“HODL,” an original misspelling taken on as a badge of courage by cryptocurrency investors, spread to “Meme stocks” during the runup in 2020 and 2021.

The term “HODL” originated from user GameKyubbi, who posted a drunk, semi-coherent, typo-laden rant about his poor trading skills.

“‘I AM HODLING.’ I type d that tyitle twice because I knew it was wrong the first time. Still wrong. WHY AM I HOLDING? I’LL TELL YOU WHY. It’s because I’m a bad trader and I KNOW I’M A BAD TRADER. Yeah, you good traders can spot the highs and the lows pit pat piffy wing wong wang just like that and make a millino bucks sure no problem bro.

You only sell in a bear market if you are a good day trader or an illusioned noob. The people inbetween hold. In a zero-sum game such as this, traders can only take your money if you sell.” – BitcoinTalk fourm

Within an hour of that post, “HODL” had become a meme. Initially, the memes referenced the movies “300″ and “Braveheart,” but there are now countless HODL memes floating around the internet.

Of course, there seemed to be no risk to a “HODL” strategy at the time, as the Federal Reserve and Government pushed trillions of dollars in liquidity into the financial markets and economy. With the economy shut down due to the pandemic, sports gamblers turned their attention to the stock market to get their “fix.” As asset prices surged and with the assistance of the Robinhood app, investing became so easy you could draw letters out of a Scrabble bag.

Unfortunately, when it comes to buying and “HODLing,” the outcome from periods of excess speculation is always the same.

The “HODL” Fallacy

I recently wrote about the problems with “armchair” investment strategies. To wit:

“As shown in the chart below, the advice given is not entirely wrong. Since 1900, the markets have averaged roughly 10% annually (including dividends). However, that figure falls to 8.08% when adjusting for inflation.

By looking at the chart, it’s pretty evident that you should invest heavily in the market and “fughetta’ bout’ it.”

If it was only that simple.”

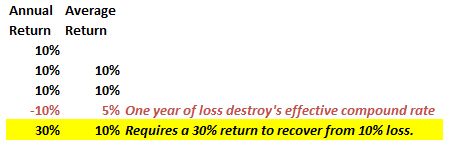

While the average rate of return may have been 10% over the long term, the markets do not deliver 10% yearly. Let’s assume an investor wants to compound their returns by 10% a year over five years. We can do some basic math.

After three years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%. Furthermore, it then requires a 30% return to regain the average rate of return required.

