The stock market is having its worst week since March 2020 when the Pandemic first rocked the economy. This time the aggressive monetary policy is worrying investors. While there are many debates about whether this is a bear market, we must acknowledge it is a bearish trend. As investors, we must then ask if the recent stock washout is creating a tradable bottom, or is there more pain to follow?

A tradable bottom allows investors to partake in some upside and recoup some losses. We suspect a tradable bottom is near. Accordingly, we removed our S&P 500 hedge on Friday. If the tradable bottom shows more promise, it may be wise to add to our stock exposure. The bigger question is whether said bottom is THE bottom of the bearish trend, or is the rally an opportunity to rebalance, take more protective measures, and brace for even lower prices?

Our Daily Commentary and SimpleVisor Buy Sell Reviews allow us to share our thoughts on important questions like those we pose above.

What To Watch Today

Economy

- Chicago Fed National Activity Index, May (0.47 prior month)

- Existing Home Sales, May (5.40 million expected, 5.61 prior month)

- Existing Home Sales, month-over-month, May (-3.7% expected, -2.4% prior month)

Earnings

Pre-market

- Lennar (LEN)

Post-market

- La-Z-Boy (LZB)

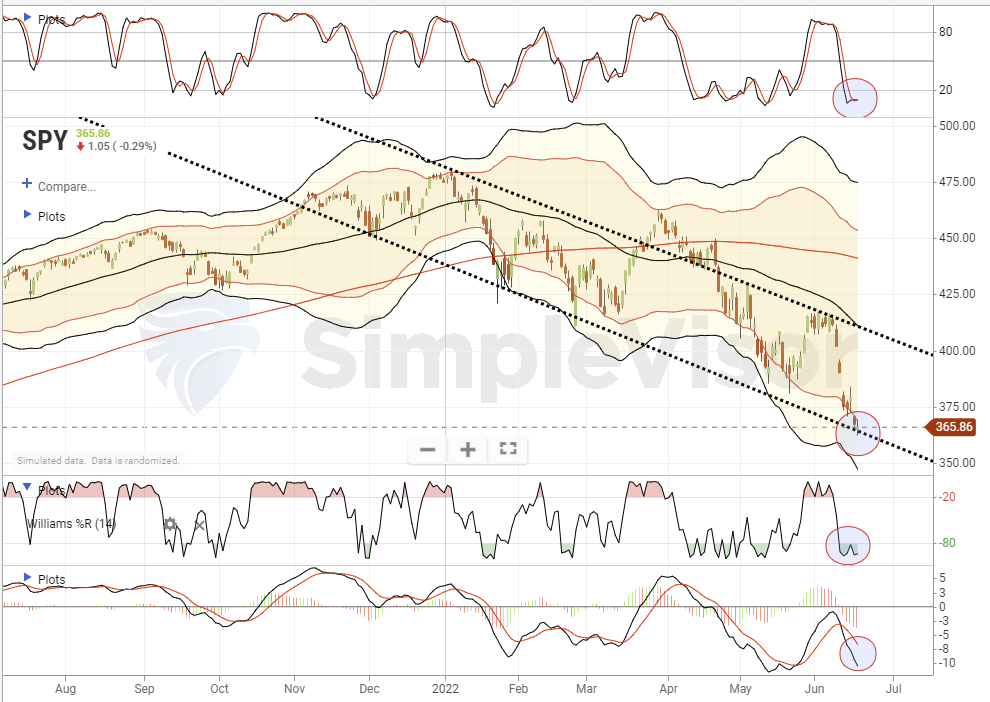

