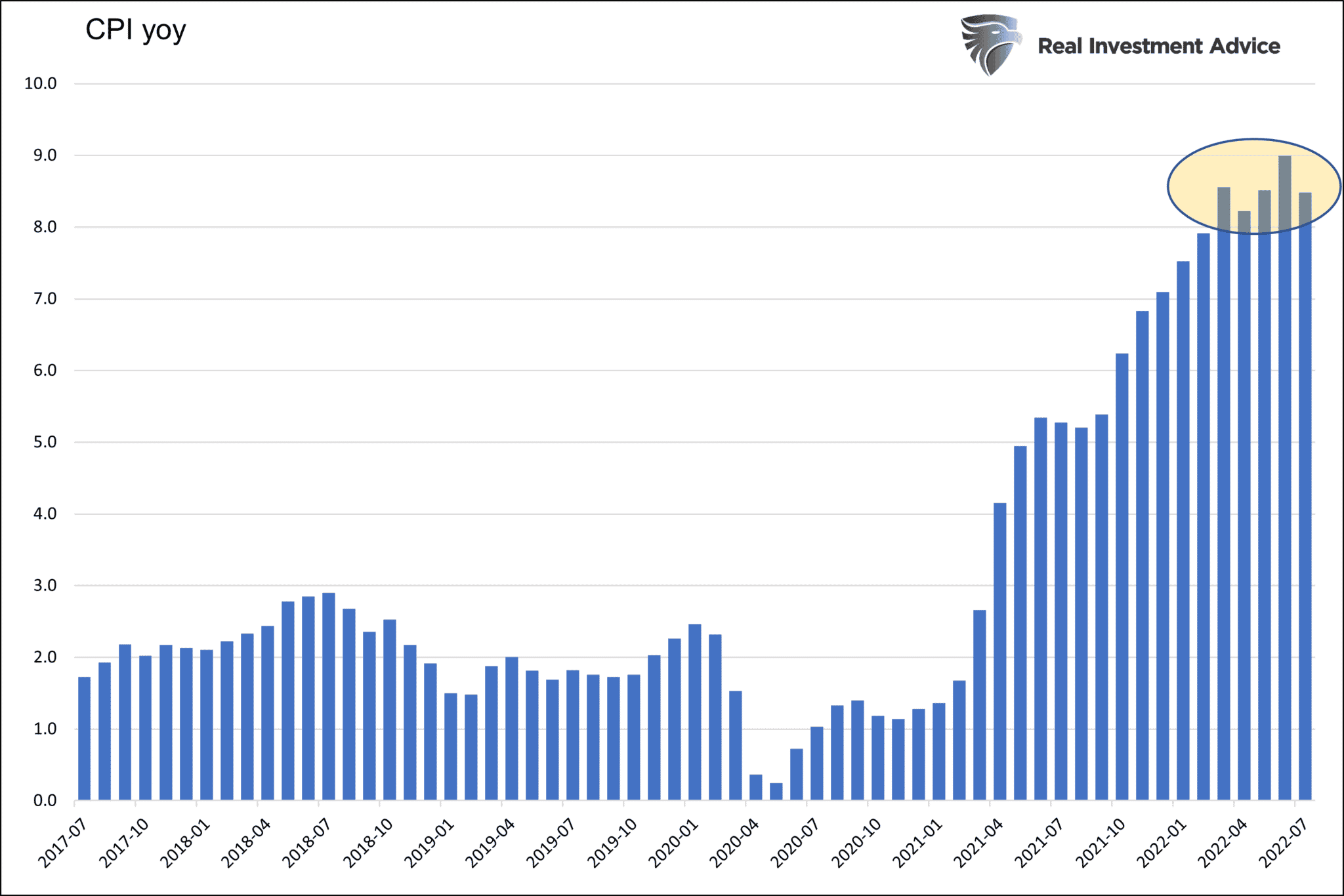

Finally, the BLS CPI report provided a bit of relief on the inflation front. Relief was immediately felt in the futures markets, where the S&P 500 futures gapped higher by over 80 points in minutes following the release of the inflation data. For the month of July CPI was 0.0%, which reduced the year-over-year rate to 8.5% from 9.1%. Further providing relief, core inflation (ex-food and energy) only rose .3% for the month versus expectations of a 0.5% increase. The year-over-year core rate remains at 5.9%. Finding relief and calling for inflation to continue falling may be a bit too soon. As we show, the year-over-year inflation rate has been stable in the 8-9% range for the last five months. Inflation may have peaked but has it started to normalize?

