Jaret Seiberg of Cowen & Co. wrote an interesting report pointing to the potential of a credit crunch for mortgages. In his recent article highlighted by Bloomberg, he discusses four factors that will make mortgage lending by banks and other financial institutions more difficult. This is not an immediate problem but one that might start to appear next year. We summarize Jaret’s factors that might cause a mortgage credit crunch below.

- The government appears unlikely to ensure non-banks remain important mortgage credit providers. Subsequently, less competition for banks results in higher mortgage rates.

- The latest Basel 3 proposal increases the risk weighting on mortgages. If banks have to hold more collateral/capital against mortgage credit, mortgage loans will be less profitable to originate.

- Banks are sitting on losses on their mortgage books due to higher rates. Such “could cause banks to retrench.“

- The capital charge for banks to provide warehouse lines to mortgage lenders is expensive. Therefore banks may likely raise rates for warehouse lines or reduce the amount of said loans. This, too, will make mortgage origination more costly for most non-bank lenders.

The bottom line is that offering mortgages to clients will be more costly; consequently, fewer participants are likely to offer loans. Less competition and higher mortgage rates may likely negatively impact home prices.

What To Watch Today

Earnings

Economy

- No notable reports today

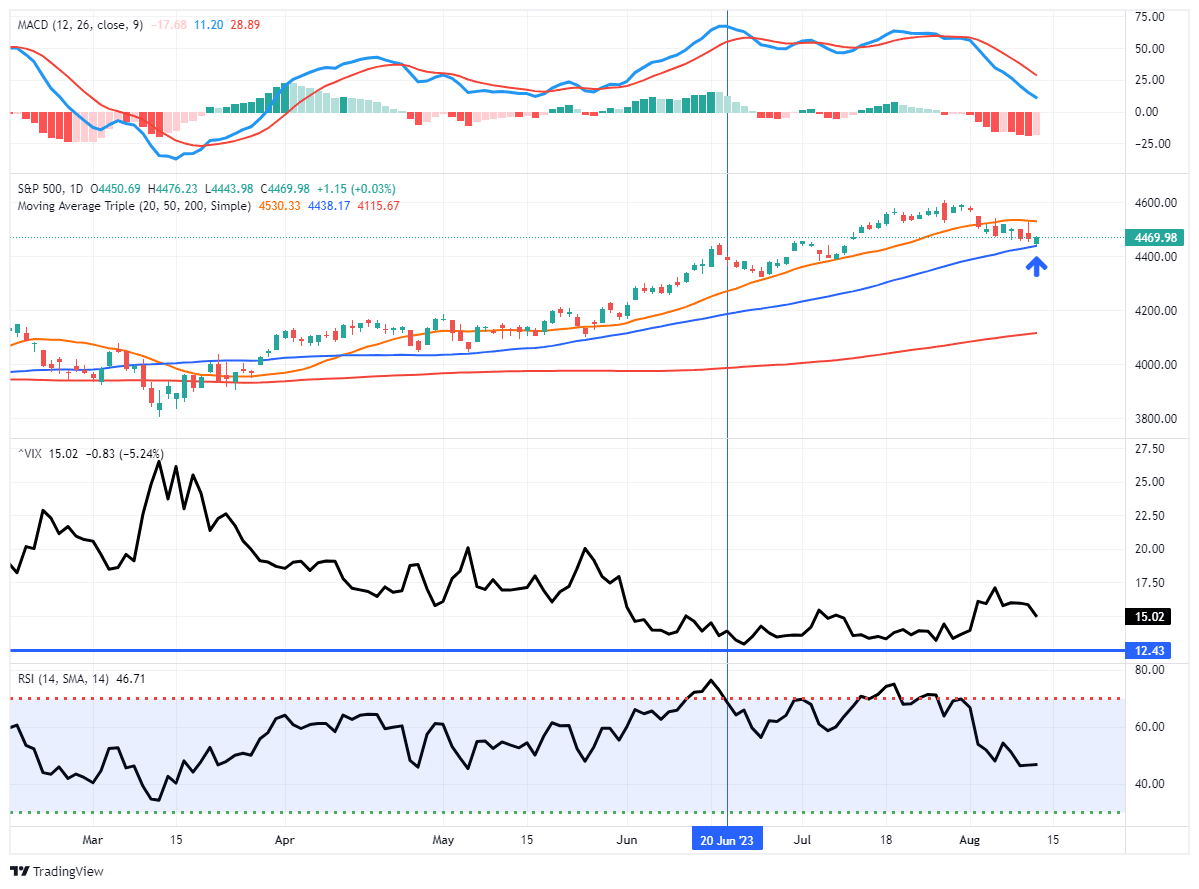

Market Trading Update

The market took a breather this past week as earnings season begins to wind down. Such was expected, as discussed in last week’s commentary. To wit:

There are several vital points in the chart below.

