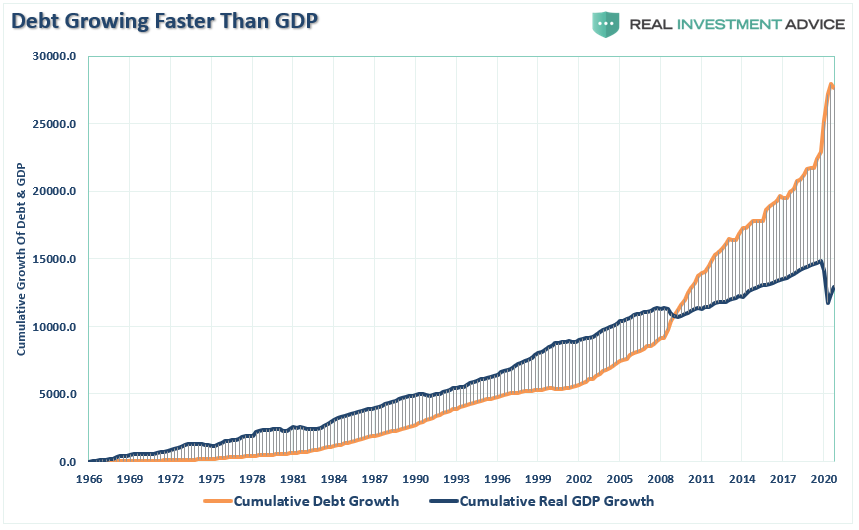

We have frequently discussed the “one-way trip” of American debt and the long, slow slide into the “Japanification” of America.

The amount of outstanding debt, and the subsequent deficit, has long been a problem in the U.S. For the last two decades, policymakers have made annual promises for more substantial economic growth. Yet with each passing year, growth rates weaken, and economic prosperity worsens. As we discussed pre-pandemic in “Economy Should Grow Faster Than Debt:”

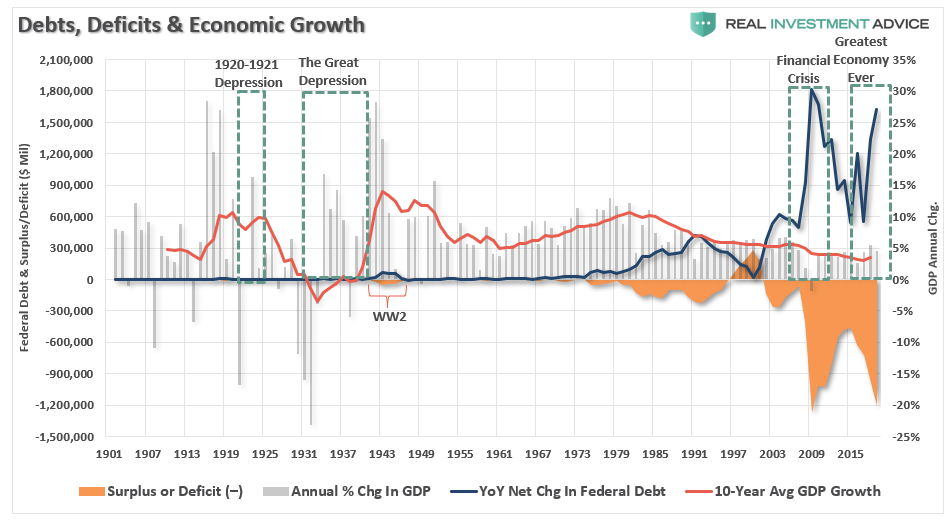

“The chart below shows the deficit, 10-year average GDP growth, and the annual change in Federal Debt. The problem should be obvious. Since the Federal government began ramping up debt, and running deficits, growth continues to deteriorate. Such is not a coincidence.”

“The government is already running a massive deficit. It also expects to issue another $1.5-2 Trillion in debt during the next fiscal year. The efficacy of ‘deficit spending’ in terms of its impact on economic growth has been greatly marginalized.”