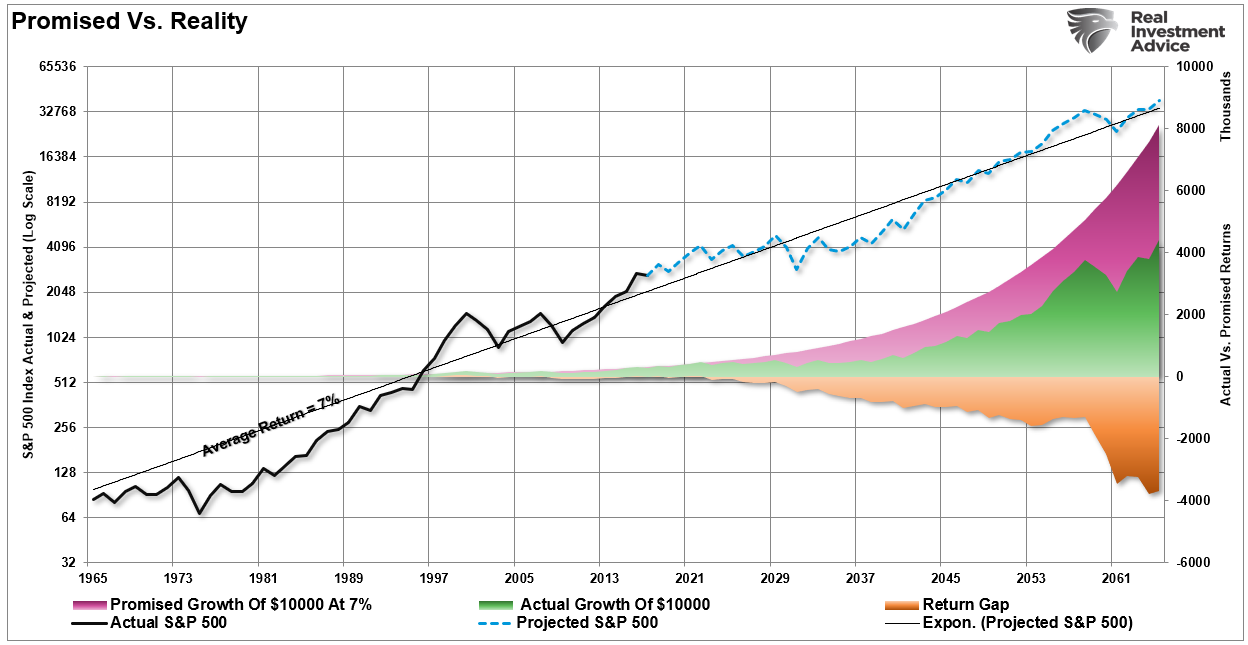

While an investor can “HODL” for the long term, there is a significant difference between the AVERAGE and ACTUAL returns received. As I showed previously, the impact of losses destroys the annualized “compounding” effect of money. (The purple shaded area shows the “average” return of 7% annually. However, the differential between the promised and “actual return” is the return gap.)

The differential between what investors were promised and actual returns is substantial over the long term. Furthermore, you DIED long before realizing the long-term average return rate.

Amid a “bull market,” the impact of losses during the second half of the market cycle becomes obscured. The stronger the bull market advance, the more mistakes investors make by assuming the current cycle will not end as they take on more speculative risk.

Unfortunately, all cycles end.

HODL – Another Word For Speculation

One of the more disappointing developments in the financial markets over the last 12 years has been the rise of “performance chasing” by investors. But such is not surprising given the repeated interventions by the Federal Reserve. As Larry McDonald of the Bear Traps Report noted:

“Inflation is forcing central bankers to allow price discovery. There was always price discovery before Lehman, but for much of the last 12 years markets have been in a Fed zombie trance.“

Such isn’t “investing,” it’s “speculation.” But who could blame young, inexperienced individuals with a “stimmy” check and promises of quick riches in Bitcoin as it surged daily?

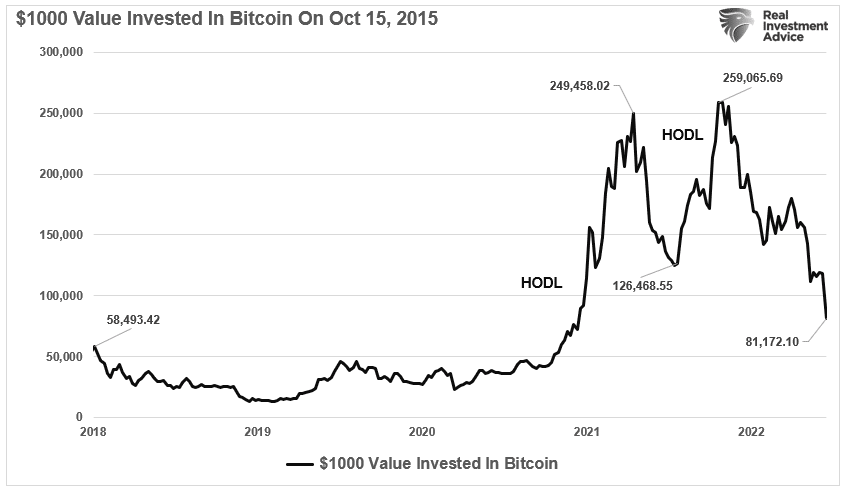

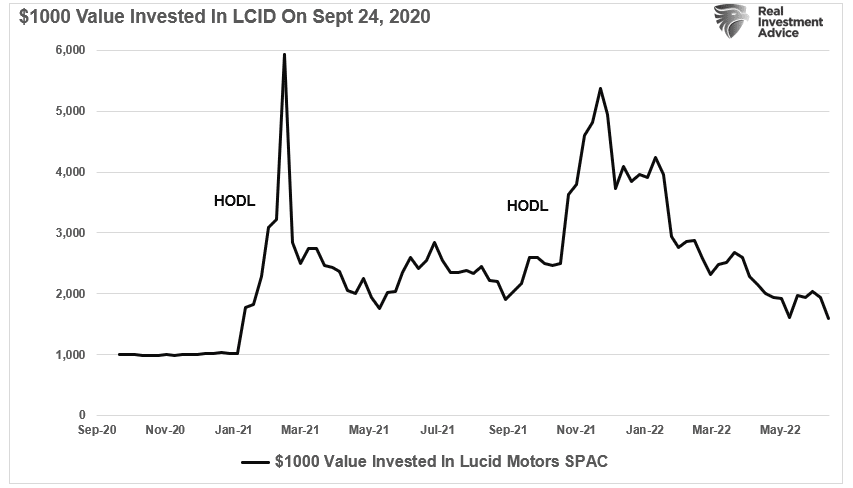

But it wasn’t just cryptocurrencies. Wall Street supplied traders with SPACs like Lucid Motors when IPOs could not get pushed out fast enough.