There is some irony in the inflation report. The relief in the markets due to CPI peaking is sending asset prices higher. The Fed is more likely to hike interest rates when asset prices are rising.

What To Watch Today

Economy

- 8:30 a.m. ET: Initial jobless claims, week ended August 6 (263,000 expected, 260,000 prior)

- 8:30 a.m. ET: Continuing claims, week ended July 30 (1.407 million expected, 1.416 prior)

- 8:30 a.m. ET: PPI final demand, month-over-month, July (0.3% expected, 1.1% prior)

- 8:30 a.m. ET: PPI excluding food and energy, MoM, July (0.4% expected, 0.4% prior)

- 8:30 a.m. ET: PPI excluding food, energy, and trade, MoM, July (0.4% expected, 0.3% prior)

- 8:30 a.m. ET: PPI final demand, year-over-year, July (10.4% expected, 11.3% prior)

- 8:30 a.m. ET: PPI excluding food and energy, year-over-year, July (7.6% expected, 8.2% prior)

- 8:30 a.m. ET: PPI excluding food, energy, and trade, year-over-year, July (5.9% expected, 6.4% prior)

Earnings

Market Surges On Lower Inflation Read

As we discussed yesterday morning in our daily 3-Minutes Video, the market was set up to surge or crash depending on whether inflation came in above or below estimates. Inflation that was too hot would send yields screeching higher and stocks lower as the Fed would need to be more aggressive. Fortunately, the inflation relief in yesterday’s print gave bulls hope the Fed might be able to back off its aggressive monetary stance. However, as Anna Wong from Bloomberg noted:

“Both headline and core CPI inflation were surprisingly soft in July, but with recent wage and productivity data signaling prices pressures ahead, the Federal Reserve is unlikely to step back from the inflation fight just yet. Another soft print is likely in August as gasoline prices have continued to decline.”

But, on a bullish take, the always perma-bullish Jim Paulsen from the Leuthold Group stated:

“Wow, finally, the anecdotal evidence that inflation was easing has finally showed up in a mainstream inflation report. The Fed is rapidly losing its case for further tightening, and this report reinforces for investors that either a new easing cycle has already begun or we are getting very close to one.”

I suspect Jim is a little overly optimistic as even if the Fed does pause rate hikes currently, we are likely a VERY long way from the Fed returning to a monetary easing cycle.

