The recent #MacroView blog noted economists are increasingly confident the economy will avoid a recession. Such is due to strong job and retail sales data. Even Jerome Powell, in his recent speech, made note of the strength of the data. To wit:

“Additional evidence of persistently above-trend growth, or that tightness in the labor market is no longer easing, could put further progress on inflation at risk and could warrant further tightening of monetary policy. In any case, inflation is still too high, and a few months of good data are only the beginning of what it will take to build confidence that inflation is moving down sustainably toward our goal.‘”

Despite substantially tighter monetary policy, the strength of jobs and retail sales stumped expectations of a recessionary downturn in 2022. However, such was not surprising. This was a topic we wrote on several times, including Michael Lebowitz’s “Stimulus And Consumption Are Fueling Economic Resilience:”

“The economy has marched forward, ignoring higher interest rates and consistent calls for a recession. Credit goes to ‘We The People,’ the citizens of the U.S. A shout-out also goes to Uncle Sam for showering us with trillions of dollars of stimulus during the pandemic to fuel consumption.

Understanding why the economy has done so well is easy. Massive stimulus drove consumption. The difficult task ahead is forecasting how much the remnants of stimulus, and other forms of financial relief, will continue to fortify personal consumption and boost economic activity.”

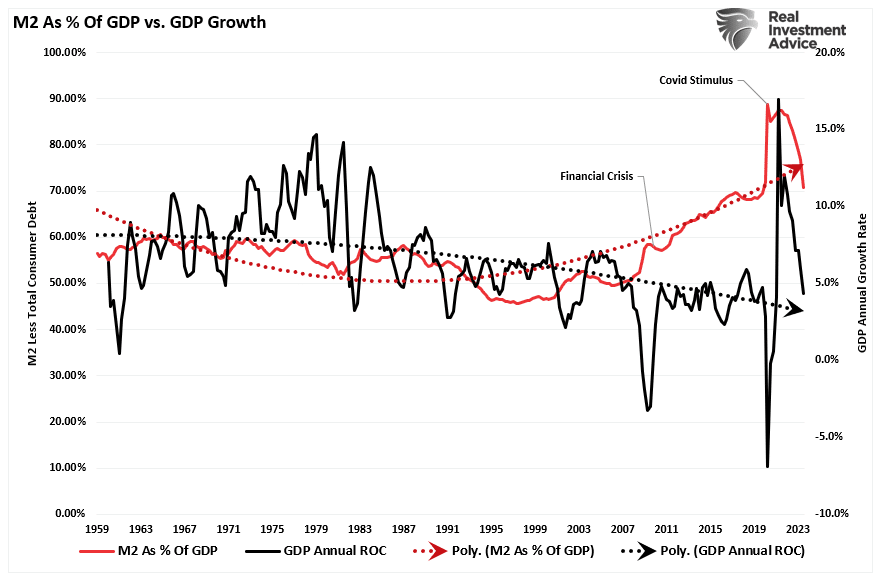

Given that personal consumption consistently accounts for over two-thirds of economic activity, it is not surprising that when you send money directly to households, the result would be both a surge in consumption and higher inflation. Three years after the pandemic-driven economic shutdown, monetary liquidity remains highly elevated as a percentage of GDP. That surge in stimulus-driven demand led to increased job growth, higher wages, and, as noted, higher inflation.

Much like a massive bonfire, that surge in monetary supply ignited economic activity takes time to “burn out.” As that excess liquidity expires, the rate of economic growth, and ultimately inflationary pressures, will reverse.

As such, what we currently see in the job and retail sales data is not suggesting a more robust economic growth rate in the future. As we will discuss, it is just a reflection of the fading economic activity driven by the last remnants of financial stimulus.

Driving In The Rear View Mirror

As noted in that blog, economic data runs with a reasonably significant lag. Such is because the data is subject to extensive negative revisions in the future.

“Each of the dates above shows the economy’s growth rate immediately before the onset of a recession. You will note in the table that in 7 of the last 10 recessions, real GDP growth was running at 2% or above. In other words, according to the media, there was NO indication of a recession. But the next month, one began.”

