The 10-Commandments were born from the boom of the stock market and the internet. That boom changed the face of investing from the stodgy oak-filled rooms of brokerage firms to computer and mobile phone screens. There is nothing wrong with this; of course, except for the fact that a raging bull market, as seen from 2009-2021 makes even the most uneducated of investors believe they are smart.

In reality, none of us are perfect as investors; even the most respected investors admit they make errors. As Warren Buffett has told his shareholders in various annual letters: “You’d have been better off if I had gone to the movies [this year]” and: “I have erred [by] not making repurchases [of shares].”

In 2004, when asked at the Berkshire Hathaway annual meeting what his worst investing mistake was:

“I set out to buy $100 million shares of Wal-Mart at [a pre-split price] $23. We bought a little and it moved up a little and I thought maybe it will come back a bit. That thumb-sucking has cost us in the current area of $10 billion.” – Warren Buffett

The purpose of this article is to detail some of the basic rules of investing that should NEVER be broken. Just as Moses came down from the mountain with the two stone tablets; these rules are just about as sacred when it comes to trading and investing your capital.

I have personally made many mistakes over the last 30 years. We are talking about the types of errors that almost cost me my livelihood. However, I turned those mistakes into valuable lessons. Therefore, before we get started I will let you in on two observations I learned along the way:

- No investment strategy works all the time and;

- There’s a reason why consistent producers get paid the big bucks. Flashy bets and big swings sometimes connect but, in the end, a disciplined approach pays the bills.

Commandment 1) Worship No Price Action Before Discipline

The price action of stocks can be a valuable tool when investing. However, many investors fall victim to the lure of fast money. Just as the ringing of the bell causes Pavlov’s dogs to salivate; when stocks are rising it becomes hard to resist the temptation to take on excessive risk. Ultimately, that is always a losing proposition. Remember, the whole purpose of investing is to buy something that is trading at a discount to its fair value and sell it when it is at a premium.

The reason most investors fail at investing over a long period of time is that emotion takes over discipline. As investors chase stocks higher, the definition of the “greater fool theory,” the “fear of missing out” on a hot stock or sector overrides the basic tenants of investing. As such, the whole premise of buying low and selling high becomes inverted. Such is pertinent as headlines of new highs serve as sexy sirens for those on the sidelines.

We will talk more about removing emotion from investing in a moment.

Commandment 2) Honor Thy Discipline

Discipline is absolutely THE hardest thing to adhere to especially when it doesn’t appear to be working. We have written many times about the importance of building a strategy and following it strictly over time. Such is important to avoid behavioral biases, no matter how strongly you feel about a given position, sector, or market.

To win the long-term investing game, you must defer to the principles of your discipline when investing. Ultimately, any investment strategy you utilize should define the parameters of controlling the risk to the underlying investment capital. If it doesn’t, then it is not a good investment strategy.

Just like in a game of Monopoly, once you run out of money – you are out of the game.