- The negative divergence of the MACD and RSI was a warning sign of an impending correction. All that was needed was a catalyst to spook buyers: the debt downgrade.

- There was a significant uptick in the volatility index for the first time since May. (As discussed in “Complacency”)

- Moving average support levels are important indicators of the potential depth of the correction.

The chart was updated through Friday’s close.

As stated, the breather from the 5-month advance was unsurprising, and this week’s inflation reports, both within expectations, did little to change the course of the Federal Reserve in the short term. The “market breather” remains within a consolidation range between the rising 20- and 50-day moving averages. On Friday, the market successfully tested and held the 50-DMA. If the market falls below the 50-DMA, which is possible, this breather becomes a correction, and the 100-DMA becomes the next level of logical support.

The market has done very little wrong so far. As such, we continue to suggest using this correction to add exposure to portfolios when the current “sell” signals reverse. With earnings season mostly behind us, the market’s focus will turn to the upcoming Jackson Hole Summit and Jerome Powell’s speech which will be parsed for clues as to upcoming changes to Fed policy.

There is a reasonable risk that Mr. Powell could disappoint the bulls again as he did last year. We will have to wait and see.

The Week Ahead

Retail Sales data tomorrow will be the highlight of the week. Expectations are for a 0.2% increase. Such would entail that real retail sales are declining. Jobless Claims picked up slightly last week to 248k. It is still relatively low, but jobless claims are the best leading indicator of employment furnished by the government.

Wednesday will see the release of the FOMC minutes from their July meeting. Therefore, with the coming late August Jackson Hole Fed Summit, it will be telling to see if they leak any new policy or economic thoughts. Might their view on inflation be changing? Are they concerned that higher Treasury rates are putting significant pressure on the deficit? Would they discuss yield curve control (YCC) to help limit increases in long-term rates? These summits are often the stage for big policy announcements, which are usually leaked to some degree beforehand.

