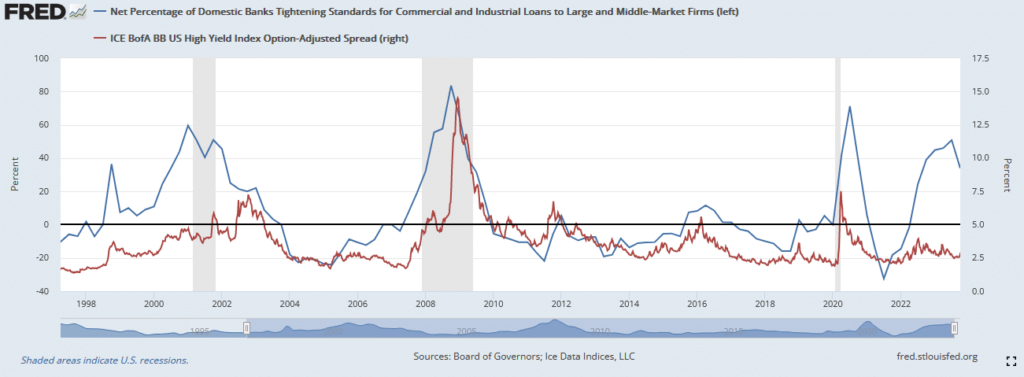

Corporations predominately borrow from banks and credit investors via the corporate debt markets. Most often, banks and credit investors have similar views as to pricing corporate loans/debt. Today, their views are starkly different. The graph below compares bank lending standards to the yield premium of junk bonds versus U.S. Treasury securities. As shown, spikes in lending standards often precede or accompany recessions. Subsequently, junk bond spreads soar as investors require more yield to offset rising default risks. Given the economy’s reliance on debt continues to grow, this relationship should strengthen over time. However, the percentage of banks tightening lending standards has surged, yet junk bond spreads haven’t budged from historically low levels.

Why might this time be different? Currently, banks have two predominant reasons to tighten lending standards. First, the yield curve is inverted. Consequently, their profit margins on new loans are lower than they typically prefer. To offset it, they can raise interest rates or refuse to lend money. Both options equate to tighter lending standards. Secondly, per the Fed, deposits at commercial banks have shrunk by approximately $800 billion since mid-2022. Deposits provide banks with the capital to lend. As deposits flee for higher-yielding alternatives, banks are forced to reduce assets. Therefore, even if the banks are comfortable with lending risks, the inverted yield curve and loss of deposits force them to enact more conservative lending standards. Junk bond investors have no such constraints.

