While it’s far from guaranteed, a Fed rate cut in September is looking increasingly likely. Wednesday’s FOMC statement changed to reflect a growing concern for the labor markets and less worry about inflation. The opening paragraph below says job gains have moderated, whereas the prior statement said job gains remained strong. They also changed the characterization of inflation by adding the word “somewhat” in front of elevated.

Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have moderated, and the unemployment rate has moved up but remains low. Inflation has eased over the past year but remains somewhat elevated. In recent months, there has been some further progress toward the Committee’s 2 percent inflation objective.

For the first time in a while, the Fed appears to be equally managing their two mandates, labor and prices. Before this meeting, inflation was the most important of the two. As they note:

The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

The prior statement said: “The economic outlook is uncertain, and the Committee remains highly attentive to inflation risks.”

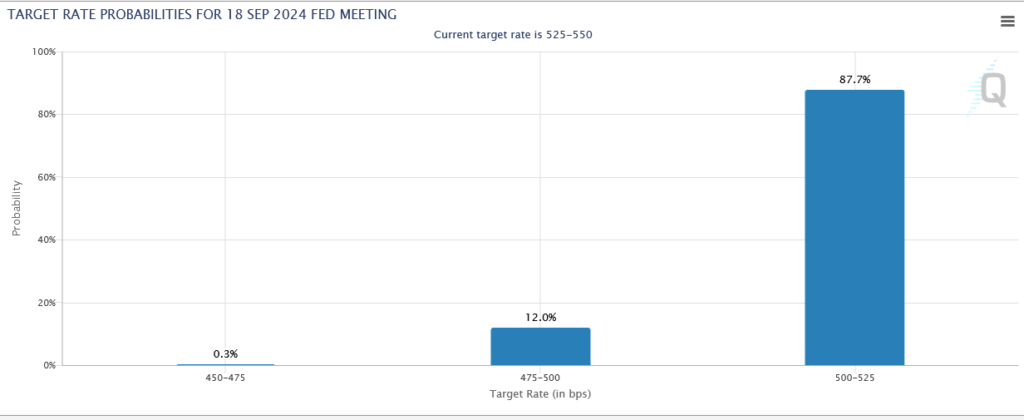

While not explicit, the Fed’s FOMC statement certainly leaves the door open for a rate cut at the next meeting. As shown below, Fed Funds futures imply a 100% chance of a Fed cut in September and a 12% chance that the Fed’s September rate cut will be 50bps.

What To Watch Today

Earnings

Economy

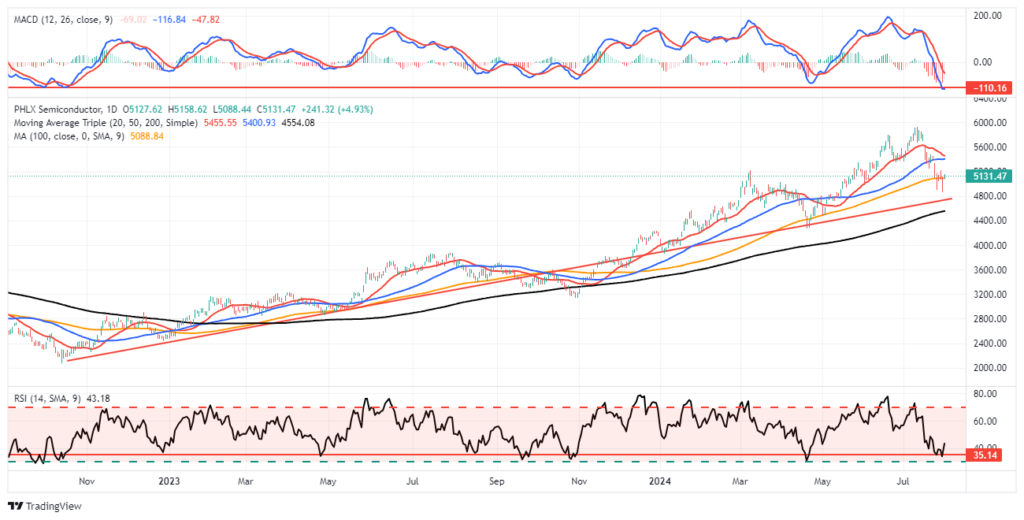

Market Trading Update

After the recent decline, I am starting to like the setup for adding back to Technology and Semiconductor stocks. From a technical perspective, the recent decline in the Nasdaq (QQQ) and the Semiconductor sectors (SOX) was needed to reverse some of the more egregious overbought conditions. Such was the point of yesterday’s commentary on the Megacap Growth ETF (MGK). The chart of QQQ shows the same setup as MGK yesterday, which is obvious since they are dominated by the same stocks.

The Philadelphia Semiconductor Index (SOX) has a similar setup.

Notably, the recent drawdown in the SOX index was extremely aggressive, and previous such drawdowns have been good buying opportunities for increasing exposure.

