Recently, James Grant, editor of the Interest Rate Observer, was asked about his outlook for interest rates. He sees interest rates moving in a cyclical pattern, potentially rising for another multi-decade period. Grant bases his view on historical observations rather than a mystical belief in cycles. He states that finance has shown a cyclical nature, moving from extremes of euphoria to revulsion in various asset classes. Therefore, he proposes that persistent inflation, increased military spending, and significant fiscal deficits could drive rates higher. The Fed’s target of a 2% inflation rate and the electorate’s preference for policies that lead to inflation also contribute to this trend.

Let me state that I have a tremendous amount of respect for Grant and his work. However, I can’t entirely agree with his view. I will focus today’s discussion on the outlook for interest rates based on the two bolded sentences above.

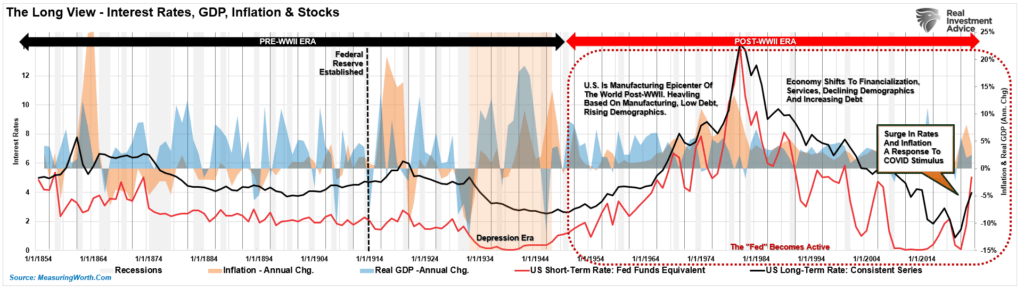

The chart below shows the long-term view of short and long-bond interest rates, inflation, and GDP. As Grant notes, there is a cycle to interest rates previously.

Interest rates rose during three previous periods in history.

- During the economic/inflationary spike in the early 1860s

- The “Golden Age” from 1900-1929 saw inflation rise as economic growth resulted from the Industrial Revolution.

- The most recent period was the prolonged manufacturing cycle in the 1950s and 1960s. That cycle followed the end of WWII when the U.S. was the global manufacturing epicenter.

Remembering History

However, while interest rates fell during the Depression, economic growth and inflationary pressures remained robust. Such was due to the very lopsided nature of the economy at that time. Like the current economic cycle, the wealthy prospered while the middle class suffered. Therefore, money did not flow through the system, leading to a decline in monetary velocity.

The 1950s and 60s are the most important.

Following World War II, America became the “last man standing.” France, England, Russia, Germany, Poland, Japan, and others were devastated, with little ability to produce for themselves. America found its most substantial economic growth as the “boys of war” returned home to start rebuilding a war-ravaged globe.

But that was just the start of it.

In the late ’50s, America stepped into the abyss as humankind took its first steps into space. The space race, which lasted nearly two decades, led to leaps in innovation and technology that paved the way for America’s future.

These advances, combined with the industrial and manufacturing backdrop, fostered high levels of economic growth, increased savings rates, and capital investment, which supported higher interest rates.

Furthermore, the Government ran NO deficit, and household debt to net worth was about 60%. So, while inflation increased and interest rates rose in tandem, the average household could sustain its living standard.

So, why is this bit of history so important to the outlook of interest rates,

What Drives Interest Rates

Grant suggests that interest rates will rise because they have been low for so long. That is akin to saying that since the Atlanta Falcons have not won a Super Bowl in the last 58 years, they should now win it every year for the next 58 years. What drives the Atlanta Falcons to win a Super Bowl are the ingredients to lead to a great team, not just the fact that they have never won one. The same goes for interest rates.

Interest rates are a function of the general trend of economic growth and inflation. More robust growth and inflation rates allow lenders to charge higher borrowing costs within the economy. Such is also why bonds can’t be overvalued. To wit:

“Unlike stocks, bonds have a finite value. The principal and final interest payments are returned to the lender at maturity. Therefore, bond buyers know the price they pay today for the return they will get tomorrow. Unlike an equity buyer taking on investment risk, a bond buyer loans money to another entity for a specific period. Therefore, the interest rate takes into account several substantial risks:”