Commandment 3) Thou Shalt Not Covet Opportunity

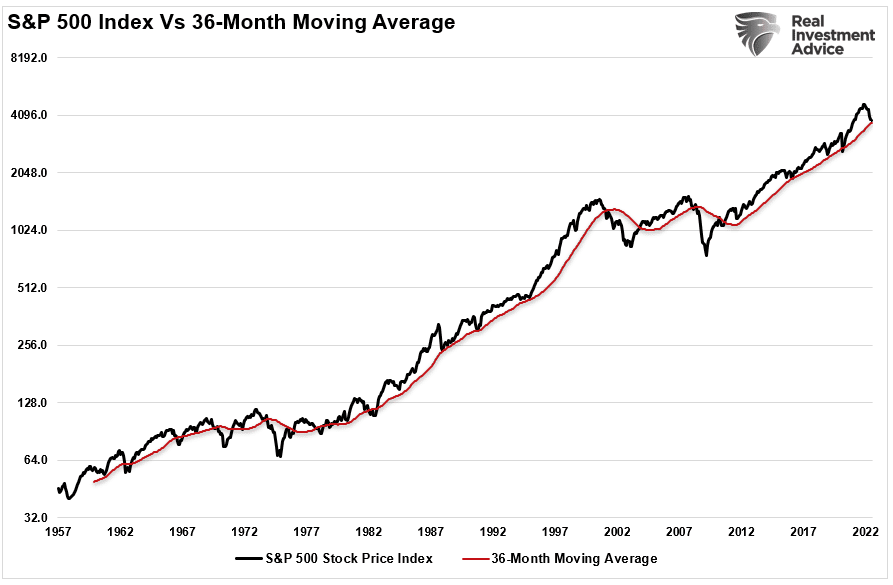

Investors tend to get “sucked” into investing; even when they inherently know it is not the best of ideas. However, that is the nature of investing, and ultimately investor psychology. The basic problem that occurs when investing is that when a stock or a whole market is moving higher, investors tend to “feel” as if they are being left behind. Such is the classic example of the “Fear Of Missing Out,” or “F.O.M.O.” Individuals tend to believe they standing alone on an imaginary dock, as some mythical ship is setting sail never to return to port again.

If you will look at the chart above of the S&P 500 vs its 36-month moving average, there are numerous opportunities to both BUY and SELL investments in order to realize gains and protect investment capital. When the price of the index deviates too far above the 36-month moving average, it is a good time to sell. When it returns to, or below, that moving average, it is a good time to buy. The problem is that when markets are reaching levels investors should be selling, they are in a panic to “buy,” and vice-versa.

Missing an opportunity to invest money is NOT the end of the world. There will always be other opportunities in the future, either in the same investment or another. Opportunities are easy to repeat, however, recovering lost investment capital from making bad investment decisions is both hard to recover and time-consuming in terms of opportunity costs.

Not every investment you make will be profitable. You will lose money on some investments and you must be okay with that reality. Otherwise, don’t invest.

It is only necessary to have a high enough winning percentage on the investments you choose to make to reach your goals.

“In investing the ability NOT to invest is as important as investing ability.”

Commandment 4) Thou Shalt Be Unemotional About Investments

The single most important commandment of them all is to remain unemotional. Such is the root of all investment mistakes you will ever make.

“It’s the swings of psychology that get people into the biggest trouble, especially since investors’ emotions invariably swing in the wrong direction at the wrong time. When things are going well people become greedy and enthusiastic, and when times are troubled, people become fearful and reticent. That’s just the wrong thing to do. It’s important to control fear and greed.” – Howard Marks

Emotion is the devil of investing and is solely responsible for more lost capital than any other single event in human history. The worst thing you can do as an investor is to become emotionally attached to any investment. When we allow emotions to drive the buy or sell decision, we forfeit the logical decision-making process.

Emotional decisions always come back to haunt you. We often get attached to a particular position because:

- It belonged to your grandparents, or

- You invested money into a particular “hot” stock because some guy on television told you it is “going to the moon, booyah,” or

- You keep holding onto a bad investment hoping it will “come back” because you don’t want to admit you made a mistake.

Whatever the reason, the decision process was flawed.

Emotions and investing ultimately do not mix which is why a well-built investment strategy with strict guidelines for both buying AND selling is important. Of course, absolutely NO strategy will work over time if you don’t have the discipline to adhere to it in both good times and bad.

Commandment 5) Thou Shalt Sell Hope And Buy Fear

Jesse Livermore once said,

“Buy stocks when there is blood in the streets.”

The concept of “selling hope and buying despair” is the basic premise of investing. It is also more commonly known as “buying low and selling high”. However, while such seems to be a very simple concept, it is nearly impossible for most investors to actually implement.

The reason, again, is our inherent emotional biases. When the markets are coming unwound and rapidly losing money most investors aren’t willing to step up and buy stocks that are “bleeding.” The psychological “fear,” known as “loss aversion,” is that stocks, or markets, could go lower. However, what most investors fail to understand is that if you are following a well-structured investment strategy, a “bleeding investment” is becoming cheaper in terms of valuation and therefore a more valuable long-term investment. A good investment strategy will identify at what price levels an investment can be purchased to capitalize on under-valuation. Such is why all great investors in history focused on fundamentals and were ready to relieve panicking investors of their holdings at bargain-basement prices.