Spending Without Controls

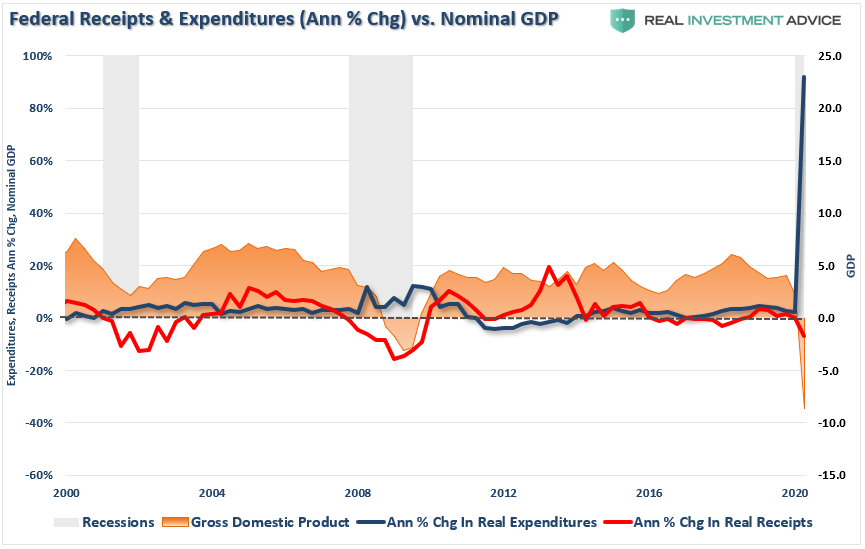

Since then, Government debt surged n response to the “Coronavirus Pandemic,” to provide fiscal support. Concurrently, the drop in economic activity has dramatically reduced Federal revenues to pay for it all.

Unfortunately, this also means the CBO’s already catastrophic long-term debt forecast has become even more disastrous. It already requires over 100% of all Federal revenues to cover mandatory spending. Such was a point in the most recent Long-Term Budget Outlook report from the CBO.

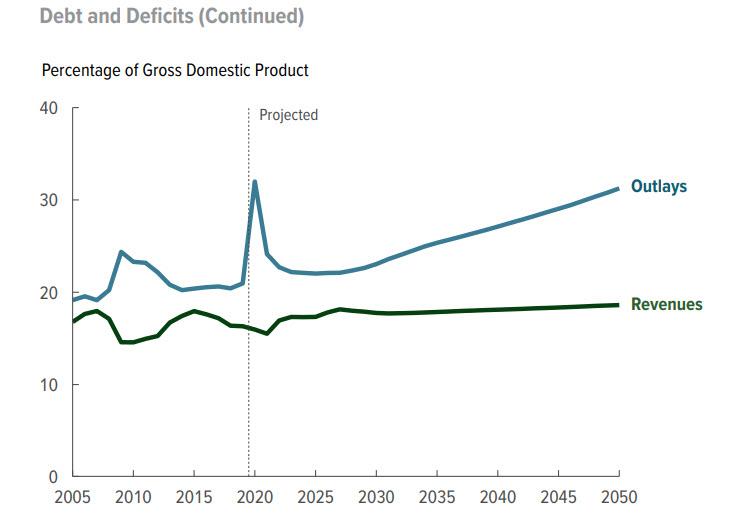

“Once the effects of decreased revenues associated with the economic disruption caused by the pandemic dissipate, revenues measured as a percentage of GDP will rise. After 2025, CBO’s projections increase largely due to scheduled changes in tax rules. Such includes the expiration of nearly all of the changes made to individual income taxes by the 2017 tax act. After 2030, they continue to rise. But that growth does not keep pace with the growth in spending. Most of the long-term growth in revenues is attributable to the increasing share of income that is pushed into higher tax brackets.” – CBO

Deficits Set To Grow

Of course, to fund the excess spending by the Government, the debt burden and subsequent debt service will continue to grow.