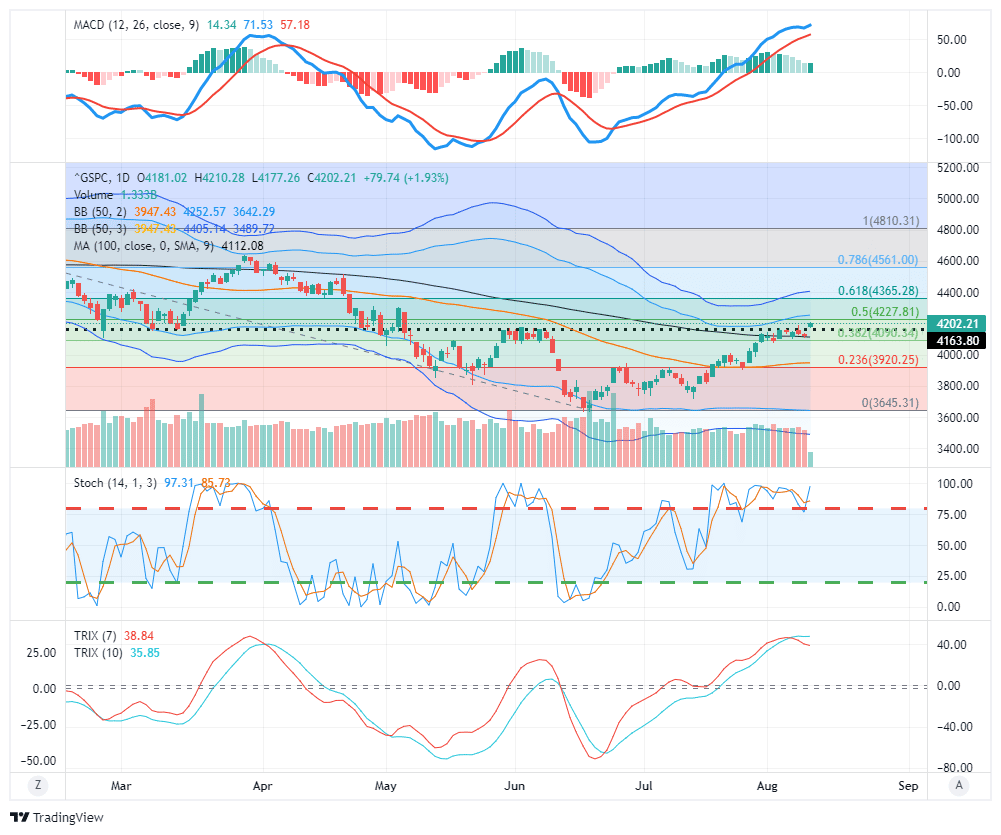

Nonetheless, markets rallied nicely yesterday, breaking above the recent consolidation. The 100-dma (black line) is now important support for any short-term corrective action and would allow for additional equity exposure to be added. The markets have also retracted 50% of the decline from the peak in January, which is now a “make or break point” for the rally. A break above the 50% retracement would suggest markets will move to eventually retest previous highs.

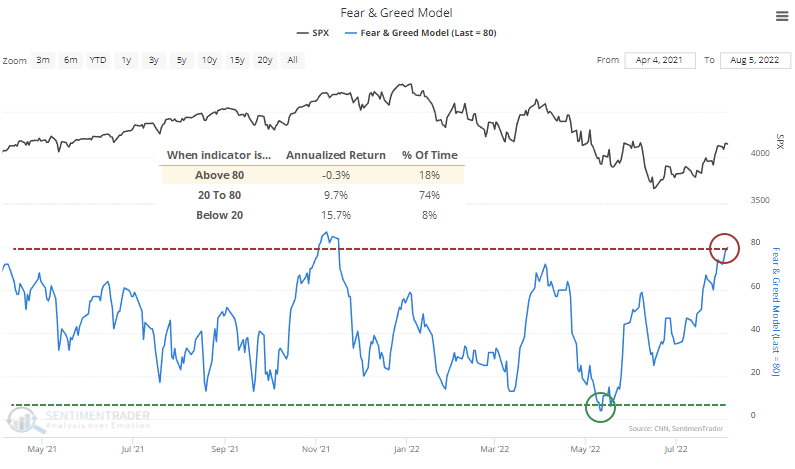

From Maximum Fear To Extreme Greed

“The Fear & Greed Model, based on the inputs published by CNN, has entered excessive optimism territory. Over the past 24 years, the S&P 500 has returned an annualized -0.3% when the model is above 80%.

Signs of pessimism abounded in June, and some residual indicators like fund flows still show investors’ repulsion toward stocks. Higher-frequency indicators have rebounded recently, pushing our sentiment models to the upper end of neutral or even into excessive optimism territory.

This is the point of sink-or-swim. Fly-or-die. Fish-or-cut-bait. All the idioms, including more colorful ones my grandpa would have used. During bear markets, this is the point where brave buyers take their gains, and shorts feel emboldened. During bull markets, this is when the latter gets steamrolled. Which one comes out on top over the next 3-4 weeks will tell us a whole lot about prospects through year-end and beyond.” – Sentiment Trader

