It’s not just a handful of AI-related stocks that signal a speculative investment atmosphere. Many other stocks and markets are exhibiting similar behavior. For instance, Bitcoin and junk-rated corporate bonds show complacency and wild speculation. While both markets are inherently very different, traders and investors of bitcoin and junk bonds tend to behave similarly.

The top graph on the left shows the yield premium for holding a BB-rated corporate junk bond versus a similar maturity risk-free Treasury bond is below 2%. That is the lowest spread since the eve of the financial crisis. Similarly, the spread between junk and investment-grade bonds is also at the tightest levels since the financial crisis. Yield spreads on junk bonds imply that investors believe there is minimal credit risk. Therefore, they likely believe a recession of any consequence is not in the cards. Given the high debt loads of junk-rated companies and the level of interest rates, such complacency seems misplaced.

Bitcoin has been on a tear recently. Since the start of the year, it’s up 42%. Some of the gain is attributable to new spot bitcoin ETFs. However, the recent surge is not new. Since the start of 2023, bitcoin has been up nearly 300%. Since it has no calculable fundamental value, bitcoin tends to attract speculators. Accordingly, it provides an excellent gauge of speculation and exuberance in the financial markets.

What To Watch Today

Earnings

Economy

- No notable reports are due today.

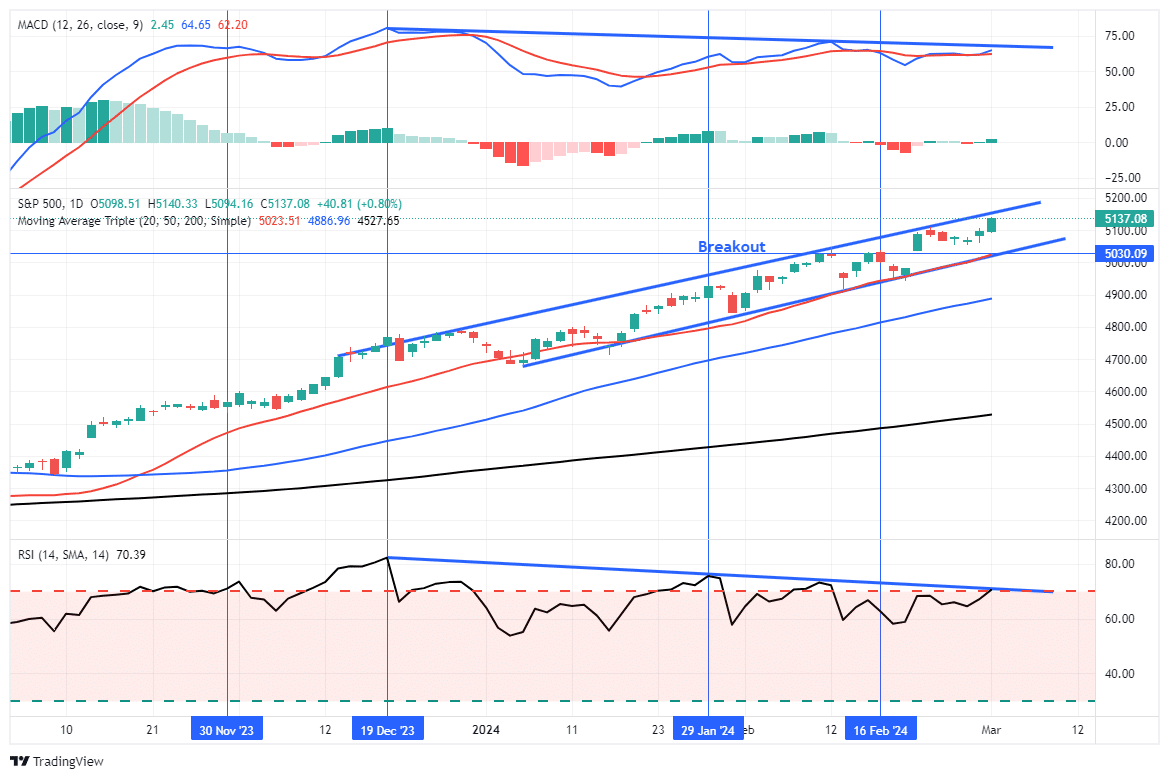

Market Trading Update

Last week, we discussed the ongoing bull rally following Nvidia’s blowout earnings report. To wit:

“The rally continued this past week, spurred higher by Nvidia’s blowout earnings report Wednesday night. After a brief test of the 20-DMA, the market surged to new all-time highs on Thursday, confirming the ongoing bullish trend. As shown, the 20-DMA continues to act as crucial support for the market.”