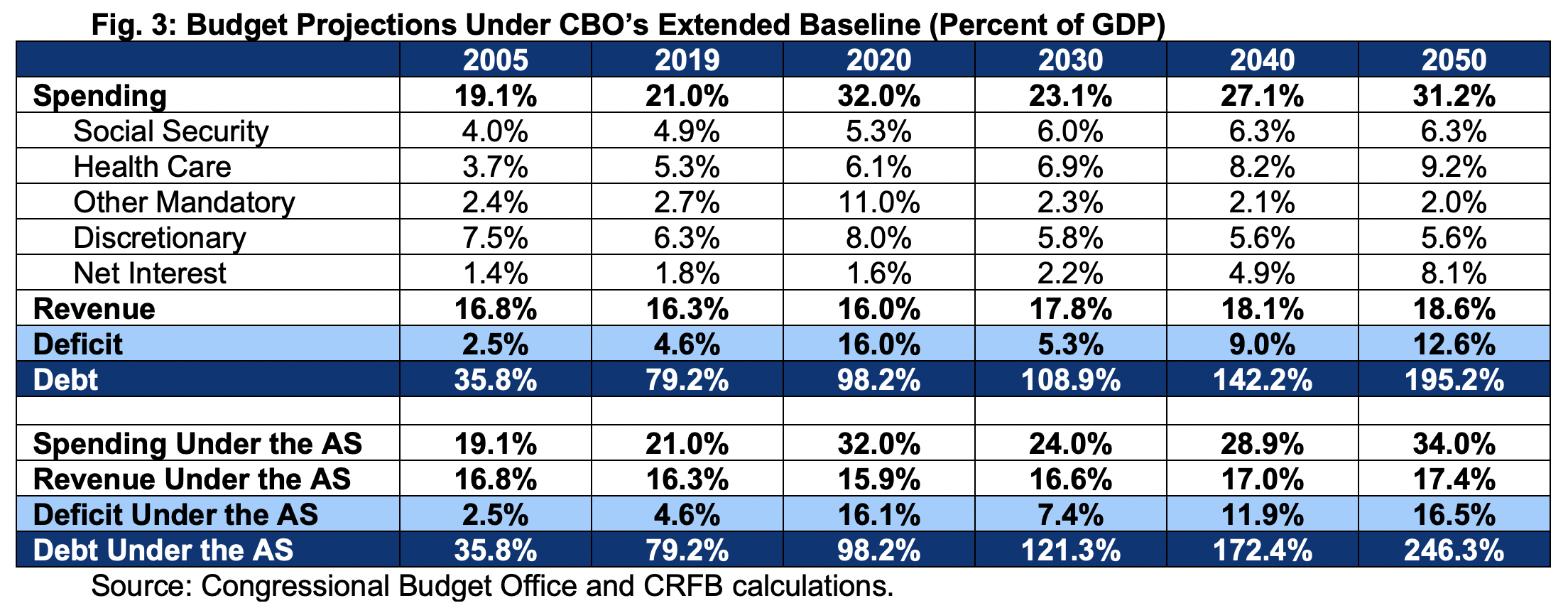

“Deficits increase again in the last few years of the decade, reaching 5.3 percent of GDP in 2030. That level is historically high and more than one-and-a-half times the average over the past 50 years (3.0 percent of GDP).

