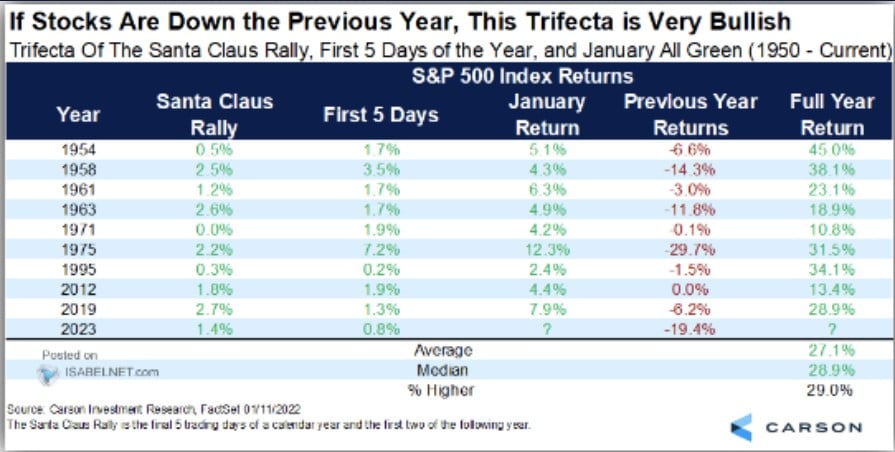

From the bullish side of the ledger, the outlook for 2023 has statistical support for a positive outcome. After having a negative year in 2022, the markets were visited by “Santa Claus,” although very late, and the first 5-days of January turned out a positive return. As the table below shows, there are only a few periods in history where this has occurred, and each yielded positive returns in the following year.

