The Fed has begun cutting interest rates with the timing and amount of future cuts predicated on incoming employment and CPI data. As the Fed likes to say, they are data-dependent in determining their course of action. Given the importance of Fed policy on the markets, one would presume that on the day of the release of crucial employment and inflation data, market volatility would be higher than average in the stock and bond markets.

The table below calculates the difference between the daily high and low on employment and CPI reporting days divided by the opening price for the respective securities. As shown, volatility has been higher on average in the stock market over the last year on both reporting days. However, the average deviation from the norm is not significant. Interestingly, bond prices, which should be more sensitive to the data, have not been overly volatile. In fact, on average, there is no discernable difference on employment report days, and the days in which CPI is released have been slightly below average.

These reports remain extremely critical for the Fed, but the media may be overstating their market importance.

What To Watch Today

Earnings

Economy

Market Trading Update

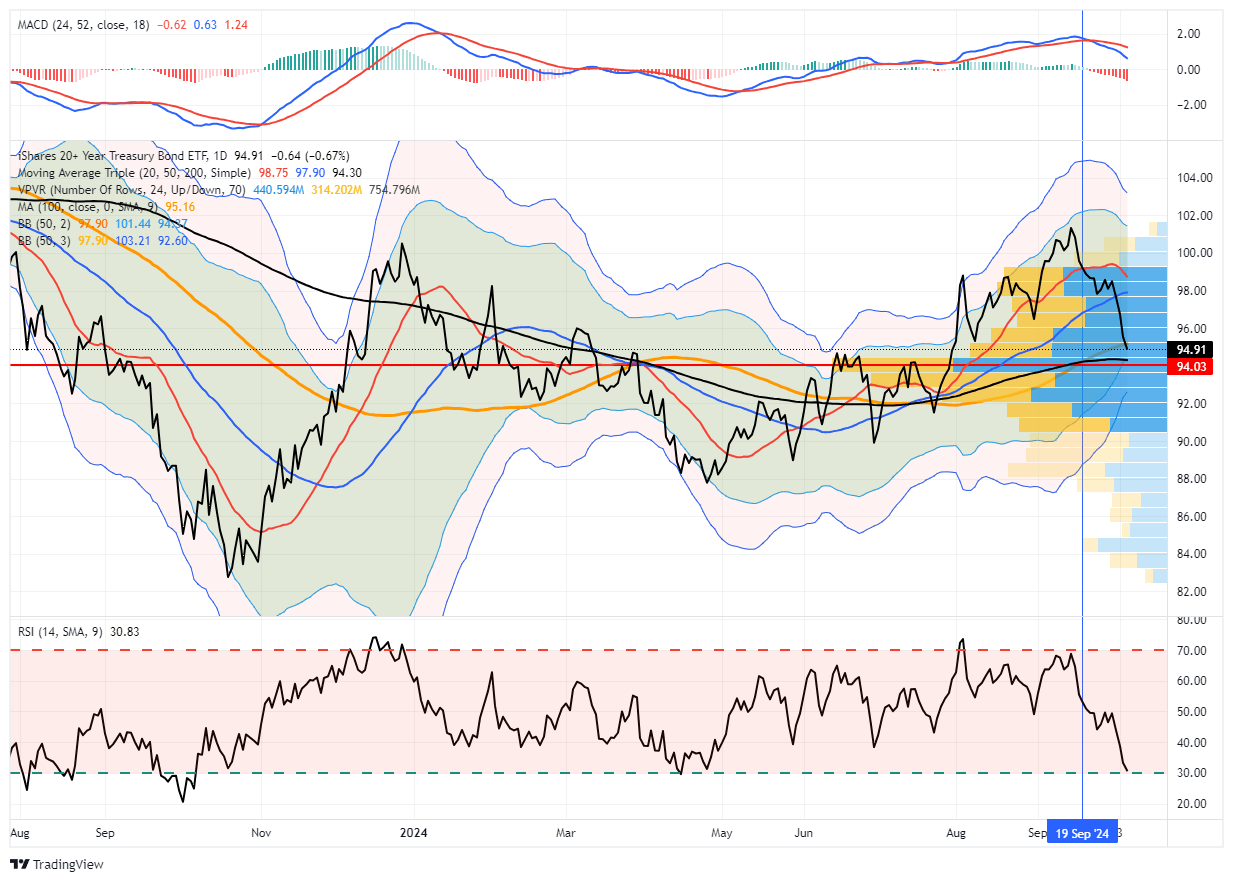

Yesterday, our discussion focused on the kick-off of earnings season, which begins in earnest with the major banks on Friday. However, one of the big questions lately has been the rise in interest rates. Panic again starts to surface, and numerous questions arise about the return on inflation as interest rates increase. However, the recent rise in rates was well expected. As we noted on September 17th, the day before the Fed Meeting:

“As shown, Treasury bonds (as represented by TLT) are quite deviated from the 50-DMA and overbought on multiple levels. While we remain bullish on bonds in the longer term, particularly as the economy slows, the current overbought conditions and “exuberance” into the bond trade over the last few months is a bit overdone.

With the Fed meeting this week, the current setup suggests that even if the Fed cuts rates as expected, this could be a “buy the rumor, sell the news” setup for bonds. Of course, as is always the case, overbought conditions can remain overbought longer than most imagine, so trade accordingly.”

That turned out to be the case, and as shown, the previous overbought conditions and massive deviation from the 200-DMA have fully reversed. With bonds now sitting on support at the 200-DMA and 2-standard deviations oversold, bonds are now in a much better position to add to portfolios. It is also important to note that most of the volume on Treasury bonds has occurred between $92 and $94 on the iShares 20+ Year Treasury bond ETF (TLT). While rates could certainly increase from here (our target was 4.1% to 4.2% on yield), the more deeply oversold condition sets bonds up for a decent trade.

As discussed, yields are a function of economic and inflation over time, and both will continue to decline into next year. However, as with everything, nothing moves in a straight line.

In Hindsight, The Employment Report Was Not As Rosy As It Seemed

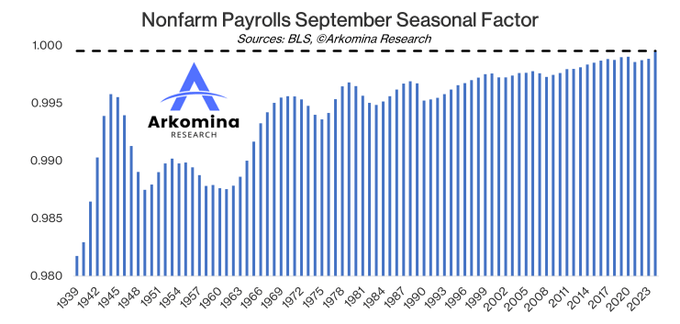

As noted in yesterday’s Commentary, the BLS employment report showed solid strength in the labor markets. Consequently, the bond market is lowering its expectations for the number of Fed rate cuts. However, as we will share, that may be a mistake. With a deeper review of the BLS data, some dark clouds remain despite the sunny headlines.

The first notable concern is the BLS’s seasonal adjustments to the data. The first graph below, courtesy of Arkomina Research, shows that the September seasonal adjustment was the highest in the data’s history. Like ADP, it also showed a considerable jump from last year’s figure. Arkomina calculates that had last year’s seasonal adjustment been used, the payroll growth would have been in line with expectations at +145k. The ADP report would have shown zero job growth had the same seasonal factor as 2023 been used.

The second curious piece of data in the report is government job growth. The BLS reported that 785k jobs were added to the labor market by the government. The second graph from ZeroHedge shows that on a seasonally adjusted and non-adjusted basis, the increase in government jobs in September dwarfs prior September data. Furthermore, as the second Arkomina chart shows, that was the largest gain in government jobs, excluding June 2020, since 1948.

Lastly, we show that the average hours worked by employees are not rising, as typically occurs in a robust jobs market.

