With the midterm elections behind us, does the market outlook improves given a now gridlocked Congress? Historically speaking, such is the case. As noted by Michael Cannivet via Forbes:

“Before you hit the panic ‘Sell Everything’ button, though, it’s worth considering at least one bullish catalyst on the horizon—voters head to the ballot box on November 8th.

The data is clear: Midterm elections are historically bullish for the stock market.”

While garnering less attention than a presidential election, midterm elections are important because they could lead to a change in control of the U.S. Senate and House of Representatives. Such can significantly impact policy, laws, and foreign relations. Historically, markets tend to favor “gridlock” in Washington as it dramatically reduces the risk of an adverse policy change regarding taxation, geopolitical conflict, or substantive changes to spending and debt.

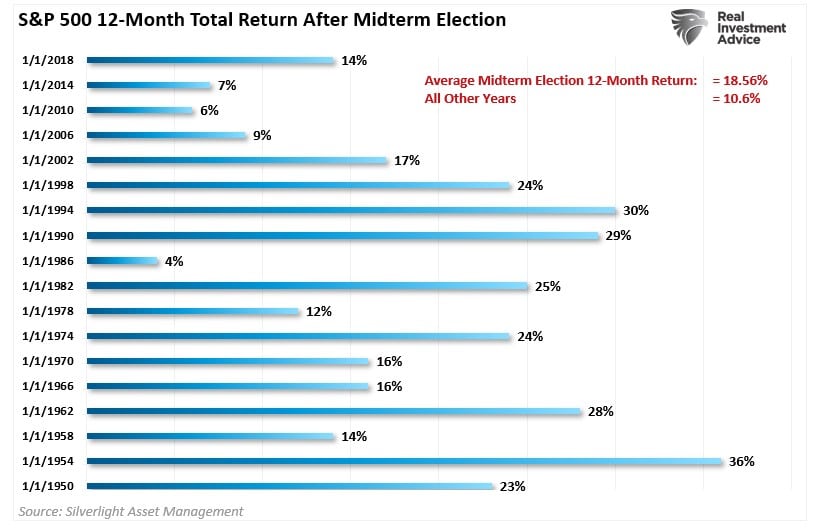

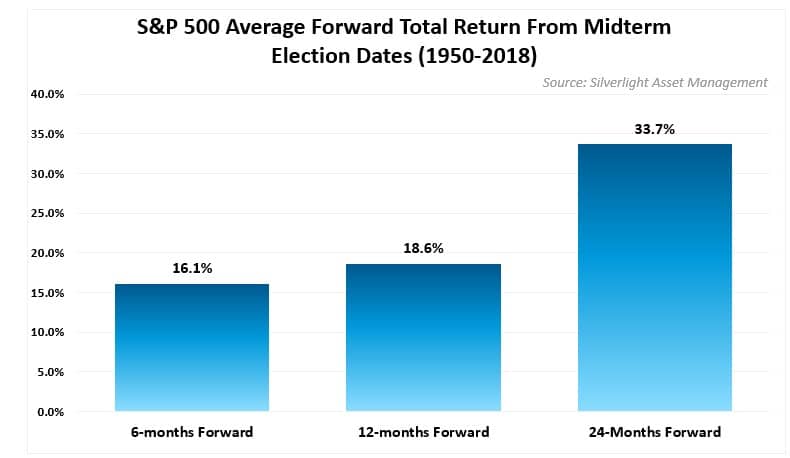

Since 1950, there have been 18 midterm election cycles, and in the twelve months following each of those cycles, the stock market has had positive returns. Over the subsequent 12 months, stocks delivered an 18.56% average annualized gain compared to just 10.6% over all other years.

Over a more extended 24-month period, stocks returned an average of 33.7% after a midterm election.

However, while the data above goes back to 1958, the last time the S&P 500 produced a negative return over the 12 months following a midterm election was 1939. Of course, there was a massive economic contraction and uncertainty at that time as the U.S. battled the Great Depression and World War II began in Europe.

Another period of interest is the late 1960s and 1970s, marked by slow economic growth, high unemployment, rising energy prices, and significant inflation. Given the similarities currently, the bearish pre-midterm market returns and an un-accommodative Federal Reserve, the outlook, while bullish, is less clear.