That remains the case this past week. While the overall market traded higher into the end of the week, setting new all-time highs, the bullish November trend remains intact. While the market remains confined to that narrow rising trend channel, the MACD “buy signal” remains elevated, and a clear deterioration in the market’s momentum remains.

With sentiment very stretched, as shown, the risk of a short-term correction to relieve price extensions remains the most probable outcome.

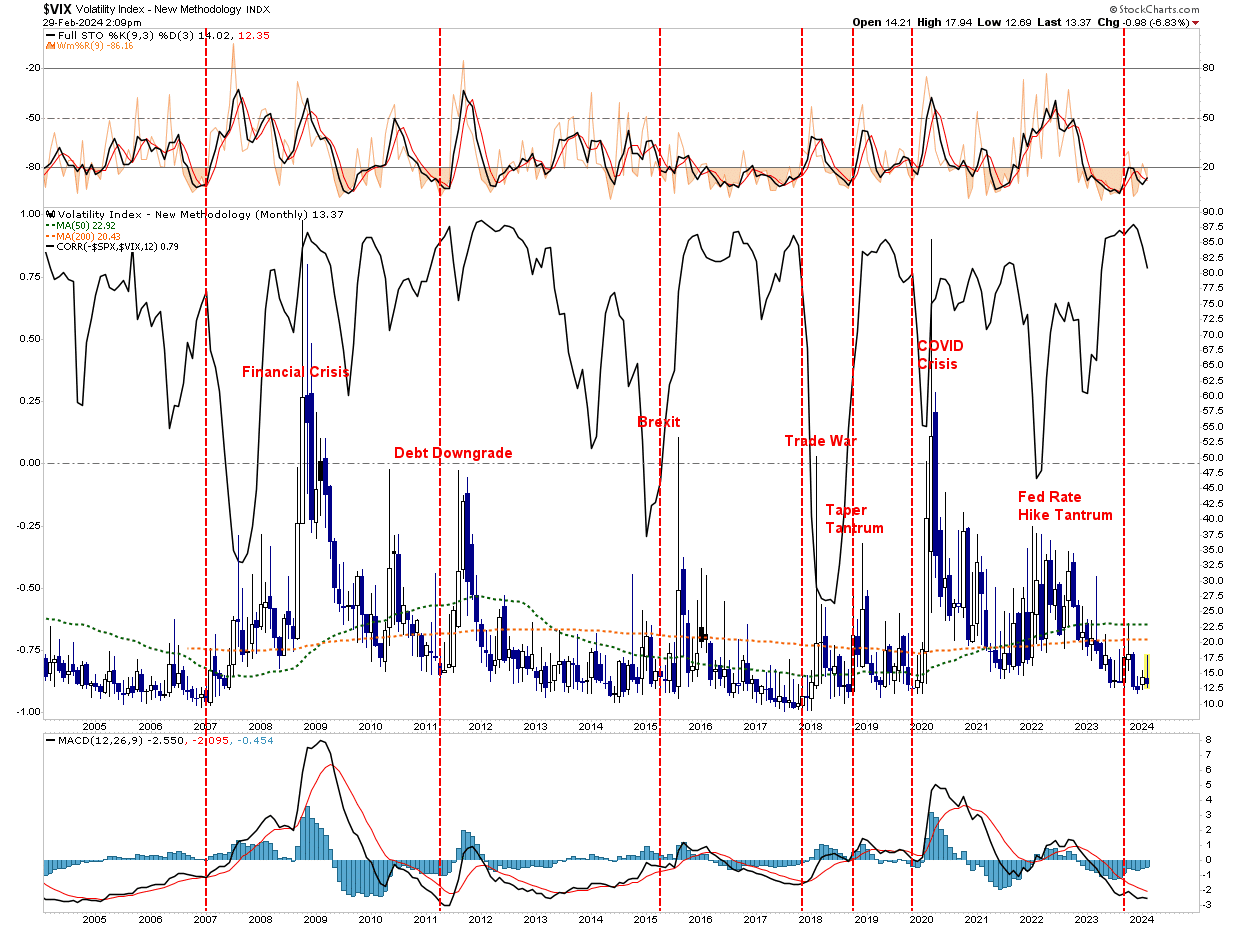

Furthermore, as noted in our Daily Market Commentary on Thursday:c

“The negative relationship between the VIX and stocks is the norm, but any deviations in the correlation and, therefore, irregular behaviors of some investors can provide market signals.”