Notably, the recent selloff in the semiconductor and mega-cap stocks was driven by a narrative that the “AI Trade” is dead as there is no viable money-making product for AI, and companies will drastically cut CapEx in artificial intelligence. The problem with that narrative is that it is WAY too early to know that with any certainty, and AMD’s earnings report certainly doesn’t support that narrative. As noted yesterday:

“My 2c is that there is enough evidence in tech prints tonight that suggests to me that growing AI fears lately on fears of capex stalling/slowing or lack of monetization proof (essentially any way for ppl to try to call peak on AI spend) is not necessarily occurring in the fundamentals nor the company’s messages as much as one would think reading news or looking at how any of these stocks have traded in the last 6 weeks.” – JP Morgan.

Will the “AI Trade” eventually come to an end? Most assuredly. However, it is likely not now, and the recent selloff looks more like a buying opportunity to me than not.

Jerome Powell’s Press Conference

Given that the Fed appears to be preparing markets for a rate cut in September, it’s worth sharing a few quotes from Jerome Powell’s FOMC press conference and some commentary.

- “Data suggest that the labor market has returned to where it was on the eve of the pandemic.”

- “If the labor market were to weaken unexpectedly, we are prepared to respond.”

- The Fed remains data-dependent.

- Powell thinks a rate could occur in September if inflation continues moving down with expectations and the labor market remains firm.

- The Fed is “well-positioned to respond to labor market weakness.” A poor employment number from the BLS all but assures a rate cut in September.

- They didn’t cut at the meeting because they didn’t want to undermine progress on inflation.

- He won’t give specific forward guidance on the pace or timing of future rate cuts.

- “This is a broader disinflation.” This is in reference to the recent decline in inflation compared to last year. Powell is optimistic the recent decline in inflation is sustainable.

- “There was a real discussion about the case for reducing rates at this meeting, but the strong majority supported not moving rates at this meeting.”

Another Weak Labor Report

The ADP private sector jobs report showed a below-consensus gain of 122K compared to 155K last month. This is the lowest job growth since January’s 111K, bringing the 2024 monthly average to 160K. ADP’s Chief Economist Nela Richardson made a very important statement regarding the report: “If inflation goes back up, it won’t be because of labor.” If correct, a critical driver of inflation is no longer a problem.

The breakdown of the contribution within the labor report was interesting. Services comprised +85K of these new hires, with goods-producing businesses adding +37K. By industry, Trade/Transportation/Utilities led the way with +61K jobs filled, followed by +39K in Construction, +24K in Leisure/Hospitality, and +22K in Education/Healthcare. Remember, Leisure/Hospitality was adding 400k to 500k jobs a month not long ago.

Manufacturing lost 4K jobs, Information Services were down 18K, and Professional/Business Services, which, like Leisure/Hospitality, had been among the highest-growing employment sectors, shed 37K jobs.

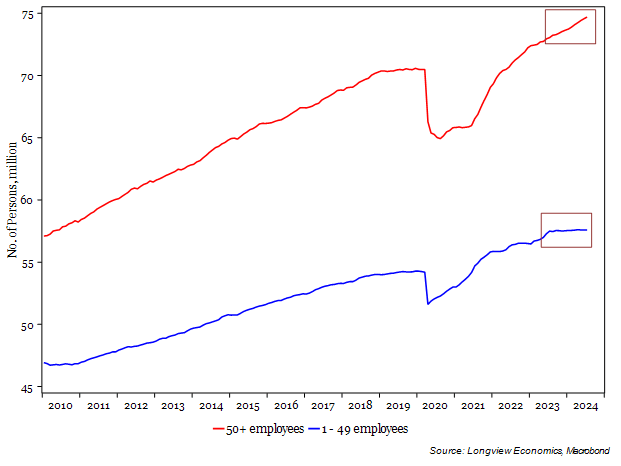

Between ADP and JOLTs, the labor market clearly shows signs that the labor market has normalized completely. The current estimate for Friday’s BLS payroll growth is +185K. Note that the BLS survey only includes large companies. However, as shown below, companies with less than 50 employees have seen no job growth for about a year. This is a good example of the weakness beneath the headlines.

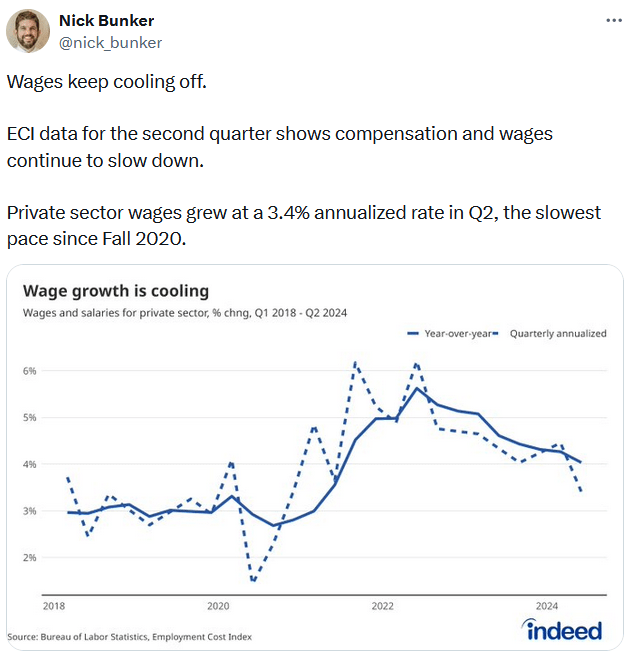

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.