Getting Back To Even Is Not The Same Thing

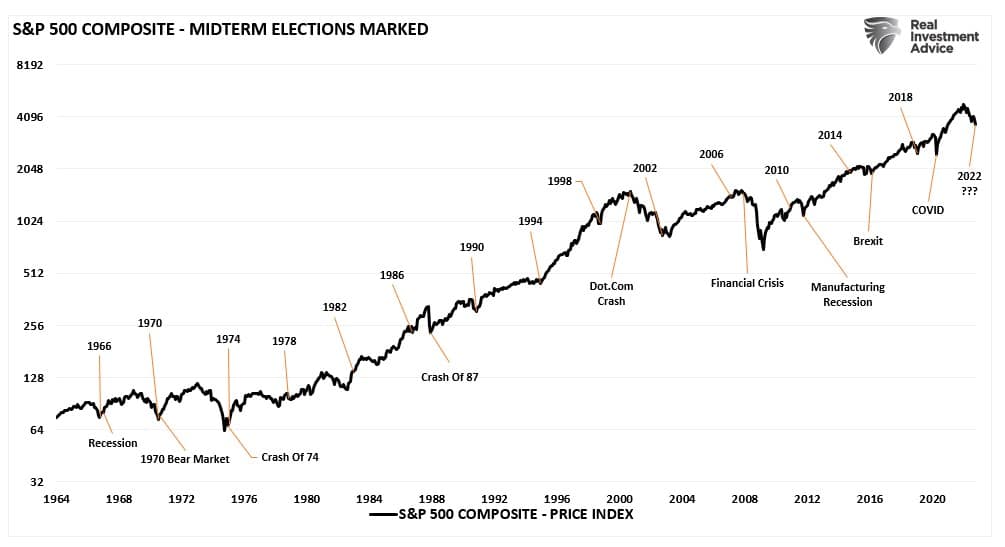

There are a couple of caveats to this analysis that must be considered. The first is that while returns tend to be positive post-midterm elections, several times, it coincides with when the midterm elections fell. The chart below shows the S&P 500 with the years of midterm elections marked and significant events.

For example, in 1966, 1970, and 1974 the midterm elections coincided with the bottom of the three recessionary bear market cycles. Coincidence? Probably. More importantly, on a longer-term basis, returns on a “buy-and-hold” basis were negative as the secular bear market continued. We see the same effect between 1998 and 2014, midterm elections yielded positive short-term results, but long-term returns were near zero.

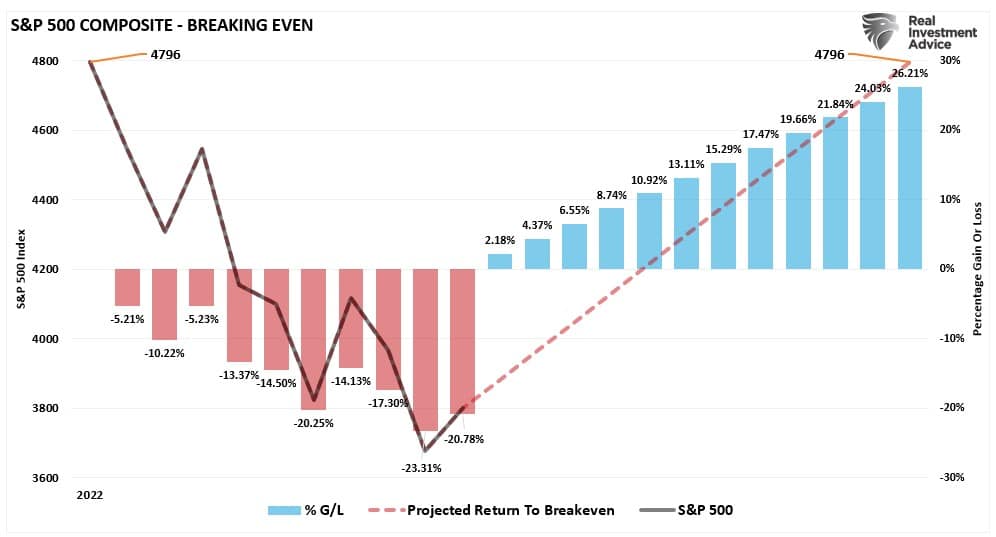

The second caveat to the historical data is the difference between making money and getting back to even. While the mainstream analysis suggests investors should buy the midterm elections for positive 12-month returns, most are already invested. In a year where the midterm elections fall in the middle of a bear market, like 1974, 2002, or 2022, most investors used those returns to “get back to even.”

The chart below shows the S&P 500 for 2022, starting at 4796. It will require a return of 26% over the next 12 months for investors to break even. Notably, that does not include the rate of return necessary to meet their financial goals. For example, if your financial plan requires 6% annualized returns, the 26% advance still leaves you another 12% short of your annual return goals (6% for 2022 and 2023). Given the average yearly return post-midterm elections is 18.6%, investors will fall short of their goals.

While I am not discouraging you from taking advantage of a robust post-midterm election rally, there is a vast difference between “getting back to even” and “making money.”