In the second and third decades of CBO’s projection period, deficits grow from 5.3 percent of GDP in 2030 to 9.0 percent by 2040. They hit 12.6 percent by 2050. Over that 20-year period, deficits average 9.0 percent of GDP, which is higher than their 50-year average of 3.0 percent of GDP.” – CBO

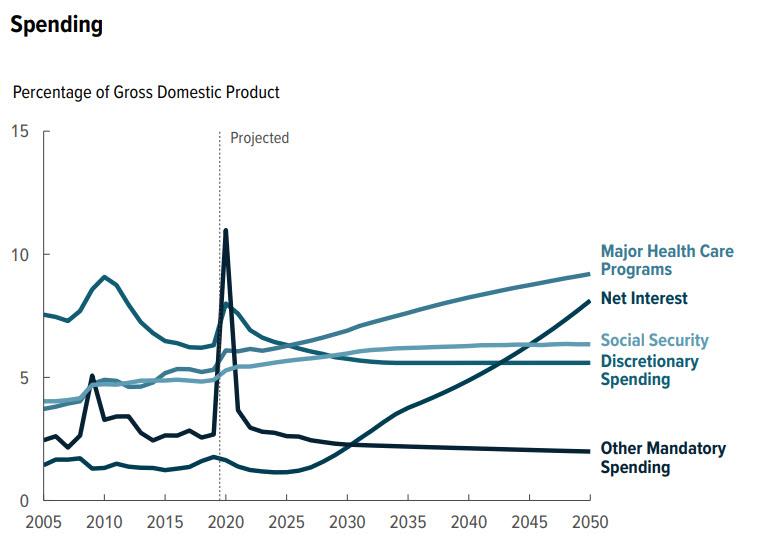

Spending Set To Increase

Note what is driving the deficit. The mandatory spending, comprised of Social Security, Medicare, Medicaid, prescription drug benefits, and the Affordable Care Act, also includes interest on the debt.

Given rising debt levels erode economic growth, as it displaces revenue from productive uses, debt continues to grow to support “mandatory spending” requirements.

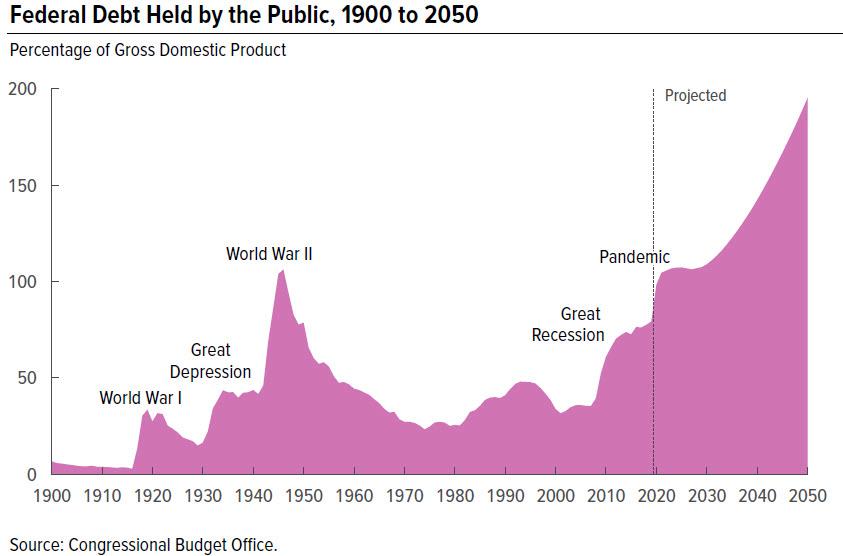

“Debt continues to increase in most years thereafter, reaching 195 percent of GDP by 2050. That amount of debt will be the highest in the nation’s history, and will increase further. High and rising federal debt makes the economy more vulnerable to rising interest rates and, depending on how the debt is financed, rising inflation. The growing debt burden also raises borrowing costs and slows the growth of the economy and national income. There is an increased risk of a fiscal crisis or a gradual decline in the value of Treasury securities.” – CBO

As the CBO further explains:

Debt as a percentage of GDP will increase in most years as the government incurs budget deficits larger than the growth of the economy. If current laws generally remain unchanged, federal deficits will be substantially larger over the next 30 years than over the past 50 years. In CBO’s projections, deficits rise after 2030 as mandatory spending, outlays for the major health care programs, and interest payments grow faster than revenues.