The correlation is above +.75 on a monthly chart. The current level is on par with some of the bigger market corrections since the Financial Crisis. While this analysis provides a reason for caution, like any indicator, it is imperfect, and the market could move higher before a correction ensues. Therefore, we must know the risks and navigate the market accordingly.

While I realize this has been a consistent message over the past few weeks, it is tempting to throw caution to the wind and assume that this bull trend will last indefinitely. I assure you that will not be the case. While we maintain our long exposure, the level of discomfort in that positioning continues to grow.

The Week Ahead

Last week’s PCE prices gauge showed an uptick in services prices. Accordingly, Tuesday’s ISM Services survey will be closely followed. In particular, the price component, which remains high. Jobs data will also be followed closely, starting with JOLTs on Wednesday, and followed by ADP on Thursday, and the BLS jobs report on Friday. Current expectations are for an increase of 190k, well below last month’s sizzling 353k gain.

Jerome Powell will testify to Congress on Wednesday and Thursday. We will closely listen for thoughts on how the speculative market environment may affect his policy forecast. Further, might he take this opportunity to discuss plans to reduce QT?

The Bank of England May Exit QE

The Bank of England (BOE) appears to be taking a different approach to its balance sheet than the Fed. Based on recent comments, including the one below, courtesy of Bloomberg, the BOE could entirely rid its balance sheet of bonds.

BOE Deputy Governor Dave Ramsden, who oversees financial markets, said officials may continue running down the QE portfolio, which peaked at £895 billion, even after hitting the “preferred minimum range of reserves.”…“The Monetary Policy Committee could unwind the APF fully, if it judged necessary for policy reasons, and the level of the PMRR should not affect this judgment,” Ramsden said.

While the comments make it appear the BOE is exiting the bond-buying business, they are not. Per Ramsden:

“It’s important to normalize our balance sheet when we can to ensure we have sufficient headroom to respond to future shocks,”

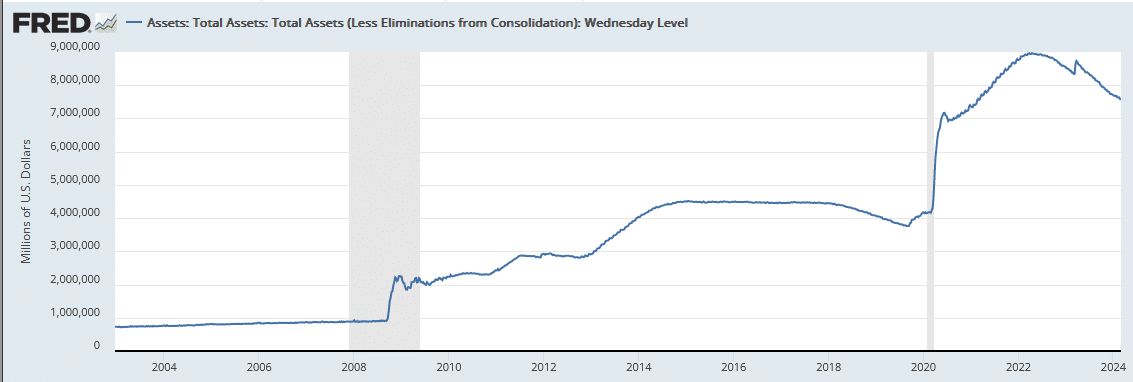

It appears the BOE is considering exiting for now but will employ QE when needed. Such a threat, as we see with rate caps by the Bank of Japan, may allow the BOE to manage interest rates without directly intervening in the markets. Words/threats instead of actions may do the job for them. We do not expect the Fed to follow as its $7.5 trillion holdings would overwhelm the stock and bond markets, ultimately forcing them to add significant reserves via QE.

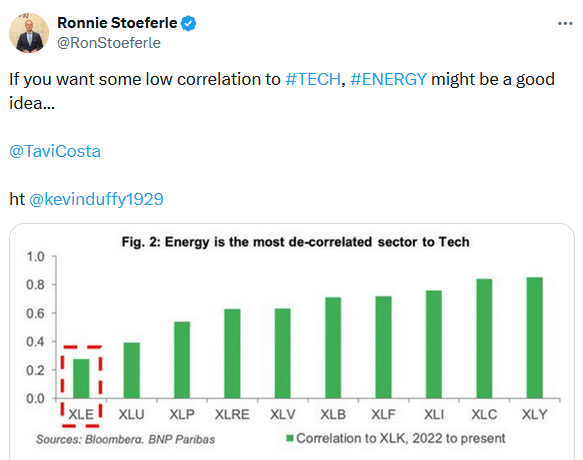

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.