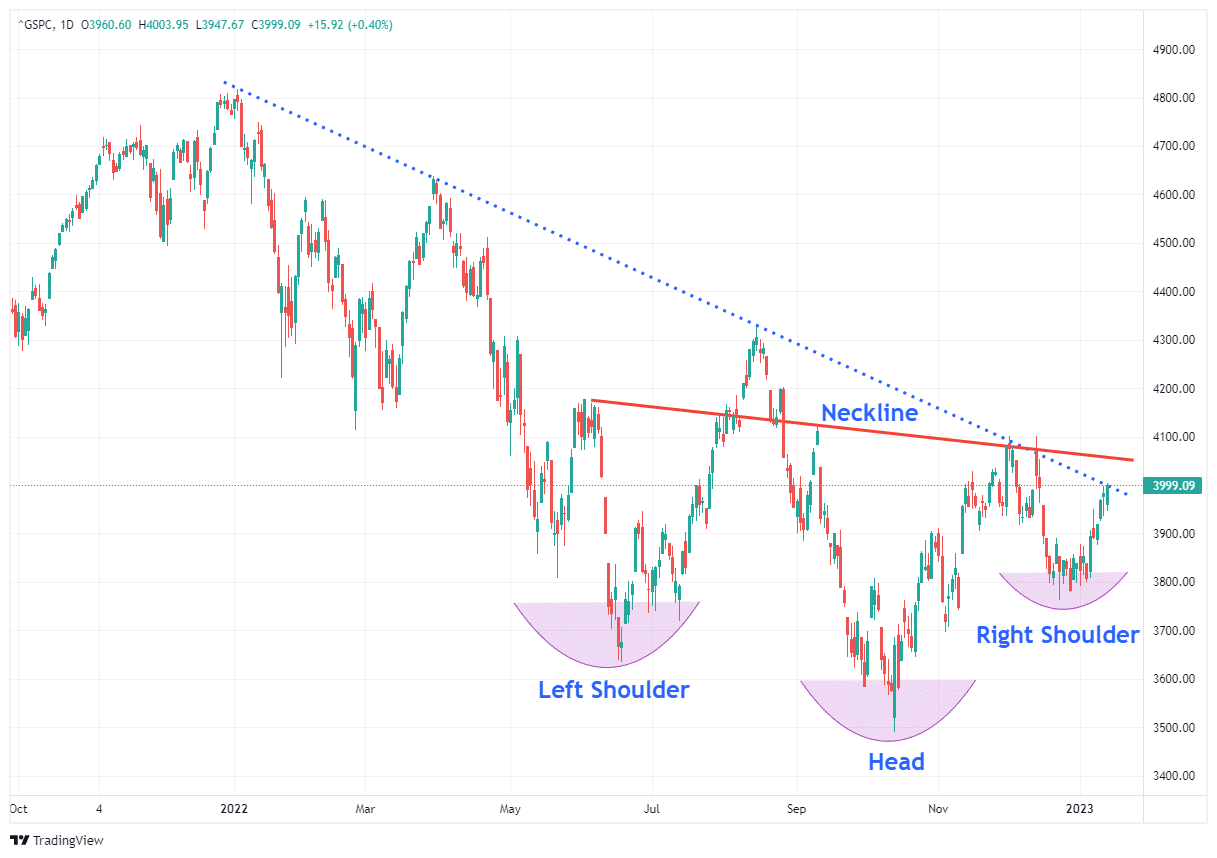

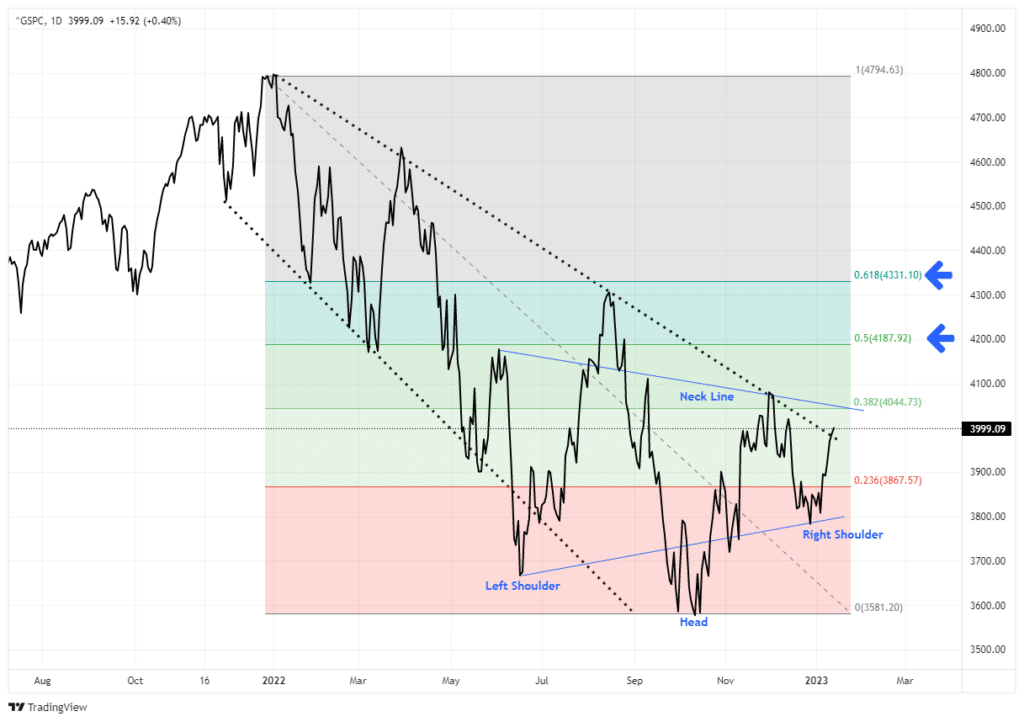

Furthermore, there is also a bullish pattern developing in the S&P 500. The market has recently established a higher low and potentially formed a “right shoulder” of an “inverse head-and-shoulders” technical pattern.

“An inverse head and shoulders, also called a “head and shoulders bottom”, is similar to the standard head and shoulders pattern, but inverted: with the head and shoulders top used to predict reversals in downtrends.

This pattern is identified when the price action of a security meets the following characteristics: the price falls to a trough and then rises; the price falls below the former trough and then rises again; finally, the price falls again but not as far as the second trough. Once the final trough is made, the price heads upward, toward the resistance found near the top of the previous troughs.” – Investopedia

With the market approaching the downtrend line from last year’s peak, and as shown below, a higher low and tightening consolidation suggests a higher move is possible. While the market is short-term overbought, the MACD buy signal continues to suggest the “pain trade” is higher for now.