Debt Likely To Be Worse

The Committee For A Responsible Federal Budget just released the following analysis:

“Projected debt in 2050 is nearly five times higher than the 50-year average of 42 percent of GDP. It will be on track to double the previous record of 106 set just after World War II. In dollar terms, debt will rise from nearly $21 trillion today to $121 trillion by 2050.”

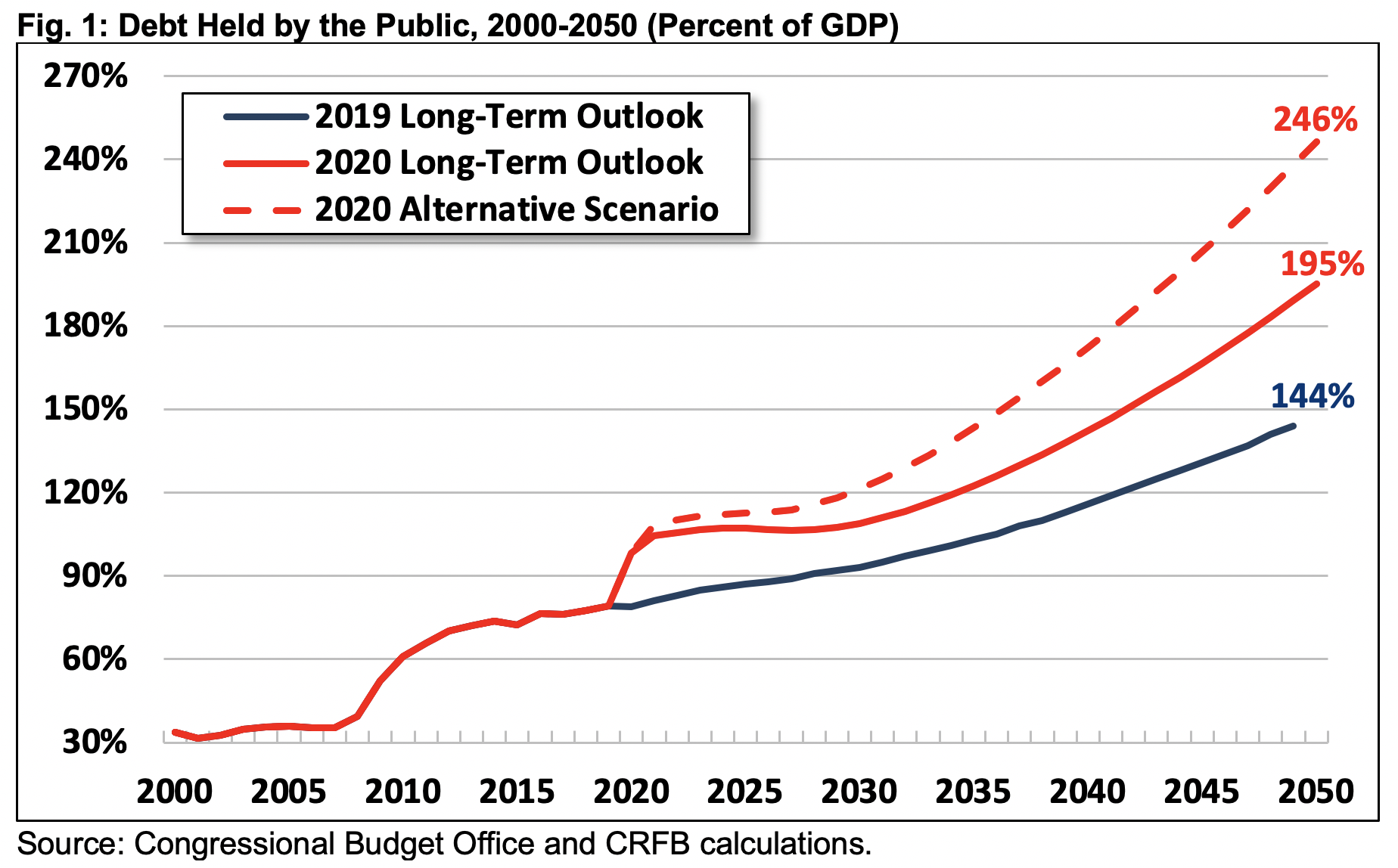

“Actual debt levels could grow significantly faster than CBO forecasts. Under our alternative scenario, debt would reach 246 percent of GDP in 2050.

Even under current law, high and rising debt represents a large fiscal gap. For example, CBO estimates policymakers would need to enact 3.6 percent of GDP in spending cuts and tax increases starting in 2025. Such actions could restore the debt to 2019 levels by 2050. That’s the equivalent of cutting all spending by one-sixth or increasing all revenue by one-fifth.”

Neither of those things will happen.

Spending Will Be Higher

As we showed previously, at the end of 2019, we were already spending more than we brought in.

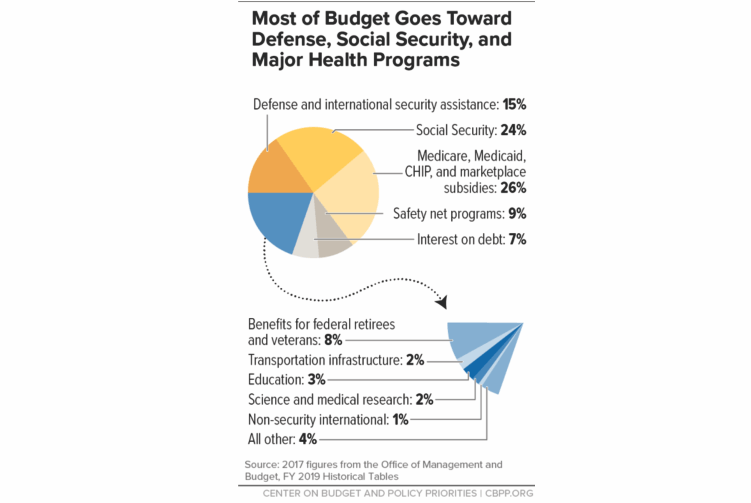

“According to the Center On Budget & Policy Priorities, roughly 75% of every tax dollar goes to non-productive spending.”

“Here is the real kicker. In 2018, the Federal Government spent $4.48 Trillion, which was equivalent to 22% of the nation’s entire nominal GDP. Of that total spending, ONLY $3.5 Trillion was financed by Federal revenues and $986 billion was financed through debt.

In other words, if 75% of all expenditures is social welfare and interest on the debt, those payments required $3.36 Trillion of the $3.5 Trillion (or 96%) of revenue coming in.”

The CFRB report expands on this analysis with future projections.

Rising debt and deficits are driven by a disconnect between spending and revenue. CBO expects spending to grow rapidly over the next three decades and revenue to grow gradually.

The 11.7 percent of GDP growth in Social Security, health, and interest costs explains more than the entire 10.3 percent growth in total spending through 2030. Meanwhile, revenue will only grow by 2.3 percent of GDP – failing to cover the rising cost.

Here is the real problem as we advance:

Rising health and retirement costs and insufficient funding also puts trust funds in danger. On a combined basis, CBO estimates the Social Security trust funds will run out in calendar year 2031 and face a 75-year shortfall of 1.6 percent of GDP, or 4.7 percent of taxable payroll.

Slower Economic Growth

The underlying structure of the economy continues to weaken as non-productive debt erodes growth. As discussed just recently in “Debts, Deficits & The Path To MMT:”

“The relevance of debt growth versus economic growth is all too evident. When debt issuance exploded under the Obama administration and accelerated under President Trump, it has taken an ever-increasing amount of debt to generate $1 of economic growth.”