- Default risk

- Rate risk

- Inflation risk

- Opportunity risk

- Economic growth risk

“Since the future return of any bond, on the date of purchase, is calculable to the 1/100th of a cent, a bond buyer will not pay a price that yields a negative return in the future. (This assumes a holding period until maturity. One might purchase a negative yield on a trading basis if expectations are benchmark rates will decline further.) “

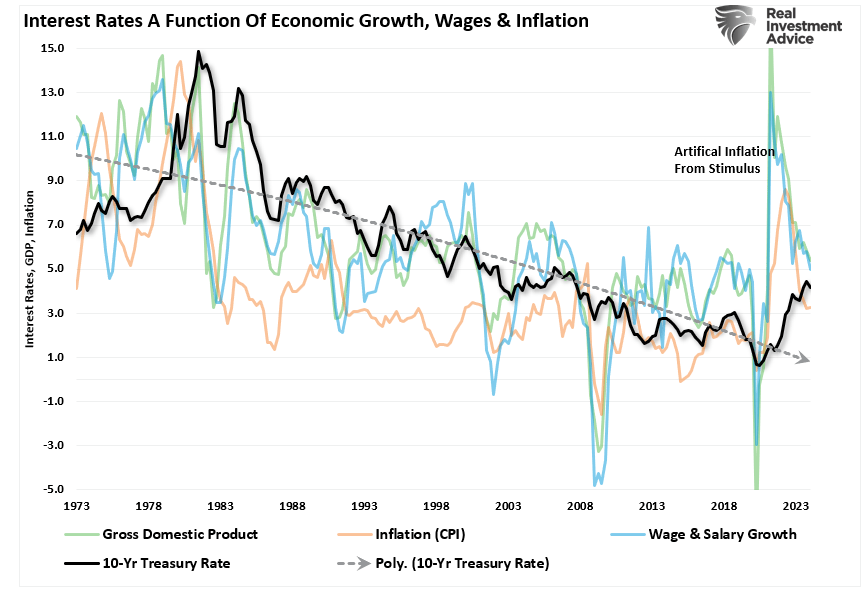

The chart below shows the correlation between economic growth, inflation, and interest rates. Unsurprisingly, interest rates rise when economic growth increases, leading to more demand for credit. Inflation rises with economic activity as the supply/demand imbalance increases prices. That is basic economics.

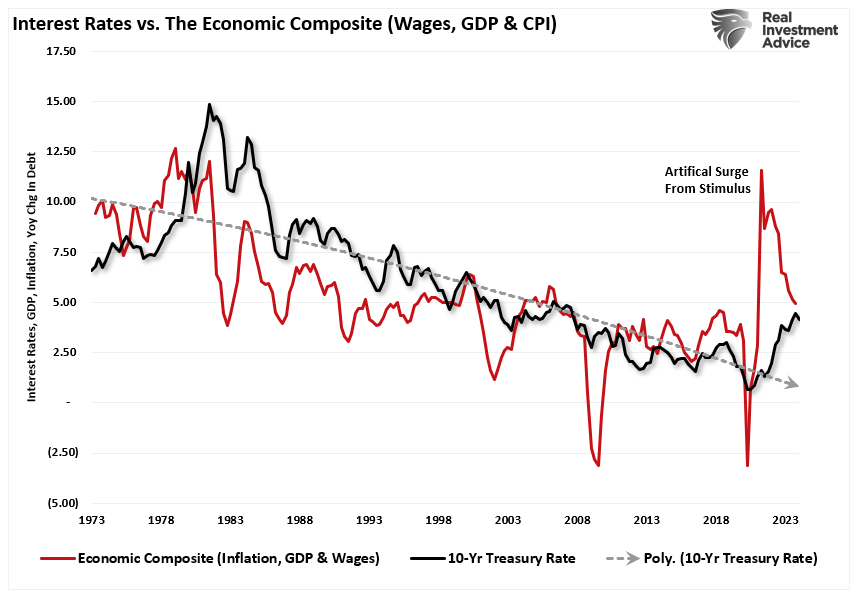

The chart above shows a lot going on, so let’s create a composite index of wages (which provides consumer purchasing power, aka demand), economic growth (the result of production and consumption), and inflation (the byproduct of increased demand from rising economic activity). We then compare that composite index to interest rates. Unsurprisingly, there is a high correlation between economic activity, inflation, and interest rates as rates respond to the drivers of inflation.