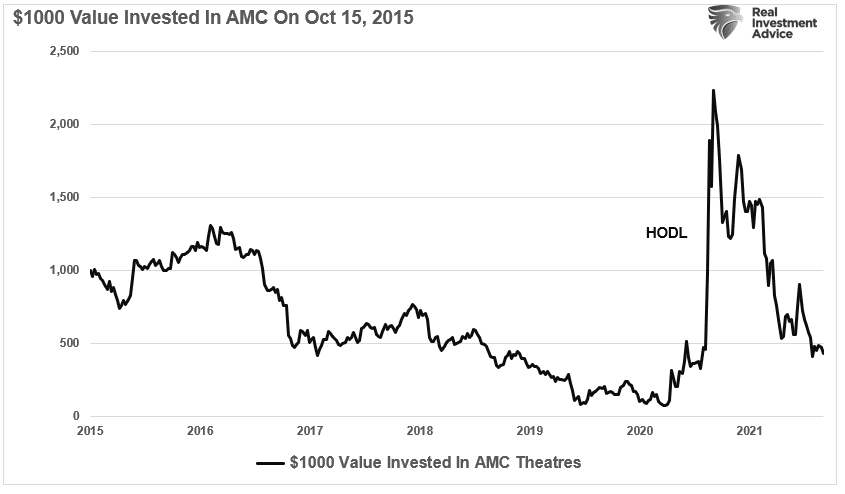

And “Meme” stocks like AMC Movie Theatres got touted on websites like WallStreetBets.

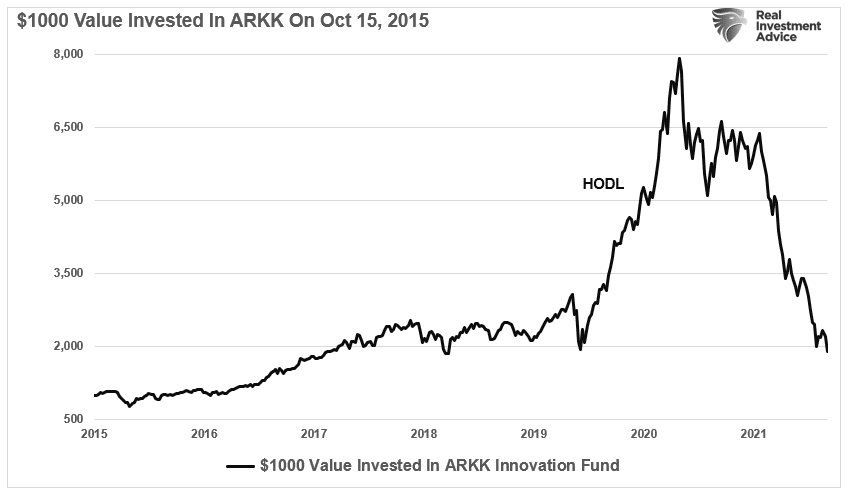

Of course, the “MoMo” craze got represented best by Cathie Wood and the Arkk ETFs.

While “HODLing” worked during the rising bull market, individuals have now discovered holding during a “bear market” can be devastating.

Ultimately, investing is about managing the risks that will substantially reduce your ability to “stay in the game long enough” to “win.”

“The distinction between investment and speculation is a useful one and its disappearance is a cause for concern. We’ve often said Wall Street should reinstate this distinction and emphasize it in its dealings with the public. Otherwise, stock exchanges may some day be blamed for heavy speculative losses which those who suffered them had not been properly warned against.” – Benjamin Graham – The Intelligent Investor:

The current bear market is no exception and is the logical outcome of what follows the last advance.

Time To Let Go Of “HODL”

There is a huge market for “get rich quick” investment schemes and programs as individuals keep hoping to find the secret trick to amassing riches from the market. There isn’t one.