Such reckless abandon by politicians is simply due to a lack of “experience” with the consequences of debt.

However, as the CFRB stated:

“Unfortunately, the actual fiscal situation could turn out to be even worse than CBO projects.

CBO estimates stabilizing debt at 2019 levels would require annual tax and spending adjustments between 2025 and 2050. Such would be equivalent to 3.6 percent of GDP. A carefully crafted package could be phased in gradually, targeted to ask the most from those who can best afford it. It could be designed to improve economic growth and thus reduce the burden of any adjustments. However, there is no magic wand we can wave to fix these problems

While policymakers should prioritize addressing the current pandemic and economic crisis, they cannot and should not continue to ignore our dangerous long-term fiscal situation.”

Ratcheting Growth Down Again

As the CFRB states, ignoring the issue will only lead to longer-term declines in economic growth and prosperity.

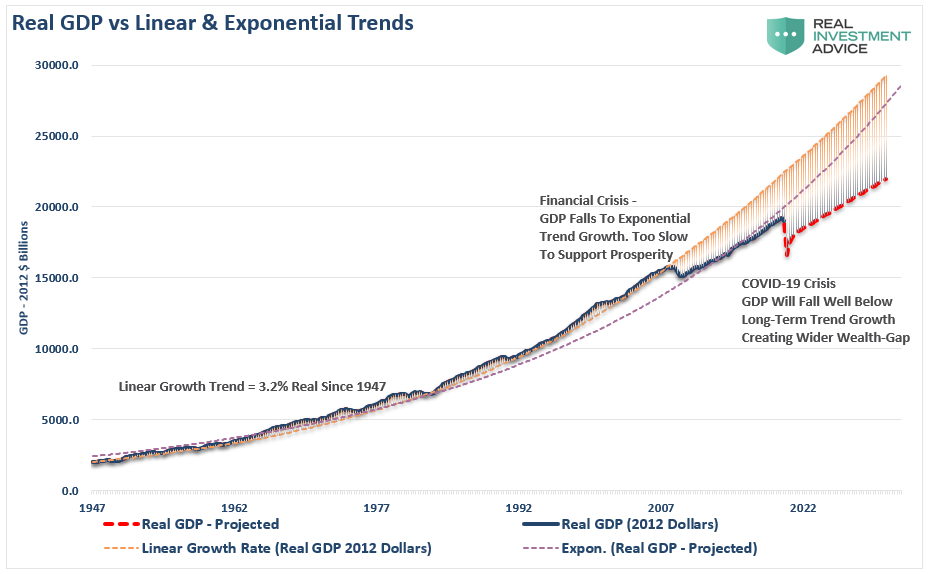

Before the “Financial Crisis,” the economy had a linear growth trend of real GDP of 3.2%. Following the 2008 recession, the growth rate dropped to the exponential growth trend of roughly 2.2%. Instead of reducing the debt problems, unproductive debt and leverage increased.

The “COVID-19″ crisis led to a debt surge to new highs. Such will result in a retardation of economic growth to 1.5% or less, as discussed recently. Simultaneously, the stock market may rise due to massive Fed liquidity, but only the 10% of the population owning 88% of the market benefits. In the future, the economic bifurcation will deepen to the point where 5% of the population owns virtually all of it.