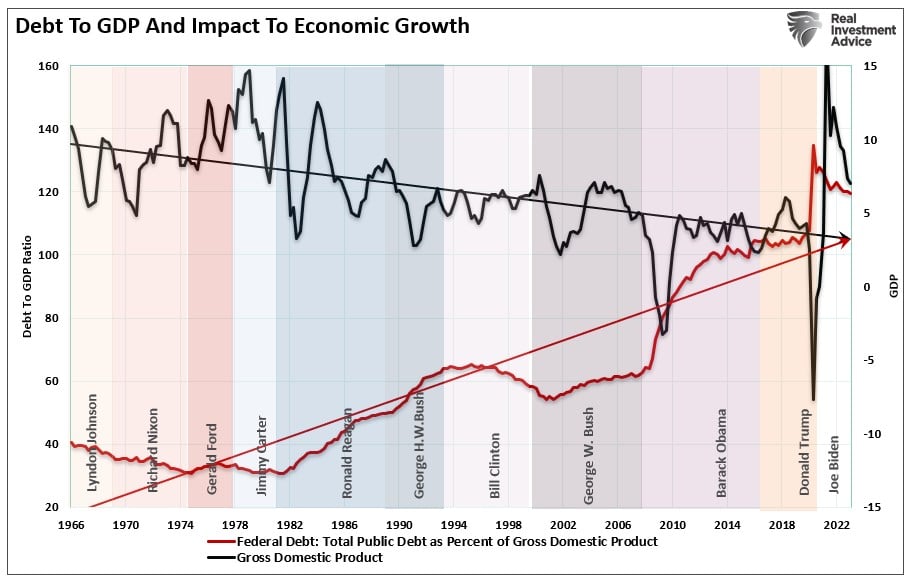

Grant further suggests that interest rates will be higher due to increased debt and deficits. Unfortunately, there is no evidence supporting that hypothesis.

The Deficit Fallacy

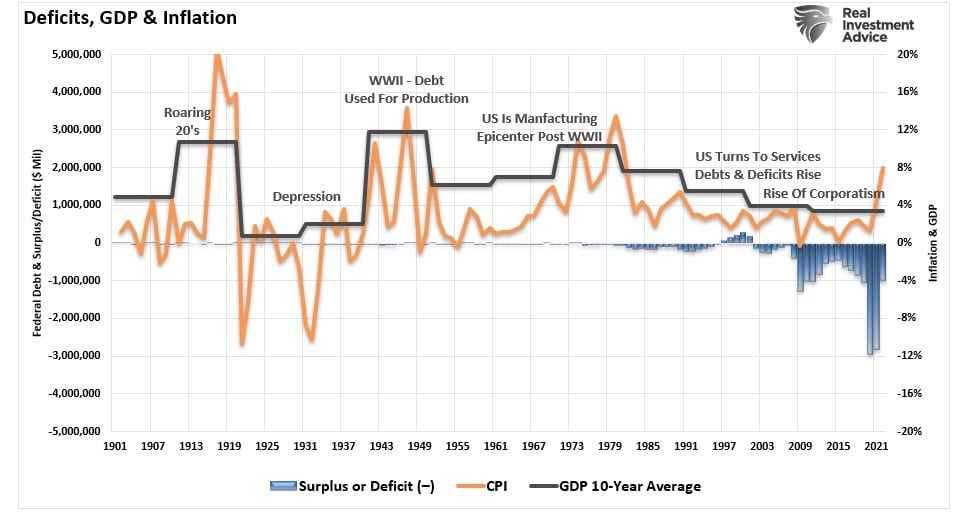

As shown below, the 10-year economic growth average correlates with interest rates. When economic growth rises, lenders can charge higher interest rates.