What To Watch Today

Earnings

Economics

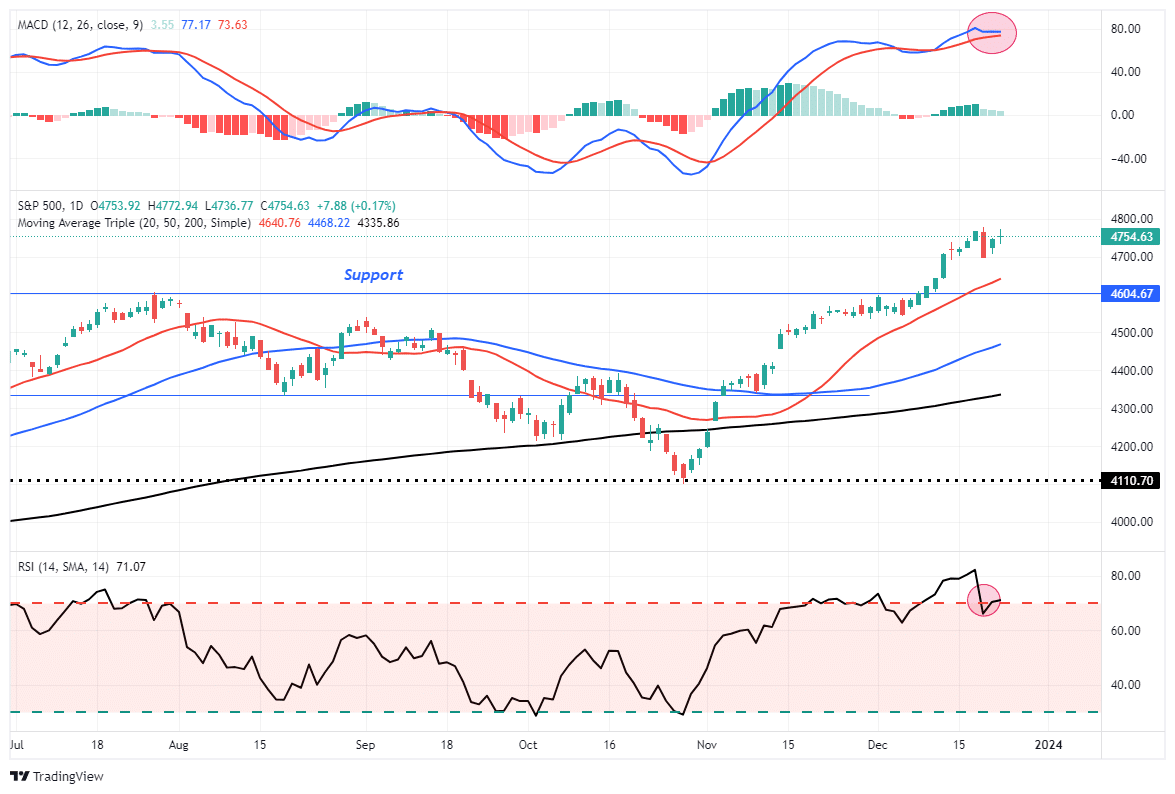

Market Trading Update

Last week, we noted that:

“The FOMC pivot sent stocks soaring and bond yields lower, as the message was more dovish than even the bulls expected. Notably, as measured by the volatility index, any bearishness was crushed.”

However, with the market very overbought, we suggested the upside gains would be somewhat limited, and consolidation, or correction in price, was needed before the market made an attempt at all-time highs. Such was the case last week, as a sharp selloff in the market on Wednesday was followed by two days of gains, keeping the market in a fairly tight trading range.

While the price action this past week did reduce some of the overbought conditions, as represented by the Relative Strength Index (RSI), there is still more work ahead. Next week, the “Santa Claus Rally” will officially begin, which will last through the first two days of January. Given the overbought condition, further upside may remain limited.

While we continue to maintain our equity market exposure currently, we suggest using the current market to rebalance portfolio risks as needed as we head into 2024. Taking profits, tax loss selling laggards, and raising a bit of cash never leads to a poor outcome. The market will provide a better opportunity on a risk/reward basis in the next few weeks. However, patience is required.

The Week Ahead

The week between Christmas and New Year’s Eve will likely prove quiet. Little economic data of consequence is due out. Additionally, there are not many Fed speakers on the docket. The markets will close early on Friday.

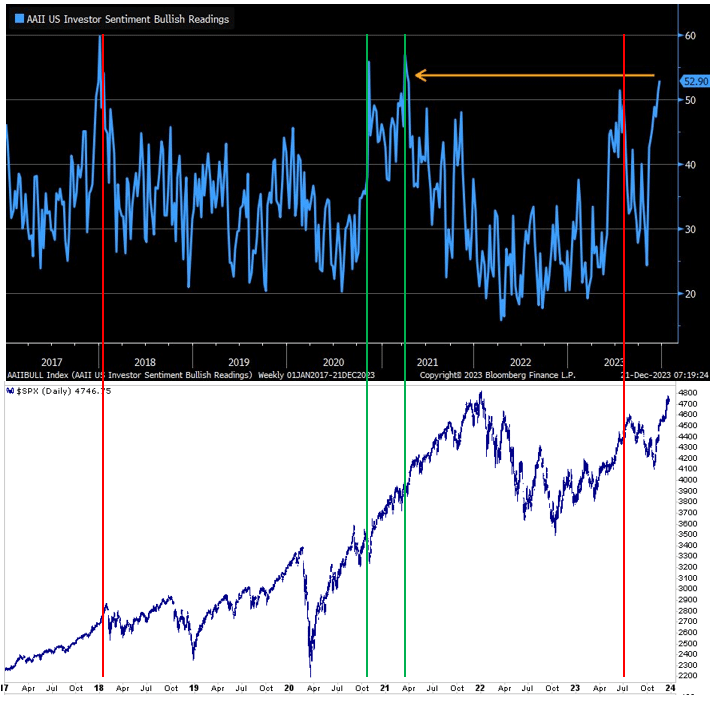

Individuals Are Very Bullish

The top graph below from the American Association of Individual Investors (AAII) shows that bullish sentiment is now at levels fast approaching the last peak in April 2021. While your instinct may be that such a high level of sentiment is bearish, the data over the last six years is not as conclusive. The red lines show that two of the four times sentiment has been this high or higher, a decent market decline followed. However, the two green lines highlight that sentiment can decline without a significant market drawdown. It is also worth noting that AAII sentiment at its peak in early 2022 was high but below prior highs. This graph further affirms that the market is overbought short-term, but not necessarily that a large decline, ala 2022, is in store.

PCE Inflation Is Weaker Than Expected

The Fed’s favorite inflation gauge, PCE, was weaker than expected across the board. November’s core PCE rose 0.1%, below 0.2% expectations and the previous 0.2% reading. Core year-over-year inflation is now 3.2%, down 0.3% from the last month. The headline number was -0.1%.

The graph below, courtesy of Renaissance Macro Research, shows the six-month annualized core PCE rate is down to 1.87%. The data further confirm that inflation is declining, which helps explain why the Fed appears to be shifting to a more dovish stance.

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.