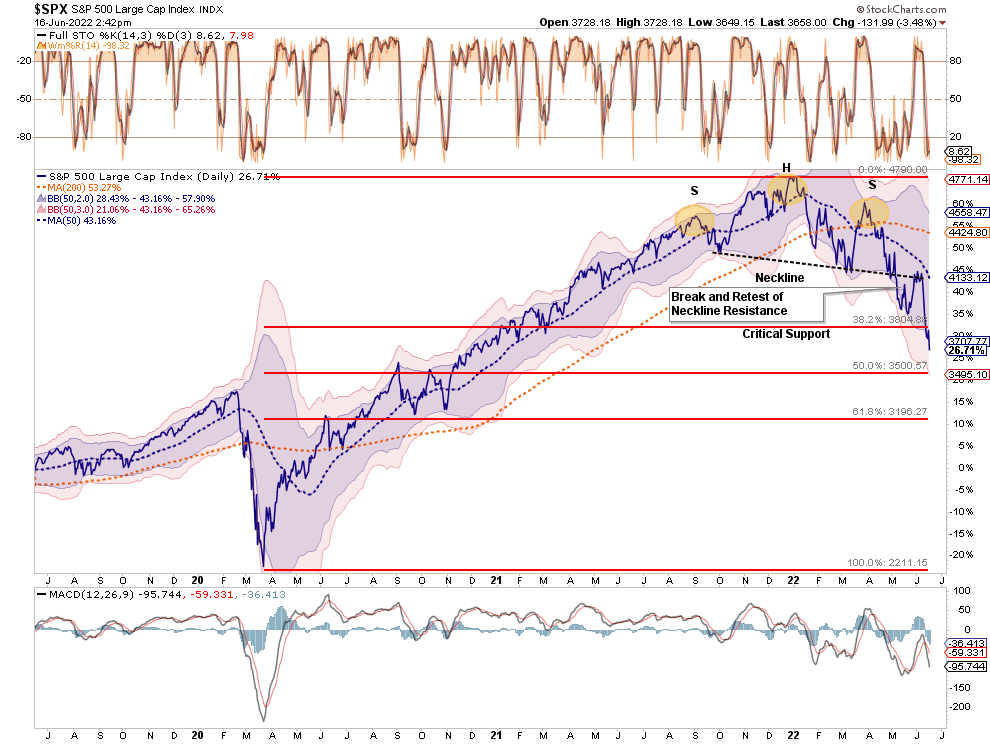

Is A Tradable Bottom Near

At previous market bottoms, the Fed was cutting rates to zero, introducing QE programs, or providing other measures of monetary liquidity. Today that is not the case, as the Fed is just starting to reduce its balance sheet and hike interest rates aggressively. The reversal of liquidity suggests that any short-term bottom in stocks may be tradable bottoms, but not “the” bottom, particularly as the economy approaches earnings and economic recessions.

With the market completing a “head and shoulders” topping process and violating important support at the 38.2% Fibonacci retracement level, the next logical support is 3500. Such a correction would wipe out all the gains since the 2020 peak. Such would also push the S&P 500 index nearly 4-standard deviations below the 50-day moving average.

If the market fails to find support at 3500, 3196 becomes the next logical level.

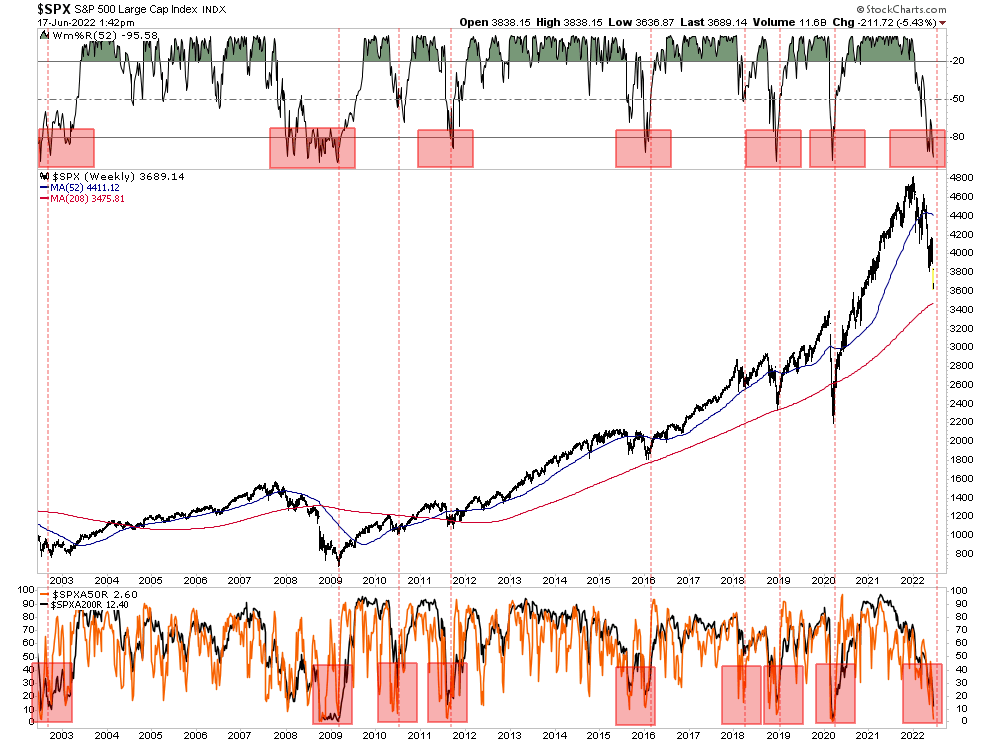

However, the market is currently showing several signals aligned with previous market bottoms. Currently, only 2.6% of stocks in the S&P 500 index are trading above their 50-day moving average. Moreover, only 12.4% are above their respective 200-dma. As shown, with the market oversold and so many stocks trading below their respective moving averages, such typically denotes market lows.