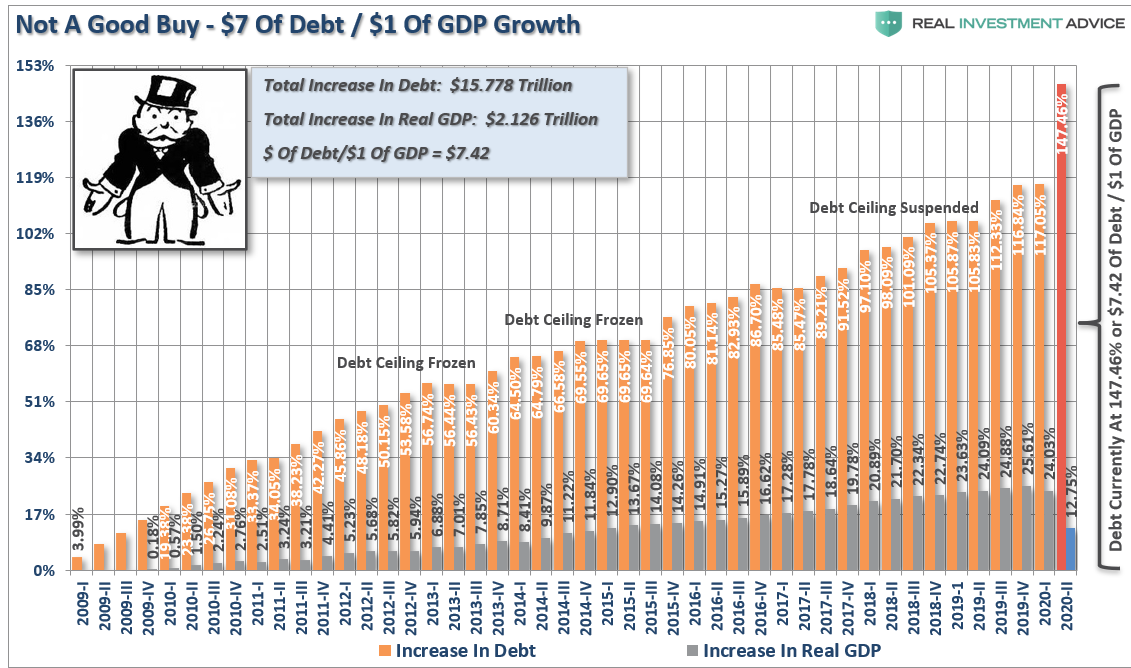

As I noted previously, it now requires $7.42 of debt to create $1 of economic growth, which will only worsen as the debt continues to expand at the expense of more robust rates of growth.

That is not economic prosperity. It is a distortion of economics.

Hypocritical

The CBO’s latest budget projections confirm what we, and the CRFB, have been warning about. The current Administration has taken a path of fiscal irresponsibility, which will take an already dismal fiscal situation and made it worse.

While “conservative” Republicans continually chastised the previous Administration for running trillion-dollar deficits, the Republicans have now decided trillion-dollar deficits are acceptable.

That is entirely hypocritical.

Given the flaws in the CBO’s calculations, their current projections of multi-trillion deficits next year, and exceeding that mark every year after, will likely turn out to be overly optimistic.

Notably, the projected budget deficits in the coming decade are “full-employment” deficits. Such is significant because, while budget deficits can help recessions by providing an economic stimulus, there are good reasons we should be retrenching during good economic times, including the one we are in now.

Conclusion

As President Kennedy once said:

“The time to repair the roof is when the sun is shining.”

Instead, we seem to have just removed the roof altogether.

The fact that debt and deficits had risen under conditions of full employment suggests a more profound underlying fiscal problem existed and has now worsened.

The CBO’s budget projections are a harsh reminder of the consequences of debt and deficits.

“The longer policymakers wait to fix the debt, the harder and costlier it will get. That fiscal gap would grow to 4.4 percent of GDP if action was delayed until 2030, or 5.9 percent if delayed until 2035. Delaying action means the necessary changes will be spread among fewer people. Policymakers will have less ability to carefully target adjustments. And ultimately, it will be harder to phase in new policies or give families and businesses time to prepare and adjust for them.” – CFRB

It is just a function of time until the “bill comes due.”

As we concluded previously, you can make choices today, which may be unpopular, and induce short-term pain for a more robust economy tomorrow. Or, you can wait until creditors force those painful choices upon you all at once.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read