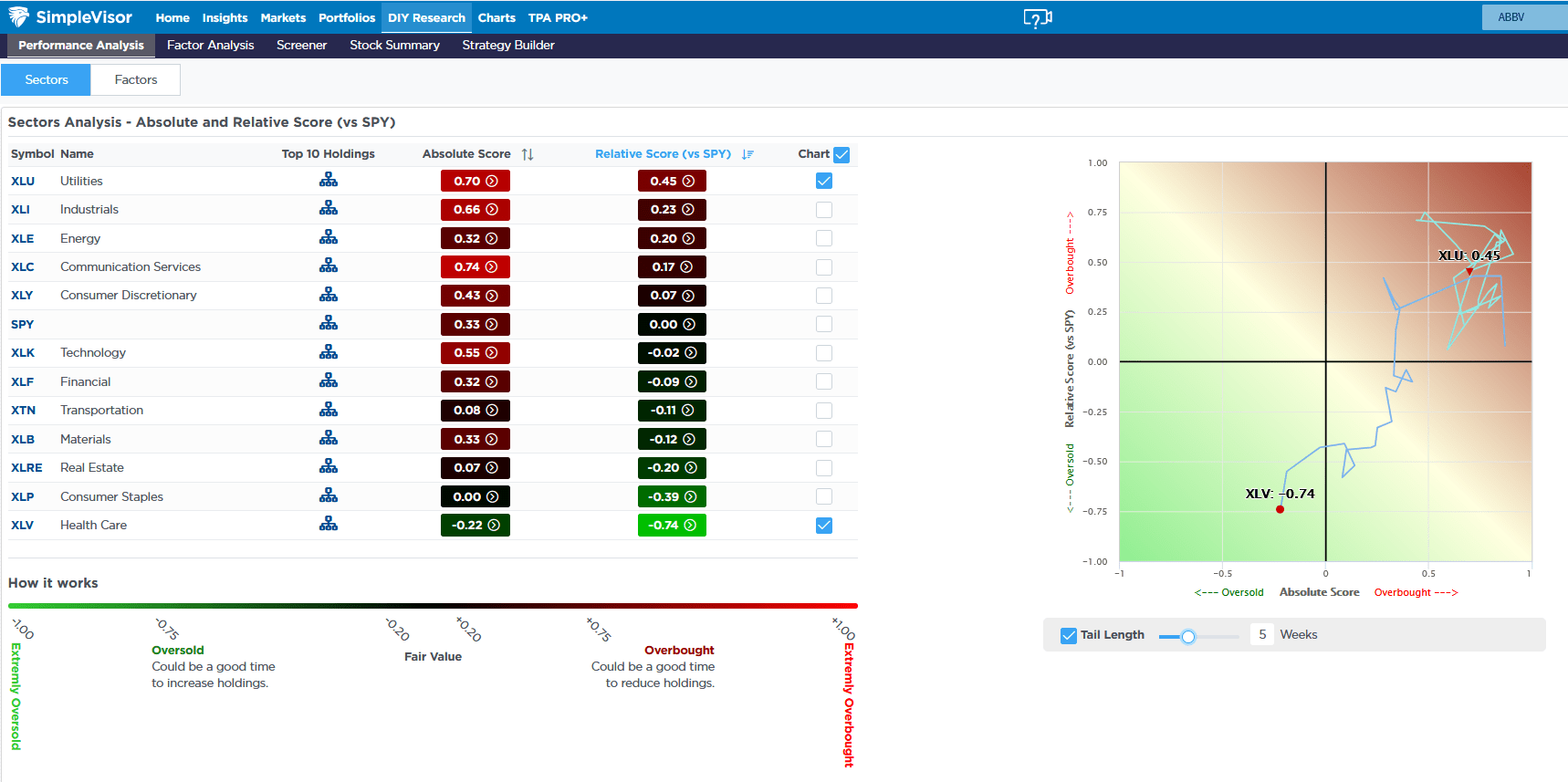

A Tale Of Two Sectors

Five weeks ago, healthcare and utility stocks led the market higher. Today, the two sectors are opposites. Utilities are the most overbought sector. Despite rising interest rates, the higher dividend-paying stocks are doing well. The culprit appears to be the expansion of the power grid to facilitate AI. Think of the recent action in utilities as the AI chase part 2. Healthcare stocks are under pressure. They, too, pay higher than market dividends, so there is some pressure due to interest rates. This can be attested to by staples and real estate, among the most oversold. Secondly, there is probably some consternation with the election and uncertainty about how the new President and Congress will deal with healthcare-related issues.

The SimpleVisor graph on the right side shows healthcare (XLV) absolute and relative technical scores have steadily weakened over the last five weeks. At the same time, utility stocks remain strong.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.