Furthermore, the market selling as of late has been brutal. As noted by BofA:

“More than 90% of stocks in the S&P 500 declined today. It’s the 5th time in the past 7 days. Since 1928, there have been exactly 0 precedents. This is the most overwhelming display of selling in history.”

While none of this data “guarantees” a market bottom is near, history suggests the odds of a reflexive rally remain elevated. We also suspect Wall Street will call the “Fed bluff” on aggressive monetary policy sooner than later.

The Week Ahead

On Wednesday and Thursday, Chairman Powell will likely spark investor interest when he testifies on monetary policy, the economy, and inflation to Congress. We suspect he will tote the party line and fully commit to fighting inflation. It will be interesting to see how he handles concerns that fighting inflation entails job losses.

The economic calendar is light. Of note will be existing home sales for May. Houses that were sold in May were likely negotiated for in February or March when mortgage rates were much lower. Accordingly, the data may not represent what is truly going on in the housing sector. Similarly, new home sales, due out on Friday, are fraught with a similar data lag. The Chicago Fed National Activity Index will provide its latest update on the state of the national economy. It is expected to fall but remain in economic expansion territory.

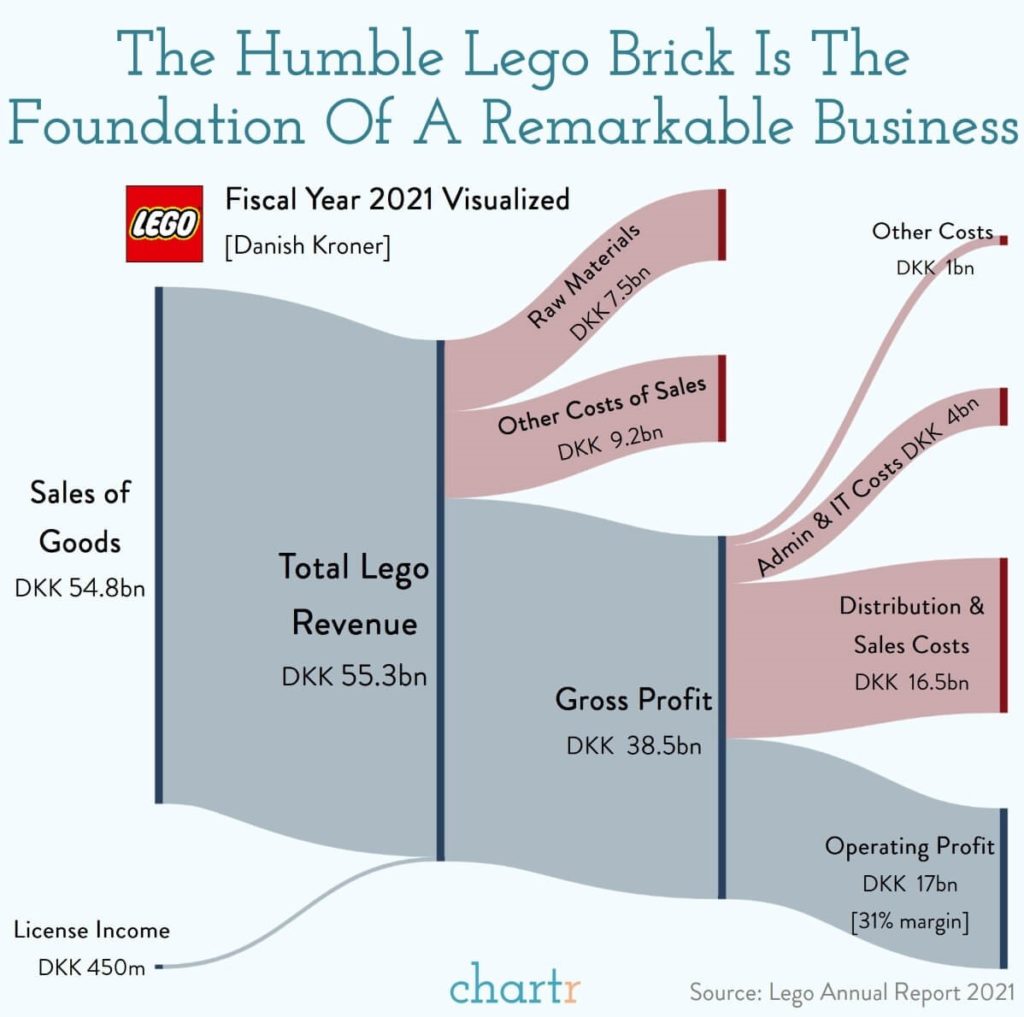

The Building “Bricks” Of A Remarkable Business

“This week iconic toymaker Lego announced its plan to build a new 1.7 million-square-foot factory in Virginia, creating up to 1,800 jobs once complete. The Danish company plans to spend $1bn on the factory, which is an enormous investment for any company, let alone one that produces such a simple product.