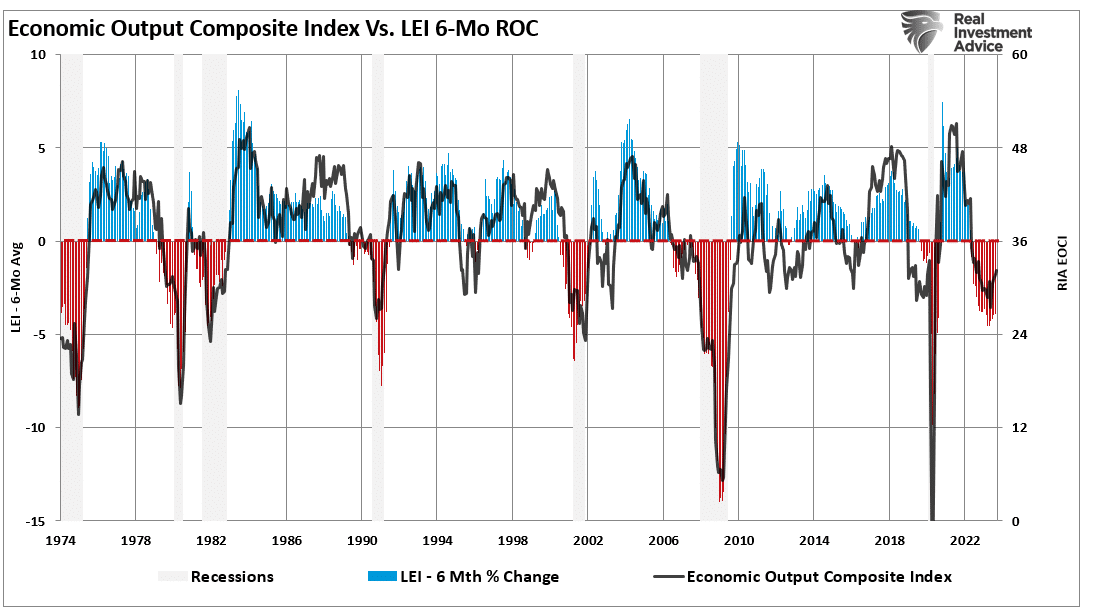

This is an even more critical issue when understanding how the Federal Reserve manages monetary policy in the “rear view” mirror. Current real-time economic data suggests the economy is rapidly moving from economic slowdown toward recession. The signals are becoming more evident from inverted yield curves to the 6-month rate of change of the Leading Economic Index.

However, while those signals generally precede economic recessions, jobs, and retail sales data lag. For example, if we look at the unemployment rate versus real GDP, we see that low unemployment, the sign of a strong jobs market, always precedes recessionary onsets.

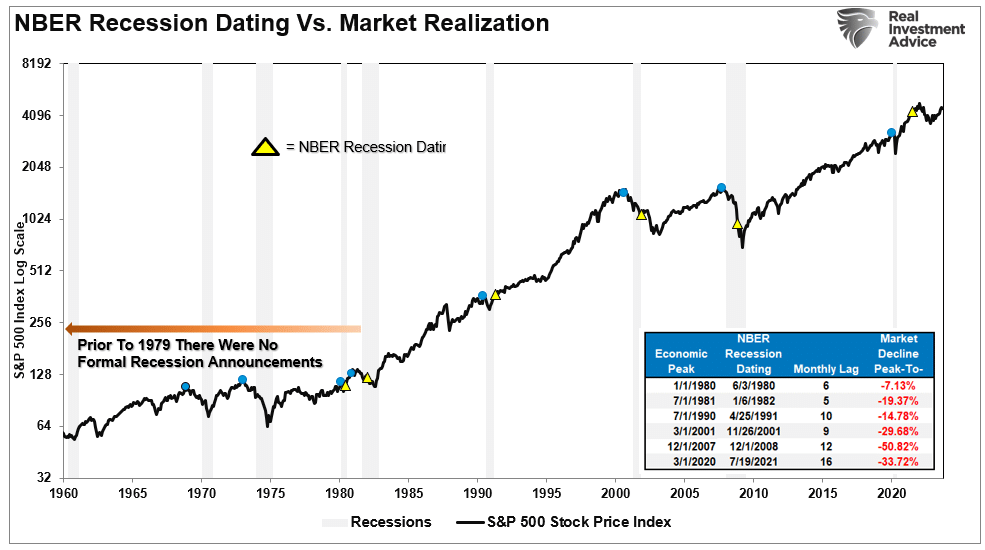

Recession Dating Happens With A Lag

Low unemployment precedes recessions because we are looking at “revised” data. As noted last Friday, it is often 6-12 months later when the National Bureau of Economic Research (NBER) dates the start of a recession. This is because the data must be revised before the official dating of the recession start is made.

“The chart below shows the S&P 500 with two dots. The blue dots are when the recession started. The yellow triangle is when the NBER dated the start of the recession. In 9 of 10 instances, the S&P 500 peaked and turned lower before the recognition of a recession.“