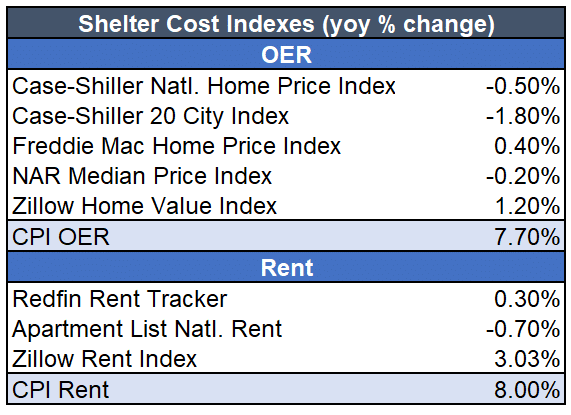

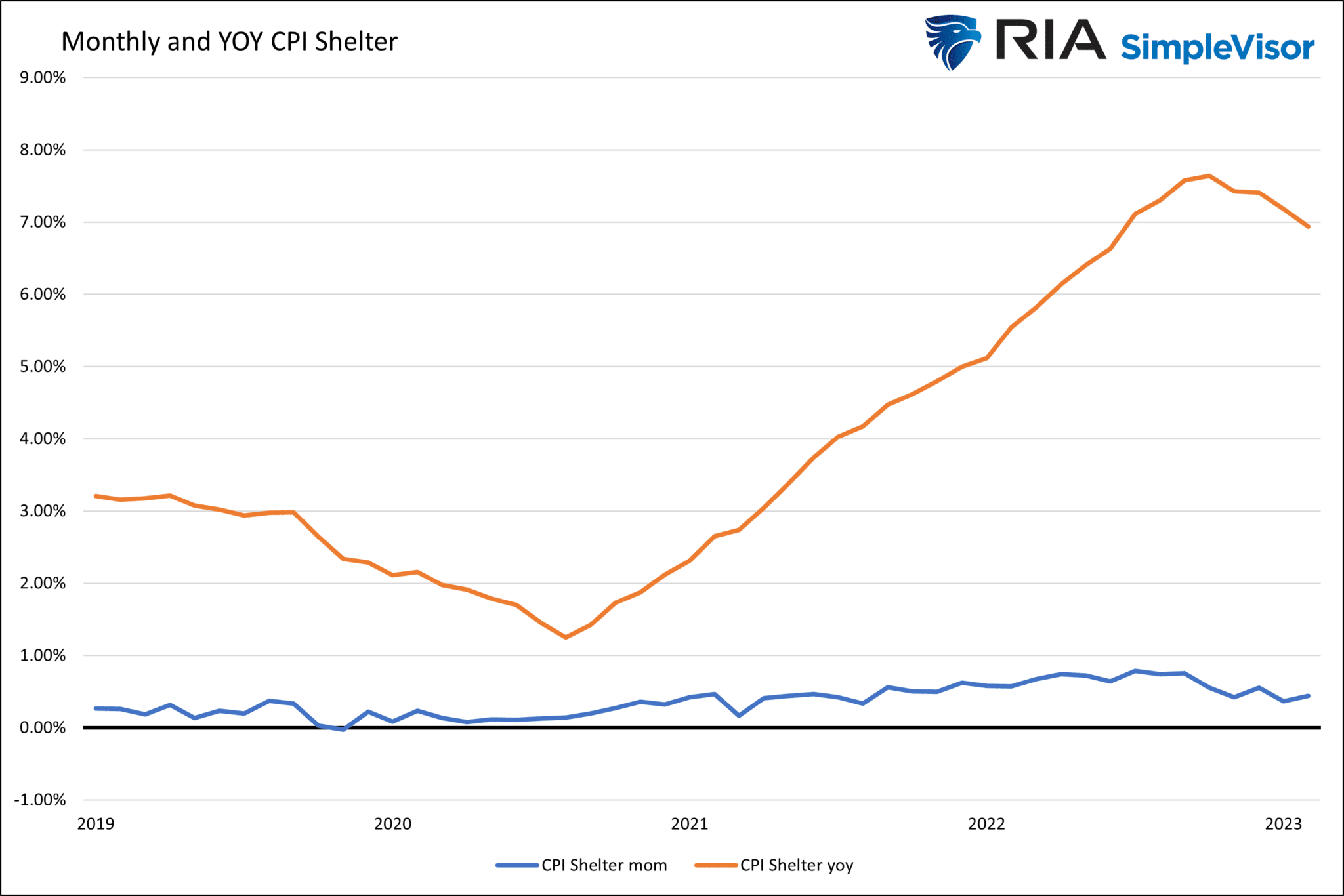

CPI Is Lower Than Advertised

The Fed’s next move and their “higher for longer” policy are all predicated on high and sticky inflation. Inflation has been declining nicely but not enough to sway the Fed to cut or stop raising rates. For rate cuts, they seem intent on meeting their 2% inflation goal or a recession.

What if we told you that effectively CPI was already at 2%? What if the data used to compute CPI lags reality by a significant amount? And the largest component accounts for a third of CPI. We will detail this in a coming article, but we want to share a graph and table below to whet your whistle. The table shows the BLS measure of shelter is well above many other private sector measurements that are essentially real-time. The second graph shows that CPI -Shelter prices are turning lower but still at lofty levels. If the private sector shelter costs were instead used, what would happen to CPI?

PPI

Unlike CPI, PPI came in slightly above expectations. The monthly rate was +0.3%, the highest monthly print since last November. That is also higher than last month’s downwardly revised 0%. The core monthly was 0.2% which was in line with expectations. The year-over-year core PPI data, the Fed’s favorite gauge of producer prices, is now at 2.4%, down a tenth from last month. As shown below, PPI has largely retraced back to pre-pandemic levels. PPI tends to lead CPI.

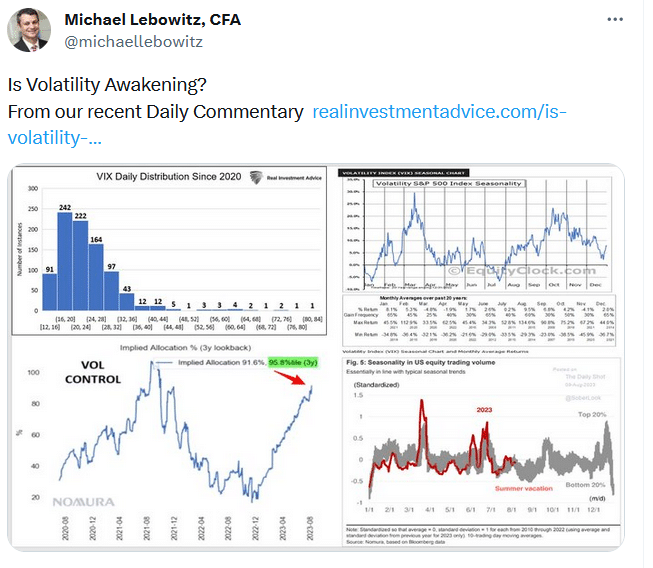

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read