But selling a simple product, and doing it really, really well, has been the cornerstone of Lego’s remarkable business model. Sales last year jumped 27%, a number that some cash-burning tech companies would have been happy with. All told Lego sold ~55bn Danish Kroner worth of plastic bricks in 2021, squeezing out a 31% margin on those sales thanks to the company’s iconic brand and build quality, with a reported manufacturing error rate of just 18-in-a-million.

In USD Lego sales work out to around $7.8bn — suggesting that its factory investment, which will presumably be spread over 3 years, will only cost around ~4% of Lego’s sales over that period. Lego is betting big that playing with plastic bricks is here to stay. They’re probably right.” – Chartr

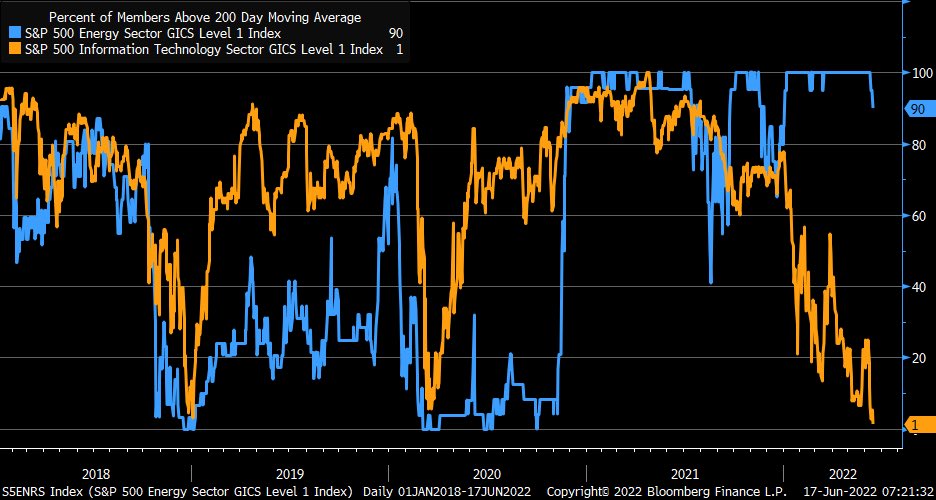

Energy vs. Tech- A Tale of Two Sectors

The Bloomberg graph below shows the stunning divergence between the tech and energy sectors. Currently, 90% of stocks in the energy sectors are trading above their 200 dmas. At the same time, only 1% of tech stocks exceed their 200 dmas. One only has to look back to 2020 to see a similar divergence. Through most of 2020, it was the energy sector with a small percentage of constituents trading above their 200 dmas. And, most tech stocks were increasingly surpassing their 200 dmas.

Just because the divergence is extreme doesn’t mean it can’t continue for a while. However, in the coming months, it is likely to revert. Will energy stocks finally break and trade below their 200 dma? Such argues for an extended bear market. Or, will tech stocks retake their 200 dma, in what may signal a bullish trend for the markets?

Central Banks Are All Over the Monetary Map

Last week many of the world’s major central banks held monetary policy meetings and took action. As shown below, the policy prescriptions for weaker economic activity and inflation spanned a vast chasm. The Fed was the most aggressive, with a 75 bps rate hike and a commitment to fight inflation aggressively. On the other side of the spectrum is the Bank of Japan. On Friday, they announced that they would continue to do as much QE as is needed to cap its 10-year yield at 0.25%. They clearly remain willing to prop up their economy and ignore rising inflationary pressures and the weakening yen. The graph below shows how the BOJ’s actions put a kink in its yield curve. The yield should be closer to 0.40% if they leave it alone.

- Fed: Hikes rates 75bps

- Switzerland (SNB): Hikes rates by 50bps

- England (BoE): Hikes by 25bps

- Europe (ECB): Working on a plan to hike rates this summer and will stop QE

- Japan (BoJ): Monetary guns blazing. Will defend cap on ten-year yields and “short & long term policy rates to remain at present OR LOWER levels.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read