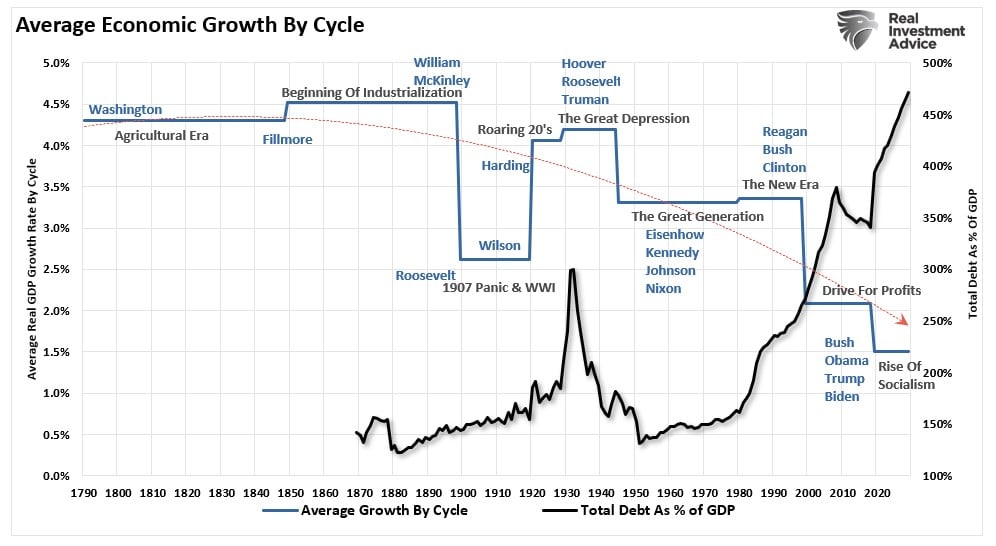

What should immediately jump out at you is that the 10-year average economic growth rate was around 8%, except for the Great Depression era, from 1900 through 1980. However, there has been a marked decline in economic growth since then. (The current spike in interest rates is a function of the artificial stimulus injected into the economy, which is now reversing.)

Increases in the national debt squandered on non-productive investments and rising debt service results in a negative return on investment. Therefore, the larger the debt balance, the more economically destructive it is by diverting increasing amounts of dollars from productive assets to debt service.

Since 1980, the overall increase in debt has surged to levels that currently usurp the entirety of economic growth. What should be evident is that increases in debt and deficits continue to divert more tax dollars away from productive investments into the service of debt and social welfare. The result is lower, not higher, economic growth, inflation, and, ultimately, interest rates.

When put into perspective, one can understand the more significant problem plaguing economic growth. A long look at history clearly shows the negative impact of debt on economic growth.

Furthermore, changes in structural employment, demographics, and deflationary pressures derived from changes in productivity will magnify these problems.

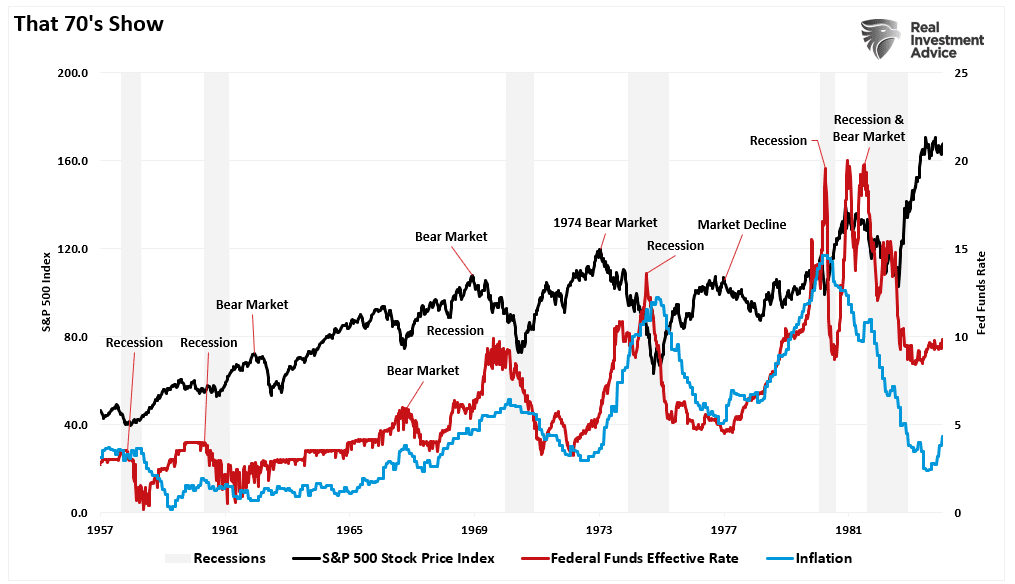

Inflation Wasn’t Just The 1970s

While many focus on the inflation surge during the late 1970s, as noted above, the entire period from the 1950s through 1980 was marked by rising interest rates and inflation due to a more robust economic growth cycle.

Like today, the Fed was hiking rates to quell inflationary pressures from exogenous factors. In the late 70s, the oil crisis led to inflationary pressures as oil prices fed through a manufacturing-intensive economy. Today, inflation resulted from monetary interventions that created demand against a supply-constrained economy.

Such is a critical point.