Importantly, this is just an improving technical picture for the market short-term. The breakouts have not happened yet, and may not. However, given the technical improvement, a break above the downtrend and the 200-DMA will set targets between 4200 (50% retracement) and 4360 (61.8% retracement) of last year’s decline.

While the current “pain trade” appears to be higher, there are still many risks to the market. Such is especially the case as we head into earnings season and the next Fed meeting. Therefore, it is important to remain cautious until the markets declare themselves. We remain overweight in cash, and our bond duration remains short of our benchmark index. However, we will adjust our holdings accordingly if these technical patterns mature.

The Week Ahead

This holiday-shortened week will not be short on potential news events. On Wednesday, we get another round of inflation data with the release of PPI. Economists expect the monthly rate to fall by 0.1%, bringing the annual rate to +6.9%. Also, on Wednesday, analysts expect retail sales to decline by 0.4%. If so, the year-over-year rate will be 5%, or -1.5%, on an inflation-adjusted basis. The Philadelphia Fed will release its survey of business conditions on Thursday.

There will be a host of Fed speakers making headlines. Thus far, they all seem united, thinking the Fed will not cut rates this year. The divergence between the market-implied pivot and the Fed’s stubbornness is noteworthy. The markets will likely react violently, up or down, when that expectation gap closes.