The Difference This Time May Be The Fed

While the history following midterm elections is bullish, there is a difference this time that could produce a less-than-optimistic outcome. That difference is Fed and their current fight against inflation. We have previously discussed the “lag effect” of monetary policy and its impact on economic growth and earnings. To wit:

“As the Fed continues to hike rates, each hike takes roughly 9-months to work its way through the economic system. Therefore, the rate hikes from March 2020 won’t show up in the economic data until December. Likewise, the Fed’s subsequent and more aggressive rate hikes won’t be fully reflected in the economic data until early to mid-2023. As the Fed hikes at subsequent meetings, those hikes will continue to compound their effect on a highly leveraged consumer with little savings through higher living costs.

Given the Fed manages monetary policy in the “rear view” mirror, more real-time economic data suggests the economy is rapidly moving from economic slowdown toward recession.”

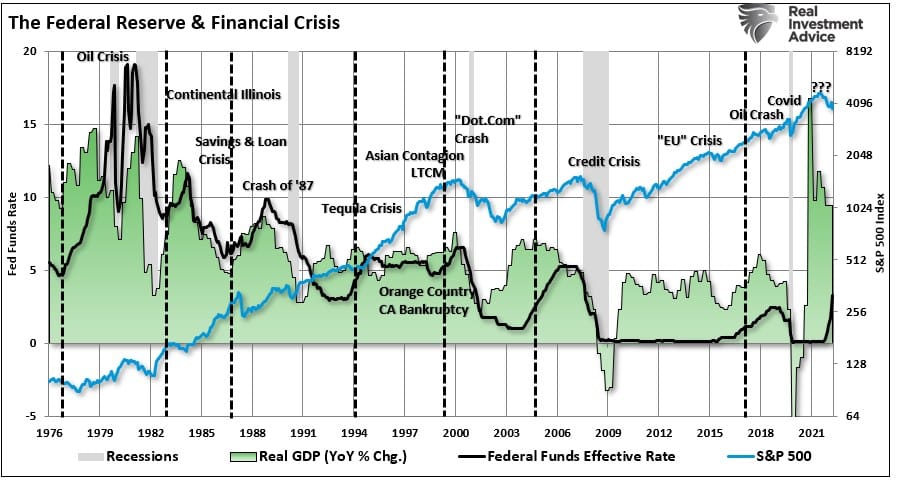

Currently, the Fed is still tightening monetary policy to further slow economic growth. As shown, when the Fed has previously stopped hiking rates, forward stock returns tended not to be robust.

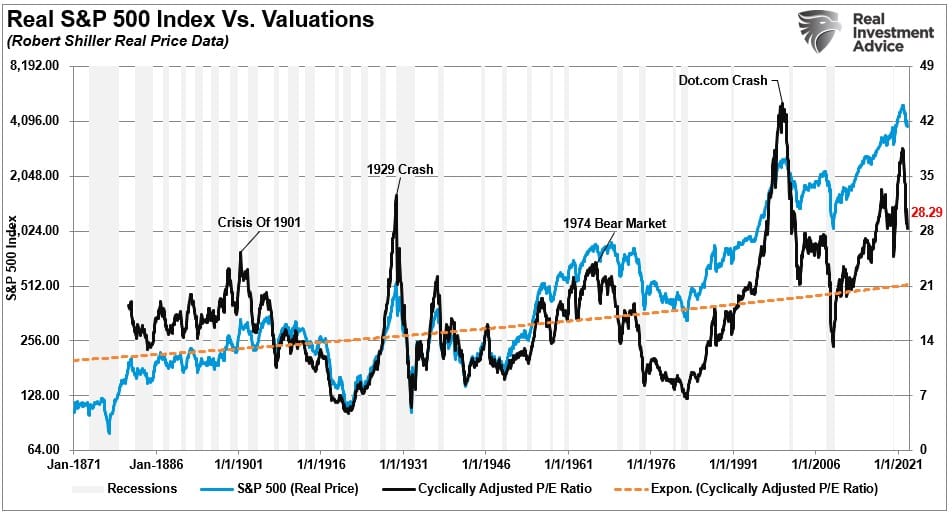

Another difference is that previous market lows, which coincided with bear markets and midterm elections, were low valuations. Despite the market decline in 2022, valuations remain elevated relative to historic market bottoms.

Given the more extreme negative market sentiment, a substantial rally is undoubtedly possible through year-end and early 2023.

However, we suspect following that, the market environment will become more challenging. Particularly as the Fed’s monetary tightening becomes more evident in slower economic activity, declining inflation, and slower earnings growth. If that is the case, asset prices, and ultimately valuations, will need to drop before the final market low.

There are no guarantees in the financial market. While history certainly supports the bullish outlook, it should not be considered gospel. Bull markets happen in bear markets. However, many factors could negatively impact returns over the next 12- to 24 months. As such, investors should measure and manage their risk accordingly.

The good news is the negative backdrop will pass, and longer-term returns will become evident. Of course, to participate in the next bull market, you must ensure you survive the bear market.

This returns me to my main point. Spending the next bull cycle “getting back to even” is not the same as making money.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read