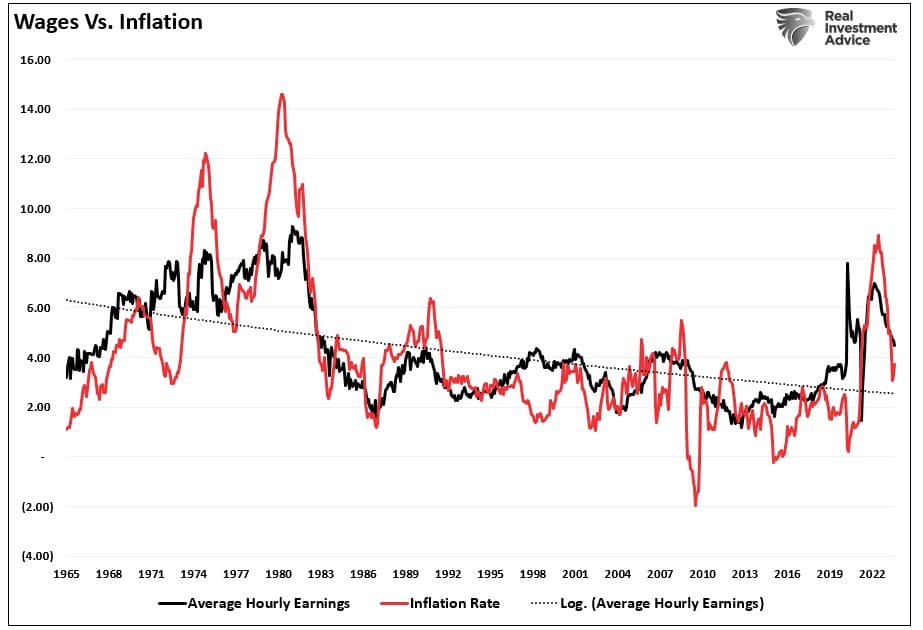

During “That 70s Show,” the economy was primarily manufacturing-based, providing a high multiplier effect on economic growth. Today, the mix has reversed, with services making up the bulk of economic activity. While services are essential, they have an extremely low multiplier effect on economic activity.

One primary reason is that services require lower wage growth than manufacturing. Inflation rose in the 1970s due to a steady trend of increasing wages, which created more economic demand. Outside of the artificial spike in demand from government stimulus in 2020, the longer-term trend of wage growth, and ultimately inflation, is lower as wage growth remains suppressed.

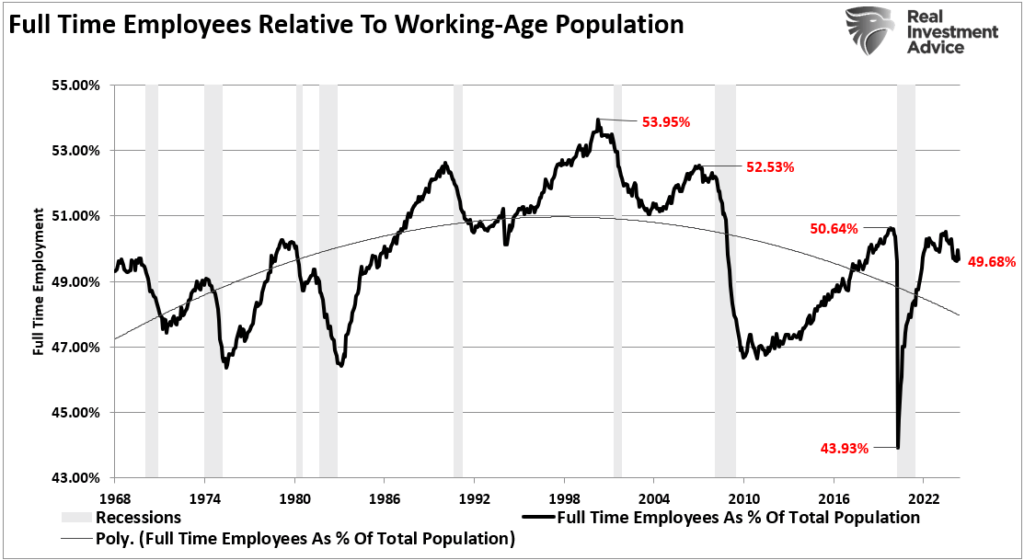

Wages come from the type of employment. Full-time employment provides higher salaries to support economic growth. Unfortunately, full-time employment as a percentage of the working-age population has declined since the turn of the century. Such is due to increased productivity levels through technology, offshoring, and immigration. The byproduct of fewer full-time employees is lower consumption and lower rates of economic growth.