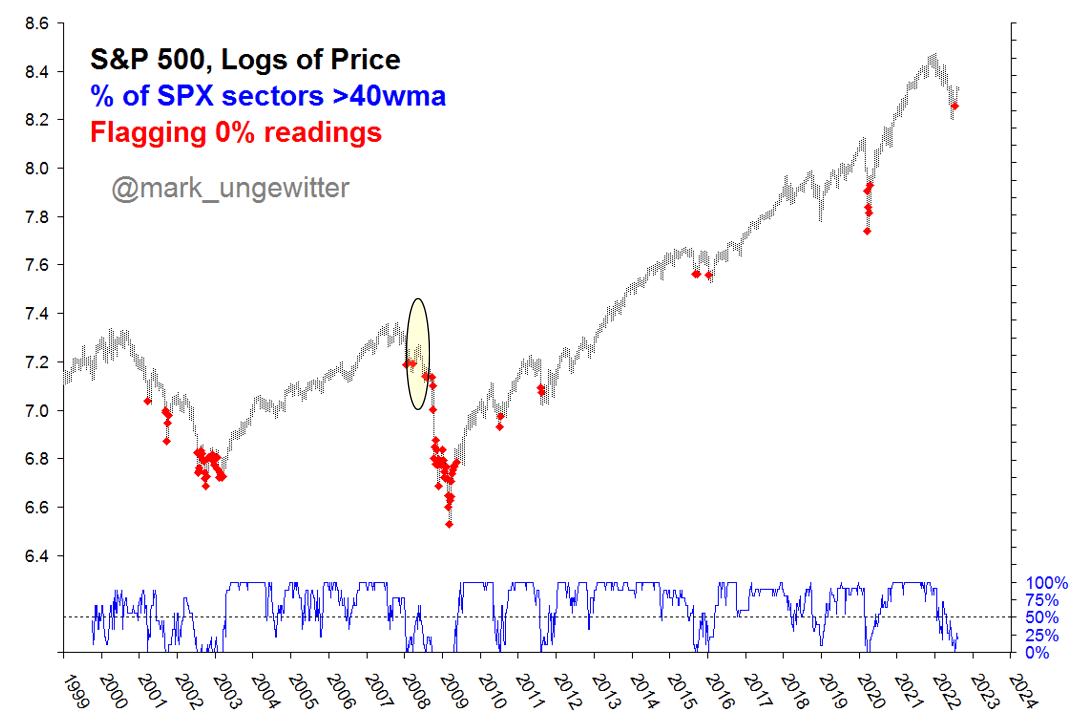

2008 Redux or New Highs Ahead?

The graph below shows the S&P 500 on a log scale and highlights (red) instances when every S&P 500 sector was simultaneously below their respective 40-week moving averages (WMA). A few weeks ago, all of the sectors were below their 40 WMA, which potentially signals the decline is ending. Such was the case in 2015-2016, however, as we see, the indicator often triggers multiple times during larger bear markets before a true bottom forms.

As we have written, the recent decline and rally look eerily similar to the S&P decline leading to the Bear Stearns failure and the rally that ensued. The 40wma triggered twice at the initial lows of the 2008 bear market, but they proved to be false signals. If the economy enters a recession as it did in 2001 and 2008, we fear this may not be the last red dot for this bear market. Is the graph a reason for optimism or concern?