Commandment 6) Thou Shalt Adapt Thy Ways

The markets experience both cyclical and secular periods where prices are either rising or falling during an extended period of time. As an investor, it is crucial to understand what part of the investment cycle you are in and adapt strategies to compensate for the current environment.

“Tweaking” a strategy is NOT the same thing as dumping one strategy for another. It is the modification of the current strategy to adapt to current conditions as they exist. For example, if your strategy is to buy stocks with low valuation multiples, that strategy must get modified during a long-duration secular bull market to account for a market environment where valuations are consistently rising for a long period of time.

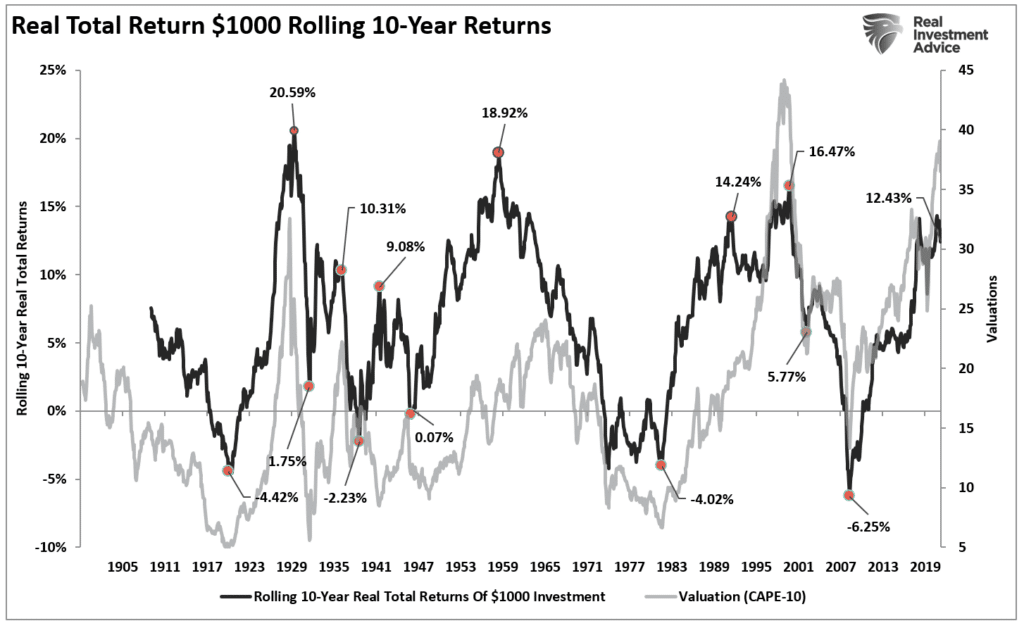

There have been 5 very long-term secular markets (15 years or more in length) since 1900. However, there are many short-term cyclical markets (1-3 years in length) within secular periods. Notably, during secular bear markets, there are bullish cycles that lure investors in only to destroy more capital. However, the same process is true in a secular bull market where sudden market downturns chase investors out of the market only to then reverse up leaving them behind.