Today’s economic environment vastly differs from the economic boom years of the 1970s. Rising debt levels, increased deficits, productivity, and wage suppression erode economic growth, not support it. Therefore, while Grant makes the case for higher interest rates for “much, much longer,” the economic evidence does not support that thesis.

Conclusion

However, even if Grant is correct and increasing debt levels and deficits do cause higher rates, central banks will take actions to artificially lower rates.

At 4% on 10-year Treasury bonds, borrowing costs remain relatively low from a historical perspective. However, we still see signs of economic deterioration and negative consumer impacts even at that rate. When the economy’s leverage ratio is nearly 5:1, 5% to 6% rates are an entirely different matter.

- Interest payments on the Government debt increase, requiring further deficit spending.

- The housing market will decline. People buy payments, not houses, and rising rates mean higher payments.

- Higher interest rates will increase borrowing costs, which leads to lower profit margins for corporations.

- There is a negative impact on the massive derivatives market, leading to another potential credit crisis as interest rate spread derivatives go bust.

- As rates increase, so do the variable interest payments on credit cards. Such will lead to a contraction in disposable income and rising defaults.

- Rising rates negatively impact banks, as higher rates impair the banks’ collateral, leading to bank failures.

I could go on, but you get the idea.

Therefore, as debt and deficits increase, Central Banks are forced to suppress interest rates to keep borrowing costs down and sustain weak economic growth rates.

The problem with Grant’s assumption that rates MUST go higher is three-fold:

- All interest rates are relative. The assumption that rates in the U.S. are about to spike higher is likely wrong. Higher yields on U.S. debt attract flows of capital from countries with low to negative yields, pushing rates lower in the U.S. Given the current push by Central Banks globally to suppress interest rates to keep nascent economic growth going, an eventual zero-yield on U.S. debt is not unrealistic.

- The budget deficit balloon. Given Washington’s lack of fiscal policy controls and promises of continued largesse, the budget deficit is set to swell above $2 Trillion in coming years. This will require more government bond issuance to fund future expenditures, which will be magnified during the next recessionary spat as tax revenue falls.

- Central Banks will continue to buy bonds to maintain the current status quo but will become more aggressive buyers during the next recession. The Fed’s next QE program to offset the next economic downturn will likely be $4 trillion or more, pushing the 10-year yield toward zero.

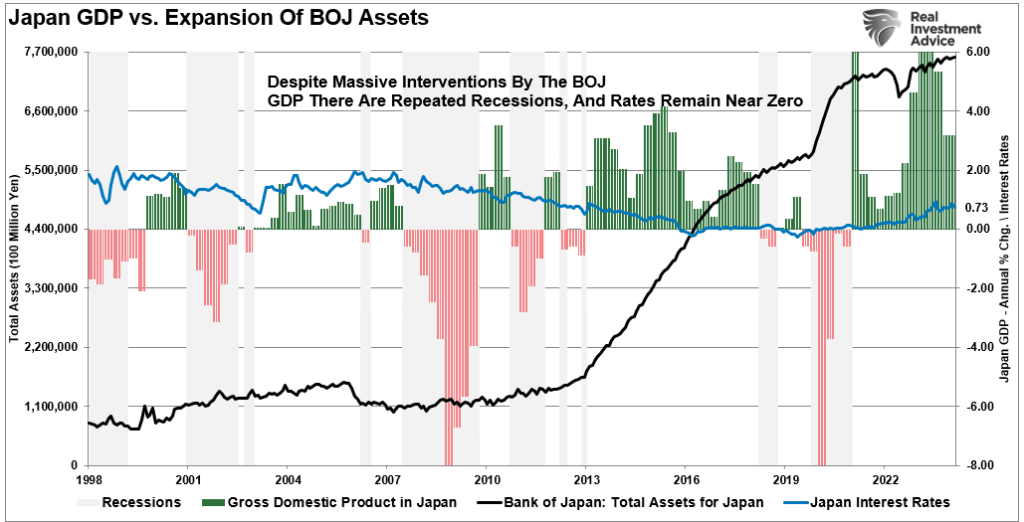

If you need a road map of how this ends with lower rates, look at Japan.

Historical evidence suggests that interest rates will be lower, not higher, unless the Government embarks on a massive infrastructure development program. Such would potentially revitalize the American economy and lead to higher rates, stronger wages, and a prosperous society.

However, outside of that, the path of interest rates in the future remains lower.