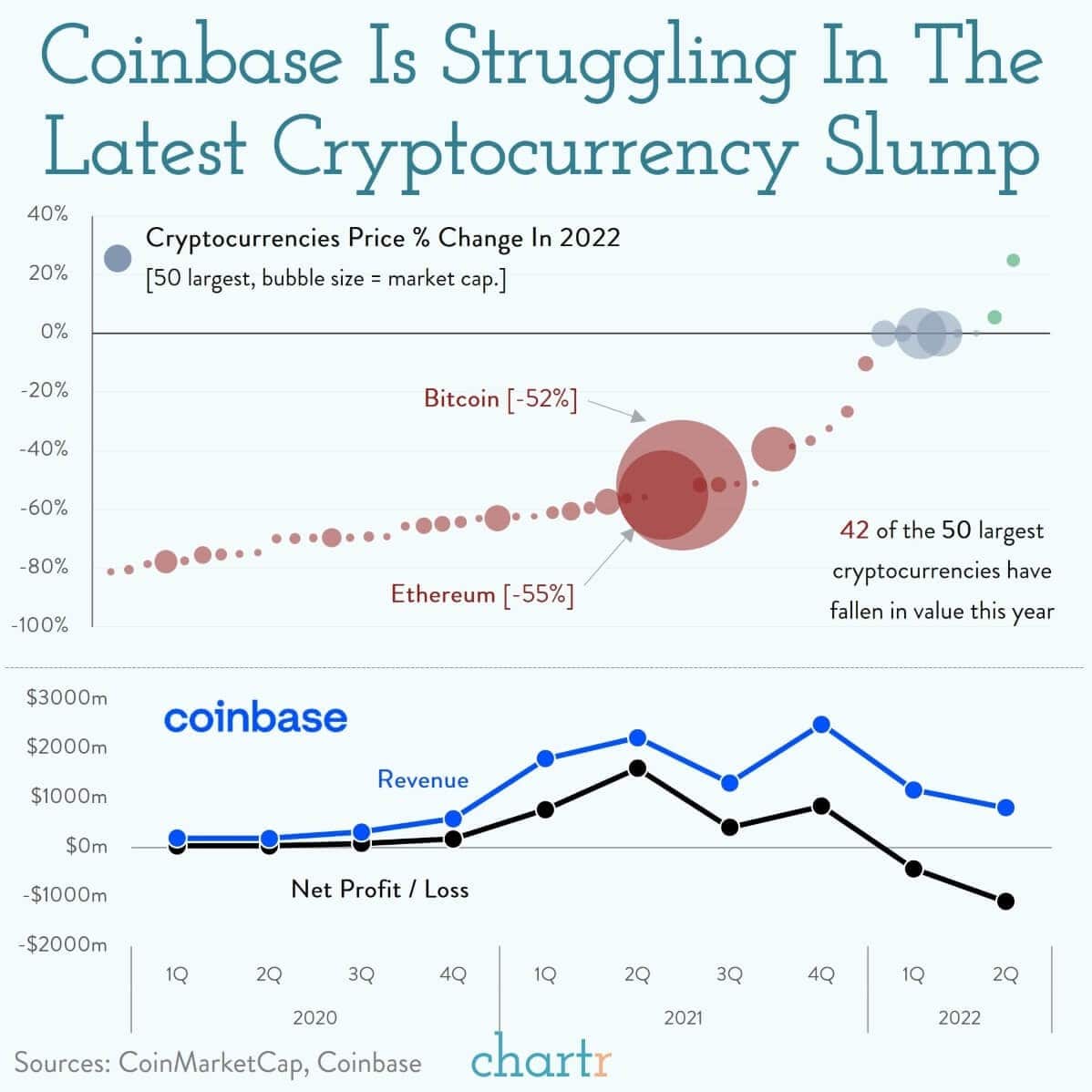

Is Coinbase Finally Basing?

“Coinbase’s role as a crypto exchange operator has been made much harder in the last 6 months as cryptocurrencies have slumped. Indeed, 42 of the 50 largest cryptocurrencies have fallen in value this year. The two largest — Bitcoin and Ethereum — have lost more than half their value in the year-to-date.

Falling crypto markets have meant smaller transaction revenues for Coinbase, but it hasn’t just been about prices falling. The company’s active userbase — those making at least one trade per month — also fell, from 11.2m at the end of last year to 9m today. Taken together, this meant total trading volumes on the platform (in USD) fell by more than half.

As the largest US-based crypto exchange and one of the 3 largest globally, Coinbase’s results are generally a bellwether for the crypto sector — but it hasn’t been all bad news. Coinbase’s total userbase did pass nine figures, with 103 million total registered users now on the platform, and a new partnership with asset management giant BlackRock that could help the company reach an entirely new set of customers.” – Chartr

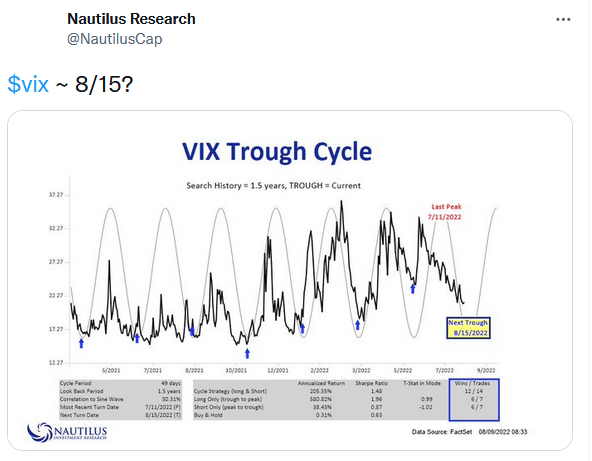

VIX Troughing Again

We shared this graph in late March and early June. In both instances, the reliable VIX cycle troughed. We update it as a warning that VIX is set to trough again on August 15th. While VIX is lower today than the prior trough, it sits on a solid rising support line that goes back to late 2021. A break of support would lead to a lower VIX and likely higher stock prices. Conversely, a bounce in the coming days, especially if it jumps to the prior highs (the mid-30s), could likely push the market back toward prior lows.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

Also Read