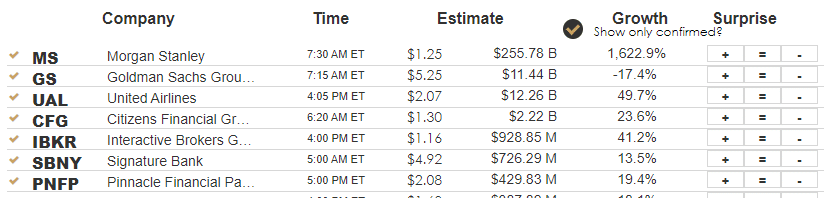

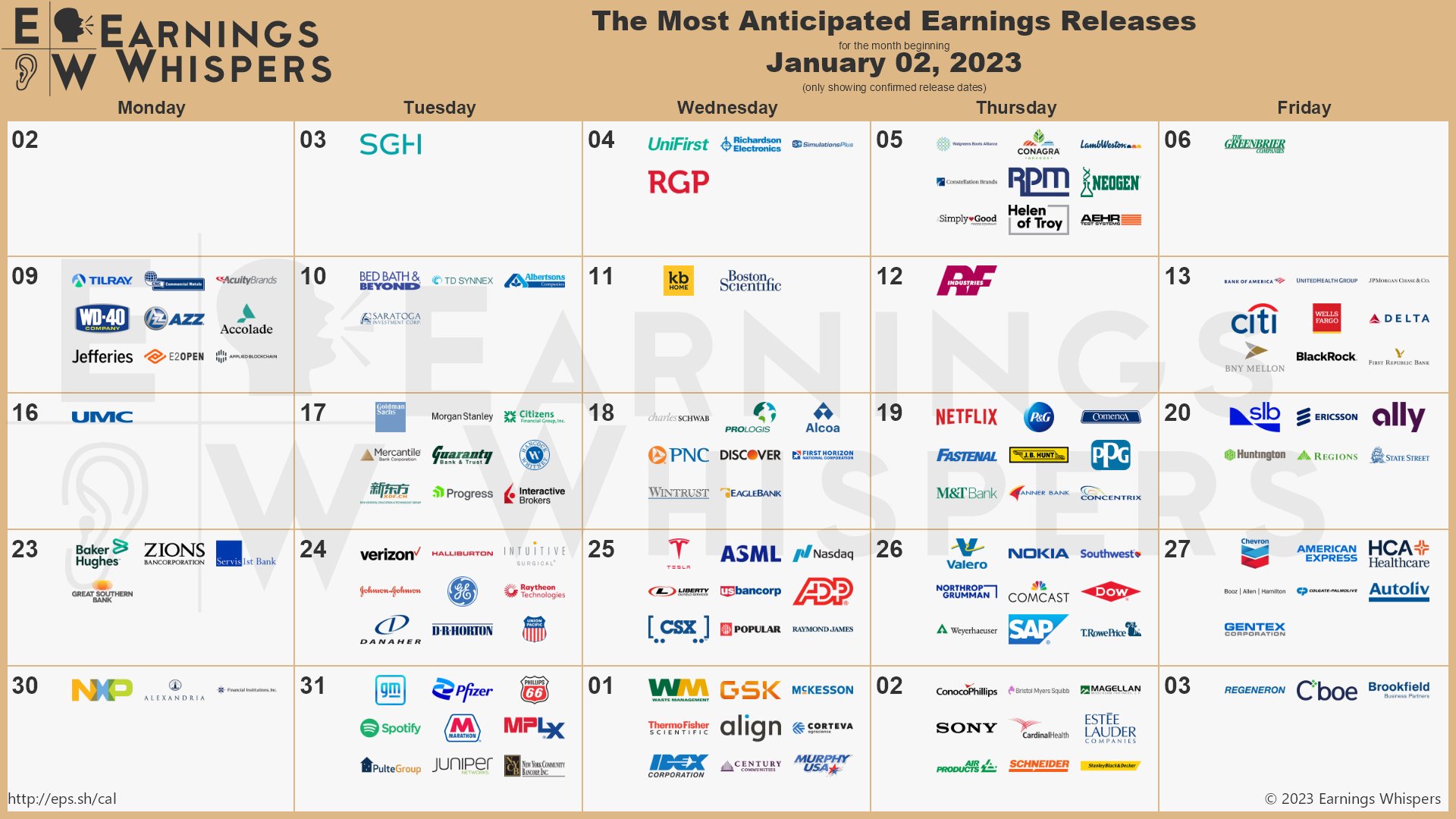

Lastly, following the major banks last Friday, earnings will be released for an increasing number of corporations. The table below shows the more notable earnings release dates.

Revisiting The Mother of all Recession Warnings

As we wrote in the Foghorn is Blowing, an inversion in the 3-month 10-year UST yield curve has signaled each of the last eight recessions. It is worth revisiting the yield curve as it has inverted another 40bps since we wrote the article. The four boxes highlight that each time the curve was in an inverted state, whereby the 3-month yield is above the 10-year yield, it reversed course suddenly. Once the curve was flat to positive, a recession occurred. The yield curve steepened by over 4% in the first three cases below. Such a steepening today implies the Fed will resort to a zero-interest rate policy again. The steepening of the curve in 2019-2020 was interrupted by the pandemic and the Fed’s extreme monetary actions.

As we ponder the graph, we are left to wonder how the curve might un-invert. Equally important is what may cause such a steepening. Further, while history can be prescient, we must also consider how this time might be different.

Home Prices Will Fall Further

Lance Roberts published Home Prices Will Likely Fall Further to provide insight into what will likely be a tough market for home sellers. The wealth effect, as we share in Lower Stock Prices are the Fed’s Goal, is a theory by Ben Bernanke. It theorizes that wealth, be it from the stock market or real estate, is an important factor that drives consumption. Homeowners feel wealthier when house prices are surging, as we saw in 2020 and most of 2021. Per Bernanke’s theory, homeowners are likely to spend more when they feel wealthier. The theory also works in reverse. With the Fed wanting to curb demand to stifle inflation, higher rates are an essential tool. More specifically, 6%+ mortgage rates significantly hamper sales and lower home prices and thus crimp demand for other goods and services.

Per Lance:

The reversion in home prices that has begun will likely continue as that excess liquidity continues to leave the economic system. That drain of liquidity, coupled with higher interest rates, and less monetary accommodation, will drag home prices lower. As that occurs, the “home equity” that many new buyers had in their homes will dissipate as homeownership costs continue to rise due to higher rates and inflation.

Just as the Fed wants to take some froth out of the stock market, they likely harbor the same goal with the housing market. Home prices will likely fall further unless mortgage rates fall quickly and the economy avoids recession.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.