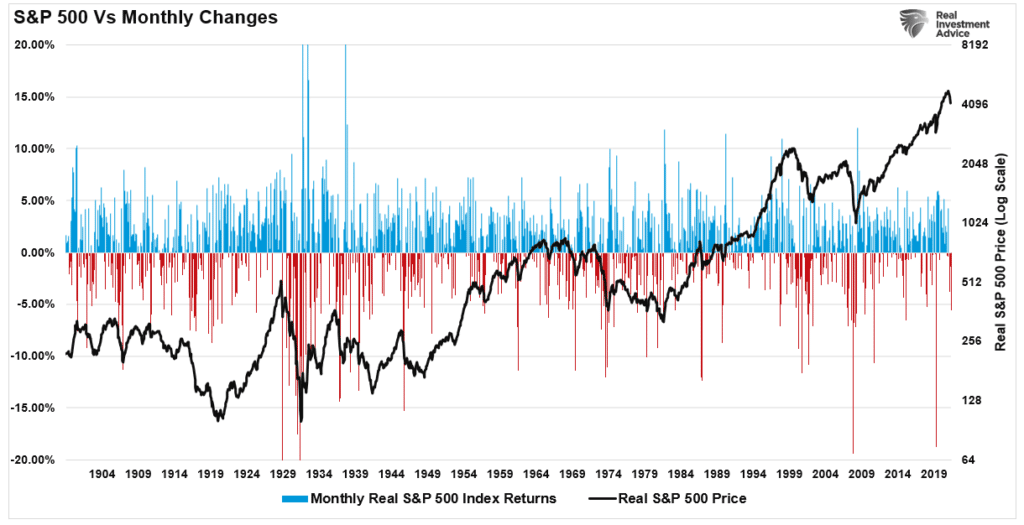

If you look at the chart above you will see that the markets have had very distinct cycles to navigate. At the peaks, when the markets are insanely expensive and general-stock P/E ratios are pushing 20x earnings or even higher, the returns going forward after these euphoric times are horrible.

After the 1929 peak, the US stock markets plunged and then traded sideways for almost two decades. The same thing happened again after the 1960s valuation peak.

Let me repeat that point for you: Between 1929 and 1982 a period of 53 years in total – 37 of those years were with little or no returns.

In other words, if you were 20 in 1929 you had one opportunity to make money in the markets before you were 73. The problem with that is that life expectancy was a bit shorter then.

If you look at the chart above it is easier to see the “cyclical” nature of the markets within the broader confines of the secular period. As you can see even during the broader confines of the “Secular” Bull and Bear market periods the monthly changes in the market can swing wildly in both directions. In fact, it is very difficult to discern any real predictive pattern other than monthly returns seem to be almost totally random.

Conversely, the hardcore contrarian approach is to not settle for fair value but to patiently wait until the general stock markets are undervalued in historical terms. If you are like Warren Buffett and buy at one-half historical fair value or 7x earnings, your reciprocal annual return (1/7) is a whopping 14.3%! This huge number compounded over three decades yields a final capital multiplier of a staggering 158 times!

That’s right, just by buying stocks at historically undervalued levels you can potentially multiply your capital by almost 158 times in 30 years! This compares to 16 times for buying at fair value and a dismal 4 times for playing the fool and buying at historically expensive levels. Buying stocks at expensive levels is almost a guarantee of pathetic long-term returns.

It makes no sense whatsoever to employ an investment strategy that may take 15 to 20 years to mature when your time horizon to retirement is only 10 years. This is why you must “tweak” your investment strategy to adapt your time horizon and strategy to the current market cycle.

Ultimately, different investment approaches are warranted, and applying the right methodology is half the battle. However, the most important part of the battle is to identify your time horizon and employ a risk profile that allows the market to work for you.

Commandment 7) Thou Shalt Maximize Thy Reward And Minimize Thy Risk

We have often related investing in the markets to playing a hand of “Blackjack” in Las Vegas. Good blackjack players can quickly identify when the potential of losing a bet to the house is in their favor or not. However, when it comes to investing, almost all investors have no ability to determine what their risk is relative to the potential for reward in any given investment.

Patience and discipline will help you determine the “when” to make an investment so that you can maximize the potential for making a profitable investment. If you’re patient and pick your spots, edges will emerge that provide an advantageous risk/reward profile. Proactive patience is a virtue. Investing with no understanding of risk is dangerous to your capital.

Remember, all investments are subject to the laws of gravity. What goes up will ultimately come back down. Therefore refer to Commandment 3 if you think you are “missing the boat”.

Commandment 8) Thy Perception Is Thy Reality

During very short-term periods in the market, identifying the prevalent psychology is a necessary process when investing. It’s not “what is,” it’s what’s perceived “to be” that dictates supply and demand.

While your longer-term investment strategy and discipline may dictate certain actions, there are periods in the market where the resident psychology will ignore economic, political, and fundamental realities. At such points, the demand or supply of investments available to investors may drive the markets further than rationality might suggest. As John Maynard Keynes once stated;

“The markets can remain irrational longer than you can remain solvent.”

It is during these periods of irrationality that your strategy and discipline are closely adhered to and that emotions don’t override the underlying premise of that strategy.

Commandment 9) Honor Thy Risk Profile

Many investors believe the “more risk they take, the more money they will make.”