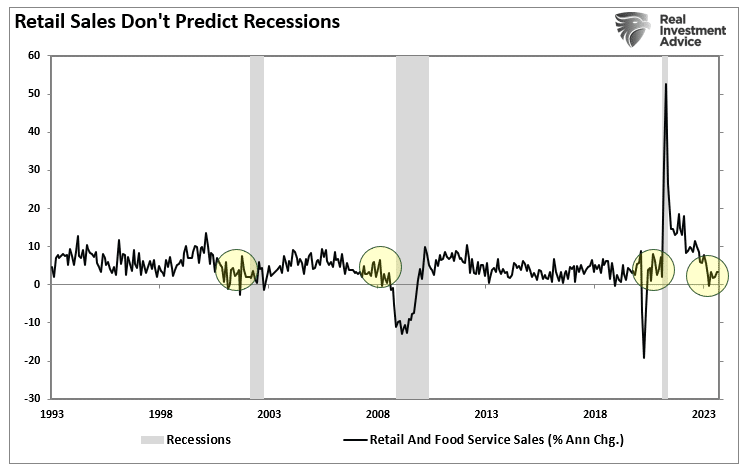

Do you see the problem of the “no recession” call by economists? The same issue comes to retail sales data. Economists believe that recent robust retail sales data negates the recession.

“Despite a low saving rate, slow demographics, depressed confidence, a crippled housing market, rising interest costs and growing credit problems, we estimate that American consumers increased their inflation-adjusted spending by more than 4% in the third quarter.” – David Kelly, chief global strategist at JPMorgan Asset Management

On a nominal basis, it is pretty clear that retail sales have ticked up recently. However, as shown, upticks in retail spending, like the jobs data, are often seen just before the onset of a recession. As such, the recent strength in trailing retail sales data gives us little to no indication of the recession risk ahead.

The same is true concerning inflation-adjusted retail sales data. Before the last three recessions, retail spending was strong just before the recession. Again, the current trailing real retail sales data does not indicate recession avoidance.

We should be paying attention to the gap between retail sales and jobs. The current gap is likely unsustainable because the income needed to consume comes from employment. Unsurprisingly, that gap will rectified with a recessionary downturn in the economy.

The challenge for the Federal Reserve and the mainstream economists is that “driving in the rearview mirror” has repeatedly had disappointing outcomes.

The Fed’s Big Risk

Here is the risk. Jerome Powell and other Fed members are directing changes to monetary policy based on strong economic data. To wit:

“Additional evidence of persistently above-trend growth, or that tightness in the labor market is no longer easing could put further progress on inflation at risk and could warrant further tightening of monetary policy.“

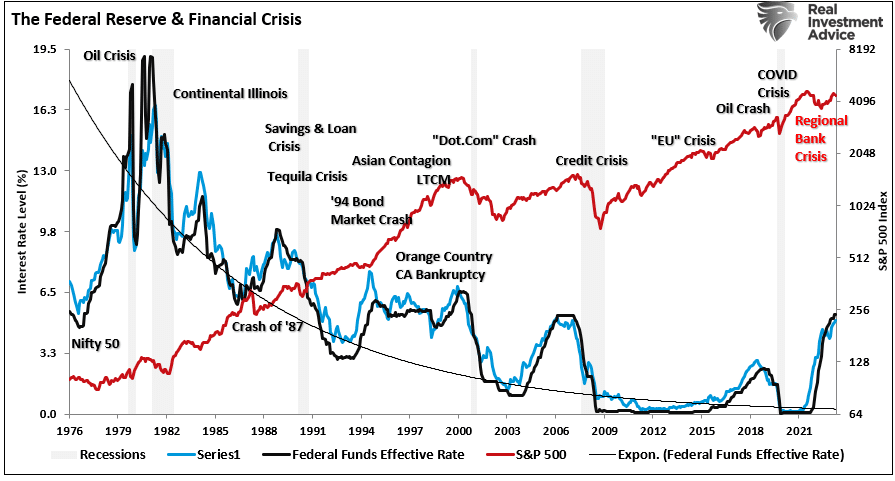

However, that robust data is subject to sharp negative revisions in the future. Such puts the Fed at risk of exacerbating an economic contraction by keeping monetary policy “too tight for too long.” Historically, when the Fed hikes rates, there is eventually a breaking point where unemployment rates shoot higher. Such is because the data is strong until it isn’t.

That breaking point occurs because the real-time economy adjusts to monetary policy changes. However, data such as employment and inflation can lag by several months.

Given this lag effect, the Fed will continue thinking it must maintain restrictive “monetary policy” to slow economic demand and bring inflation back to its target. However, the actual impact on consumers and economic activity is not reflected in CPI on a timely basis. Such creates the probability of the Fed over-tightening monetary policy and turning an economic slowdown into a more severe economic contraction.

Of course, this is what history tells us will happen.

Monetary supply also tells us the same. As discussed, inflation resulted from restricted supply due to the economic shutdown and increased demand from “stimulus” checks. The massive surge in M2 money supply has reversed.

Given the lag of changes in monetary supply, retail sales, and jobs data, the risk of the Fed “breaking something” remains high. While it may seem that the economic data suggests a “no recession” scenario, the problem of looking backward leaves everyone vulnerable to a head-on collision with what lies ahead of us.

Such is the risk we are facing now.

How does a recession happen?

“Slowly and then all at once.”