In the 1990s, investors plowed money into speculative investments. Ultimately, they lost most of it at the turn of the century. Then, they turned their focus to real estate, only to get wiped out in 2008. The runup and crash in the cryptocurrencies, disrupter technologies, SPACs, and “Meme” stocks have all met a similar end.

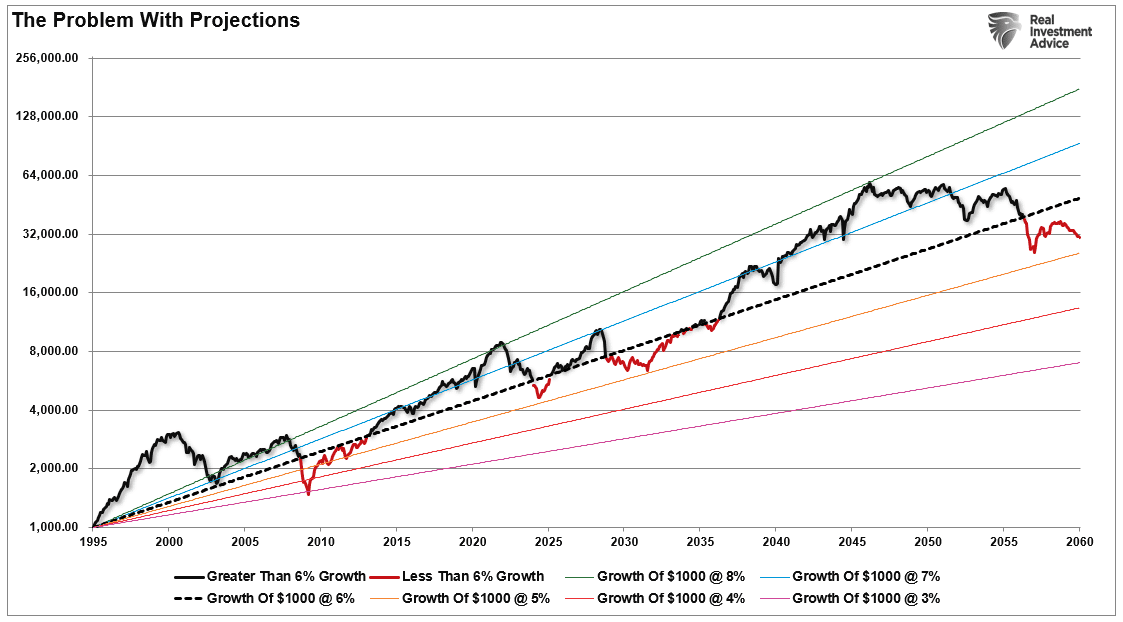

Many believe that investing in the financial markets is their only option for retiring. Unfortunately, they fell into the same trap as most pension funds hoping market performance will make up for a “savings” shortfall. The chart below shows a 6% annual “average” return rate and what stocks historically should return. Starting when returns are high has invariably poor outcomes.

The damage market declines inflict on investors hoping to garner annualized 8% returns to make up for the lack of savings is all too real and virtually impossible to recover from. When investors lose money in the market it is possible to regain the lost principal given enough time, however, what can never be recovered is the lost “time” between today and retirement. “Time” is finite and the most precious commodity that investors have.

Navigating The Next Cycle

We have previously detailed the basic guidelines for navigating market cycles.

- Investing is not a competition.

- Emotions have no place in investing.

- The ONLY investments you can “buy and hold” are those providing an income stream and return of principal.

- Market valuations are very poor market timing devices.

- Fundamentals and Economics drive long-term investment decisions – “Greed and Fear” drive short-term trading.

- “Market timing” is impossible– managing exposure to risk is both logical and possible.

- Investment is about discipline and patience.

- There is no value in daily media commentary– turn off the television and save yourself the mental capital.

- Investing is no different than gambling– both are “guesses” about future outcomes based on probabilities.

- No investment strategy works all the time.

Before sticking your head in the sand and ignoring market risk based on an article touting “long-term investing always wins, just ‘HODL'” ask yourself who benefits?

Emotions and investment decisions are very poor bedfellows. Unfortunately, most investors make emotional decisions because FEW follow a well-thought-out investment plan. Retail investors generally buy an off-the-shelf portfolio allocation model heavily weighted in equities. The illusion is that stocks will somehow make money over a long enough period.

Unfortunately, history has been a brutal teacher about the value of risk management.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read