In reality, the equation is rather simplistic. RISK = Potential For Loss

When investing over longer-term periods, investors should realize that for every percentage point of return sought over risk-free rates, the level of risk, or rather the risk of loss, exponentially increases.

In other words, investors should view risk as:

“How much money could I lose if my investment assumptions are wrong”.

Risk is measured by “Beta,” or the volatility, of a particular investment in relation to a benchmark or a norm. The wider the swings away from the norm the greater the probability for the investor to make an emotionally driven decision that ultimately leads to losses in the portfolio and the destruction of investment capital.

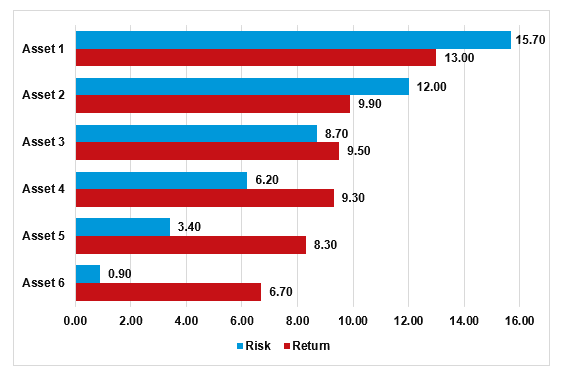

Therefore, controlling risk is a primary consideration in the conservation of your investment capital, even at the risk of missing an investment opportunity. The chart below is of 6-different asset classes with varying degrees of risk and return over long-term periods.

The BLUE bar is the average return of a particular investment over a long-term period, while the RED bar is the standard deviation or volatility of holding that investment. For example: If you look at Asset 6, you will see that during the holding period, the average annualized return was 6.7% with a very low standard deviation of 0.9%.

So, let’s assume for the moment that you are an investor who determines that you need an average annualized return of 8% to reach your investment objective over the next 20 years. The obvious choice is to put all your money into Asset 5 as it will give you an 8.3% rate of return with a very low level of risk.

However, note that if you want to increase your investment returns by 1%, you could invest your money into Asset 4 and receive a return of 9.3%. However, the level of risk increases not by 1%, but by 100% as the standard deviation from the norm moves from 3.4% to 6.2%.

Should you decide to invest in Asset 1, your risk, or potential for loss, increases by 500%.

What is important for you to extract from the chart above is that there is not a direct correlation between an increase in return and the amount of risk taken to achieve that return. In actuality, there is an exponential increase in the “risk” taken for each additional percentage point of return expected in a particular portfolio allocation.

Commandment 10) Thou Shall Not Kill Capital With Bad Investments

Rationalization has no place in investing. Every investment decision should be controlled by both a profit and protection motive. The basic premise is to cut losers short and let winners continue to win in your investment strategy. Remember, the goal of investing is to get MOST of your investment decisions right…not ALL.

Too many investors think that if a position doesn’t work, then they are not good investors. In reality, it is the nature of investing. Sell losing positions and move on to more profitable investment opportunities, rather than building a portfolio of losing positions over time and “hoping” they will regain value someday. Odds are they won’t in the short-term and the opportunity costs could be very high.

Why Investors Fail

The first thing that we do with each and every client that walks in our door is to establish their investing goals. More often than not investors have no idea what their money is supposed to be doing for them on a daily basis. For the most part, they think that if they buy stocks, those investments will ultimately go up and make them wealthy.

That is an incorrect assumption.

The reason we invest our “savings,” is to ensure those savings adjust over time to compensate for inflation. In other words, we want our savings to maintain their “purchasing power parity.”

As such, without a clear understanding of investment goals, investors generally take on too much risk and make investment decisions based on emotion rather than a strategy.

If you want to be happy, the first thing you need to do is eliminate that which is making you unhappy—all of the comparisons. Clients who have learned the wisdom of “enough” are content. Their benchmark is not an artificial one, but one based on their own goals and risk tolerance. They are comfortable that risk-managed returns will get them from Point A (where they are now) to Point B (retirement). They invest to obtain their goals with as little risk as possible.

The lesson we want to drive home here is the danger of following Wall Street’s advice of beating some arbitrary index from one year to the next. What most investors are taught to do is to measure portfolio performance over a twelve-month period. Such is absolutely the worst thing you can do. It is like being on a diet and weighing yourself every day.

The mistakes that most of us make are very mundane. First and foremost is chasing performance. Study after study shows the average investor does much worse than the average mutual fund, as he switches from his poorly performing fund to the latest hot fund just as it turns down.

Past performance is pretty much worthless when it comes to trying to figure out the future. The best use of past performance is to determine how a manager behaved in a particular set of prior circumstances.

- How did he perform during a market advance?

- Did he preserve capital during a market downturn?

- Could you have withstood the volatility of the fund?

These are the important questions to ask. Yet investors always read that past performance is not indicative of future results, and then promptly ignore it. It is like reading statements at McDonald’s that coffee is hot. Most just don’t pay attention.

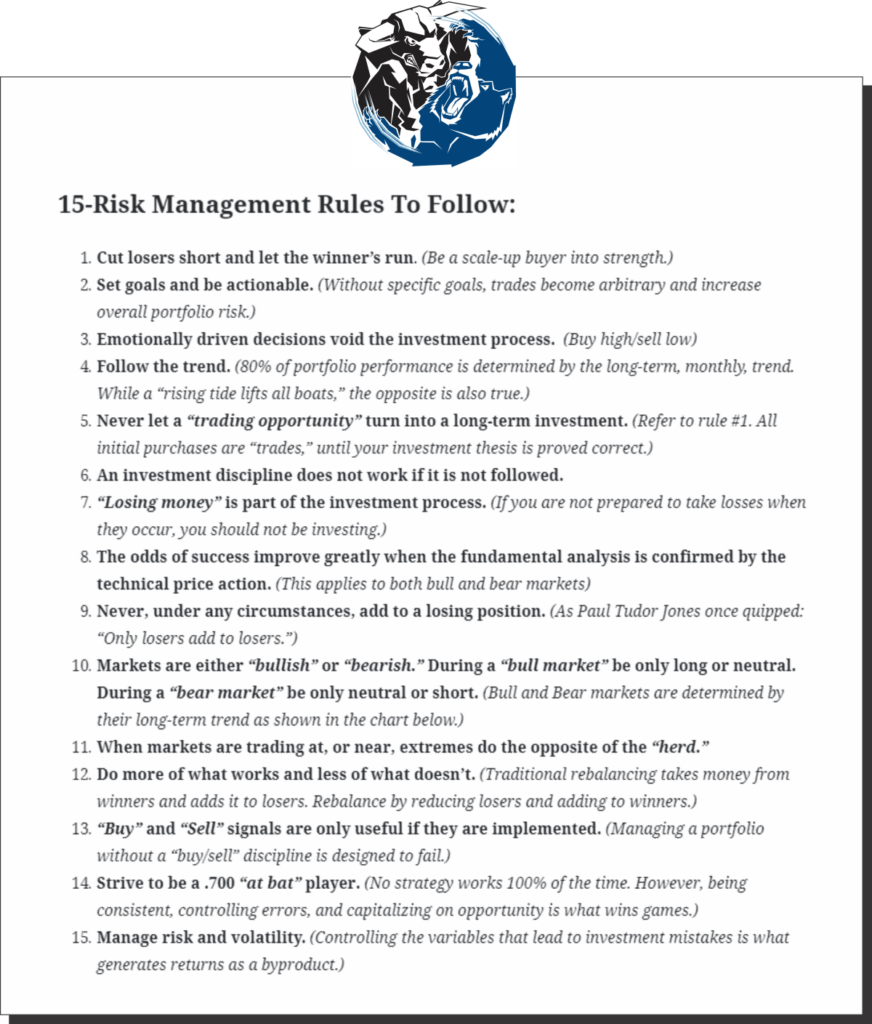

Here is a list of the trading rules we have developed over the last 30 years.

There are obviously more rules, but I’ve found these to be the common thread through the years. Each and every investor has a unique risk profile and time horizon, so some of these commandments just may not apply.

However, as always, I share these thoughts with the hope it adds value to your process. The most important point to take away from this article is to find a strategy that works for you, but allows for a margin of error so you can maintain it over time with discipline.

No approach is failsafe – for if there wasn’t risk, it would be called “winning,” not investing